Polyvinylidene Fluoride (PVDF) Coatings Market Size, Energy Transition Demand, and High-Durability Applications

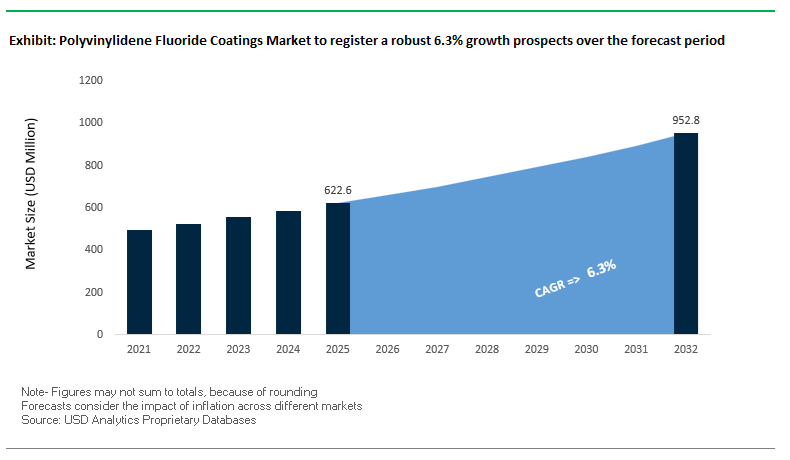

The global Polyvinylidene Fluoride (PVDF) Coatings Market was valued at $622.6 million in 2025 and is projected to grow at a CAGR of 6.3% through 2032, reaching $954.9 million by 2032. Growth is being driven by expanding applications in architectural coatings, lithium-ion batteries, semiconductor manufacturing, and high-performance industrial systems, where PVDF offers exceptional chemical resistance, UV stability, and long-term durability.

PVDF coatings are widely regarded as a premium fluoropolymer solution for environments requiring extreme weatherability, corrosion resistance, and color retention over multi-decade lifecycles. In architectural applications, PVDF-based coatings are extensively used for metal facades, roofing systems, and curtain walls, particularly in regions exposed to high UV radiation, humidity, and pollution.

A major structural growth driver is the rapid expansion of the energy transition ecosystem, particularly electric vehicles (EVs), battery manufacturing, and renewable infrastructure. PVDF plays a critical role as both a coating material and binder in lithium-ion batteries, contributing to electrode stability and long-term performance. Additionally, its use in semiconductor fabrication and high-purity fluid handling systems is increasing, driven by the need for materials that can withstand aggressive chemical environments.

The market is also being shaped by supply chain realignment and regulatory pressure related to PFAS (per- and polyfluoroalkyl substances). While PVDF remains a high-performance material, manufacturers are adapting to stricter environmental regulations and evolving customer expectations by investing in next-generation formulations and sustainable production processes.

Market Analysis: Capacity Expansion, Supply Chain Shifts, and Green Building Technologies Driving Market Evolution

Recent developments in the PVDF coatings market highlight a strong convergence of capacity expansion, supply chain restructuring, and sustainability-driven innovation. In March 2026, Arkema announced a 20% capacity expansion at its Changshu site in China, alongside progress on its Kentucky facility expansion, targeting growing demand for PVDF in battery, semiconductor, and architectural applications. These investments underscore the critical role of PVDF in the global energy transition and advanced manufacturing sectors.

The competitive landscape is being reshaped by supply chain disruptions. 3M’s exit from PVDF production (December 2025) has forced coating formulators to requalify alternative suppliers, accelerating market share gains for companies such as Arkema, Daikin, and Syensqo. This transition is creating short-term supply challenges but also opening opportunities for regional production and supplier diversification.

Strategic investments are aligning with regional growth opportunities. Daikin’s establishment of Daikin Chemical India (March 2026) strengthens its presence in South Asia, supporting demand from semiconductor fabrication and infrastructure projects, while Syensqo’s long-term contracts for battery-grade PVDF resins reinforce its leadership in the EV value chain.

Sustainability-driven product innovation is gaining traction in architectural applications. PPG’s DURANAR® PVDF coatings (September 2025) introduce enhanced solar reflectance (“cool roof”) properties, reducing building energy consumption while maintaining long-term color and gloss retention. Similarly, AkzoNobel’s integration of PVDF coatings into solar-absorbing wall technologies highlights the transition of coatings from passive protection to active energy management systems.

High-performance applications continue to expand into extreme environments. Syensqo’s involvement in the Artemis II mission demonstrates the capability of PVDF-based materials to withstand radiation exposure and thermal cycling, reinforcing their relevance in aerospace and advanced engineering sectors.

Market Trend: Waterborne PVDF Coatings Accelerating LEED v5 Compliance and Low-Emission Architectural Facades

The polyvinylidene fluoride coatings market is undergoing a strategic transition toward waterborne and high-solids PVDF systems as architectural manufacturers align with stringent sustainability frameworks, particularly LEED v5 certification requirements. This shift is being driven by the need to reduce embodied carbon, improve indoor air quality metrics, and meet ultra-low emission thresholds in large-scale infrastructure projects such as airports, commercial high-rises, and stadiums.

VOC reduction is a central performance benchmark. Advanced waterborne PVDF coatings now consistently achieve emission levels between 50 and 100 g/L, representing a reduction of up to 85% compared to traditional solventborne PVDF systems, which typically range from 350 to 450 g/L. This substantial emission compression enables compliance with the most restrictive environmental standards in North America and Europe.

Sustainability certification advantages are reinforcing adoption. Under LEED v5 Materials and Resources credits for low-emitting materials, coatings that approach or fall below the 50 g/L threshold qualify for maximum scoring potential. This is critical for developers targeting LEED Platinum certification, particularly in high-visibility public infrastructure where environmental credentials directly influence project approval and financing.

Energy efficiency performance further enhances value. PVDF coatings integrated with high-reflectivity pigments used in cool metal roofing systems can reflect up to 70% of incident solar radiation. This reduces peak cooling demand by approximately 10% to 30% in large buildings, contributing to lower operational energy consumption and improved thermal comfort.

Market Trend: PVDF Powder Coatings Advancing Zero-VOC Coil Coating and High-Efficiency Building Envelope Manufacturing

The coil coating segment is experiencing a technological shift toward PVDF powder coatings, driven by the need to eliminate solvent emissions and improve material utilization efficiency. This transition is particularly significant in pre-painted metal applications used in roofing, cladding, and facade systems.

Zero-VOC processing is a defining advantage. PVDF powder coatings operate as 100% solids systems, completely eliminating volatile organic compound emissions during application. This allows manufacturers to bypass capital-intensive emission control infrastructure such as thermal oxidizers and solvent recovery units, significantly reducing operational costs.

Material efficiency gains are substantial. Modern electrostatic powder application systems achieve transfer efficiencies between 95% and 98%, as overspray can be fully reclaimed and reused. This results in more than 20% reduction in material waste compared to conventional liquid coating methods, improving both cost efficiency and sustainability metrics.

Durability performance remains uncompromised. Powder-applied PVDF coatings maintain the industry-standard 70/30 resin composition, ensuring long-term resistance to UV degradation and chemical exposure. These coatings deliver over 20 years of color and gloss retention in high-UV environments while providing thicker film builds of 50 to 80 microns, compared to 20 to 25 microns typical of liquid PVDF systems. The increased film thickness enhances impact resistance and mechanical durability in demanding exterior applications.

Market Opportunity: California Rule 1113 Enforcement Creating High-Growth Market for Ultra-Low VOC PVDF Coatings

Regulatory developments in California are creating a strong growth pathway for advanced PVDF coating technologies, particularly under the revised Suggested Control Measure for architectural coatings. The tightening of VOC limits across multiple districts is significantly narrowing the compliance window for traditional solventborne PVDF systems.

The effective VOC cap for high-performance architectural coatings is being reduced toward 50 g/L in key regions such as those governed by the South Coast Air Quality Management District. This threshold effectively mandates the transition to waterborne or ultra-high-solids PVDF formulations for both factory and field-applied coatings.

This regulatory shift is generating a “forced innovation” cycle across the supply chain. Manufacturers capable of delivering compliant waterborne PVDF latex systems are gaining preferential specification in major construction projects, particularly those seeking alignment with green building standards.

The broader influence of California’s regulatory framework extends beyond the state. As the Suggested Control Measure serves as a reference model for other jurisdictions, including members of the Ozone Transport Commission, early compliance provides access to a wider North American market. This creates a competitive advantage for coating producers that can meet ultra-low VOC thresholds while maintaining the performance characteristics required for architectural applications.

Market Opportunity: China VOCs Phase 4 and GB/T 47088-2026 Driving High-Purity PVDF Adoption and Export Compliance

China’s evolving regulatory landscape is creating a large-scale opportunity for PVDF coatings, particularly through the implementation of the VOCs Phase 4 Action Plan and the GB/T 47088-2026 standard. These policies introduce stricter controls on both emissions and material purity, fundamentally reshaping the architectural and coil coating markets.

The GB/T 47088-2026 standard introduces advanced analytical requirements, including high-performance liquid chromatography methods for detecting extractable heavy metals in coating systems. This is forcing manufacturers to adopt high-purity PVDF resins and non-toxic pigment formulations to meet compliance thresholds, particularly for export-oriented production.

At the same time, the VOCs Phase 4 Action Plan mandates aggressive reductions in solvent emissions across industrial sectors. This is accelerating the transition toward waterborne and high-solids fluoropolymer coatings, with a targeted domestic adoption rate of 70% for low-emission technologies by 2030 under China’s industrial policy framework.

Export dynamics further amplify this opportunity. Compliance with low-VOC and non-toxic material standards is increasingly required to meet international trade regulations, including carbon-related tariffs such as the Carbon Border Adjustment Mechanism. Chinese manufacturers adopting compliant PVDF systems are better positioned to maintain competitiveness in global markets.

The combination of regulatory enforcement, industrial policy incentives, and export requirements is driving rapid expansion in demand for high-performance, environmentally compliant PVDF coatings across China’s manufacturing ecosystem.

PVDF Coatings Market Share and Segmentation Insights

By Product Type: Homopolymer PVDF Coatings Lead with Architectural Durability and High-Purity Applications

The homopolymer PVDF coatings segment dominated the market with a 68.4% share in 2025, driven by its exceptional performance in architectural coatings and high-purity industrial applications. Widely recognized under premium brands such as Kynar 500®, homopolymer PVDF has become the benchmark for metal building facades, roofing systems, and curtain wall coatings, offering over 30 years of weatherability, superior chalk resistance, and outstanding color retention. These properties make it the preferred choice for commercial construction, high-rise buildings, and infrastructure projects, where long-term aesthetic and structural performance is critical. Beyond construction, homopolymer PVDF is highly valued in semiconductor manufacturing, pharmaceutical processing, and ultra-pure water systems due to its low extractables, high chemical purity, and broad chemical resistance. This dual advantage of architectural durability and chemical stability continues to solidify its leadership in the global PVDF coatings market.

By Sales Channel: Direct Sales Channel Dominates with Custom Formulation and Certification Advantages

The direct sales segment accounted for a leading 55.9% share of the PVDF coatings market in 2025, reflecting the importance of close collaboration between resin manufacturers and end-use applicators. Major coil coating companies and spray applicators work directly with leading PVDF suppliers such as Arkema, Solvay, and Syensqo to develop customized resin formulations, including precise color matching, gloss control, and metallic finishes tailored for high-end architectural projects. This direct engagement ensures superior product consistency and innovation in fluoropolymer coatings technology. Additionally, large-scale construction projects require stringent quality certifications, mill test documentation, and long-term warranty registrations, such as 30-year Kynar warranties, which are more efficiently managed through direct supplier relationships. By enabling end-to-end quality assurance, regulatory compliance, and advanced coating customization, the direct sales channel continues to play a pivotal role in strengthening market penetration and customer trust in the PVDF coatings industry.

Competitive Landscape of the Polyvinylidene Fluoride (PVDF) Coatings Market

Arkema Leads PVDF Market with Kynar® Innovation and Global Capacity Expansion

Arkema S.A. is the undisputed global leader in the PVDF coatings market, driven by its flagship Kynar® brand. In 2026, the company announced a 20% capacity expansion at its Changshu facility in China to meet rising demand in EV batteries and industrial coatings. It also commissioned a new production line in Kentucky for semiconductor and water treatment applications. Arkema is prioritizing PFAS-free polymerization technologies to align with evolving global regulations. Its strong pricing power in specialty materials highlights its leadership in high-value PVDF resin technologies.

PPG Drives Architectural PVDF Coatings Leadership with Duranar® Systems

PPG Industries, Inc. is a leading applicator of PVDF-based coatings, particularly in architectural applications. Its Duranar® coatings are widely recognized as industry standards for high-rise buildings and infrastructure projects. The company has maintained steady organic growth and is investing in modular coating systems to improve project delivery timelines. PPG is also integrating PVDF coatings with advanced metallic pigments to create color-shifting finishes for EV exteriors. Its strong sustainability credentials, including low-VOC and chrome-free systems, reinforce its position as a leader in high-performance architectural coatings.

AkzoNobel Expands Global PVDF Footprint Through Strategic Merger and Portfolio Optimization

AkzoNobel N.V. is strengthening its position in the PVDF coatings market through its TRINAR® portfolio and strategic consolidation efforts. The proposed merger with Axalta is expected to create a global coatings powerhouse with extensive manufacturing and R&D capabilities. The company has improved operational efficiency through cost reductions, enabling resilience against PVDF raw material volatility. Its focus on cool-roof PVDF coatings supports urban heat island mitigation, while its divestment of non-core assets allows greater investment in high-margin performance coatings.

Solvay (Syensqo) Advances High-Purity PVDF Solutions for Semiconductor and Infrastructure Applications

Solvay, now operating alongside Syensqo, is a major player in the PVDF coatings market, particularly in high-purity and specialty applications. Its Solef® PVDF products are widely used in semiconductor manufacturing and architectural membranes. The company is investing in cost optimization and sustainability initiatives while expanding its PVDF research capabilities. Its innovations include self-cleaning hydrophilic coatings for large-scale infrastructure, reducing maintenance costs and improving durability. Solvay’s strong position in semiconductor-grade materials reinforces its leadership in high-performance fluoropolymer coatings.

Daikin Strengthens Vertical Integration with Sustainable PVDF Production Technologies

Daikin Industries, Ltd. is a key vertically integrated player in the PVDF coatings market, producing both raw fluorochemicals and finished coating resins. In 2026, the company invested over $300 million in advanced PFAS capture technologies, achieving near-total removal of emissions in production processes. Daikin is a leader in photovoltaic backsheet coatings, offering PVDF-based films with long-term weatherability for solar modules. Its global manufacturing footprint enables localized compliance with regional regulations, strengthening its position in sustainable fluoropolymer coatings.

Beckers Group Leads Sustainable Coil Coatings with Advanced PVDF Technologies

Beckers Group is a specialized leader in PVDF coil coatings, particularly in Europe and Asia. The company is investing in sustainable innovations, including renewable-sourced chemical components for high-performance coatings. Its new R&D center in Shanghai supports development of coatings for green building applications in China. Beckers is widely specified for large architectural projects requiring high-gloss, durable PVDF finishes with reduced carbon footprint. Its strong sustainability positioning and innovation focus reinforce its leadership in eco-friendly architectural coatings solutions.

China PVDF Coatings Market: Dual-Carbon Strategy and Battery Gigafactory Expansion

China dominates the global polyvinylidene fluoride (PVDF) coatings market, driven by its leadership in electric vehicle (EV) batteries, solar photovoltaics, and large-scale infrastructure development. Strategic expansions such as Arkema’s Changshu facility have significantly increased production capacity for battery-grade PVDF binders, supporting millions of EV batteries annually.

The enforcement of GB 30981.1-2025 is accelerating the transition toward waterborne PVDF dispersions, reducing VOC emissions in key industrial regions. Technological advancements include the development of flexible photovoltaic PVDF films with optimized moisture barrier properties, enhancing solar panel performance. Additionally, government incentives in regions like Hainan are promoting investments in smart-monitoring PVDF coating systems for coastal infrastructure, improving resistance to high salinity and environmental degradation.

United States PVDF Coatings Market: CHIPS Act Infrastructure and Domestic Content Growth

The U.S. PVDF coatings market is undergoing significant transformation, driven by semiconductor expansion, energy infrastructure, and regulatory shifts. The construction of advanced semiconductor fabs, such as the TSMC facility in Arizona, is boosting demand for PVDF-lined piping systems due to their resistance to aggressive chemicals and low outgassing properties.

Government initiatives like the Inflation Reduction Act (IRA) are strengthening domestic PVDF supply chains, encouraging local production of fluoropolymer materials. Environmental regulations under the EPA PFAS roadmap are also driving innovation in non-PFOA PVDF formulations, ensuring compliance while maintaining high-performance standards. Additionally, PVDF coatings are gaining traction in aerospace and infrastructure projects, including NASA contracts and long-life bridge coatings, highlighting the versatility and durability of these materials.

Japan PVDF Coatings Market: Hydrogen Infrastructure and 6G Precision

Japan continues to lead in high-precision PVDF coatings, particularly in applications related to hydrogen energy, semiconductors, and next-generation telecommunications. Government-backed initiatives are supporting the integration of PVDF-based membranes in fuel cell systems, improving durability and efficiency.

Innovations such as ULVAC’s ENTRON-EXX deposition system are enabling advanced coating processes for 2nm semiconductor fabrication, while Japanese telecom companies are deploying PVDF-based dielectric coatings for 6G signal reflection in urban environments. The country is also advancing in water treatment technologies, with PVDF membranes improving filtration efficiency and reducing plant footprints. Additionally, the use of PVDF-hybrid coatings in marine applications is enhancing performance and sustainability in high-speed vessels.

India PVDF Coatings Market: Semiconductor Growth and Urban Infrastructure Development

India is emerging as a high-growth market in the PVDF coatings industry, supported by government incentives, infrastructure expansion, and increasing domestic manufacturing capabilities. The launch of semiconductor-grade PVDF materials by Gujarat Fluorochemicals is strengthening India’s position in high-purity coating applications.

Government initiatives such as the PLI scheme for specialty chemicals are promoting domestic production of PVDF resins and reducing reliance on imports. Infrastructure projects, including railway modernization and urban development programs, are driving demand for durable, UV-resistant PVDF coatings in harsh environmental conditions. Additionally, the rapid growth of electronics manufacturing is increasing the adoption of PVDF conformal coatings to protect circuit boards from humidity, further expanding market opportunities.

Germany PVDF Coatings Market: Circular Economy and Hydrogen-Ready Barriers

Germany is a leader in the European PVDF coatings market, driven by sustainability, circular economy initiatives, and hydrogen infrastructure development. The country is pioneering high-density PVDF barrier coatings that significantly reduce hydrogen permeation, enabling the safe conversion of natural gas pipelines for hydrogen transport.

Innovations include the development of aqueous-based PVDF dispersions, reducing reliance on solvent-heavy systems, and the adoption of PFOA-free polymerization processes to meet strict EU REACH standards. Digital product passports are enhancing traceability and recyclability of coated materials, while investments in renewable energy infrastructure are increasing demand for high-performance PVDF coatings. Additionally, Germany’s automotive sector is driving growth in PVDF-based coatings for battery separators and lightweight components.

South Korea PVDF Coatings Market: Semiconductor Precision and Battery Innovation

South Korea’s PVDF coatings market is closely aligned with its leadership in semiconductors, OLED displays, and battery manufacturing. The expansion of semiconductor clusters is driving demand for plasma-resistant PVDF coatings used in cleanroom environments and advanced fabrication facilities.

Strategic investments are also focused on PVDF-based dielectric coatings for high-bandwidth memory (HBM) chips, supporting AI server growth. In the battery sector, South Korean manufacturers are diversifying PVDF supply chains to ensure resilience against raw material volatility. Additionally, the adoption of PVD-metallized PVDF coatings in cosmetic packaging and the integration of PVDF coatings in smart grid infrastructure highlight the material’s versatility across industries.

Saudi Arabia PVDF Coatings Market: Vision 2030 and Extreme Climate Applications

Saudi Arabia is emerging as a key market for high-performance PVDF coatings, driven by large-scale infrastructure projects under Vision 2030. Developments such as NEOM are mandating the use of high-resilience PVDF coatings for architectural facades, capable of withstanding extreme UV exposure and desert conditions.

The oil and gas sector is also a major driver, with PVDF coatings used for internal pipeline linings to improve efficiency and reduce energy consumption. Innovations in thermal management, including solar-reflective PVDF coatings, are helping reduce cooling loads in residential and commercial buildings. Localization initiatives under IKTVA are strengthening domestic production capabilities, while large-scale projects such as Jafurah are increasing demand for abrasion-resistant PVDF coatings. Additionally, PVDF-lined systems are being widely adopted in desalination infrastructure to enhance corrosion resistance and operational longevity.

Polyvinylidene Fluoride Coatings Market Report Scope

Polyvinylidene Fluoride Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$622.6 Million

|

|

Market Size (2032)

|

$954.9 Million

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Technology (Solvent-borne Coatings, Powder Coatings, Aqueous Dispersions), By Product (Homopolymer PVDF, Copolymer PVDF, Terpolymer PVDF), By Substrate Material (Metals, Polymers, Glass, Silicon Wafers, Battery Separator Films), By Application (Architectural Coatings, Li-ion Battery Coatings, Chemical Processing Equipment, Electrical and Electronics, Photovoltaic, Water Treatment Membranes, Energy Infrastructure), By End-Use Industry (Building and Construction, Automotive and Transportation, Electrical and Electronics, Chemical and Petrochemical, Renewable Energy, Aerospace and Defense, Pharmaceutical and Medical), By Functional Property (Weathering and UV Resistance, Chemical and Corrosion Resistance, High-Purity, Electrochemical Stability, Piezoelectric and Pyroelectric), By Sales Channel (Direct Sales, Specialty Fluoropolymer Distributors, Third-Party Contract Coaters)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Arkema S.A., Solvay S.A., PPG Industries, Inc., Akzo Nobel N.V., Daikin Industries, Ltd., The Sherwin-Williams Company, Kureha Corporation, AGC Inc., 3M Company, Dongyue Group Limited, Beckers Group, Axalta Coating Systems Ltd., Zhejiang Juhua Co., Ltd., KCC Corporation, Shanghai 3F New Materials Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polyvinylidene Fluoride Coatings Market Segmentation

By Technology

- Solvent-borne Coatings

- Powder Coatings

- Aqueous Dispersions

By Product

- Homopolymer PVDF

- Copolymer PVDF

- Terpolymer PVDF

By Substrate Material

- Metals

- Polymers

- Glass

- Silicon Wafers

- Battery Separator Films

By Application

- Architectural Coatings

- Li-ion Battery Coatings

- Chemical Processing Equipment

- Electrical and Electronics

- Photovoltaic

- Water Treatment Membranes

- Energy Infrastructure

By End-Use Industry

- Building and Construction

- Automotive and Transportation

- Electrical and Electronics

- Chemical and Petrochemical

- Renewable Energy

- Aerospace and Defense

- Pharmaceutical and Medical

By Functional Property

- Weathering and UV Resistance

- Chemical and Corrosion Resistance

- High-Purity

- Electrochemical Stability

- Piezoelectric and Pyroelectric

By Sales Channel

- Direct Sales

- Specialty Fluoropolymer Distributors

- Third-Party Contract Coaters

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Polyvinylidene Fluoride Coatings Industry

- Arkema S.A.

- Solvay S.A.

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Daikin Industries, Ltd.

- The Sherwin-Williams Company

- Kureha Corporation

- AGC Inc.

- 3M Company

- Dongyue Group Limited

- Beckers Group

- Axalta Coating Systems Ltd.

- Zhejiang Juhua Co., Ltd.

- KCC Corporation

- Shanghai 3F New Materials Co., Ltd.

*- List not Exhaustive