Porcelain Enamel Coatings Market Size, High-Temperature Applications, and Durable Surface Demand

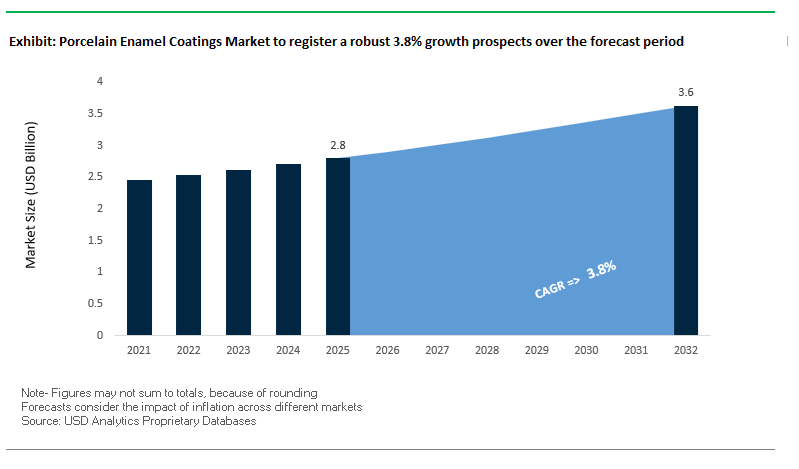

The global Porcelain Enamel Coatings Market was valued at $2.8 billion in 2025 and is projected to grow at a CAGR of 3.8% through 2032, reaching $3.6 billion by 2032. Growth is supported by steady demand across appliances, cookware, architectural panels, industrial equipment, and infrastructure, where porcelain enamel delivers exceptional heat resistance, chemical stability, and long-term durability.

Porcelain enamel coatings are inorganic, glass-like materials fused onto metal substrates at high temperatures, providing non-combustibility, corrosion resistance, scratch resistance, and color permanence. These properties make them indispensable in applications exposed to extreme heat, abrasive environments, and long lifecycle requirements, such as industrial ovens, transit infrastructure, and architectural façades.

A key structural driver is the increasing need for high-performance, fire-safe, and low-maintenance materials in public infrastructure and industrial systems. Compared to organic coatings, porcelain enamel offers decades-long service life without degradation, reducing lifecycle costs and aligning with sustainability goals focused on durability rather than frequent replacement.

The market is also benefiting from advancements in application technologies and formulation chemistry, including electrostatic deposition, digital printing, and low-temperature firing (LTF). These innovations are improving production efficiency, reducing energy consumption, and expanding the aesthetic capabilities of enamel coatings for modern architectural and consumer applications.

Market Analysis: Low-Temperature Firing Innovation, Renewable Energy Applications, and Digital Enamel Technologies Driving Market Evolution

Recent developments in the Porcelain Enamel Coatings Market highlight a convergence of process innovation, sustainability initiatives, and expanding application scope. The commercialization of Low-Temperature Firing (LTF) enamels in January 2026 represents a major breakthrough, reducing firing temperatures by 100°C. This innovation significantly lowers natural gas consumption and carbon emissions in industrial kilns, addressing one of the industry’s most energy-intensive processes.

High-performance product innovation continues to target demanding industrial applications. Vibrantz Technologies’ heat-resistant enamel series, rolled out globally through 2025, is engineered to withstand temperatures exceeding 600°C, supporting next-generation industrial ovens and professional cooking systems. In parallel, GlazeTech’s Visual-Prime coatings are targeting the premium appliance and cookware segment, combining enhanced scratch resistance with high-gloss aesthetics, reflecting growing consumer demand for durable yet visually refined surfaces.

Sustainability and manufacturing efficiency are central to recent strategic shifts. Investments highlighted by KPS Capital Partners emphasize the adoption of electrostatic and electrophoretic deposition technologies, which can reduce material waste by up to 25% in appliance manufacturing. Additionally, regulatory milestones such as EPA certification for North American facilities confirm the industry’s transition toward powder-based enamel systems, which offer lower VOC emissions compared to traditional processes.

The market is also expanding into renewable energy applications. Porcelain enamel coatings are increasingly used in solar thermal receivers and heat exchangers, where their ability to withstand extreme thermal cycling and oxidation provides a clear advantage over organic coatings. This positions enamel as a critical material in energy transition infrastructure.

Architectural innovation is further enhancing market potential. The introduction of direct-to-enamel digital printing technology enables photographic-quality designs on façade panels, offering long-lasting resistance to UV degradation and vandalism. Meanwhile, Hunan Noli Enamel’s production expansion (March 2026) supports growing demand for ready-to-use enamel powders in emerging markets, particularly in Southeast Asia and the Middle East.

Regulatory-driven demand is also shaping adoption. Infrastructure projects under Middle East “Vision 2030” initiatives are mandating the use of fire-rated, non-combustible enamel coatings for transit systems and tunnel linings, reinforcing the material’s role in safety-critical applications.

Market Trend: Low-Temperature Porcelain Enamel Firing Transforming Energy Efficiency and Steel Utilization in Appliance Manufacturing

A structural shift toward low-temperature porcelain enamel coatings in the 680–720°C range is redefining manufacturing economics across the home appliance coatings market, particularly in washing machines and dishwasher segments. This transition directly addresses industrial decarbonization targets while enabling compatibility with next-generation high-strength steel substrates. Compared to conventional enameling cycles operating at 820–850°C, low-temperature porcelain enamel systems reduce furnace energy consumption by 30% to 40%, significantly lowering energy intensity and CO₂ emissions per unit. This is becoming a critical KPI for OEMs aligning with ESG reporting frameworks and Scope 1 emission reduction targets.

Simultaneously, lower firing temperatures mitigate substrate distortion risks such as sagging and warping, allowing manufacturers to shift from traditional 1.2–1.5 mm steel to thinner 0.8–1.0 mm gauge steel. This substrate optimization strategy reduces raw material consumption by approximately 20–25%, directly improving cost competitiveness in price-sensitive appliance markets. The mechanical integrity of high-strength steel remains intact due to reduced thermal stress, enabling lightweight appliance design without compromising durability.

From a process efficiency standpoint, low-temperature frit formulations offer a wider firing window, enhancing operational flexibility in high-throughput automated enamel coating lines. Manufacturers are reporting up to a 15% reduction in scrap rates due to fewer firing defects, translating into improved yield and lower rework costs. These combined benefits position low-temperature porcelain enamel coatings as a core technology trend in sustainable appliance manufacturing and energy-efficient industrial coatings.

Market Trend: Electrostatic Dry Powder Porcelain Enamel Advancing Zero-Waste Coating and High-Performance Architectural Cladding

The adoption of electrostatic dry powder porcelain enamel coatings is accelerating within the architectural coatings and façade cladding market, particularly for curtain wall panels and high-rise building envelopes. This dry application technology eliminates the need for water-based or solvent-based slurry systems, addressing both environmental compliance and operational efficiency challenges in industrial coating processes.

Electrostatic dry powder systems achieve transfer efficiencies of 97–98%, significantly outperforming traditional wet spray methods. Overspray powder is fully recoverable and recyclable within the system, resulting in near-zero material waste and substantially improving coating material utilization rates. This aligns with circular manufacturing principles and waste minimization targets increasingly mandated in green building certifications and sustainable construction standards.

In addition, the precision of dry powder deposition enables a thinner and more uniform coating layer, delivering approximately 30% reduction in coating weight. This is a critical advantage in architectural engineering, where reducing dead-load on curtain wall assemblies enhances structural efficiency and lowers installation costs. The lightweight yet durable coating structure also supports long-term performance in high-rise applications exposed to extreme weather conditions.

Surface performance metrics further reinforce the value of electrostatic dry powder porcelain enamel. The elimination of defects such as tearing and slumping ensures superior surface uniformity and aesthetic consistency. Accelerated weathering tests indicate gloss retention exceeding 90% after 2,000 hours, highlighting the coating’s exceptional durability and UV resistance. These performance characteristics are positioning dry powder porcelain enamel coatings as a preferred solution in high-performance architectural coatings and sustainable façade systems.

Market Opportunity: US DOE Industrial Demonstrations Program Unlocking Capital for Low-Carbon Porcelain Enamel Manufacturing

The expansion of the U.S. Department of Energy Industrial Demonstrations Program presents a significant growth opportunity for porcelain enamel coatings manufacturers investing in low-carbon production technologies. As of April 2026, the program allocates $6.3 billion in funding through the Office of Clean Energy Demonstrations, targeting energy-intensive sectors such as steel processing and glass-to-metal bonding, both central to porcelain enamel production.

Porcelain enamel facilities implementing low-temperature enameling systems or transitioning to electric furnace technologies are eligible for cost-share grants covering up to 50% of capital expenditures. This level of financial support substantially reduces the payback period for decarbonization investments, enabling faster adoption of energy-efficient furnace systems and advanced enamel coating technologies. The availability of such funding is expected to accelerate capacity upgrades and technology retrofits across North American enamel coating plants.

In parallel, federal “Buy Clean” procurement policies are creating a premium demand environment for low-carbon building materials, including architectural porcelain enamel panels. Manufacturers that leverage DOE funding to validate reduced CO₂ emission profiles can gain preferential access to federally funded infrastructure projects. This is driving a shift toward carbon-labeled construction materials and creating a differentiated market segment for sustainable porcelain enamel coatings, particularly in public infrastructure and institutional building projects.

Market Opportunity: China VOCs Phase 4 Policy Accelerating Shift Toward Zero-VOC Porcelain Enamel in Industrial Coatings

The implementation of the VOCs Phase 4 Action Plan by the Ministry of Ecology and Environment for the 2026–2030 period is catalyzing a major transition toward inorganic and zero-VOC coating technologies in China’s manufacturing sector. This regulatory framework imposes stringent VOC emission limits, often below 50 g/L, placing significant compliance pressure on solvent-based coatings and organic finishes.

Porcelain enamel coatings, being inherently 100% inorganic and glass-based, are uniquely positioned to benefit from this regulatory shift. Unlike conventional coatings, porcelain enamel does not emit volatile organic compounds, allowing manufacturers to fully comply with evolving environmental standards without requiring additional abatement systems. This creates a strong competitive advantage in industries such as appliances, cookware, and architectural panels.

The policy also introduces a “High-Quality Development” incentive structure that prioritizes clean production technologies. In the white goods sector, provincial authorities are enforcing mandatory clean production audits starting in late 2026. Facilities utilizing porcelain enamel coatings are increasingly being designated as “Green Factories,” a status that provides exemptions from seasonal production restrictions typically imposed during high-pollution periods.

This regulatory-driven demand is expected to accelerate the replacement of organic coatings with porcelain enamel across China’s industrial coatings market. The combination of compliance benefits, operational continuity, and environmental certification is creating a substantial growth opportunity for global and domestic manufacturers specializing in zero-VOC porcelain enamel coatings.

China Porcelain Enamel Coatings Market: Capacity Expansion and Low-Carbon Innovation

China leads the global porcelain enamel coatings market, supported by large-scale appliance manufacturing, infrastructure development, and sustainability initiatives under the “Dual-Carbon” strategy. The commissioning of advanced facilities, such as Midea’s smart enameling factory, is improving efficiency through electrostatic powder application, reducing waste while enhancing coating uniformity.

Technological advancements include the development of low-temperature firing frits (<800°C), enabling thinner steel usage and lowering carbon emissions in water heater production. Regulatory compliance with GB 4806.10-2025 is accelerating the adoption of nickel-free and cobalt-free enamels, particularly for export-grade cookware. Additionally, large infrastructure projects like the Guangzhou Metro expansion are driving demand for enamel cladding panels due to their durability and long-term color stability. Innovations in solar thermal coatings and government incentives for upgrading small-scale facilities further strengthen China’s leadership in sustainable enamel technologies.

Porcelain Enamel Coatings Market Share and Segmentation Insights

By Form: Frit (Powder) Segment Leads with Versatility and Material Engineering Advantages

The frit (powder) segment dominated the porcelain enamel coatings market with a 68.1% share in 2025, driven by its role as the core raw material in glass-ceramic coating systems. Frit is produced by fusing and rapidly quenching mineral-based raw materials, then ground into fine powder, which enamelers further process into liquid slips or electrostatic powder coatings for diverse applications. Its importance lies in its high versatility as an intermediate material, enabling tailored formulations for different substrates such as steel, cast iron, and aluminum, with controlled coefficients of thermal expansion. Additionally, frit-based enamel coatings can be engineered for functional properties including acid resistance, antibacterial performance, and electrical insulation, making them essential in appliances, sanitary ware, and industrial components. This adaptability, combined with consistent quality and scalability, reinforces frit’s dominance in the global porcelain enamel coatings market.

By Distribution Channel: Direct Sales Channel Dominates with Customization and High-Volume Supply Contracts

The direct sales segment accounted for a leading 62.3% share of the porcelain enamel coatings market in 2025, reflecting the importance of technical collaboration and bulk procurement efficiency. Major end users, including appliance manufacturers, architectural panel producers, and sanitary ware companies, rely on direct partnerships with frit manufacturers to develop custom formulations tailored to firing curves, opacity levels, color consistency, and chemical resistance requirements. These collaborations are critical for ensuring optimal performance in high-temperature enamel applications. Furthermore, porcelain enamel frit is typically purchased in large tonnage volumes, supporting continuous production lines for products such as washing machine drums, ovens, bathtubs, and industrial tanks. Direct sales agreements enable competitive pricing, batch-to-batch consistency, and just-in-time delivery, minimizing production disruptions. This strong alignment between manufacturers and end users continues to drive the dominance of the direct sales channel in the global porcelain enamel coatings market.

Competitive Landscape of the Porcelain Enamel Coatings Market

Vibrantz Technologies Leads Market Transformation with Digital Enamel and Safety Innovations

Vibrantz Technologies has emerged as the global leader in the porcelain enamel coatings market, following the consolidation of Ferro and Prince International. In 2026, the company spearheaded the transition toward nickel-free and low-quartz enamel coatings, aligning with stringent EU safety regulations. Its VitroInx digital inkjet technology enables high-definition, multi-color designs to be directly applied to substrates, disrupting traditional screen-printing methods. Vibrantz coatings demonstrate exceptional durability, withstanding temperatures up to 450°C and achieving high hardness ratings. The company is also investing in BIPV applications, using ceramic inks to integrate aesthetic finishes into solar modules.

AkzoNobel Strengthens Industrial Enamel Leadership with Sustainable Powder Coatings

AkzoNobel N.V. is a dominant player in the porcelain enamel coatings market, particularly in high-performance powder coatings. The company holds a leading share in the porcelain sector, driven by its eco-friendly, zero-VOC formulations and efficient application processes. In 2026, AkzoNobel continued to optimize its portfolio by reallocating capital toward industrial enamel production in Asia. Its integration of AI-driven color matching technologies ensures precise and consistent finishes across complex appliance components. The company’s potential merger with Axalta further strengthens its global supply chain and innovation capabilities in industrial enamel coatings.

PEMCO Drives Specialized Enamel Innovation for Water Heating and Industrial Applications

PEMCO International is a specialized leader in the porcelain enamel coatings market, focusing on technical innovation for water heaters and boilers. Its Vitromail series is designed for energy-efficient hot water systems, offering enhanced thermal stability and resistance to corrosion. PEMCO’s expertise in thermal expansion control and milling additives ensures superior performance in challenging environments, such as softened water systems. The company’s active participation in global industry forums and expansion into emerging markets strengthens its position in high-performance industrial enamel solutions.

A.O. Smith Leverages Vertical Integration with Advanced Glass-Lining Technologies

A.O. Smith Corporation holds a unique position in the porcelain enamel coatings market due to its vertical integration and proprietary technologies. Its Blue Diamond® glass-lining system offers superior corrosion resistance compared to conventional enamels, particularly in water heating applications. The company utilizes advanced electrostatic powder coating systems to achieve uniform coverage on complex tank geometries. Its focus on thermal compatibility between enamel and steel substrates ensures long-term durability under extreme conditions. A.O. Smith is also investing in next-generation systems for heat pump water heaters, reinforcing its leadership in integrated enamel solutions.

PPG Enhances Market Position with Energy-Efficient and High-Durability Enamel Coatings

PPG Industries, Inc. is a key player in the porcelain enamel coatings market, focusing on high-performance and energy-efficient solutions. The company has developed low-temperature firing enamels that reduce energy consumption during production by 15%, aligning with sustainability goals. PPG is also strengthening its supply chain resilience to address raw material volatility. Its coatings are widely used in architectural panels and infrastructure projects, offering UV stability and graffiti resistance. These innovations position PPG as a leader in durable and environmentally efficient enamel coatings.

Altana Strengthens Industry Backbone with Advanced Additives and Functional Enhancements

Altana AG, through its BYK and ECKART divisions, plays a critical role in the porcelain enamel coatings market by supplying high-performance additives and pigments. Its products enhance coating properties such as viscosity control, particle distribution, and color intensity, which are essential for automated manufacturing processes. In 2026, Altana introduced silver-ion antimicrobial additives, targeting healthcare and food preparation applications. Its localized technical centers in China support regional manufacturers in optimizing production processes. Altana’s expertise in formulation stability and functional additives reinforces its position as a key enabler of next-generation enamel coating technologies.

United States Porcelain Enamel Coatings Market: Re-Industrialization and High-Purity Applications

The U.S. porcelain enamel coatings market is undergoing a transformation driven by domestic manufacturing expansion, infrastructure investments, and stringent regulatory standards. Tariff-driven policies have encouraged local production of enamel frit, strengthening supply chain resilience.

The growing biotech sector is increasing demand for glass-lined steel reactors with high-purity enamel coatings, ensuring contamination-free processing. New DOE energy standards are boosting the use of high-silica enamel linings in water heaters for improved corrosion resistance. Additionally, infrastructure funding is driving adoption of acid-resistant enamel coatings in wastewater treatment systems. The transition to electrostatic powder enameling is also improving environmental performance by eliminating liquid waste streams, while AI-driven inspection systems are enhancing quality control in modern enameling facilities.

Turkey Porcelain Enamel Coatings Market: Export Hub and Antimicrobial Innovation

Turkey has emerged as a major porcelain enamel coatings export hub, supplying frit and finished components across Europe, the Middle East, and Africa. The country’s strong manufacturing base and strategic geographic position support its leadership in the global supply chain.

Innovations such as the Neo-Glass antimicrobial enamel series are enhancing hygiene in sanitary and medical applications, achieving significant bacterial reduction. Turkish manufacturers are also advancing PVD-hybrid enamel coatings, enabling metallic finishes that rival stainless steel aesthetics. Growth in infrastructure and transportation projects is further driving demand for enamel-coated components, while alignment with EU REACH standards is strengthening Turkey’s position as a reliable supplier to European markets.

Germany Porcelain Enamel Coatings Market: Engineering Excellence and Circular Economy Leadership

Germany is at the forefront of high-performance porcelain enamel coatings, focusing on sustainability, energy efficiency, and advanced industrial applications. The introduction of hydrophilic enamel coatings for flue-gas systems is improving thermal efficiency in industrial operations, while innovations such as self-stratifying primers are reducing energy consumption during production.

The adoption of Blue Angel eco-label standards is encouraging the use of fully recyclable enamel coatings, supporting circular economy goals. Germany is also leading in digital printing on enamel surfaces, enabling long-lasting architectural designs with high visual quality. Advanced recycling technologies are achieving near-zero waste in enameling processes, while applications in renewable energy infrastructure and automotive components continue to expand the market.

India Porcelain Enamel Coatings Market: Smart Cities and Railway Modernization

India is one of the fastest-growing markets for porcelain enamel coatings, driven by infrastructure development, government initiatives, and rising demand for durable materials. Railway modernization projects, including the Vande Bharat and Amrit Bharat trains, are driving the adoption of enamel-coated steel panels for interior applications due to their fire safety and ease of maintenance.

The Smart Cities Mission is further boosting demand for enamel-coated signage and public infrastructure components that can withstand harsh environmental conditions. Government support through PLI schemes is encouraging domestic production of enamel materials, while partnerships with steel manufacturers are enabling the use of pre-enameled steel coils in construction. Additionally, growth in sanitary ware and power sector applications is expanding the market, reinforcing India’s position as a key growth region.

Brazil Porcelain Enamel Coatings Market: Appliance Growth and Bio-Based Integration

Brazil is a key market in the porcelain enamel coatings industry, driven by strong demand from the appliance sector and a growing focus on sustainable manufacturing practices. Investments such as Whirlpool’s expansion in Joinville are increasing production capacity for enameled appliance components, including washing machine drums and oven cavities.

The country is also integrating bio-based solvents derived from sugarcane into enameling processes, aligning with national green chemistry goals. Demand for enamel-coated cookware is rising due to its non-toxic properties, while infrastructure projects are increasing the use of enamel-lined pipes for corrosion resistance. Additionally, government housing initiatives are supporting the adoption of enamel-lined solar water heaters, further driving market growth.

Japan Porcelain Enamel Coatings Market: Precision Engineering and Advanced Functional Coatings

Japan remains a global leader in high-precision porcelain enamel coatings, particularly in applications intersecting with advanced electronics, healthcare, and telecommunications. Innovations such as Ultra-Clean enamel coatings are enabling air purification by capturing VOCs in commercial environments.

The country is also exploring enamel-based substrates for 6G signal reflection, leveraging their dielectric stability for next-generation communication systems. In healthcare, biocompatible enamel coatings are being developed for medical devices, while advancements in optical applications are supporting AR/VR device manufacturing. Updated standards such as JIS R 4201:2024 are enhancing global competitiveness, while new safety regulations are driving the use of enamel coatings in hydrogen-powered marine systems. These developments reinforce Japan’s leadership in advanced functional enamel technologies.

Porcelain Enamel Coatings Market Report Scope

Porcelain Enamel Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.8 Billion

|

|

Market Size (2032)

|

$3.6 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Product (Acid-Resistant Enamel, High-Temperature Enamel, Antibacterial, Decorative and Gloss Enamel, Single-Coat Enamel, Multi-Coat Enamel), By Form (Frit, Powder, Liquid), By Substrate Material (Steel, Cast Iron, Aluminum, Copper and Precious Metals), By Application Technique (Spraying, Dipping and Flow Coating, Roll Coating, Electrophoretic Deposition), By End-Use Industry (Home Appliances, Cookware and Kitchenware, Building and Construction, Industrial and Chemical, Healthcare and Laboratory), By Functional Property (Corrosion and Chemical Resistance, Thermal Shock and Heat Resistance, Abrasion and Scratch Resistance, Aesthetic, Hygienic), By Distribution Channel (Direct Sales, Specialty Distributors and Dealers, Online B2B Marketplaces)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Vibrantz Technologies, Colorobbia S.p.A., Akcoat, A. O. Smith Corporation, Pemco International, Hunan Noli Enamel Co., Ltd., Tomatec Co., Ltd., Hae Kwang Co., Ltd., Keskin Kimya, Sinopigment and Enamel Chemicals Ltd., GWIPPO Co., Ltd., Wendel Email GmbH, Roesch Inc., Keystone Corporation, Meitner GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Porcelain Enamel Coatings Market Segmentation

By Product

- Acid-Resistant Enamel

- High-Temperature Enamel

- Antibacterial

- Decorative and Gloss Enamel

- Single-Coat Enamel

- Multi-Coat Enamel

By Form

By Substrate Material

- Steel

- Cast Iron

- Aluminum

- Copper and Precious Metals

By Application Technique

- Spraying

- Dipping and Flow Coating

- Roll Coating

- Electrophoretic Deposition

By End-Use Industry

- Home Appliances

- Cookware and Kitchenware

- Building and Construction

- Industrial and Chemical

- Healthcare and Laboratory

By Functional Property

- Corrosion and Chemical Resistance

- Thermal Shock and Heat Resistance

- Abrasion and Scratch Resistance

- Aesthetic

- Hygienic

By Distribution Channel

- Direct Sales

- Specialty Distributors and Dealers

- Online B2B Marketplaces

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Porcelain Enamel Coatings Industry

- Vibrantz Technologies

- Colorobbia S.p.A.

- Akcoat

- O. Smith Corporation

- Pemco International

- Hunan Noli Enamel Co., Ltd.

- Tomatec Co., Ltd.

- Hae Kwang Co., Ltd.

- Keskin Kimya

- Sinopigment & Enamel Chemicals

- GWIPPO

- Wendel Email

- Roesch Inc.

- Keystone Corporation

- Meitner GMBH

*- List not Exhaustive