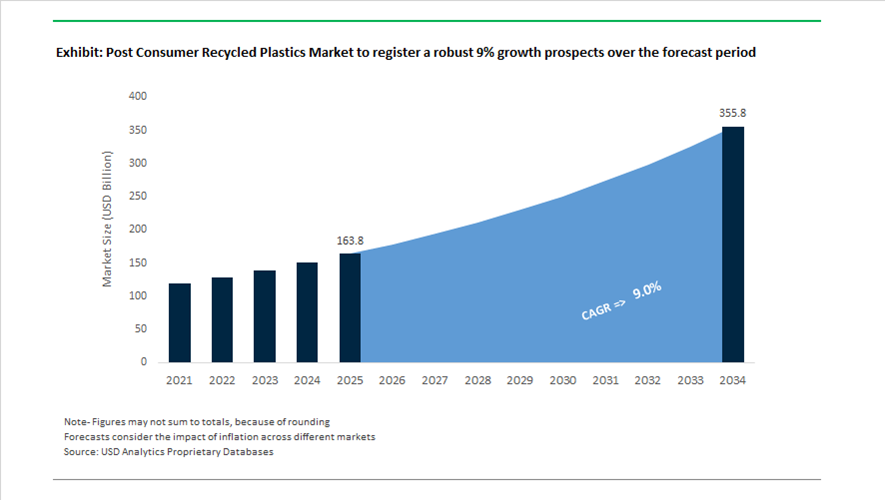

Post-Consumer Recycled Plastics Market Valued at $163.8 Billion in 2025, Projected to Reach $355.8 Billion by 2034 at 9% CAGR

The global post consumer recycled plastics market is valued at $163.8 billion in 2025 and is forecast to reach $355.8 billion by 2034, expanding at a robust CAGR of 9%. Growth is being driven by regulatory mandates on recycled content, brand owner commitments to virgin plastic reduction, and rapid advancements in mechanical and solvent-based recycling technologies. Demand spans PCR polyethylene (PE), recycled PET (rPET), recycled polypropylene (rPP), recycled LDPE films, and high-purity PCR resins across packaging, consumer goods, cables, telecommunications, and healthcare applications. Infrastructure investments in advanced sorting and purification systems are materially increasing the availability of food- and pharma-grade recycled polymers.

In January 2024, Republic Services opened its Next-Gen Salt River recycling facility in the United States. The 51,000-square-foot center uses advanced optical sorting systems capable of processing 40 tons of recyclables per hour, significantly expanding domestic output of high-purity PCR flakes. In the same month, TekniPlex Healthcare and Alpek Polyester launched the first pharmaceutical-grade PET blister film containing 30% PCR content, representing a major regulatory breakthrough for medical packaging. In April 2024, Amcor introduced a one-liter carbonated soft drink bottle made entirely from 100% post-consumer recycled PET, overcoming pressure-containment challenges historically associated with high recycled content. In September 2024, Dow launched REVOLOOP™ recycled plastic resins for cable jacketing, marking a strategic shift of PCR materials into energy and telecommunications infrastructure beyond traditional packaging. In October 2024, LyondellBasell acquired full ownership of Germany-based APK AG, securing its solvent-based recycling technology capable of producing high-purity LDPE from complex flexible waste streams. That same month, SCGC introduced 100% recycled plastic skincare packaging under its Green Polymer platform in ASEAN markets.

Corporate sustainability commitments intensified in 2025. In January 2025, Mondelēz International announced that 80% of its Cadbury sharing bars in the UK and Ireland would transition to packaging containing 600 tonnes of certified PCR plastic annually. In early 2025, Unilever revised its sustainability roadmap, targeting a one-third reduction in virgin plastic by 2026, having already achieved 21% PCR usage across its global portfolio by 2024. In April 2025, the Indian government mandated defined recycled plastic content levels across FMCG, retail, and e-commerce packaging, triggering substantial investment in domestic recycling capacity and driving demand for compliant PCR resin grades. Berry Global reported a 36% year-on-year increase in PCR polyethylene usage across its European operations between late 2024 and 2025, reflecting internal alignment with brand-driven circularity requirements.

Material innovation and cross-sector R&D integration are also influencing the competitive landscape. Following the $1.8 billion combination of Tate & Lyle and CP Kelco in late 2024, the group expanded research into bio-based texturants paired with recycled resins to improve tactile properties and surface aesthetics of sustainable packaging. The post consumer recycled plastics market is increasingly defined by advanced optical sorting facilities, solvent-based flexible plastic recycling, food-grade and pharma-grade rPET production, PCR cable compounds, mandatory recycled content regulations, and brand-level virgin plastic reduction targets. Regulatory enforcement, consumer-facing sustainability commitments, and technology-driven purification advancements are accelerating the transition from linear to circular polymer value chains across global packaging and infrastructure sectors.

Trends and Opportunities in the Post-Consumer Recycled (PCR) Plastics Market

Mandated Demand Creation through Legislation and Extended Producer Responsibility Frameworks

The Post-Consumer Recycled plastics market has entered a structurally different phase where demand is no longer driven by voluntary sustainability commitments alone but is increasingly anchored in enforceable legislation. Across Europe and key U.S. states, minimum recycled content mandates are effectively establishing a non-negotiable demand baseline for PCR resins, transforming them into a prerequisite for market participation rather than a cost-sensitive alternative to virgin plastics.

The formal publication of the EU Packaging and Packaging Waste Regulation in January 2025 represents one of the most consequential policy interventions in the global plastics value chain. Under PPWR, all plastic packaging placed on the EU market must contain a defined share of recycled content by 2030, including 30% for PET contact-sensitive packaging and 10% for non-PET contact-sensitive plastics. These thresholds rise sharply by 2040 to 50% and 25% respectively, creating a multi-decade visibility window for PCR demand growth. For brand owners and converters, compliance is binary. Failure to integrate PCR into packaging structures directly limits access to the European consumer market.

In the United States, California’s SB 54 is playing a similarly catalytic role. The initiation of formal rulemaking by CalRecycle in August 2025 marked the operational phase of the most ambitious Extended Producer Responsibility framework in North America. The law mandates that by 2032, all packaging sold in California must be recyclable or compostable, while total plastic packaging weight must be reduced by 25%. The designation of the Circular Action Alliance as the state’s first Producer Responsibility Organization formalizes a projected USD 5 billion, industry-funded recycling system overhaul. Together, these regulatory mechanisms are institutionalizing PCR demand, insulating it from short-term resin price volatility and anchoring long-term offtake commitments across consumer goods, retail, and food packaging sectors.

Brand-Backed Strategic Investment in Advanced Recycling Capacity

As regulatory pressure intensifies, leading consumer packaged goods companies are fundamentally changing how they secure PCR feedstock. Rather than relying on spot-market procurement of mechanically recycled material, brands are increasingly deploying capital directly into advanced recycling technologies to secure long-term access to high-quality recycled polymers.

Between late 2024 and 2025, more than 80 global brand owners, including multinational food, beverage, and home care companies, publicly reaffirmed recycled-content targets ranging from 15% to 50% by 2025 to 2030. Meeting these commitments at scale is not feasible through mechanical recycling alone, particularly for food-grade and multilayer packaging. As a result, the advanced recycling segment encompassing pyrolysis-based conversion and monomer-level decomposition is projected to require cumulative investments exceeding USD 40 billion to reach 20 to 40 million metric tons of annual capacity by 2030.

Strategic partnerships and equity participation are becoming the dominant investment model. In March 2025, Unilever emphasized circular supply chain partnerships within its Growth Action Plan 2030, highlighting long-term offtake agreements that de-risk capital-intensive chemical recycling facilities. These arrangements provide technology providers with predictable revenue streams while granting brand owners preferential access to recycled feedstocks that meet both regulatory and performance requirements. This vertical alignment is accelerating project financing timelines and shifting advanced recycling from pilot-scale experimentation toward bankable industrial infrastructure.

Supply of Food-Grade PCR Resins for Contact-Sensitive Packaging

Food-contact PCR represents the highest value segment within the Post-Consumer Recycled plastics market due to its stringent purity requirements and limited qualified supply. Achieving regulatory approval from food safety authorities requires advanced decontamination or molecular-level recycling processes capable of removing inks, additives, odors, and legacy contaminants from post-consumer waste streams.

A major inflection point occurred in September 2025 when the U.S. Food and Drug Administration issued a Letter of No Objection to the NextLooPP project, authorizing the use of 100% recycled polypropylene in food-contact applications. This approval significantly expands the addressable PCR feedstock universe, as polypropylene represents one of the largest and most underutilized fractions of municipal plastic waste. Food-grade rPP can now be deployed in applications ranging from frozen food containers to high-temperature heat sterilization, unlocking substantial price premiums relative to non-food PCR grades.

Commercial validation has further strengthened confidence in advanced recycling routes. In November 2025, PureCycle Technologies received the U.S. Plastics Pact Sustainable Packaging Innovation Award for its Run It Back product line, which uses dissolution recycling to produce PureFive resin with 100% recycled content suitable for food-contact cups. The success of these technologies demonstrates that chemical purity, regulatory compliance, and commercial-scale output can coexist, positioning food-grade PCR as one of the most strategically attractive investment opportunities in the circular plastics economy.

High-Performance PCR Compounds for Automotive and Electronics Applications

Beyond packaging, durable goods represent a structurally important growth vector for PCR plastics. Automotive and electronics manufacturers are increasingly integrating recycled polymers into high-performance components, driven by carbon footprint reduction targets, supply chain resilience, and evolving procurement standards that prioritize recycled content.

By early 2025, global automotive OEMs had begun embedding recycled-material thresholds into supplier qualification frameworks, particularly for interior components, underbody panels, and battery housings in electric vehicles. Companies such as Mercedes-Benz and BMW are advancing circularity strategies aligned with software-defined vehicle platforms, where sustainability metrics now influence material selection alongside weight, safety, and thermal performance. In October 2025, Mercedes confirmed that its upcoming Little G and C-Class EQ platforms would incorporate advanced recycled polymers as part of broader carbon-neutral manufacturing objectives.

Parallel investment is underway in recycling infrastructure capable of producing consistent, high-specification PCR pellets for durable applications. In December 2025, Circulate Capital announced a strategic investment in See Hau Global to triple its production capacity for high-quality recycled polyolefins used in heavy-duty pallets and industrial goods. These applications offer longer product lifecycles than single-use packaging, improving the overall carbon efficiency of PCR utilization and supporting the economic case for higher-cost recycling technologies.

Post Consumer Recycled Plastics Market Share and Segmentation Insights

Recycled PET Leads Post Consumer Recycled Plastics Market with Established Bottle-to-Bottle Recycling Infrastructure

Polyethylene terephthalate accounted for 42.80% of the Post Consumer Recycled Plastics Market by polymer type in 2025, reflecting the strong global recycling infrastructure built around PET beverage bottles. Bottle collection systems, mechanical recycling technologies, and bottle to bottle processing have enabled the production of food grade recycled PET suitable for beverage containers and food packaging. Major consumer brands and packaging manufacturers have committed to incorporating higher recycled content in plastic packaging, which continues to increase demand for rPET materials worldwide. In 2025, expansion of food grade rPET recycling capacity has accelerated, supported by regulatory mandates such as the EU Single Use Plastics Directive and recycled content requirements in North America, with advanced sorting and decontamination technologies improving recyclate quality for thermoformed packaging applications.

Packaging Industry Dominates PCR Plastics Consumption Across Beverage, Food, and Consumer Packaging Applications

Packaging represented 58.60% of the Post Consumer Recycled Plastics Market by end-use industry in 2025, supported by the large volume of plastic packaging generated in global consumer markets. Beverage bottles, food containers, rigid packaging, and flexible packaging formats represent the most significant sources and end markets for post consumer recycled plastics. Increasing regulatory pressure and corporate sustainability commitments have accelerated the incorporation of PCR materials into new packaging products across multiple industries. In 2025, regulatory approvals for food contact recycled plastics have expanded packaging applications, enabling recycled PET and other recycled polymers to be used in thermoformed trays, clamshell containers, and food packaging films through improved mechanical and advanced recycling technologies.

Post-Consumer Recycled Plastics Market Competitive Landscape

The global post-consumer recycled (PCR) plastics market in 2026 is defined by carbon footprint verification, food-grade resin production, and regulatory compliance with PPWR mandates. Industry leaders are investing in closed-loop recycling, AI-enabled sorting, and integrated polymer centers to deliver high-purity PCR plastics with superior traceability and lifecycle sustainability.

Veolia Scales Closed-Loop Recycling Infrastructure with GreenUp Strategy and Municipal Feedstock Control

Veolia is strengthening its leadership in the PCR plastics market through its GreenUp (2024–2027) strategy, focusing on high-margin circular polymer production and hazardous waste integration. The company reported €44.4 billion in 2025 revenue and is targeting 5%–6% EBITDA growth in 2026, supported by the €2.6 billion Clean Earth acquisition. Its £70 million UK investment in closed-loop recycling infrastructure is part of a broader £1 billion plan to scale advanced polymer recovery systems by 2030. Veolia’s dominance in municipal contracts, exceeding £1 billion in 2025, ensures a consistent supply of post-consumer feedstock for high-purity recycling. The company is also integrating decarbonization initiatives such as Vehicle-to-Grid (V2G) technology, reinforcing its position in sustainable waste-to-resource ecosystems. Its vertically integrated model enhances traceability, carbon reduction, and compliance with global recycling mandates.

Indorama Ventures Drives Global rPET Leadership with Vertical Integration and Single Pellet Technology

Indorama Ventures remains the global leader in PET recycling, having processed over 150 billion post-consumer bottles since 2011. The company reported THB 467.3 billion ($14.95 billion) in 2025 revenue while focusing on margin recovery and deleveraging strategies through 2026. Its target to reach 1.5 million tons of PCR input capacity by 2030 underscores its scale advantage in the recycled plastics market. Indorama’s proprietary single pellet technology enables seamless integration of recycled flakes into virgin polymer streams, ensuring consistent food-grade resin quality. Its global Sustainable Solutions network supports localized supply chains for major FMCG brands, enhancing circular packaging adoption. The company’s “Zero Plastic Waste to Nature” initiative aligns with regulatory pressures and ESG-driven procurement trends across global markets.

Republic Services Advances Polymer Center Model with Verified Low-Carbon rPET and Integrated Recycling

Republic Services is redefining the PCR plastics value chain by moving upstream into high-value polymer processing through its Polymer Center strategy. Its ISO-compliant Product Carbon Footprint study confirmed that rPET flake from its Las Vegas facility delivers an 82% lower carbon footprint than virgin PET. The company is expanding its infrastructure with facilities in Las Vegas, Indianapolis, and Allentown, each capable of processing 120 million pounds annually. Through its Blue Polymers joint venture, Republic produces high-quality PCR HDPE and PP resins with full traceability from curbside collection to final output. This integrated approach enhances supply chain transparency and supports brand owners seeking verified sustainable materials. Its focus on bottle-to-bottle circularity maximizes recovery rates and reduces landfill dependency.

Biffa Strengthens UK Recycling Leadership with Policy Advocacy and High-Capacity MRF Infrastructure

Biffa is reinforcing its position as a leading UK recycler by combining large-scale infrastructure with proactive regulatory engagement. The company holds approximately 20% market share in UK plastic recycling, supported by its Edmonton Materials Recovery Facility, one of the largest in the country. Its £830 million refinancing in 2025 improves financial flexibility, with EBITDA margins projected to exceed 12.5% in 2026. Biffa’s “Reality Check 2025” report highlights its role in shaping national recycling policy, advocating for stricter controls on unverifiable PCR imports. The company operates across the full waste value chain, from collection to advanced polymer processing, enabling efficient circular economy integration. Its capabilities in converting waste films into industrial-grade resins support demand for high-performance recycled plastics.

Alpek Optimizes Polyester Recycling Portfolio Through Capacity Rationalization and Specialty Focus

Alpek is navigating challenging market conditions by rationalizing its recycling footprint and prioritizing high-value polyester applications. The company suspended operations at its California facility in 2026 to consolidate production at its more competitive Indiana site, improving cost efficiency. Despite margin pressures, Alpek expects volume growth in its polyester segment and is targeting EBITDA expansion in its emerging specialty businesses. Its expertise in advanced PET sheet and thermoform packaging enables differentiation in high-recycled-content applications. The company is adopting a capital-light strategy to preserve free cash flow while maintaining competitiveness in the recycled plastics market. With decades of operational resilience, Alpek continues to align its portfolio with evolving sustainability and circular packaging demands.

Suez Accelerates Digital Recycling with AI Sorting and Closed-Loop Water Systems for PCR Optimization

Suez is positioning itself as a digital-first leader in the PCR plastics industry by integrating AI and advanced sorting technologies into its operations. Investments in Near-Infrared (NIR) systems and AI-enabled sorting are expected to improve recycling yields by up to 15% compared to 2019 benchmarks. The company focuses on producing high-quality recycled HDPE for automotive and construction applications, expanding beyond traditional packaging markets. Its closed-loop recycling systems provide municipalities with detailed lifecycle analysis, supporting zero-waste targets and regulatory compliance. Suez also integrates water recycling technologies into its plastic washing processes, reducing operational costs and environmental impact. This dual expertise in waste and water management strengthens its position in sustainable circular economy solutions.

European Union: Regulation-Led Market Restructuring and High-Purity PCR Enforcement

The European Union is entering a decisive enforcement phase for post consumer recycled plastics, with regulatory certainty now shaping investment, trade, and technology choices. The Packaging and Packaging Waste Regulation EU 2025/40 takes full effect on August 12, 2026, replacing the directive framework with a directly applicable regulation that mandates recyclability across all packaging formats and introduces an exceptionally strict 25 ppb limit for any single PFAS in food-contact materials. This threshold is materially altering polymer selection, additive systems, and decontamination processes for food-grade PCR. From 2026 onward, the EU will also enforce recycled content floors of 30% for contact-sensitive PET packaging and 10% for non-PET plastics, excluding medical and infant formula uses. These obligations are shifting demand toward high-quality mechanical recycling outputs and accelerating qualification pipelines for food-contact compliant PCR resins.

Trade and capacity protection have become equally strategic. On January 2, 2026, the European Commission confirmed a new import control framework introducing distinct customs codes for recycled versus virgin plastics, directly targeting mislabeled low-cost imports that have undercut EU recyclers. This move coincides with the proposed Circularity Plastics Package of December 2025, which is positioned as transition finance support for a sector that lost close to one million tonnes of capacity in 2025 due to energy cost pressures. Infrastructure resilience is improving selectively. In October 2025, Trioworld inaugurated a specialized recycling facility in Korsberga capable of processing 25,000 tonnes per year of high-risk waste streams such as agricultural films and hospital plastics. Looking ahead, by December 31, 2026, the Commission and European Chemicals Agency will finalize assessments of substances of concern, a decision that will define which contaminated waste streams remain viable for high-purity PCR reprocessing in Europe.

India: Digitized Traceability and Rapid Scaling of Domestic Recycling Capacity

India’s post consumer recycled plastics market is undergoing a rapid formalization phase, anchored in digital traceability, enforceable recycled content mandates, and capacity expansion by domestic recyclers. Effective July 1, 2025, amendments to the Plastic Waste Management Rules require all plastic packaging to carry QR codes or unique identifiers linked to a centralized portal operated by the Central Pollution Control Board. This system enables batch-level traceability back to registered producers, significantly raising compliance costs for informal operators while improving credibility for verified PCR supply. Parallel to traceability, the 2025–26 fiscal year marks the start of mandatory recycled content obligations, requiring 30% recycled plastic in all Category I rigid packaging, with a legally defined escalation path to 60% by 2028–29.

Market economics are being reshaped by Extended Producer Responsibility enforcement. The October 2025 amendments institutionalized a digital EPR credit trading marketplace, allowing obligated companies to purchase compliance from over-performing recyclers. This mechanism has created price discovery for verified PCR and incentivized investments in scale. At the same time, the 2025 ban on non-recyclable or non-energy-recoverable multi-layered plastics has forced FMCG and packaging producers to pivot toward mono-material structures, directly expanding demand for mechanically recyclable PCR grades. Capacity growth is responding. Gravita India announced a ₹600 crore investment in late 2025 to double recycling capacity to 434,000 tonnes by 2026, with diversification into rubber and paper recycling to stabilize feedstock economics. Enforcement risk is now tangible, as revised penalties under the Environment Protection Act include fines up to ₹1 lakh and potential imprisonment for falsified digital recycling records.

China: Standards-Based Control and Accelerated Chemical Recycling Deployment

China is moving toward a standards-first and enforcement-driven PCR ecosystem, combining mandatory usage rules with rapid deployment of chemical recycling infrastructure. The State Administration for Market Regulation has issued nine national recycled plastics standards effective February 1, 2026, establishing technical specifications designed explicitly to prevent virgin-washing practices. These standards are reinforced by the Ecological Environment Code draft reviewed in late 2025, which for the first time embeds a mandatory system for the use of recycled materials across designated product categories. Together, these measures signal a structural shift from voluntary adoption to regulated demand for PCR content in China’s domestic market.

Technology pathways are diversifying. Chemical recycling is transitioning from pilot to commercial scale. In December 2025, Shandong Recon is scheduled to commission a 40,000 tonne per year waste plastics facility using a horizontal screw-type three-stage continuous reactor, producing approximately 30,000 tonnes of pyrolysis oil annually. Mechanical recycling is being reinforced upstream through Design for Recycling mandates introduced in 2025, which require manufacturers to eliminate metal bottle mouths and reduce adhesive and label complexity to enable automated optical sorting. Internationally, Chinese recyclers continue to secure feedstock access through overseas investments. Firms such as Global Recycling have invested more than $15 million in facilities in Georgia and other hubs, processing waste into high-quality pellets for re-export to China following the domestic scrap import ban.

United States: Fragmented Policy Signals and Shift Toward Advanced Recycling

The United States post consumer recycled plastics market remains structurally fragmented, with state-level regulation driving divergent outcomes and creating uncertainty for long-term capital deployment. A key inflection point is the legal challenge to Oregon’s Plastic Pollution and Recycling Modernization Act, scheduled for January 2026. The case National Association of Wholesaler-Distributors v. Oregon will test the constitutionality of single-entity EPR mandates and is widely viewed as precedent-setting for other states considering similar frameworks. In the absence of federal recycled content mandates, market volatility has intensified. Low virgin resin prices in late 2025 led to the idling or shutdown of major mechanical recycling assets, including WM’s Natura facility in Texas and Alpek-affiliated PET operations in North Carolina.

In response, investment momentum is shifting toward advanced recycling in supportive jurisdictions. In late 2025, Clean Vision began commercial feeding of plastic waste at its West Virginia pyrolysis facility, reflecting growing alignment between state policy and chemical recycling pathways. Regulatory pressure is nonetheless increasing at the state level. California accelerated implementation of SB 54 in 2025, requiring Producer Responsibility Organizations to register by April 1, 2025, ahead of a 2030 target for full recyclability. Additionally, more than 12 states enacted PFAS bans in food packaging during 2025, driving demand for non-fluorinated barrier solutions and indirectly shaping PCR-compatible packaging design.

United Kingdom: Tax-Based Enforcement and FMCG-Led Demand Signals

The United Kingdom’s PCR plastics market is being driven primarily by fiscal instruments and brand-led commitments rather than direct recycled content mandates. The Plastic Packaging Tax was maintained at £217.85 per tonne for packaging containing less than 30% recycled content through the 2025–26 period. While industry groups are lobbying for a higher rate to counter historically low virgin polymer prices, the existing tax continues to act as a material cost signal favoring PCR adoption in consumer packaging. Compliance has become a procurement priority for brand owners rather than recyclers alone.

Brand commitments are translating into measurable PCR offtake. In January 2025, Mondelēz International announced the rollout of 80% certified recycled plastic packaging for Cadbury sharing bars, consuming an estimated 600 tonnes of PCR annually. Such FMCG-led initiatives are stabilizing demand for food-grade recycled plastics even as broader market conditions remain volatile. The UK market therefore remains characterized by demand-pull economics, where taxation and brand commitments compensate for the absence of EU-style binding recycled content regulations.

Comparative Overview of Country-Level Dynamics in Post Consumer Recycled Plastics

Post Consumer Recycled Plastics Market County Level Snapshot

|

Region

|

Primary 2025–2026 Policy Driver

|

Structural Impact on PCR Market

|

|

European Union

|

PPWR enforcement and import controls

|

Shift toward high-purity, food-contact compliant PCR

|

|

India

|

QR traceability and EPR credit trading

|

Rapid formalization and capacity scaling

|

|

China

|

National recycled standards and chemical recycling

|

Mandated demand and diversified technology mix

|

|

United States

|

State-level EPR and PFAS bans

|

Fragmentation and pivot to advanced recycling

|

|

United Kingdom

|

Plastic Packaging Tax and FMCG commitments

|

Demand stability through fiscal and brand pressure

|

Post-Consumer Recycled Plastics Market Report Scope

Post Consumer Recycled Plastics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$163.8 Billion

|

|

Market Size (2034)

|

$355.8 Billion

|

|

Market Growth Rate

|

9%

|

|

Segments

|

By Polymer Type (Polyethylene Terephthalate, High-Density Polyethylene, Low-Density Polyethylene & Linear Low-Density Polyethylene, Polypropylene, Polystyrene, Other Polymers), By Recycling Process (Mechanical Recycling, Chemical Recycling, Bio-Based Recycling), By Source (Bottles, Non-Bottle Rigid Plastics, Flexible Packaging, Ocean-Bound Plastics), By End-Use Industry (Packaging, Building & Construction, Automotive, Textiles & Apparel, Consumer Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Indorama Ventures Public Company Limited, Veolia Environnement SA, Biffa PLC, Suez SA, Berry Global Inc., Alpek SAB de CV, KW Plastics, Far Eastern New Century Corporation, Remondis SE & Co. KG, PreZero International, LyondellBasell Industries N.V., Borealis AG, Plastipak Holdings Inc., Avangard Innovative, Gravita India Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Post-Consumer Recycled Plastics Market Segmentation

By Polymer Type

- Polyethylene Terephthalate

- High-Density Polyethylene

- Low-Density Polyethylene & Linear Low-Density Polyethylene

- Polypropylene

- Polystyrene

- Other Polymers

By Recycling Process

- Mechanical Recycling

- Chemical Recycling

- Bio-Based Recycling

By Source

- Bottles

- Non-Bottle Rigid Plastics

- Flexible Packaging

- Ocean-Bound Plastics

By End-Use Industry

- Packaging

- Building & Construction

- Automotive

- Textiles & Apparel

- Consumer Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Post-Consumer Recycled Plastics Industry

- Indorama Ventures Public Company Limited

- Veolia Environnement SA

- Biffa PLC

- Suez SA

- Berry Global Inc.

- Alpek SAB de CV

- KW Plastics

- Far Eastern New Century Corporation

- Remondis SE & Co. KG

- PreZero International

- LyondellBasell Industries N.V.

- Borealis AG

- Plastipak Holdings Inc.

- Avangard Innovative

- Gravita India Limited

*- List not Exhaustive