Primer Market Size, Surface Preparation Demand, and Industrial Coating Expansion

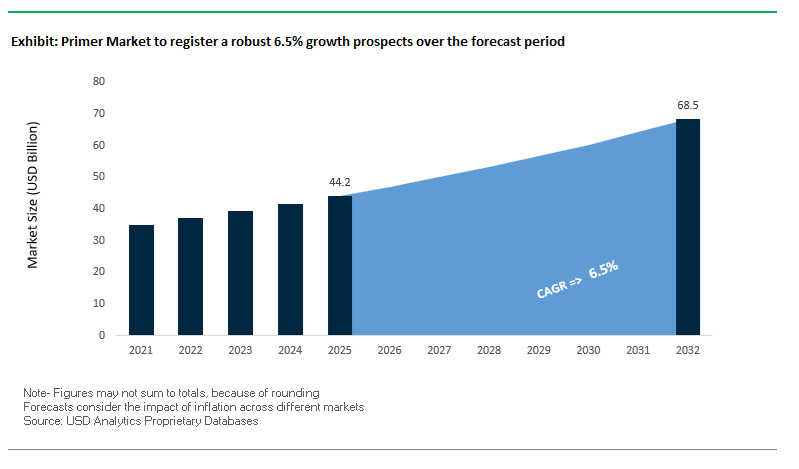

The global Primer Market was valued at $44.2 billion in 2025 and is projected to grow at a CAGR of 6.5% through 2032, reaching $68.7 billion by 2032. This growth reflects the critical role of primers as the foundational layer in coating systems, enabling adhesion, corrosion protection, surface sealing, and performance enhancement across construction, automotive, marine, and industrial applications.

Primers are essential in ensuring the longevity and effectiveness of multi-layer coating systems, particularly in environments exposed to moisture, chemicals, and mechanical stress. Their use spans a wide range of substrates, including steel, concrete, plastics, and composites, making them indispensable in both new construction and maintenance cycles.

A key structural driver is the expansion of global infrastructure and industrial activity, particularly in regions such as Asia-Pacific and the Middle East, where demand for protective coatings in construction, energy, and transportation sectors is accelerating. Additionally, the growth of automotive refinishing, marine coatings, and coil coating systems is increasing the need for high-performance primers that deliver enhanced adhesion and defect-free surfaces.

Sustainability is also reshaping the primer market. Manufacturers are increasingly developing waterborne, low-VOC, and fast-curing primer technologies to meet stringent environmental regulations while improving production efficiency. Innovations in high-opacity primers and advanced surface preparation technologies are further reducing material consumption and application time.

Market Analysis: Ultra-Fast Waterborne Primers, Capacity Expansion, and Automotive Surface Innovation Driving Market Evolution

Recent developments in the Primer Market highlight a strong convergence of process innovation, regional capacity expansion, and advanced material engineering. A major breakthrough is PPG’s AQUACRON® Waterborne Shop Primers (March 2026), which achieve curing in two minutes, compared to the 12–24 hours required for conventional waterborne systems. This innovation significantly enhances throughput for high-volume steel fabricators while maintaining compliance with strict VOC regulations.

Capacity expansion is reinforcing supply capabilities across key regions. Sherwin-Williams’ expansion of its Kentucky coil coatings facility (April 2026) more than doubles production capacity for primer-integrated systems such as PolyPREMIER™ and WeatherXL™, supporting the growing demand for metal roofing and siding applications in North America. Similarly, Jotun’s new manufacturing facility in Abu Dhabi (January 2026) strengthens its ability to supply specialized primers for large-scale infrastructure and energy projects in the Middle East.

Marine and industrial demand continues to drive growth. Hempel’s record performance in 2025, with strong growth in its marine segment, highlights the importance of anti-corrosive primers in shipbuilding and offshore applications, where long-term durability and fuel efficiency are critical. Additionally, Jotun COSCO’s production milestone of 100 million liters underscores the scale of demand for epoxy shop primers in Asia’s shipbuilding industry.

Innovation in automotive coatings is also shaping market trends. BASF’s “DRIVING THE PROXY” initiative (October 2025) introduces advanced primer technologies designed to support multi-dimensional color effects, while Axalta’s refinements to its primer portfolio (January 2026) focus on improving coverage efficiency for bold automotive finishes, reducing material usage and process steps.

Strategic integration and market expansion are further strengthening competitive positioning. Sherwin-Williams’ integration of the Suvinil portfolio enhances its presence in the South American architectural primer market, particularly in wall-sealing and masonry applications.

Market Trend: Ultra-High-Solids Epoxy Primers Advancing Long-Life Infrastructure Protection and Low-VOC Compliance

The industrial primers market is witnessing a decisive shift toward ultra-high-solids epoxy primers with volume solids exceeding 90%, particularly across transportation infrastructure and marine-exposed steel assets. State Departments of Transportation and infrastructure authorities are increasingly specifying these advanced epoxy primer systems to meet dual performance requirements of extended corrosion protection in C5-M environments and compliance with tightening VOC emission limits.

Performance benchmarks for modern zinc-rich high-solids epoxy primers have significantly improved. These systems now achieve more than 3,000 hours of salt spray resistance under ASTM B117 testing, with scribe creepage limited to less than 2 mm. This level of corrosion resistance is critical for bridge coatings, offshore structures, and coastal infrastructure where aggressive environmental exposure accelerates substrate degradation.

From an environmental compliance standpoint, ultra-high-solids epoxy primers operate at VOC levels of 100 g/L or lower, representing a reduction of approximately 75% compared to legacy solvent-borne primers that typically range between 350 and 400 g/L. This reduction enables infrastructure projects to align with regional air quality regulations while minimizing the need for emission control systems.

Lifecycle performance is a key differentiator driving adoption. Data from transportation authorities indicates that high-solids epoxy primer systems applied over abrasive-blasted steel surfaces can extend the first major maintenance cycle of bridges to 20–25 years. This significantly reduces lifecycle costs, minimizes traffic disruption, and improves asset reliability. As a result, high-solids epoxy primers are becoming the standard specification in long-life infrastructure coatings and corrosion protection systems.

Market Trend: Waterborne Primer-Surfacer Systems Gaining Standardization in Automotive Refinish Applications

The automotive refinish coatings market is transitioning toward waterborne primer-surfacer systems, particularly in wet-on-wet application processes. This shift is driven not only by VOC compliance requirements but also by the superior adhesion performance of waterborne technologies across mixed-material automotive substrates including steel, aluminum, and engineered plastics.

Advancements in drying technologies have eliminated historical throughput limitations associated with waterborne systems. Modern formulations combined with infrared curing and high-velocity air drying achieve sandable conditions within 15 to 20 minutes, matching the production efficiency of traditional solvent-based primers. This enables body shops and refinish centers to maintain high throughput while transitioning to environmentally compliant coatings.

Waterborne primers offer a significantly improved VOC profile, with commercial systems achieving levels at or below 50 g/L. This supports compliance with stringent air quality regulations and facilitates certification under environmentally sustainable programs such as green body shop initiatives. The low-emission profile is particularly important in urban regions with strict environmental enforcement.

Material efficiency is also enhanced in waterborne systems. Due to optimized pigment-to-binder ratios and improved atomization characteristics, these primers deliver 15% to 20% higher transfer efficiency compared to conventional solvent systems. This reduces material consumption, minimizes overspray losses, and lowers maintenance costs associated with spray booth filtration systems. These combined advantages are accelerating the adoption of waterborne primer technologies in global automotive refinishing operations.

Market Opportunity: US EPA NESHAP Subpart MMMM Revisions Driving Adoption of Low-VOC and High-Solids Primer Technologies

The 2026 revisions to the National Emission Standards for Hazardous Air Pollutants under Subpart MMMM, implemented by the U.S. Environmental Protection Agency, are creating a strong regulatory push toward low-VOC primer formulations across industrial coating applications. The updated framework mandates reductions in hazardous air pollutant emissions for major sources and removes legacy exemptions related to startup, shutdown, and malfunction conditions, requiring continuous compliance.

These changes are significantly increasing compliance costs for facilities relying on high-VOC solvent-borne primers. As a result, manufacturers are incentivized to adopt primer systems with VOC content at or below 100 g/L to qualify for the “Compliant Material” pathway. This pathway eliminates the need for capital-intensive emission control systems such as Regenerative Thermal Oxidizers, reducing both upfront investment and ongoing operational expenses.

High-solids epoxy primers and waterborne primer systems are emerging as the primary compliance solutions under this regulatory framework. Their ability to deliver both environmental performance and high durability makes them attractive alternatives across sectors including automotive components, industrial machinery, and infrastructure coatings. This regulatory shift is expected to accelerate technology upgrades and drive broader adoption of sustainable primer chemistries in North America.

Market Opportunity: China VOCs Phase 4 Action Plan Accelerating Transition to Low-VOC Primer Systems Across Industrial Clusters

The implementation of the VOCs Phase 4 Action Plan by the Ministry of Ecology and Environment is creating substantial growth opportunities for low-VOC primer technologies across China’s industrial coatings market. Effective from mid-2026, the policy mandates that 62 key industries, including automotive manufacturing, metal furniture production, and wood processing, prioritize primer systems with VOC levels at or below 100 g/L.

In addition to national-level mandates, regional enforcement is intensifying through the establishment of low-VOC industrial zones in major economic clusters such as the Yangtze River Delta and Pearl River Delta. Within these zones, the use of high-VOC solvent-based primers is subject to significant environmental taxation, creating a strong financial incentive for manufacturers to transition toward waterborne and high-solids primer technologies.

This regulatory environment is expected to drive a substantial shift in procurement patterns, with projections indicating that up to 40% of primer demand in these regions will transition to low-VOC formulations by 2028. Manufacturers that align their product portfolios with these requirements are positioned to capture increased market share, particularly in export-oriented industries that must comply with both domestic and international environmental standards.

The convergence of regulatory enforcement, economic incentives, and sustainability targets is establishing low-VOC primers as the dominant technology pathway in China’s industrial coatings sector, while also enhancing the global competitiveness of compliant manufacturers.

Primer Market Share and Segmentation Insights: Epoxy-Based Industrial Leadership and Face Primer Dominance in Cosmetic Segment

By Chemistry (Industrial/Protective Primers): Epoxy Primers Lead with High-Performance Corrosion Protection

The epoxy primers segment dominated the industrial and protective primers market with a 42.6% share in 2025, driven by its superior adhesion strength, corrosion resistance, and chemical durability across demanding environments. Epoxy primers are widely used on steel, aluminum, and concrete substrates, making them the preferred solution for industrial coatings, marine applications, oil & gas infrastructure, and heavy construction projects. Their ability to provide excellent moisture resistance and long-term protection against corrosion ensures extended asset lifespan and reduced maintenance costs. A key growth factor is the advancement of high-solids epoxy primer formulations exceeding 90% solids, which significantly reduce volatile organic compound (VOC) emissions while delivering thick, high-build protective films in single-coat applications. This aligns with global environmental regulations and sustainability trends. The combination of low-VOC compliance, strong substrate adhesion, and industrial-grade protection continues to position epoxy primers as the backbone of the global protective coatings market.

By Product (Cosmetic Primers): Face Primers Dominate with Skincare Integration and Long-Lasting Makeup Performance

The face primer segment held a leading 55.4% share of the cosmetic primers market in 2025, fueled by rising consumer demand for long-lasting makeup, smooth skin finish, and multifunctional beauty products. Face primers are essential in modern beauty routines, as they minimize pores, control oil, and enhance foundation adhesion, creating a flawless base that extends makeup wear throughout the day. This segment benefits from widespread adoption across diverse age groups and skin types, making it the most commercially significant category in the cosmetic primer market. A major trend driving growth is the emergence of skincare-makeup hybrid primers, incorporating SPF protection, hydration, anti-aging ingredients, and color-correcting properties, which increase product value and encourage repeat purchases. With the rise of premium beauty products, clean beauty formulations, and personalized skincare solutions, face primers continue to dominate, supported by strong consumer engagement and innovation in the global cosmetics industry.

Competitive Landscape of the Primer Market

AkzoNobel Leads Sustainable Primer Innovation with AI-Driven Inspection and Bio-Based Technologies

AkzoNobel N.V. is a leading player in the primer market, strengthening its position through sustainability initiatives and digital innovation. In Q1 2026, the company reported a 14.5% adjusted EBITDA margin, supported by cost optimization and pricing discipline. Its ongoing merger with Axalta is expected to create a major global coatings powerhouse. AkzoNobel has introduced AI-driven drone inspection tools capable of detecting primer degradation and corrosion with micron-level precision, significantly reducing maintenance time for industrial assets. Its Interpon® and International® primer systems are transitioning toward bio-attributed resins, targeting a 25% reduction in carbon footprint.

Sherwin-Williams Expands Market Leadership with High-Performance and Fast-Curing Primer Systems

The Sherwin-Williams Company continues to dominate the primer market, particularly in North America, leveraging its extensive retail and professional network. In Q1 2026, the company reported record net sales of $5.67 billion and strong EBITDA margins. Its Latex White High Build Primer has become an industry benchmark for same-day return-to-service applications, offering superior stain-blocking and mold resistance. Sherwin-Williams is also integrating its Suvinil and Valspar portfolios to deliver comprehensive coating systems, including low-VOC and UV-cure primer solutions, strengthening its position in both residential and industrial markets.

PPG Drives Innovation with Sustainable and EV-Focused Primer Technologies

PPG Industries, Inc. is a key innovator in the primer market, leveraging its strong R&D capabilities to develop advanced coating solutions. In 2026, the company exceeded earnings expectations and maintained strong revenue growth. Its Sigma Wallprimer Plus and Sigma Glide® systems feature Environmental Product Declarations (EPDs), supporting green building certification requirements. PPG is also a leader in dielectric primers for EV battery systems, providing thermal management and electrical insulation for high-voltage applications. Its PPG LINQ™ platform integrates AI-driven color matching and process optimization, improving efficiency and reducing material waste.

BASF Strengthens Industry Backbone with Integrated Chemical Solutions and Sustainable Primer Technologies

BASF SE plays a critical role in the primer market, leveraging its integrated chemical production capabilities. The company has expanded its MDI production capacity to support the growing demand for polyurethane-based primers. Its “Integrated Process” technology in automotive coatings eliminates the need for a primer-surfacer layer, reducing energy consumption and CO₂ emissions by up to 20%. BASF’s strategic focus on sustainability and cost efficiency, supported by its Verbund system, reinforces its position as a key supplier of high-performance primer materials and technologies.

Axalta Advances Primer Technologies with AI and Low-Temperature Curing Innovations

Axalta Coating Systems is a leading player in the primer market, particularly in automotive and mobility applications. Its TintMaster AI platform enhances production efficiency by predicting and optimizing primer formulations. The company’s Lumeera™ 3250 system enables low-temperature curing at 80°C, significantly reducing energy consumption and CO₂ emissions in automotive manufacturing. Axalta has also developed fire-resistant primer systems for EV batteries, capable of withstanding extreme temperatures. Its strong financial performance and strategic positioning reinforce its leadership in advanced and sustainable primer technologies.

Jotun Expands Global Leadership with Smart and High-Durability Primer Systems

Jotun Group is a dominant player in the primer market, particularly in marine and offshore applications. The company has achieved record revenues driven by strong growth in infrastructure and newbuilding projects. Its Fenomastic Emulsion Primer is widely recognized for its durability and compliance with environmental standards, supported by verified carbon data through Environmental Product Declarations. Jotun is also developing smart primer systems that integrate with robotic cleaning technologies to prevent biofouling and enhance asset longevity. Its expansion in the Middle East and Asia-Pacific strengthens its leadership in high-performance and climate-resistant primer coatings.

China Primer Market: High-Volume Innovation and Waterborne Transition

China dominates the global primer market, undergoing a rapid transition from traditional solvent-based systems to eco-friendly, high-performance primer technologies. The 2025 “Green Manufacturing” mandate has accelerated the shift from solvent-based to waterborne epoxy primers (S2W transition), significantly reducing VOC emissions across industrial sectors.

Technological advancements include the development of low-temperature curing shop primers, reducing energy consumption in steel processing by up to 20%. China is also leading innovation in graphene-enhanced anticorrosive primers, particularly for marine and offshore applications. The country’s infrastructure boom is driving large-scale adoption of zinc-rich primers for ultra-high-voltage (UHV) transmission towers, ensuring long service life. Additionally, the EV sector is fueling demand for dielectric primers used in battery housings for thermal management and electrical insulation. Emerging innovations such as smart primers with corrosion-indicating microcapsules further highlight China’s leadership in advanced coating technologies.

India Primer Market: Infrastructure-Led Growth and Automotive Advancements

India is witnessing strong growth in the primer coatings market, driven by infrastructure expansion and manufacturing localization. Government initiatives such as the PM Gati Shakti Master Plan are boosting demand for epoxy-zinc phosphate primers in large-scale transportation projects, including airports and railway stations.

Industrial expansion by major players like Asian Paints and JSW is supporting increased domestic production, while the automotive sector is adopting Thin-Film Electrocoat (E-coat) technologies to enhance corrosion resistance in lightweight components. The aerospace and defense sectors are also driving demand for wash (etch) primers, particularly in emerging manufacturing clusters. Regulatory alignment with updated BIS standards is promoting lead-free and low-odor primer formulations, strengthening India’s position as a high-growth market.

United States Primer Market: Aerospace Leadership and PFAS-Free Transition

The U.S. primer market is defined by innovation, reshoring trends, and stringent environmental regulations. The implementation of PFAS-free mandates (2026) is driving the development of new primer chemistries for architectural and industrial applications.

Technological advancements include UV-curable primers, enabling rapid curing without thermal stress, and nano-silica modified primers that enhance bonding for advanced manufacturing, including 3D-printed components. The aerospace sector is a key driver, with widespread adoption of chrome-free epoxy primers to meet environmental and safety standards. Infrastructure investments under the Bipartisan Infrastructure Law are increasing demand for moisture-cured urethane (MCU) primers for bridge and structural applications. Additionally, automotive refinish primers are gaining traction due to their ability to reduce labor time and improve efficiency.

Germany Primer Market: Sustainability and Precision Engineering

Germany leads the European primer coatings market through its focus on sustainability, precision engineering, and advanced manufacturing. The country is pioneering biodegradable primer binders in response to EU REACH microplastic regulations, reducing environmental impact.

Technological advancements include digital twin modeling for precise primer application, minimizing material waste and optimizing coating thickness. The automotive sector is driving demand for low-bake primers compatible with heat-sensitive EV components, while renewable energy projects are increasing the use of high-performance primers for offshore wind installations. Innovations such as bio-attributed epoxy resins and antimicrobial primer systems further reinforce Germany’s leadership in sustainable coating technologies.

South Korea Primer Market: Maritime Strength and Electronics Innovation

South Korea is a global leader in industrial primer applications, particularly in maritime and electronics sectors. The country has standardized the use of zinc silicate shop primers across shipbuilding operations, ensuring corrosion protection during long construction cycles.

Innovation is also strong in electronics-grade primers, including EMI/RFI shielding coatings used in 5G devices and telecommunications hardware. Investments in R&D are driving the development of fouling-release primers for next-generation LNG carriers, improving environmental performance. Additionally, the expansion of specialty primer production facilities and compliance with K-REACH regulations are strengthening South Korea’s global competitiveness in high-performance primer technologies.

Vietnam Primer Market: Manufacturing Growth and Clean Production Shift

Vietnam is emerging as a fast-growing market in the primer coatings industry, driven by industrial expansion and global supply chain shifts. Investments in automated coating facilities are supporting the production of ESD primers for electronics manufacturing, catering to global OEMs.

Government incentives promoting clean production technologies are accelerating the transition to water-based primer systems, reducing environmental impact. The country’s coastal infrastructure projects are increasing demand for marine-grade primers, while growth in export-oriented furniture manufacturing is driving adoption of high-weatherability primer coatings. Additionally, Vietnam’s expanding role in bicycle and e-bike production is boosting demand for powder primers, reinforcing its position as a key manufacturing hub.

Saudi Arabia Primer Market: Megaproject Growth and Energy Sector Demand

Saudi Arabia is experiencing rapid growth in the primer coatings market, driven by large-scale infrastructure projects under Vision 2030 and strong demand from the oil and gas sector. Megaprojects such as NEOM are increasing the use of fusion-bonded epoxy (FBE) primers for underground utilities and pipelines.

The energy sector is a major driver, with high demand for phenolic epoxy primers used in tank linings to withstand harsh operating conditions. Innovations such as solar-reflective primers are improving thermal performance in extreme climates, while stricter VOC regulations are promoting the adoption of waterborne systems. Additionally, the use of anti-carbonation primers in coastal infrastructure is enhancing durability and preventing corrosion, positioning Saudi Arabia as a key growth market in the region.

Primer Market Report Scope

Primer Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$44.2 Billion

|

|

Market Size (2032)

|

$68.7 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

I. Industrial and Architectural Primers), By Chemistry (Epoxy Primers, Polyurethane Primers, Acrylic Primers, Alkyd Primers, Zinc-Rich Primers, Vinyl and Chlorinated Rubber Primers), By Technology (Water-borne Primers, Solvent-borne Primers, Powder Primers, Radiation-Cured), By Substrate (Metal, Concrete and Masonry, Wood and MDF, Plastics and Composites, Fiberglass), By Application (Building and Construction, Automotive, Marine and Offshore, Aerospace and Defense, Industrial Machinery and Equipment, Infrastructure, II. Cosmetic and Makeup Primers), By Product (Face Primer, Eye Primer, Lip Primer, Lash Primer, Multi-Purpose), By Formulation (Silicone-based, Water-based, Oil-based, Stick and Solid Formulations), By Function (Mattifying and Oil Control, Hydrating and Moisturizing, Pore-Minimizing and Smoothing, Illuminating, Color Correcting, SPF-Infused), By Target Skin Type (Oily, Dry, Sensitive, Mature)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., Jotun A/S, Axalta Coating Systems Ltd., BASF SE, Hempel A/S, Kansai Paint Co., Ltd., RPM International Inc., Asian Paints Limited, Sika AG, 3M Company, Tnemec Company, Inc., Berger Paints India Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Primer Market Segmentation

Industrial and Architectural Primers

By Chemistry

- Epoxy Primers

- Polyurethane Primers

- Acrylic Primers

- Alkyd Primers

- Zinc-Rich Primers

- Vinyl and Chlorinated Rubber Primers

By Technology

- Water-borne Primers

- Solvent-borne Primers

- Powder Primers

- Radiation-Cured

By Substrate

- Metal

- Concrete and Masonry

- Wood and MDF

- Plastics and Composites

- Fiberglass

By Application

- Building and Construction

- Automotive

- Marine and Offshore

- Aerospace and Defense

- Industrial Machinery and Equipment

- Infrastructure

Cosmetic and Makeup Primers

By Product

- Face Primer

- Eye Primer

- Lip Primer

- Lash Primer

- Multi-Purpose

By Formulation

- Silicone-based

- Water-based

- Oil-based

- Stick and Solid Formulations

By Function

- Mattifying and Oil Control

- Hydrating and Moisturizing

- Pore-Minimizing and Smoothing

- Illuminating

- Color Correcting

- SPF-Infused

By Target Skin Type

- Oily

- Dry

- Sensitive

- Mature

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Primer Industry

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Jotun A/S

- Axalta Coating Systems Ltd.

- BASF SE

- Hempel A/S

- Kansai Paint Co., Ltd.

- RPM International Inc.

- Asian Paints Limited

- Sika AG

- 3M Company

- Tnemec Company, Inc.

- Berger Paints India Limited

*- List not Exhaustive