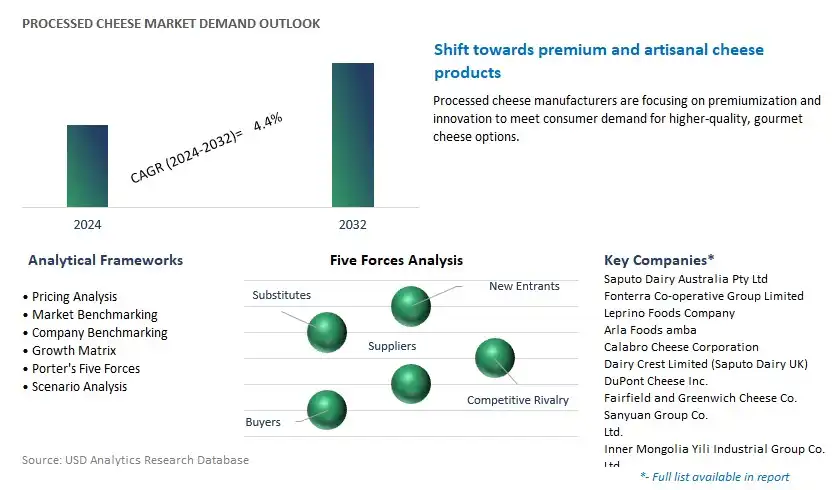

Processed Cheese Market is estimated to increase at a growth rate of 4.4% CAGR over the forecast period from 2024 to 2030.

The Processed Cheese Market Study forecasts the market size across 6 regions and 24 countries for diverse segments including-Type (Pasteurized Cheese, Pasteurized Cheese Foods, Pasteurized Cheese Spreads), Application (Food Industry, Restaurant, Others), Distribution Channel (Offline, Online).

An Introduction to Processed Cheese Market, 2024

Processed Cheese: Similar to processed cheddar, the processed cheese market thrives on convenience and versatility. Its drivers are grounded in the need for easily portioned and spreadable cheese, often used in sandwiches, burgers, and ready-to-eat meals. Its market growth is influenced by evolving consumer preferences for quick and easy meal solutions, innovations in processing techniques to enhance texture and flavor, and its utility in a variety of culinary applications.

Processed Cheese Market Trend: Shifting Consumer Preferences Towards Convenience Foods

A significant trend in the processed cheese market is the shift in consumer preferences towards convenience foods. With busier lifestyles and a demand for easy meal solutions, consumers are increasingly turning to processed cheese products. This trend is driven by the convenience factor—processed cheese's versatility in applications like sandwiches, dips, and ready-to-eat meals caters to the need for quick and hassle-free meal preparation.

Processed Cheese Market Driver: Growth in Snacking Culture and On-the-Go Eating

A key driver behind the growth of the processed cheese market is the expansion of snacking culture and on-the-go eating habits. Processed cheese's convenience as a snack or a component in portable foods like sandwiches or wraps aligns with consumers' desire for quick, satisfying snacks. This driver is propelled by the increasing demand for portable, easily accessible foods that fit into modern, fast-paced lifestyles.

Processed Cheese Market Opportunity: Innovation in Healthier Formulations and Varieties

An opportunity exists within the processed cheese market for innovation in healthier formulations and varieties. Companies can invest in research and development to create processed cheese options with reduced sodium, lower fat content, or the inclusion of natural and functional ingredients. Developing healthier varieties while maintaining taste and texture could tap into health-conscious consumer segments, addressing concerns about nutritional content and enhancing the market appeal of processed cheese.

Processed Cheese Market Segmentation

Type

Pasteurized Cheese

Pasteurized Cheese Foods

Pasteurized Cheese Spreads

Application

Food Industry

Restaurant

Others

Distribution Channel

Offline

Online

Geographical Segmentation

• North America (US, Canada, Mexico)

• Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

• Asia Pacific (China, India, Japan, South Korea, South East Asia, Rest of Asia Pacific)

• South America (Brazil, Argentina, Rest of South America)

• Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, Egypt, South Africa, Nigeria, Rest of Africa)

Processed Cheese Companies Profiled in the Study-

Saputo Dairy Australia Pty Ltd

Fonterra Co-operative Group Limited

Leprino Foods Company

Arla Foods amba

Calabro Cheese Corporation

Dairy Crest Limited (Saputo Dairy UK)

DuPont Cheese, Inc.

Fairfield and Greenwich Cheese Co.

Sanyuan Group Co., Ltd.

Inner Mongolia Yili Industrial Group Co., Ltd.

Reasons to Buy the Processed Cheese Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Processed Cheese Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Processed Cheese Market industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction To 2024 Processed Cheese Markets

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Included

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Processed Cheese Market Size Outlook, $ Million, 2021 to 2030

3.2 Processed Cheese Market Outlook by Type, $ Million, 2021 to 2030

3.3 Processed Cheese Market Outlook by Product, $ Million, 2021 to 2030

3.4 Processed Cheese Market Outlook by Application, $ Million, 2021 to 2030

3.5 Processed Cheese Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Processed Cheese Industry

4.2 Key Market Trends in Processed Cheese Industry

4.3 Potential Opportunities in Processed Cheese Industry

4.4 Key Challenges in Processed Cheese Industry

5 Market Factor Analysis

5.1 Competitive Landscape

5.1.1 Global Processed Cheese Market Share by Company

5.1.2 Product Offerings by Company

5.2 Porter’s Five Forces Analysis

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Processed Cheese Market Outlook by Segments

7.1 Processed Cheese Market Outlook by Segments

Type

Pasteurized Cheese

Pasteurized Cheese Foods

Pasteurized Cheese Spreads

Application

Food Industry

Restaurant

Others

Distribution Channel

Offline

Online

8 North America Processed Cheese Market Analysis and Outlook To 2030

8.1 Introduction to North America Processed Cheese Markets in 2024

8.2 North America Processed Cheese Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Processed Cheese Market size Outlook by Segments, 2021-2030

Type

Pasteurized Cheese

Pasteurized Cheese Foods

Pasteurized Cheese Spreads

Application

Food Industry

Restaurant

Others

Distribution Channel

Offline

Online

9 Europe Processed Cheese Market Analysis and Outlook To 2030

9.1 Introduction to Europe Processed Cheese Markets in 2024

9.2 Europe Processed Cheese Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Processed Cheese Market size Outlook by Segments, 2021-2030

Type

Pasteurized Cheese

Pasteurized Cheese Foods

Pasteurized Cheese Spreads

Application

Food Industry

Restaurant

Others

Distribution Channel

Offline

Online

10 Asia Pacific Processed Cheese Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Processed Cheese Markets in 2024

10.2 Asia Pacific Processed Cheese Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Processed Cheese Market size Outlook by Segments, 2021-2030

Type

Pasteurized Cheese

Pasteurized Cheese Foods

Pasteurized Cheese Spreads

Application

Food Industry

Restaurant

Others

Distribution Channel

Offline

Online

11 South America Processed Cheese Market Analysis and Outlook To 2030

11.1 Introduction to South America Processed Cheese Markets in 2024

11.2 South America Processed Cheese Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Processed Cheese Market size Outlook by Segments, 2021-2030

Type

Pasteurized Cheese

Pasteurized Cheese Foods

Pasteurized Cheese Spreads

Application

Food Industry

Restaurant

Others

Distribution Channel

Offline

Online

12 Middle East and Africa Processed Cheese Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Processed Cheese Markets in 2024

12.2 Middle East and Africa Processed Cheese Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Processed Cheese Market size Outlook by Segments, 2021-2030

Type

Pasteurized Cheese

Pasteurized Cheese Foods

Pasteurized Cheese Spreads

Application

Food Industry

Restaurant

Others

Distribution Channel

Offline

Online

List of Companies

Saputo Dairy Australia Pty Ltd

Fonterra Co-operative Group Limited

Leprino Foods Company

Arla Foods amba

Calabro Cheese Corporation

Dairy Crest Limited (Saputo Dairy UK)

DuPont Cheese, Inc.

Fairfield and Greenwich Cheese Co.

Sanyuan Group Co., Ltd.

Inner Mongolia Yili Industrial Group Co., Ltd.

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

Type/brPasteurized Cheese /brPasteurized Cheese Foods /brPasteurized Cheese Spreads /br/brApplication/brFood Industry /brRestaurant /brOthers /br/brDistribution Channel/brOffline /brOnline