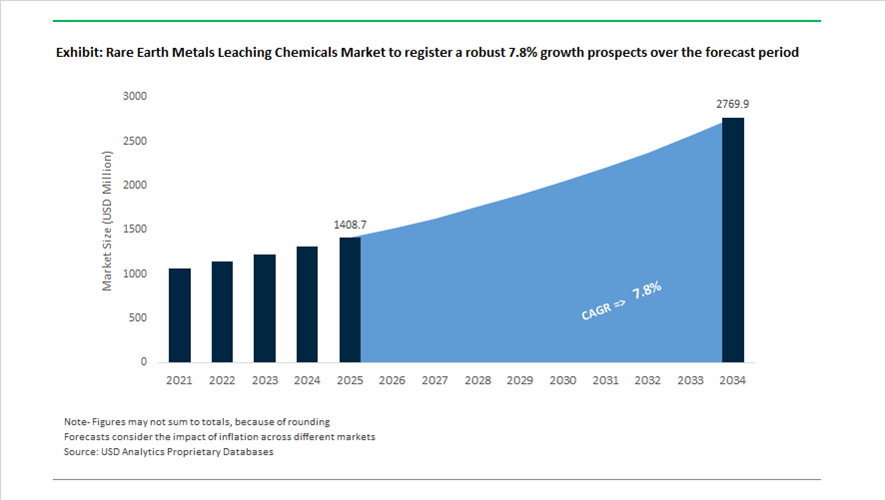

Rare Earth Metals Leaching Chemicals Market Valued at $1,408.7 Million in 2025, Projected to Reach $2,769.4 Million by 2034 at 7.8% CAGR

The global rare earth metals leaching chemicals market is valued at $1,408.7 million in 2025 and is projected to reach $2,769.4 million by 2034, expanding at a CAGR of 7.8%. Growth is driven by accelerating demand for rare earth element (REE) extraction chemicals, acid and alkaline leaching reagents, solvent extraction (SX) diluents, ion-exchange resins, heavy rare earth separation agents, and advanced hydrometallurgical processing solutions supporting magnet-grade neodymium, dysprosium, terbium, and samarium production. Strategic decoupling of supply chains, EV magnet demand, wind turbine installations, and defense-sector procurement are reshaping reagent innovation and domestic refining capacity investments.

Geopolitical shifts intensified in 2024 and 2025. China introduced strict export controls on rare earth processing and separation technologies in 2024, followed by expanded restrictions in October 2025 requiring special licenses for products containing more than 0.1% Chinese heavy rare earth content. In response, April 2025 marked a pivotal moment when MP Materials ceased shipping rare earth concentrate to China, redirecting material to its Mountain Pass facility to expand domestic cracking, leaching, and separation operations. In 2025, the U.S. Department of Defense reinforced this transition by taking a $400 million equity stake in MP Materials to accelerate domestic rare earth chemical processing capacity. In July 2024, Arafura Rare Earths secured conditional approval for over $1 billion in debt funding for its Nolans Project, followed by a $200 million Australian government equity commitment in January 2025 to advance its ore-to-oxide hydrometallurgical facility. By December 2025, Iluka Resources had invested $865 million into the Eneabba refinery in Western Australia, designed for 55,000 tonnes per annum cracking and leaching capacity, establishing Australia’s first integrated separated rare earth oxide plant. In October 2025, Aclara Resources launched Project Dynamo, a $277 million heavy rare earth separation facility in Louisiana using proprietary sustainable ionic clay extraction technology.

Technological innovation is redefining leaching chemistry efficiency. In late 2025, mining technology providers introduced engineered bioleaching systems using metagenomic microbial strains to mobilize REEs from low-grade ores, achieving 25–35% efficiency gains while significantly reducing reliance on concentrated mineral acids. Early 2026 saw the commercialization of Deep Eutectic Solvents (DES), biodegradable designer liquids capable of selectively dissolving rare earth elements based on ionic radius, positioning them as low-toxicity alternatives to kerosene-based SX diluents. AI-guided hydrometallurgical sequencing systems launched in 2026 now optimize pH, redox potential, and ion concentration in real time, improving reagent dosing precision and increasing yield by up to 50% for critical elements such as neodymium and dysprosium. Molecularly Imprinted Polymers (MIPs), introduced in 2026, provide highly selective capture of terbium and dysprosium ions from pregnant leach liquors, reducing downstream solvent extraction load and chemical waste.

Strategic supply agreements reinforce separation chemical demand. In November 2025, Solvay entered long-term agreements with Permag in the U.S. and Less Common Metals in the UK to ensure stable supply of samarium and other magnet-grade REEs using advanced separation reagents. The rare earth metals leaching chemicals market is increasingly characterized by bioleaching reagent systems, deep eutectic solvent extraction technologies, AI-optimized hydrometallurgical control, molecularly imprinted polymer selectivity, domestic cracking and leaching infrastructure expansion, magnet-grade REE separation chemistry, and geopolitically driven supply chain localization. As electrification, renewable energy, and defense procurement accelerate, chemical innovation in leaching and separation remains central to rare earth supply security and processing efficiency.

Strategic Trends and Growth Opportunities in the Rare Earth Metals Leaching Chemicals Market

Strategic Shift Toward In-Situ and Agitated Leaching Using Sustainable Reagents

The rare earth metals leaching chemicals market is undergoing a decisive methodological shift as environmental compliance, water stewardship, and community acceptance become binding constraints on project development. Traditional high-acid, high-temperature extraction routes are increasingly being replaced by in-situ leaching (ISL) and advanced agitated leaching circuits that rely on weak organic acids and ammonium-based salt systems. This transition is fundamentally altering demand patterns for leaching chemicals, favoring formulations that deliver high selectivity with reduced ecological footprint.

Industrial trials reported in August 2025 confirm that citric acid, deployed at concentrations ranging from 0.9 M to 1.45 M, can achieve high rare earth element dissolution efficiencies from permanent magnet swarf and fine secondary residues. Compared with sulfuric acid, these organic lixiviants significantly reduce downstream neutralization requirements and effluent toxicity, making them particularly attractive in jurisdictions with strict water discharge regulations. As a result, organic acids such as citric and acetic acid are moving from laboratory-scale validation into early commercial deployment across Asia-Pacific and parts of Europe.

Parallel innovation is occurring in mass transfer optimization. Pilot programs conducted in late 2024 demonstrated that compound leaching agents combining ammonium sulfate and ammonium formate substantially enhance rare earth mobility while suppressing the co-leaching of aluminum and iron. These systems enable efficient room-temperature extraction, eliminating energy-intensive roasting steps and reducing overall process energy consumption. For leaching chemical suppliers, this trend is expanding demand for tailored ammonium salt blends rather than single-chemical offerings, shifting the market toward higher-value, application-specific formulations.

Selective Lixiviants for Secondary and Unconventional Rare Earth Feedstocks

With primary rare earth mining projects facing extended permitting timelines and capital intensity, the industry is accelerating investment into secondary and unconventional feedstocks such as coal fly ash, red mud, and overburden materials. These complex matrices require a new generation of highly selective leaching chemicals capable of extracting rare earths without mobilizing hazardous heavy metals.

Policy intervention is playing a catalytic role. In January 2025, India launched the National Critical Mineral Mission with an initial allocation of ₹100 crore to support pilot-scale recovery of critical minerals from industrial waste streams. Analytical results from coal fly ash samples at the Singareni Thermal Power Plant revealed rare earth concentrations reaching 2,100 mg/kg, validating the economic case for chemically intensive hydrometallurgical recovery. This has directly increased demand for customized leaching reagents optimized for alkaline and aluminosilicate-rich substrates.

Technical progress is reinforcing this momentum. Industry data from September 2025 shows that combining alkaline or thermal pre-treatment with modified acid leaching improves rare earth recovery from coal combustion products by more than 30% versus direct acid leaching. This approach is being scaled in the Appalachian coal regions of the United States, where securing domestic neodymium and samarium supply has become a strategic priority. For chemical suppliers, these developments are creating sustained demand for selective lixiviants engineered for feedstock variability rather than uniform ore bodies.

Chemicals for Direct Lithium-Ion Battery and Magnet Recycling

The rapid growth in end-of-life electric vehicle batteries and industrial magnet scrap represents one of the most structurally attractive opportunities for rare earth leaching chemical suppliers. Recovering rare earths from the magnet fraction of battery scrap requires integrated chemical systems that can operate alongside lithium, cobalt, and nickel recovery processes without cross-contamination.

In October 2025, China announced the formation of China Resources Recycling Group Ltd., a state-owned entity designed to industrialize critical mineral recovery from batteries and electronic waste. This consolidation is expected to drive large-scale demand for sequential leaching chemistries capable of isolating rare earths after the initial extraction of base battery metals. For suppliers, this favors reagent portfolios that function as coordinated “chemical sequences” rather than stand-alone products.

According to the International Energy Agency’s Critical Minerals Outlook 2025, recycling could supply 20% to 30% of global lithium, nickel, and cobalt demand by 2040. Within these recycling flows, rare earth recovery will increasingly rely on reagent systems that selectively precipitate elements such as neodymium and dysprosium as oxalates from complex, multi-metal solutions. This requirement is opening a premium niche for suppliers that can deliver precision precipitation agents with predictable kinetics and minimal impurity drag-in.

Closed-Loop Reagent Recovery and Regenerative Leaching Systems

Environmental liabilities and rising reagent costs are accelerating adoption of closed-loop leaching systems designed for chemical regeneration and reuse. This is reshaping procurement decisions, with mining and recycling operators prioritizing reagents that can be efficiently recovered via membrane separation, solvent extraction, or counter-current flow configurations.

Breakthrough demonstrations in December 2025 at Australia’s North Stanmore Project showed that optimized counter-current leaching architectures could achieve 80% rare earth recovery in just 30 minutes, compared with conventional cycles lasting 24 to 36 hours. This eight-fold acceleration dramatically reduces reagent residence time and consumption per unit of ore, translating directly into lower operating expenditure and higher throughput.

From a capital perspective, this shift is highly consequential. While traditional rare earth separation plants require capital investments in the range of $100 million to $500 million, closed-loop chemical systems are being positioned as a means to reduce operating costs by 20% to 40% through reagent regeneration. These systems are particularly critical in emerging “third-country” processing alliances, such as India–U.S. partnerships, where lowering lifecycle costs is essential to reducing global dependence on single-source rare earth processing hubs.

Rare Earth Metals Leaching Chemicals Market Share and Segmentation Insights

Inorganic Acids Lead Rare Earth Extraction Processes in Hydrometallurgical Operations

Inorganic acids accounted for 52.80% of the Rare Earth Metals Leaching Chemicals Market by chemical type in 2025, reflecting their central role in hydrometallurgical extraction processes used to recover rare earth elements from mineral concentrates. Sulfuric acid, hydrochloric acid, and nitric acid are widely used for breaking down bastnasite, monazite, and other rare earth bearing ores in industrial scale processing facilities. These acids provide cost effective and well established leaching performance for separating rare earth metals from host minerals. Industrial scale mining operations rely heavily on acid leaching to enable downstream solvent extraction and purification steps. In 2025, process optimization strategies including acid recycling and staged leaching are improving extraction efficiency, reducing chemical consumption while maintaining recovery yields in large scale rare earth processing operations.

Primary Mining and Refining Drives Global Demand for Rare Earth Leaching Chemicals

Primary mining and refining represented 72.80% of the Rare Earth Metals Leaching Chemicals Market by application in 2025, reflecting the dominant role of virgin ore processing in global rare earth element supply. Mining operations require continuous chemical inputs for leaching, solvent extraction, and precipitation processes used to produce high purity rare earth oxides. Large scale production facilities in China, Australia, the United States, and Myanmar remain key demand centers for leaching chemicals. The scale of industrial rare earth processing supports strong consumption of acid based reagents and extraction chemicals. In 2025, global efforts to diversify rare earth supply chains are driving new mining projects, creating additional demand for leaching chemicals in emerging production regions across Africa, Brazil, and North America.

Rare Earth Metals Leaching Chemicals Market Competitive Landscape

The 2026 rare earth metals leaching chemicals market is evolving toward low-acid consumption leaching, solvent extraction optimization, and closed-loop reagent recovery. Growth is driven by critical mineral independence strategies, radionuclide management, and bio-derived leaching agents supporting sustainable rare earth oxide production.

Lynas strengthens rare earth leaching and separation with renewable-powered operations and HRE expansion

Lynas Rare Earths Ltd. is advancing its hydrometallurgical capabilities through optimized cracking and leaching operations supported by its Lynas 2025 program. The company achieved record NdPr production of 6,375 tonnes in H1 FY26 following kiln upgrades in Malaysia that improved thermal efficiency and operational safety. Expansion of heavy rare earth separation capacity enables increased production of dysprosium and terbium, with initial shipments already completed. Renewable integration at Mt Weld delivers 92% clean energy usage, reducing carbon intensity across leaching and beneficiation circuits. Strategic sourcing of ionic clay leaching reagents mitigates supply chain risks and ensures continuity. Focus on integrated extraction-to-separation capabilities enhances control over high-purity REO production.

MP Materials advances vertical integration with domestic leaching-to-magnet supply chain and HRE circuit development

MP Materials Corp. is strengthening its rare earth processing capabilities through full vertical integration from leaching to magnet manufacturing. Record NdPr oxide and metal production at Mountain Pass and Fort Worth supports the U.S. “mine-to-magnet” strategy for EV and defense sectors. Commissioning of a heavy rare earth separation circuit in 2026 will enable production of dysprosium and terbium domestically. Strategic financing through EXIM Bank and prior $400 million DoD investment provides pricing stability and capital support for refining expansion. The 10X Facility is designed to scale magnet production by directly utilizing internally leached oxides. Financial performance, including positive Q4 2025 EPS, reflects improving resilience during refinery ramp-up.

Energy Fuels establishes low-cost hydrometallurgical leadership with radionuclide handling and solvent extraction expertise

Energy Fuels Inc. is positioning itself as a competitive rare earth processor through low-cost leaching and advanced solvent extraction capabilities. Its Bankable Feasibility Study indicates an all-in production cost of $29.39/kg NdPr, placing it among the lowest-cost producers globally. Expansion plans target 6,000 tpa NdPr, 240 tpa Dy, and 66 tpa Tb, with Phase 2 expected to supply up to 45% of U.S. rare earth demand. The White Mesa Mill enables integrated processing of monazite sands into high-purity oxides using existing infrastructure. Licensed handling of uranium and thorium allows monetization of byproducts, with over 1 million lbs of U3O8 produced in 2025. Long-term EBITDA projections of $311 million annually highlight strong economic viability supported by decades of SX expertise.

Iluka builds large-scale integrated leaching refinery with government-backed critical minerals financing

Iluka Resources Limited is developing the Eneabba refinery as a fully integrated rare earth processing hub combining roasting, leaching, and solvent extraction. The facility targets a nameplate capacity of 17,500 to 23,000 tpa of rare earth oxides, positioning it among the largest outside China. Government-backed financing through the $2 billion Critical Minerals Facility supports processing of both internal and third-party concentrates. The cracking and leaching process utilizes high-temperature acid treatment followed by impurity removal to produce magnet-grade oxides. Engineering execution by Fluor ensures large-scale hydrometallurgical deployment aligned with 2025–2026 production timelines. Focus on Nd, Pr, Dy, and Tb aligns with high-demand applications in EVs and renewable energy.

Solvay advances circular leaching chemistry with recycled feedstocks and high-purity oxide production

Solvay is strengthening its position in rare earth leaching chemicals through circular economy integration and advanced purification technologies. Its La Rochelle facility processes recycled mixed rare earth oxides under a closed-loop supply agreement, reducing reliance on primary extraction. The site maintains a capacity of 600 mt/year of Pr-Nd oxide, supporting demand from EV and wind energy sectors. Product lines such as Actalys®, Optalys®, and Zenus® utilize high-purity leached compounds for catalysts and electronic applications. Participation in Europe’s €3 billion critical minerals initiative supports expansion of refining and magnet supply chains. Focus on recycling-based feedstocks enhances sustainability and supply security in rare earth processing.

Arafura advances integrated leaching and separation with Nolans project and byproduct value optimization

Arafura Rare Earths Limited is progressing the Nolans project as an integrated ore-to-oxide operation with advanced hydrometallurgical leaching stages. The facility targets a nameplate capacity of 4,440 tpa NdPr oxide supported by secured funding from Export Finance Australia, including $80 million COF and $200 million liquidity support. The process includes pre-leach, sulphation, and water leach stages, enabling efficient extraction and separation of rare earth elements. Production of 144,000 tpa fertilizer-grade phosphoric acid as a byproduct enhances overall project economics. Full permitting for radioactive waste management supports compliance with stringent ESG standards. Offtake negotiations covering up to 80% of nameplate output strengthen long-term revenue visibility with international partners.

United States: Defense-Led Price Guarantees and Closed-Loop Leaching Systems

The United States rare earth metals leaching chemicals ecosystem is being reshaped by direct federal intervention aimed at supply security and cost stabilization. In July 2025, the U.S. Department of Defense entered a strategic equity partnership with MP Materials, extending a $150 million loan to expand heavy rare earth separation at Mountain Pass, California. This intervention is structurally important for leaching chemical suppliers, as the DoD simultaneously established a 10-year price floor of $110 per kilogram for NdPr products, de-risking the high reagent consumption and energy intensity associated with advanced hydrometallurgical separation. The price guarantee allows operators to deploy more selective extractants, ion-exchange reagents, and multi-stage leaching chemistries without margin compression risk.

Parallel innovation is occurring across demonstration-scale and alternative feedstock projects. Rare Element Resources is scheduled to commission its Upton, Wyoming demonstration plant by late 2025, leveraging proprietary leaching and separation chemistry supported by a $4.4 million award from the Wyoming Energy Authority. At the same time, the U.S. Department of Energy issued targeted grants in 2025 for wastewater-based REE extraction, catalyzing demand for reagents capable of selectively leaching rare earths from coal acid mine drainage. Regulatory pressure in California has further accelerated the phase-out of legacy acids, pushing MP Materials toward closed-loop chemical systems that recycle more than 90% of process water. Looking ahead, U.S. processing hubs are preparing for AI-guided continuous-flow hydrometallurgical sequencing in 2026, a shift that is expected to improve extraction efficiency by roughly 10% through real-time reagent dosage optimization.

Australia: Integrated Ore-to-Oxide Strategy and Low-Energy Leaching Innovation

Australia is positioning itself as a vertically integrated rare earths hub, with leaching chemical demand anchored in large-scale refinery and mine development. Iluka Resources is advancing its $1.2 billion Eneabba Refinery, Australia’s first fully integrated rare earths refinery, with construction and equipment placement accelerating through the second half of 2025. This project underpins sustained demand for cracking and leaching reagents optimized for monazite and mixed rare earth concentrates. In parallel, the Nolans Bore Project led by Arafura Rare Earths integrated hybrid renewable energy systems in 2025 to power on-site extraction and separation, aligning leaching chemistry selection with lower-temperature and lower-emission operating windows while targeting 4,440 tonnes per year of NdPr oxide.

Government-backed financing and fiscal incentives are reinforcing this trajectory. In January 2025, the Australian Government committed A$200 million in equity through the National Reconstruction Fund to Arafura, explicitly securing the domestic ore-to-oxide chemical value chain. Australia’s 43.5% non-refundable R&D tax offset has further stimulated innovation in low-temperature leaching agents that reduce the energy intensity of monazite processing. At the operational level, Lynas Rare Earths implemented continuous flowsheet improvements at its Kalgoorlie processing facility in late 2025 to enhance cracking and leaching efficiency prior to downstream separation. Stricter 2025 updates to Western Australian environmental guidelines on thorium and uranium management have also forced leaching chemical suppliers to develop specialized precipitants capable of immobilizing radioactive byproducts at source.

France and the European Union: Circular Feedstocks and Solvometallurgical Leadership

France has emerged as the centerpiece of Europe’s rare earth leaching and separation strategy, anchored by industrial-scale capacity and policy-backed decarbonization. In April 2025, Solvay inaugurated a new production line at its La Rochelle facility, now the largest rare earth separation plant outside China capable of processing the full rare earth spectrum. This expansion materially increases European demand for high-selectivity leaching reagents and solvent extraction systems tailored for diverse feedstocks. Solvay’s 2025 partnership with Cyclic Materials further integrates recycled mixed rare earth oxides into the leaching stream, supporting the EU’s objective to meet 30% of rare earth demand from circular sources by 2030.

Technology direction in Europe is increasingly shaped by climate policy. Under the EU Clean Industrial Deal of 2025, solvometallurgy has been prioritized as a strategic pathway, with Solvay leading the development of non-aqueous leaching routes designed to cut CO₂ emissions from separation processes by up to 40%. Complementing this shift, French chemical clusters began piloting Deep Eutectic Solvents in late 2025, offering PFAS-free, low-toxicity alternatives for selective rare earth extraction. These designer solvents are gaining attention for their ability to decouple separation efficiency from environmental burden, strengthening Europe’s competitive positioning in sustainable rare earth processing.

China: Export Controls, Heavy REE Restrictions, and Digital Leaching Mandates

China continues to exert decisive influence over the global rare earth leaching chemicals landscape through policy controls and domestic modernization. On October 9, 2025, the Ministry of Commerce of China imposed immediate export controls on rare earth processing equipment and technologies, directly constraining global access to high-efficiency leaching catalysts and separation hardware. This was followed by expanded export restrictions effective November 8, 2025, covering five additional heavy rare earth elements, including holmium, erbium, thulium, europium, and ytterbium. These measures have tightened global availability of specialty leaching chemicals required for heavy REE extraction, amplifying geopolitical risk premiums outside China.

Domestically, regulatory pressure is accelerating technological renewal. The Ministry of Industry and Information Technology mandated equipment upgrades under its 2025 Industrial Modernization plan, forcing rare earth refineries to transition to digital-twin-controlled leaching tanks to meet 2026 energy-efficiency benchmarks. This shift is driving demand within China for advanced process-control reagents compatible with automated dosing and real-time monitoring. While these upgrades raise near-term capital and operating costs, they reinforce China’s long-term efficiency advantage in rare earth leaching and separation chemistry.

Comparative Snapshot: Rare Earth Metals Leaching Chemicals by Country

Rare Earth Metals Leaching Chemicals Market County Level Snapshot

|

Country / Region

|

Policy Anchor

|

Structural Impact on Leaching Chemicals

|

|

United States

|

Defense price floors and environmental regulation

|

High-selectivity reagents, closed-loop water systems, AI-guided dosing

|

|

Australia

|

Integrated ore-to-oxide strategy and R&D incentives

|

Low-temperature leaching agents, cracking optimization, radioactive control

|

|

France / EU

|

Clean Industrial Deal and circular economy targets

|

Solvometallurgy, DES adoption, recycled feedstock integration

|

|

China

|

Export controls and industrial modernization mandates

|

Constrained global supply, digital-twin leaching, heavy REE specialization

|

Rare Earth Metals Leaching Chemicals Market Report Scope

Rare Earth Metals Leaching Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1408.7 Million

|

|

Market Size (2034)

|

$2769.4 Million

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Chemical Type (Inorganic Acids, Organic Acids & Lixiviants, Chelating Agents & Extractants, Precipitating Agents, Green & Emerging Reagents), By Process Route (Hydrometallurgical Leaching, Pyrometallurgical Pre-Treatment, Solvent Extraction, Ion Exchange & Chromatography), By Application (Primary Mining & Refining, Secondary Recovery & Recycling, Tailings Processing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Solvay SA, BASF SE, Evonik Industries AG, Arkema SA, Dow Inc., Nippon Chemical Industrial Co. Ltd., Sino-Platinum Metals Co. Ltd., Inner Mongolia Baotou Steel Rare Earth Hi-Tech Co., Lynas Rare Earths Limited, MP Materials Corp., Arafura Rare Earths Limited, Umicore NV, IoLiTec GmbH, Lanxess AG, Aarti Industries Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Rare Earth Metals Leaching Chemicals Market Segmentation

By Chemical Type

- Inorganic Acids

- Organic Acids & Lixiviants

- Chelating Agents & Extractants

- Precipitating Agents

- Green & Emerging Reagents

By Process Route

- Hydrometallurgical Leaching

- Pyrometallurgical Pre-Treatment

- Solvent Extraction

- Ion Exchange & Chromatography

By Application

- Primary Mining & Refining

- Secondary Recovery & Recycling

- Tailings Processing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Rare Earth Metals Leaching Chemicals Industry

- Solvay SA

- BASF SE

- Evonik Industries AG

- Arkema SA

- Dow Inc.

- Nippon Chemical Industrial Co. Ltd.

- Sino-Platinum Metals Co. Ltd.

- Inner Mongolia Baotou Steel Rare Earth Hi-Tech Co.

- Lynas Rare Earths Limited

- MP Materials Corp.

- Arafura Rare Earths Limited

- Umicore NV

- IoLiTec GmbH

- Lanxess AG

- Aarti Industries Limited

*- List not Exhaustive