Global Remote Water Quality Monitoring Systems Market Overview

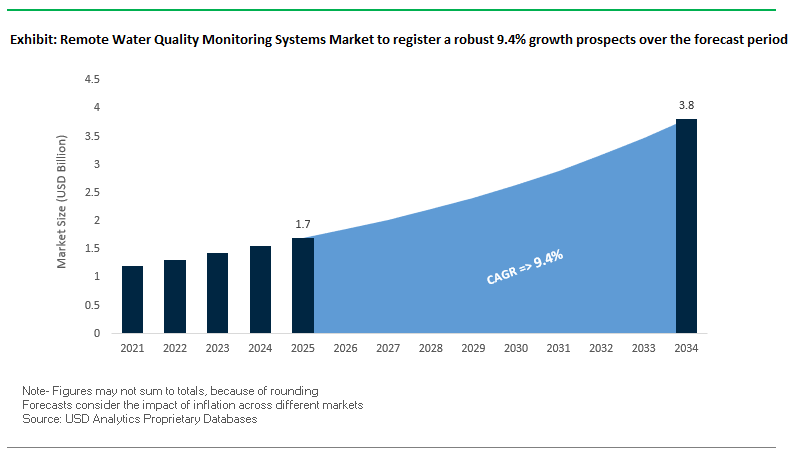

The global remote water quality monitoring systems market is forecasted to grow from $1.7 billion in 2025 to $3.8 billion by 2034, registering a CAGR of 9.4%. This growth is driven by stringent regulatory mandates, rapid urban infrastructure development, and increasing adoption of IoT-enabled water monitoring solutions. Governments worldwide, including the U.S. Environmental Protection Agency (EPA) and India’s Central Pollution Control Board (CPCB), are enforcing stricter water quality standards, compelling utilities and industries to adopt advanced remote monitoring technologies.

The market benefits from growing investments in smart city initiatives and urban water infrastructure, as seen in Navi Mumbai’s “E-System Water Sample Inspection Report and Water Quality Monitoring System” (August 2025), which digitizes and streamlines water quality processes. Remote monitoring solutions reduce the need for manual sampling and laboratory analysis, improving operational efficiency, lowering costs, and enabling real-time response to contamination events.

Technological integration is a key market driver. The use of IoT, cloud computing, AI, and hybrid sensor systems allows predictive water quality analysis and comprehensive monitoring across municipal, industrial, and environmental applications.

Key Insights for Industry Stakeholders:

- Regulatory compliance is driving demand for advanced remote water quality monitoring systems.

- Smart city and urban infrastructure projects increase adoption of IoT-enabled monitoring solutions.

- Real-time monitoring reduces operational costs and enables faster response to contamination events.

- Integration with AI and predictive analytics enhances water resource management.

- Hybrid in-situ and remote sensing systems provide a holistic approach to water quality analysis.

Market Analysis: Recent Developments in Remote Water Quality Monitoring

The remote water quality monitoring systems market has witnessed multiple technological innovations and strategic initiatives. In April 2025, OTT HydroMet launched the OTT Flood Monitoring System, integrating the OTT SensorLink 1000 IoT device with the RLS 500 radar sensor to provide high-accuracy, low-maintenance water level and quality measurements across diverse environments. This reflects a broader industry trend toward integrating IoT for precise and reliable monitoring.

In March 2025, an academic review emphasized the growing use of IoT, AI, and machine learning for predictive water quality analysis. Hybrid systems combining in-situ sensors with remote sensing are gaining prominence, offering enhanced predictive insights. February 2025 saw advancements in miniaturized sensors and cloud-based integration, enabling real-time monitoring and streamlined data access. Further supporting market growth, January 2025 updates from India’s CPCB under the NWMP highlight increasing demand for continuous and regulatory-compliant monitoring technologies.

Other notable developments include YSI’s EXO Multiparameter Sonde platform (November 2024) for long-term, continuous water monitoring and In-Situ Inc.’s acquisition of ChemScan (October 2024) to expand real-time drinking water and wastewater monitoring solutions. Additionally, Hach’s new fluorometer methods (June 2024) cater to ultra-low-range chlorine and sulfite measurements, while Libelium’s Waspmote Plug & Sense! sensor expansion (March 2024) enhances versatility for potable water and seawater monitoring applications.

Key Trends Driving Adoption of Remote Water Quality Monitoring

Regulatory Mandates Push Real-Time Monitoring Implementation

The remote water quality monitoring systems market is being strongly influenced by stringent regulations requiring real-time data collection and reporting. Agencies such as the U.S. EPA through its NPDES program and India’s Jal Jeevan Mission are shifting from periodic manual sampling to continuous, remote monitoring, driving adoption of advanced systems. Programs like India’s nationwide training of over 2.2 million women for water testing using Field Testing Kits (FTKs) demonstrate the global push for decentralized and digitized water quality surveillance. The CPCB in India further reinforces this trend with initiatives promoting Online Continuous Effluent Monitoring Systems (OCEMS), enabling regulators to take immediate action, highlighting regulatory compliance as a prime market driver.

IoT and AI Integration Enables Predictive Water Quality Management

Technological advancement is transforming water monitoring from reactive to predictive management, leveraging IoT sensors and AI-driven analytics. Studies published in 2025 highlight AI’s ability to process large-scale sensor data with up to 40% higher efficiency and 30% lower error rates compared to traditional methods. Companies such as Aquanomix are commercializing these solutions, enabling utilities and educational institutions to detect anomalies, leaks, and blockages early. This proactive approach minimizes public health risks, optimizes resource allocation, and reduces operational downtime, positioning remote monitoring as a strategic tool rather than a mere compliance solution.

Public-Private Partnerships Accelerate Infrastructure Modernization

PPPs are becoming a key enabler for deploying advanced remote monitoring systems in water infrastructure. The World Bank’s PPP framework emphasizes private sector efficiency and technology integration to enhance operational and financial sustainability. In India, hybrid annuity-based PPP models in cities like Ayodhya and Prayagraj allow private operators to implement smart water systems with long-term public oversight. These models support deployment of performance-based operations, ensuring regulatory compliance, modernizing aging infrastructure, and encouraging market growth for remote monitoring technologies.

Market Opportunities in Remote Water Quality Monitoring

The Remote Water Quality Monitoring Systems Market offers substantial opportunities for technology providers and service integrators. Growth is driven by increasing regulatory stringency, environmental awareness, and the need for operational efficiency, particularly in municipalities and industrial facilities. Providers offering integrated hardware-software solutions, predictive analytics, and managed services can capture recurring revenue streams while enabling proactive water management. Expanding applications such as source water protection, industrial effluent optimization, and public health monitoring further position remote water quality monitoring as a critical tool for sustainable water management, making it a strategic investment area for both public and private stakeholders.

Market Share Analysis of Remote Water Quality Monitoring Systems

Hardware and Software-Driven Services Define Market Share by Component

By component, hardware dominates with 55–60% of the market, covering multi-parameter sensors, probes, data loggers, telemetry units, and protective housings. The high capital intensity and technological sophistication of sensors and communication modules drive this segment’s prominence. Meanwhile, software & services (44.1%) are rapidly growing, offering cloud-based platforms, predictive analytics, visualization, and system integration. These solutions transform raw data into actionable insights, enabling utilities and agencies to optimize operations, reduce regulatory risks, and monetize performance analytics, creating a sustainable recurring revenue model.

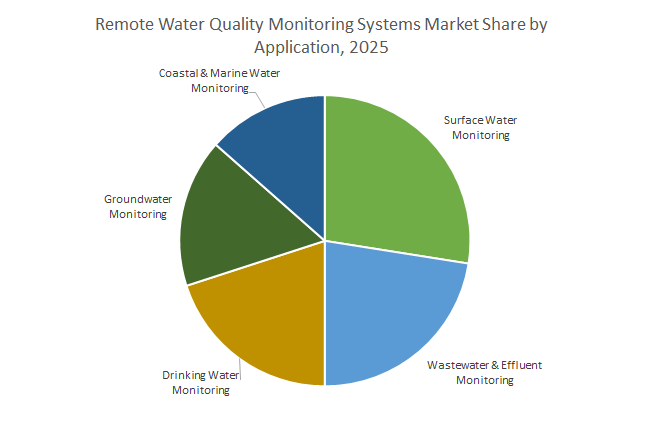

Environmental Monitoring Applications Lead Market Share by Application

In terms of application, surface water monitoring (26.9%) commands the largest share, driven by regulatory compliance and the need to protect rivers, lakes, and reservoirs. Wastewater and effluent monitoring (22.5%) is a high-growth segment, as industries and municipalities require continuous data for NPDES compliance and process optimization. Drinking water monitoring ensures public health by tracking water quality from source to tap, while groundwater monitoring focuses on contamination detection and resource management. Coastal and marine water monitoring addresses aquaculture and ecosystem health, reflecting the market’s diverse application spectrum.

Government and Industrial Users Drive Market Share by End-User

By end-user, government agencies (32.8%) are the largest segment, deploying extensive networks for environmental protection, watershed management, and public reporting. Industrial facilities (26.9%), including food & beverage, chemicals, power, and mining, adopt remote monitoring for effluent compliance and process optimization, reducing sewer surcharges and regulatory risk. Municipal water treatment plants (16.9%) and wastewater facilities (11.8%) leverage these systems for real-time process control, enhancing operational efficiency, reducing chemical and energy usage, and improving service reliability. Research institutions and universities utilize monitoring systems for ecological studies and technology development, while commercial applications serve aquaculture, agriculture, and large commercial operations, demonstrating the market’s broad end-user adoption.

United States: PFAS Compliance and Digital Transformation Fuel Adoption

The United States is witnessing robust growth in the remote water quality monitoring systems market, driven by government initiatives, regulatory mandates, and corporate innovation. The U.S. Environmental Protection Agency (EPA) leverages the Bipartisan Infrastructure Law (BIL), providing over $50 billion to modernize water infrastructure and encourage the adoption of digital water technologies, including remote monitoring systems. Section 106 grants further support ambient water quality monitoring programs across states. Regulatory pressures, such as the EPA’s new PFAS Maximum Contaminant Levels, are driving utilities and industrial operators to implement advanced remote monitoring solutions. Companies are introducing innovations like Siemens’ Water Quality Analytics as a Service (WQAaaS), which delivers real-time data and predictive insights, while federal agencies like the U.S. General Services Administration (GSA) deploy baseline water tests and monitoring best practices. Key applications include urban water management, regulatory compliance, and efficiency optimization for municipal and industrial water utilities.

China: Smart Urban Water Management Through IoT and AI Integration

China’s remote water quality monitoring systems market is propelled by ambitious urban infrastructure programs and technological innovation. The "Sponge City" initiative aims to ensure more than 80% of urban built-up areas meet stormwater management standards by 2030, necessitating extensive deployment of remote monitoring systems. Smart water management (SWM) is driving the integration of IoT, AI, big data analytics, and digital twin modeling for real-time monitoring, predictive analysis, and sustainable urban water governance. Government efforts to promote water-saving irrigation (WSI) further enhance the adoption of remote monitoring in agricultural and industrial sectors. The market is largely fueled by applications in urban flooding mitigation, rainwater management, and industrial/municipal water quality improvement.

India: IoT-Based Rural Monitoring and AI-Driven Solutions

In India, government initiatives, regulatory frameworks, and technological advancements are driving the remote water quality monitoring systems market. The Jal Jeevan Mission has deployed first-of-its-kind sensor-based IoT devices to monitor rural drinking water supply in over six lakh villages, enabling near real-time reporting without manual intervention. The Central Pollution Control Board (CPCB) maintains the National Water Quality Monitoring Programme (NWMP), updating water quality data frequently for public access. Corporate partnerships, such as Pani Energy with Murugappa Water Technology & Solutions in 2024, highlight a shift toward AI-driven, technology-based services rather than simple hardware supply. Market demand is primarily driven by the need to improve rural water quality, address challenges from urbanization and industrialization, and support sustainable sanitation practices.

Germany: Regulatory Compliance and Digital Innovation in Industrial Water Monitoring

Germany’s market growth is strongly influenced by stricter EU regulations, technological advancement, and corporate initiatives. The revised EU Urban Wastewater Treatment Directive (January 2025) mandates a "4th purification stage" to remove micropollutants, driving demand for advanced monitoring systems. Cities are adopting digital twins, AI, and predictive analytics to optimize water management, which is crucial for remote monitoring system deployment. German companies like H2O GmbH and GEA Group AG are providing innovative and sustainable solutions, including service-based models for Zero Liquid Discharge (ZLD) and industrial wastewater management. Key applications include industrial compliance, micropollutant monitoring, and operational efficiency improvements in municipal and industrial water networks.

Australia: Infrastructure Investment and Advanced Remote Sensing Technologies

Australia’s remote water quality monitoring systems market is supported by significant infrastructure investment, strict environmental regulations, and technological advancement. Sydney Water announced a $34 billion investment over 10 years, including projects like the Mamre Road Precinct Stormwater initiative, which incorporates remote monitoring systems. State environmental protection policies guide water management to maintain ecosystem quality and safeguard water resources. The Commonwealth Scientific and Industrial Research Organisation (CSIRO) is leading innovation in remote sensing and data analytics, developing satellite-based and ground sensor technologies to monitor large water bodies efficiently. Applications focus on stormwater management, water conservation, and compliance with environmental standards.

Japan: Advanced Sensor Integration and Decentralized Water Management

Japan’s remote water quality monitoring systems market is shaped by government initiatives, cutting-edge technological development, and industrial innovation. The Ministry of Land, Infrastructure, Transport and Tourism (MLIT) launched the A-JUMP project to promote Membrane Bioreactor (MBR) technology as a foundation for advanced wastewater treatment, which complements remote monitoring systems. Japanese companies and research institutions, including Toray Industries Inc., specialize in high-precision sensors for industrial and greywater monitoring, facilitating decentralized and on-site water recycling. Key applications include water conservation, compliance with stringent industrial water quality standards, and development of sustainable residential and commercial water reuse solutions.

Competitive Landscape of Remote Water Quality Monitoring Systems Market

The remote water quality monitoring systems market is highly competitive, with leading players emphasizing technological innovation, integration, and service flexibility. Companies are expanding portfolios to provide end-to-end solutions for municipal, industrial, and environmental water monitoring.

Xylem Inc. (YSI) is a leader in multiparameter water quality monitoring

Xylem Inc.’s YSI brand is a global leader in water quality instrumentation, offering multiparameter sondes, handheld meters, and data buoy systems. Their EXO sonde platform features durable titanium-sealed sensors and anti-fouling wipers for long-term deployments. Strategically, Xylem integrates solutions through its HydroSphere platform, enabling cloud-based data visualization and real-time decision-making. Recent innovations include the HydroRIG remote intelligent gateway (August 2025), simplifying data logging and remote connectivity for clients.

Hach (A Danaher Company) provides comprehensive water quality solutions

Hach is renowned for its reliable instrumentation and reagents for laboratory and field use. Its extensive product line includes sensors, analyzers, and controllers for parameters such as pH, turbidity, chlorine, and dissolved oxygen. Advanced systems like the Prognosys predictive diagnostic platform support proactive water management. Hach emphasizes complete solutions, exemplified by its partnership with 120Water (September 2020) for lead and copper compliance testing. The company also earned a Gold Medal sustainability rating (December 2022), reflecting its commitment to responsible practices.

OTT HydroMet specializes in integrated hydrological monitoring solutions

OTT HydroMet excels in hydrological and meteorological monitoring, offering integrated sensors and systems for water level, flow, and quality. The OTT Flood Monitoring System demonstrates the company’s focus on high-accuracy, low-maintenance solutions. OTT HydroMet expanded its UK operations in March 2023, reinforcing regional presence and market penetration. Its strategic focus remains on providing flexible, efficient, and integrated flood and stream monitoring solutions.

In-Situ Inc. delivers robust groundwater and surface water monitoring

In-Situ Inc. is recognized for rugged in-well monitoring equipment and solutions for challenging environments. Its TROLL® and Aqua TROLL series offer multiparameter monitoring with all-in-one data logging capabilities. The acquisition of ChemScan (2019) enhanced its real-time drinking water and wastewater monitoring offerings. In-Situ emphasizes customer support and rental services, providing flexible access to high-performance equipment for short- and long-term applications.

Libelium offers highly customizable IoT sensor platforms

Libelium specializes in modular IoT solutions, including water quality monitoring through its Plug & Sense! platform. The platform supports easy addition or replacement of sensor probes and offers enhanced performance through the Smart Water Xtreme line. Libelium’s systems ensure interoperability with various cloud services and IoT networks, enabling large-scale environmental monitoring projects. The company’s modular approach allows highly customized solutions for municipal, industrial, and environmental water management.

Remote Water Quality Monitoring Systems Market Report Scope

Remote Water Quality Monitoring Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.7 Billion

|

|

Market Size (2034)

|

$3.8 Billion

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Component (Hardware, Software & Services), By Application (Surface Water Monitoring, Groundwater Monitoring, Coastal & Marine Water Monitoring, Wastewater & Effluent Monitoring, Drinking Water Monitoring), By End-User (Government Agencies, Industrial, Commercial, Research Institutions & Universities, Municipal Water Treatment Plants, Wastewater Treatment Facilities), By Deployment Type (Fixed/Stationary Monitoring Systems, Portable/Mobile Monitoring Systems, Submersible/Sensor Buoys), By Communication Technology (Cellular, Satellite, Radio Frequency, Wi-Fi)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Xylem Inc., Danaher Corporation (Hach), ABB Ltd., Thermo Fisher Scientific, Emerson Electric Co., Siemens, SUEZ, Veolia, Endress+Hauser, Horiba, Ltd., Pentair plc, V.A. Tech Wabag Ltd., Kurita Water Industries Ltd., Mitsubishi Chemical Corporation, Badger Meter

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Remote Water Quality Monitoring Systems Market Segmentation

By Component

- Hardware

- Sensors & Probes

- Data Loggers & Telemetry Systems

- Samplers

- Communication Modules

- Remote Stations/Buoys

- Software & Services

By Application

- Surface Water Monitoring

- Groundwater Monitoring

- Coastal & Marine Water Monitoring

- Wastewater & Effluent Monitoring

- Drinking Water Monitoring

By End-User

- Government Agencies

- Industrial

- Commercial

- Research Institutions & Universities

- Municipal Water Treatment Plants

- Wastewater Treatment Facilities

By Deployment Type

- Fixed/Stationary Monitoring Systems

- Portable/Mobile Monitoring Systems

- Submersible/Sensor Buoys

By Communication Technology

- Cellular (4G/LTE, 5G)

- Satellite

- Radio Frequency (RF)

- Wi-Fi

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Remote Water Quality Monitoring Systems Industry include-

- Xylem Inc.

- Danaher Corporation (Hach)

- ABB Ltd.

- Thermo Fisher Scientific

- Emerson Electric Co.

- Siemens

- SUEZ

- Veolia

- Endress+Hauser

- Horiba, Ltd.

- Pentair plc

- V.A. Tech Wabag Ltd.

- Kurita Water Industries Ltd.

- Mitsubishi Chemical Corporation

- Badger Meter

*- List not Exhaustive

Research Coverage USDAnalytics

This report investigates the Global Remote Water Quality Monitoring Systems Market, highlighting breakthroughs in IoT-enabled sensing, cloud analytics, AI-based anomaly detection, and hybrid in-situ/remote sensing architectures; it analysis reviews regulatory catalysts (EPA, CPCB), smart-city investments, and vendor strategies shaping real-time compliance and risk mitigation. It highlights how continuous monitoring cuts manual sampling costs, accelerates contamination response, and unlocks predictive OPEX savings across municipal, industrial, coastal/marine, and source-to-tap use cases. Mapping component, application, deployment, and connectivity trajectories to 2034, this report is an essential resource for utilities, environmental regulators, EPC integrators, and technology leaders seeking scalable, interoperable platforms and recurring-revenue service models grounded in USDAnalytics’ comparative benchmarks and ROI pathways for digitized water governance. Scope Includes-

- By Component: Hardware (Sensors & Probes; Data Loggers & Telemetry; Samplers; Communication Modules; Remote Stations/Buoys); Software & Services

- By Application: Surface Water; Groundwater; Coastal & Marine; Wastewater & Effluent; Drinking Water

- By End-User: Government Agencies; Industrial; Commercial; Research Institutions & Universities; Municipal Water Treatment Plants; Wastewater Treatment Facilities

- By Deployment Type: Fixed/Stationary; Portable/Mobile; Submersible/Sensor Buoys

- By Communication Technology: Cellular (4G/LTE, 5G); Satellite; RF; Wi-Fi

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic & Forecast Window: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Analysis/ profiles of 15+ companies, include the list of given companies): Xylem Inc.; Danaher Corporation (Hach); ABB Ltd.; Thermo Fisher Scientific; Emerson Electric Co.; Siemens; SUEZ; Veolia; Endress+Hauser; Horiba, Ltd.; Pentair plc; V.A. Tech Wabag Ltd.; Kurita Water Industries Ltd.; Mitsubishi Chemical Corporation; Badger Meter.

Methodology

USDAnalytics applies a bottom-up model anchored in hardware shipments, installed node counts, sensor mix (% multiparameter vs. single-parameter), and software subscription attach rates, with top-down validation using utility budgets, grant flows, and smart-city procurement data. Primary research includes interviews with utilities, regulators, OEMs, and system integrators; secondary inputs span compliance rulebooks (NPDES, OCEMS), tender outcomes, and peer-reviewed studies on AI/IoT efficacy. Forecasts (2025–2034) incorporate scenario weights for regulation tightening, network coverage (cellular/LPWAN/satellite), and component cost curves (sensors, telemetry, power). A TCO/ROI framework benchmarks manual-sampling baselines vs. continuous monitoring (alarms, false-positive rates, truck rolls avoided), while sensitivity tests quantify impacts of probe fouling, calibration intervals, and data-hosting choices on lifecycle economics.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Remote Water Quality Monitoring Systems Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. Remote Water Quality Monitoring Systems Market Outlook (2025–2034)

2.1. Introduction: From Manual Testing to Real-Time Intelligence

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $1.7 Billion

2.2.2. Forecasted Market Size (2034): $3.8 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 9.4%

2.3. Market Drivers and Challenges

2.3.1. Drivers: Stringent Regulations, Smart City Initiatives, and IoT Integration

2.3.2. Challenges: High Initial Costs and Connectivity Issues

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments (2024–2025)

3.1. Market Trend: Regulatory Mandates Push Real-Time Monitoring

3.2. Market Trend: IoT and AI Integration Enables Predictive Management

3.3. Market Trend: Public-Private Partnerships Accelerate Infrastructure Modernization

3.4. Recent Developments & Strategic Moves

4. Remote Water Quality Monitoring Systems Market – Segmentation Insights (2025–2034)

4.1. By Component

4.1.1. Hardware (55-60% Market Share)

4.1.2. Software & Services (44.1% Market Share)

4.2. By Application

4.2.1. Surface Water Monitoring (26.9% Market Share)

4.2.2. Wastewater & Effluent Monitoring (22.5% Market Share)

4.2.3. Drinking Water Monitoring

4.2.4. Groundwater Monitoring

4.2.5. Coastal & Marine Water Monitoring

4.3. By End-User

4.3.1. Government Agencies (32.8% Market Share)

4.3.2. Industrial Facilities (26.9% Market Share)

4.3.3. Municipal Water Treatment Plants (16.9% Market Share)

4.3.4. Wastewater Treatment Facilities (11.8% Market Share)

4.3.5. Research Institutions & Universities

4.3.6. Commercial Establishments

4.4. By Deployment Type

4.4.1. Fixed/Stationary Monitoring Systems

4.4.2. Portable/Mobile Monitoring Systems

4.4.3. Submersible/Sensor Buoys

4.5. By Communication Technology

4.5.1. Cellular (4G/LTE, 5G)

4.5.2. Satellite

4.5.3. Radio Frequency (RF)

4.5.4. Wi-Fi

5. Country Analysis and Outlook: Remote Water Quality Monitoring Systems Market

5.1. United States: PFAS Compliance and Digital Transformation Fuel Adoption

5.2. China: Smart Urban Water Management Through IoT and AI Integration

5.3. India: IoT-Based Rural Monitoring and AI-Driven Solutions

5.4. Germany: Regulatory Compliance and Digital Innovation in Industrial Water Monitoring

5.5. Australia: Infrastructure Investment and Advanced Remote Sensing

5.6. Japan: Advanced Sensor Integration and Decentralized Water Management

6. Market Size Outlook by Region (2025-2034)

6.1. North America Remote Water Quality Monitoring Systems Market Size Outlook to 2034

6.1.1. By Component

6.1.2. By Application

6.1.3. By End-User

6.1.4. By Deployment Type

6.1.5. By Communication Technology

6.1.6. By Country (U.S., Canada, Mexico)

6.2. Europe Remote Water Quality Monitoring Systems Market Size Outlook to 2034

6.2.1. By Component

6.2.2. By Application

6.2.3. By End-User

6.2.4. By Deployment Type

6.2.5. By Communication Technology

6.2.6. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific Remote Water Quality Monitoring Systems Market Size Outlook to 2034

6.3.1. By Component

6.3.2. By Application

6.3.3. By End-User

6.3.4. By Deployment Type

6.3.5. By Communication Technology

6.3.6. By Country (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.4. South America Remote Water Quality Monitoring Systems Market Size Outlook to 2034

6.4.1. By Component

6.4.2. By Application

6.4.3. By End-User

6.4.4. By Deployment Type

6.4.5. By Communication Technology

6.4.6. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa Remote Water Quality Monitoring Systems Market Size Outlook to 2034

6.5.1. By Component

6.5.2. By Application

6.5.3. By End-User

6.5.4. By Deployment Type

6.5.5. By Communication Technology

6.5.6. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Company Profiles: Leading Players

7.1. Xylem Inc. (YSI)

7.1.1. Company Overview

7.1.2. Product Portfolio & Strategic Focus

7.1.3. Recent Developments

7.2. Danaher Corporation (Hach)

7.2.1. Company Overview

7.2.2. Comprehensive Water Quality Solutions

7.2.3. Recent Developments and Market Position

7.3. ABB Ltd.

7.4. SUEZ

7.5. Veolia

7.6. Endress+Hauser

7.7. OTT HydroMet

7.8. In-Situ Inc.

7.9. Libelium

7.10. Other Key Players

7.10.1. Thermo Fisher Scientific

7.10.2. Emerson Electric Co.

7.10.3. Siemens

7.10.4. Horiba, Ltd.

7.10.5. Pentair plc

7.10.6. V.A. Tech Wabag Ltd.

7.10.7. Kurita Water Industries Ltd.

7.10.8. Mitsubishi Chemical Corporation

7.10.9. Badger Meter

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures