Residential Architectural Coatings Market Size, Housing Demand, and Sustainability Transition

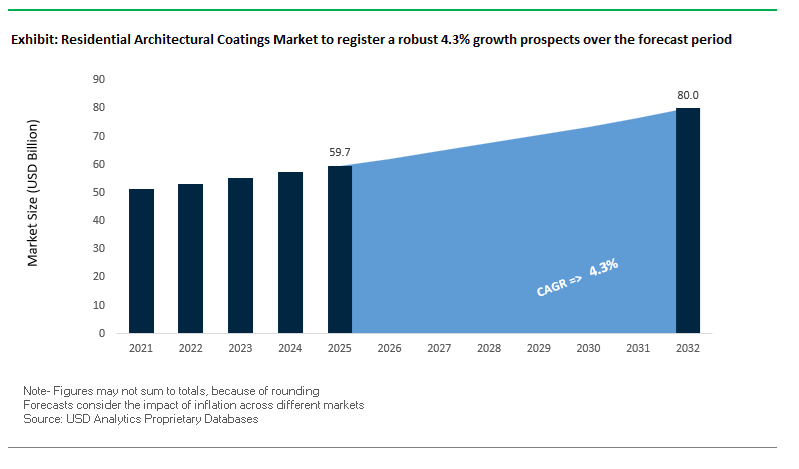

The global Residential Architectural Coatings Market was valued at $59.7 billion in 2025 and is projected to reach $80.2 billion by 2032, expanding at a CAGR of 4.3%. The market is structurally supported by urban housing expansion, renovation cycles in mature economies, and increasing consumer preference for high-performance, low-emission coatings.

Demand is particularly resilient due to the non-discretionary nature of residential repainting and maintenance, combined with rising investments in new housing construction across Asia-Pacific, the Middle East, and parts of Latin America. In emerging economies, Tier-2 and Tier-3 urbanization is creating sustained volume demand for both interior decorative paints and exterior weather-resistant coatings, while developed markets are driven more by premiumization and refurbishment cycles.

A major transformation driver is the shift toward sustainable and health-conscious formulations, including low-VOC, zero-VOC, and bio-based coatings. Regulatory frameworks in North America and Europe, alongside rising consumer awareness, are accelerating adoption of coatings that improve indoor air quality and reduce environmental impact.

Additionally, the market is witnessing a shift from purely decorative coatings to functional coatings, including those offering anti-microbial protection, stain resistance, self-cleaning properties, and thermal insulation benefits. These value-added features are increasingly influencing purchasing decisions, especially in high-density urban housing environments.

Market Analysis: Low-VOC Formulations, Radiative Cooling Technologies, and Consumer-Centric Innovation Driving Market Evolution

The Residential Architectural Coatings Market is undergoing a significant evolution driven by material innovation, consumer behavior insights, and regulatory compliance pressures.

A key innovation trend is the emergence of passive cooling technologies. In May 2025, AkzoNobel introduced a radiative cooling coating system capable of reducing residential surface temperatures by up to 10%, directly addressing the urban heat island effect. This development reflects a broader shift toward coatings that actively contribute to building energy efficiency rather than just protection and aesthetics.

Health and sustainability continue to shape product development. PPG’s ANTI-SCUFF Zero VOC interior paint (2025) targets high-traffic residential spaces, combining durability with improved indoor air quality, while Benjamin Moore’s Eco Spec® line pushes the boundary on low-odor, ultra-low emission coatings. These launches highlight how performance and environmental compliance are converging into a single product requirement.

Bio-based innovation is also gaining traction. AkzoNobel’s RUBBOL WF 3350, containing 20% bio-based materials, demonstrates how manufacturers are integrating renewable feedstocks into mainstream residential coatings without compromising durability for exterior applications such as windows and wooden trims.

From a consumer behavior standpoint, color psychology and personalization trends are becoming critical differentiators. Behr’s “Hidden Gem” (2026 Color of the Year) reflects a shift toward emotion-driven purchasing, with research indicating that 67% of consumers seek calming and expressive interior environments. This is influencing not only color portfolios but also the development of coatings capable of delivering deep, consistent finishes with minimal coats.

Market Trend: Strategic capacity expansion and localization are reshaping competitive positioning across the Residential Architectural Coatings Market.

In March 2026, Sherwin-Williams completed a major expansion of its Kentucky facility, increasing production capacity by 60%. This move is directly aligned with rising demand for metal roofing and siding coatings in North America, particularly in suburban residential developments. It also reflects a broader industry trend toward automated, high-efficiency manufacturing to manage cost pressures and supply chain volatility.

Emerging markets continue to act as primary growth engines. Jotun’s record revenue performance (2026) underscores strong demand in Southeast Asia and the Middle East, where rapid urbanization and climate-specific requirements are driving adoption of localized coating technologies, including “stay-clean” and dust-resistant formulations for harsh environmental conditions.

In India, Asian Paints is leveraging digitalization to transform the residential buying experience. The integration of visualization tools and smart coating technologies allows consumers to preview finishes and functional benefits such as antimicrobial protection, signaling a shift toward digitally enabled, experience-driven retail models.

Meanwhile, companies like Caparol are expanding their premium retail footprint in the Middle East, targeting high-end residential segments with energy-efficient and regulation-compliant coatings, aligning with stricter green building mandates across GCC countries.

Market Trend: California Title 24 VOC Limits Standardizing Ultra-Low VOC Architectural Coatings Across North America

The residential architectural coatings market in North America is undergoing a structural shift as the 2025 revision of California Title 24 (effective January 1, 2026) enforces significantly lower VOC thresholds for paints, primers, and related materials used in residential construction. This regulatory update is aligned with California’s broader objective to reduce smog-forming emissions from the built environment by 20% by 2030, directly influencing formulation strategies across the coatings value chain.

The updated limits impose a maximum VOC content of 50 g/L for flat coatings and 100 g/L for non-flat coatings, effectively eliminating legacy solvent-heavy formulations from the California market. These thresholds are forcing manufacturers to accelerate the transition toward waterborne acrylics, high-solids coatings, and hybrid resin systems that can deliver performance without exceeding emission limits.

The impact extends beyond decorative paints into adjacent product categories. Architectural primers, specialty sealants, and substrate-specific adhesives are now subject to VOC caps ranging from 50 g/L to 250 g/L, depending on application. This is increasing pressure on formulators to develop multifunctional systems that combine adhesion, durability, and environmental compliance within stricter chemical constraints.

Given that California accounts for more than 10% of total U.S. residential construction activity, these regulatory changes are effectively setting a de facto national standard. Major coatings manufacturers are standardizing low-VOC production across North America to streamline logistics, reduce SKU complexity, and ensure compliance across multiple jurisdictions. This is accelerating the industry-wide transition toward ultra-low VOC architectural coatings as the baseline product category.

Market Opportunity: China GB 18582-2024 Driving Shift Toward Ultra-Low VOC and SVOC-Free Interior Coatings

China’s implementation of GB 18582-2024, supported by the Ministry of Ecology and Environment, represents a significant escalation in regulatory rigor for residential architectural coatings. The standard expands beyond traditional VOC limits to include enforceable thresholds for semi-volatile organic compounds, addressing long-term indoor air quality concerns in high-density residential environments.

The regulation mandates VOC limits of less than 80 g/L for water-based interior wall coatings while introducing the industry’s first formal controls on SVOCs, which are associated with prolonged off-gassing and indoor pollution. This is driving a shift toward advanced resin chemistries, low-emission additives, and encapsulated functional materials designed to minimize emissions over the product lifecycle.

Restrictions on hazardous substances are also tightening. The updated standard significantly reduces allowable concentrations of biocides and halogenated hydrocarbons, requiring manufacturers to replace traditional preservatives with safer, bio-based or encapsulated alternatives. This is increasing formulation complexity while creating opportunities for innovation in sustainable coating technologies.

Analytical requirements have become more stringent, with mandatory gas chromatography-mass spectrometry testing introduced for 14 regulated substances, including phthalates and polycyclic aromatic hydrocarbons. This has increased quality control and compliance costs for regional coating manufacturers by approximately 40%, reinforcing the need for advanced testing infrastructure and robust supply chain validation.

These regulatory developments are elevating performance expectations in the Chinese residential coatings market, where ultra-low emission and health-focused coatings are rapidly becoming the standard.

Market Opportunity: Formaldehyde-Scavenging Interior Paints Emerging as Premium IAQ Solutions in China’s Residential Market

The growing emphasis on indoor air quality is creating a high-value opportunity for formaldehyde-scrubbing paints in China’s residential coatings segment. Driven by the GB/T 39600-2024 indoor air quality framework, these advanced coatings are designed not only to minimize emissions but also to actively remove harmful pollutants from indoor environments.

Unlike conventional low-VOC paints, which primarily reduce the introduction of volatile compounds, formaldehyde-scavenging coatings incorporate reactive additives that chemically bind and neutralize formaldehyde molecules present in indoor air. Performance benchmarks for 2026 indicate purification efficiencies exceeding 80% within 24 hours of application, significantly improving indoor air conditions in newly constructed or renovated homes.

These coatings also support compliance with China’s “ENF” (No-Addition Formaldehyde) certification, which is increasingly recognized as a premium standard in residential construction. Developers targeting health-conscious consumers are leveraging this certification as a differentiator in high-end housing projects, particularly in Tier-1 urban markets.

Consumer demand trends reinforce this opportunity. Surveys conducted in major Chinese cities indicate that approximately 65% of residential renovation projects in 2026 prioritize active air purification coatings over traditional aesthetic considerations. This shift reflects a broader movement toward health-centric building materials and creates a strong growth trajectory for functional architectural coatings.

Residential Architectural Coatings Market Share and Segmentation Insights: Repaint Cycle Dominance and Big-Box Retail Leadership

By Project Type: Repaint and Maintenance Segment Drives Consistent Demand Across Housing Markets

The repaint and maintenance segment dominated the residential architectural coatings market with a 66.4% share in 2025, fueled by the recurring repaint cycle and the vast global housing stock. Homeowners typically repaint interior surfaces every 3–7 years and exterior surfaces every 5–10 years, creating a stable, non-cyclical demand for interior paints, exterior coatings, primers, and decorative finishes. This recurring consumption pattern ensures steady revenue streams regardless of fluctuations in new residential construction activity. In mature markets such as the United States, Europe, and Japan, repaint applications account for 70–80% of total residential paint volume, reflecting the dominance of renovation and maintenance over new builds. The increasing focus on home aesthetics, property value enhancement, and protective coatings for durability further strengthens this segment. As the global housing base continues to expand, residential repaint coatings remain the primary driver of growth in the architectural coatings market.

By Distribution Channel: Home Improvement Centers Lead with DIY Convenience and High Retail Penetration

The home improvement centers (big box retail) segment held the largest 41.6% share of the residential architectural coatings market in 2025, driven by strong demand from DIY consumers and small-scale professional painters. Major retailers such as Home Depot, Lowe’s, B&Q, and Leroy Merlin offer a comprehensive range of interior and exterior paints, primers, and coating accessories, supported by in-store color matching kiosks and competitive pricing on premium paint brands. These stores are strategically positioned to capture high consumer traffic due to their extended operating hours, weekend availability, and convenient locations, making them the preferred purchase point for homeowners. Additionally, features such as contractor service desks, bulk purchase discounts, and product availability attract both DIY users and independent contractors. As demand grows for easy-to-apply, high-quality decorative coatings, home improvement centers continue to dominate distribution, reinforcing their critical role in the global residential architectural coatings market.

Cool Wall Coatings Unlocking Carbon Reduction Pathways Under NYC Local Law 97

The enforcement of Local Law 97 in New York City is creating a compelling opportunity for cool wall coatings as a cost-effective retrofit solution for reducing building emissions. As part of the city’s climate legislation, buildings exceeding prescribed carbon limits are subject to financial penalties, creating strong incentives for energy efficiency upgrades.

Cool wall coatings, characterized by high solar reflectance and infrared reflectivity, reduce heat absorption on building facades. By lowering solar heat gain by 10% to 15%, these coatings decrease cooling demand, directly reducing energy consumption and associated carbon emissions. This is particularly valuable for older residential buildings where HVAC system upgrades may be cost-prohibitive.

The financial implications are significant. Buildings that exceed emission thresholds face penalties of approximately $268 per metric ton of CO₂, making relatively low-cost interventions such as reflective coatings highly attractive. For a typical large residential building, implementing cool wall coatings can generate annual energy savings ranging from $0.05 to $0.12 per square foot of wall area, providing a rapid return on investment.

In addition to energy savings, these coatings contribute to urban heat island mitigation. High-performance formulations with a Solar Reflectance Index above 0.60 can reduce exterior wall temperatures by up to 20°F during peak summer conditions, improving occupant comfort and reducing strain on citywide energy infrastructure.

The combination of regulatory pressure, economic incentives, and environmental benefits is positioning cool wall coatings as a strategic solution for decarbonizing urban residential buildings under stringent climate policies.

Competitive Landscape of the Residential Architectural Coatings Market

Sherwin-Williams Dominates North American Market with Strong Distribution and Premium Innovations

The Sherwin-Williams Company remains the leader in the residential architectural coatings market, leveraging its extensive Paint Stores Group (PSG) network. The company reported record net sales of $23.57 billion and continues to maintain strong profitability despite raw material volatility. Its Emerald® Rain Refresh™ technology introduces self-cleaning exterior coatings, enhancing durability and reducing maintenance. Sherwin-Williams’ strategic reorganization into three business segments strengthens supply chain efficiency and reinforces its dominance in both professional contractor and DIY segments.

PPG Expands Market Presence with Digital Ecosystems and High-Performance Coatings

PPG Industries, Inc. is a key player in the residential architectural coatings market, leveraging its advanced R&D and digital capabilities. The company reported a 7% revenue increase in Q1 2026, supported by strong margins in its performance coatings segment. Its PPG LINQ™ platform integrates AI-driven spectrophotometers and automated mixing systems, improving first-pass yield for contractors. PPG has also introduced graphene-enhanced waterborne coatings, delivering 30% higher scratch resistance for interior applications.

AkzoNobel Leads Sustainability with Bio-Based and Heat-Reflective Coating Technologies

AkzoNobel N.V. is a major innovator in the residential architectural coatings market, focusing on sustainability and premium decorative solutions. The company is progressing toward a merger with Axalta and has achieved improved profitability through pricing and cost optimization. Its RUBBOL WF 3350 coating incorporates 20% bio-based content, while its “Rhythm of Blues” color collection integrates infrared-reflective pigments to reduce urban heat buildup. AkzoNobel’s strategic divestments and focus on high-growth markets strengthen its position in sustainable coatings.

Nippon Paint Drives APAC Growth with Antimicrobial and Integrated Construction Solutions

Nippon Paint Holdings Co., Ltd. is the dominant player in the Asia-Pacific residential coatings market, benefiting from rapid urbanization. The company reported strong revenue growth and significant operating profit increases in 2026. Its nanotechnology-based antimicrobial coatings are widely used in luxury residential developments, offering virus-neutralizing properties. Nippon Paint is also expanding into integrated solutions such as waterproof membranes and solar-reflective coatings, positioning itself as a leader in energy-efficient housing solutions.

RPM International Strengthens Market Position with Specialty and DIY-Oriented Coating Solutions

RPM International Inc., through brands like Rust-Oleum® and DAP®, is a major player in the residential architectural coatings market, focusing on specialty and DIY segments. The company operates globally with strong North American revenue contributions. Its Rust-Oleum brand holds the leading position in aerosol paints and is expanding into advanced multi-surface primers for residential use. RPM’s strategic reorganization is expected to deliver significant cost synergies, reinforcing its position in niche high-margin markets.

Axalta Expands into Residential Segment with Energy-Efficient and High-Durability Coatings

Axalta Coating Systems is emerging as a strong competitor in the residential architectural coatings market, transitioning from automotive to architectural applications. Its Lumeera™ 3250 system enables low-temperature curing at 80°C, reducing energy consumption in manufacturing residential metal fixtures. Axalta is also a leader in fluoropolymer coatings for high-rise residential facades, offering up to 30 years of UV stability. Its potential merger with AkzoNobel is expected to create a comprehensive “Total Surface Solution” provider for modern residential construction.

China Leading Green Building Transformation with Low-VOC and Smart Residential Coatings

China remains the dominant force in the global residential architectural coatings market, driven by stringent environmental regulations and large-scale urban renewal programs. The implementation of GB 30981.1-2025 standards has significantly tightened VOC limits, capping emissions at 120 g/L for interior and 140 g/L for exterior coatings, with Tier-1 cities enforcing even stricter thresholds. This regulatory push is accelerating the transition toward low-VOC, eco-friendly architectural coatings across residential projects.

Innovation is a key differentiator, with the introduction of aerogel-based thermal insulation coating systems that reduce surface temperatures by up to 10°C, enhancing energy efficiency in residential buildings. The rising adoption of “Liquid Stone” coatings is transforming façade design by offering a lightweight and cost-effective alternative to natural stone. Additionally, China’s “Old Community Renovation” initiatives are driving demand for high-durability repaint systems, while photocatalytic self-cleaning coatings are gaining traction in pollution-prone urban areas. Strategic collaborations, such as the partnership between Nippon Paint and Evonik, are further advancing the development of next-generation eco-friendly binders tailored to regional climatic conditions.

India’s Housing Boom Accelerating Demand for Decorative and Energy-Efficient Coatings

India is emerging as the fastest-growing market in the residential architectural coatings industry, fueled by massive government-backed housing programs and urbanization. The Pradhan Mantri Awas Yojana (PMAY) is creating a substantial pipeline for exterior emulsions, primers, and decorative coatings, supporting the construction of millions of homes.

Technological advancements such as POS tinting systems are revolutionizing the retail landscape by enabling customization of thousands of color shades, especially in Tier-2 and Tier-3 cities. Infrastructure initiatives like the Smart Cities Mission are increasing the use of anti-carbonation coatings for buildings near transit corridors. The growing adoption of solar-reflective cool roof coatings is helping mitigate urban heat island effects, particularly in high-temperature regions. Product innovations, including low-odor antimicrobial interior paints with silver-ion technology, are catering to the premium wellness housing segment, while investments in eco-friendly binder production are strengthening domestic manufacturing capabilities.

United States Driving PFAS-Free Innovation and Residential Retrofit Demand

The United States architectural coatings market is undergoing a structural transformation driven by regulatory pressures and strong demand from the residential repair and remodeling sector. The EPA’s PFAS-free mandates (2026) are prompting a shift from traditional fluoropolymer coatings to silicone-modified acrylic formulations, redefining product development strategies.

Technological advancements include the increasing use of UV-curable coatings for factory-finished residential components, enabling zero-VOC emissions and rapid curing processes. Sustainability is also a major focus, with rising adoption of bio-based resins to meet LEED v5 and ESG standards. Innovative products such as thermochromic smart coatings are enhancing energy efficiency by adapting to seasonal temperature changes. Additionally, demand for DIY-friendly high-build interior paints is growing due to rising labor costs, while digital tools like AI-powered color matching integrated with BIM systems are improving project efficiency for contractors and homeowners.

Germany Advancing Energy-Efficient Facade Coatings and Circular Economy Solutions

Germany is a global leader in sustainable residential coatings, driven by stringent energy efficiency regulations and advanced material innovation. Compliance with the EU Energy Performance of Buildings Directive (EPBD) has made reflective thermal facade coatings a standard requirement for residential retrofits. Government support through the BEG funding program is further accelerating adoption by subsidizing high-performance insulation systems.

Technological innovation is evident in the development of biocide-free facade coatings that utilize physical surface structures to prevent mold and algae growth, reducing reliance on chemical additives. Germany is also advancing the use of silicate-based interior paints, known for their breathability, zero-VOC content, and mold resistance. Investments in prefabricated construction are driving demand for pre-coated residential components, while sustainability initiatives such as recycled packaging and circular resin technologies are reinforcing Germany’s leadership in eco-friendly coatings.

Saudi Arabia’s Vision 2030 Driving High-Performance Residential Coating Demand

Saudi Arabia is rapidly emerging as a high-value market in the residential architectural coatings sector, driven by mega infrastructure projects under Vision 2030. Regulatory measures such as Royal Decree M/165 (2025) are eliminating solvent-based coatings by enforcing strict VOC limits, accelerating the shift toward sustainable alternatives.

Large-scale residential developments like NEOM and The Line are generating demand for UV-resistant, high-durability coatings, particularly for extreme desert climates. Advanced applications such as nano-ceramic heat-reflective coatings are helping reduce cooling loads in residential buildings. Product innovations like air-purifying interior paints are gaining popularity in new housing projects, while technological advancements, including robotic spray systems, are improving application efficiency for complex architectural designs. Local manufacturing expansion through acquisitions is also strengthening the domestic supply chain and supporting long-term market growth.

Brazil’s Residential Coatings Market Strengthened by Climate Adaptation and Domestic Manufacturing

Brazil’s residential coatings market is characterized by diverse climatic demands and increasing focus on domestic production. Government policies such as anti-dumping duties on specialty resins are encouraging the use of locally sourced materials, including titanium dioxide, to support domestic manufacturers.

Technological advancements include the development of elastic acrylic coatings capable of withstanding extreme thermal expansion, making them ideal for Brazil’s varied climate conditions. Infrastructure programs like Minha Casa, Minha Vida are driving demand for cost-effective, water-based emulsions in social housing. Urban applications such as anti-graffiti coatings are widely used in metropolitan areas, while coastal regions are witnessing increased demand for salt-resistant, high-gloss coatings with superior corrosion protection. Investments in resin production capacity are further supporting long-term growth in the residential construction sector.

Vietnam Emerging as a High-Growth Residential Coatings Market in Southeast Asia

Vietnam is rapidly evolving into a key growth market for residential architectural coatings, driven by rising foreign investment and expanding urban infrastructure. Major cities like Ho Chi Minh City and Hanoi are witnessing a surge in residential construction, with a strong emphasis on EDGE and LEED-certified materials.

Regulatory changes requiring strict TVOC limits are accelerating the adoption of waterborne and polyurethane dispersion coatings, ensuring compliance with environmental standards. Technological advancements such as infrared curing systems are improving manufacturing efficiency for pre-finished interior panels. Growing demand for premium housing developments is driving the use of stain-resistant, easy-clean coatings, while suburban areas are seeing increased adoption of weather-resistant acrylic coatings for moisture and fungal protection. Innovative solutions like dual-function waterproofing and thermal insulation coatings are addressing unique architectural needs, particularly in Vietnam’s traditional housing designs.

Residential Architectural Coatings Market Report Scope

Residential Architectural Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$59.7 Billion

|

|

Market Size (2032)

|

$80.2 Billion

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Resin Type (Acrylic, Alkyd, Vinyl Acetate-Ethylene, Polyurethane, Epoxy, Polyester, Sustainable), By Technology (Water-borne Coatings, Solvent-borne Coatings, Powder Coatings, UV-Cured Coatings), By Application Area (Interior Coatings, Exterior Coatings, Floor Coatings), By Function and Performance (Decorative, Protective, Functional), By Project Type (New Residential Construction, Repaint and Maintenance), By Distribution Channel (Specialty Paint Stores, Home Improvement Centers, Direct-to-Consumer, Wholesale)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., Asian Paints Limited, Masco Corporation, Benjamin Moore and Co., Kansai Paint Co., Ltd., Jotun Group, RPM International Inc., Berger Paints India Limited, DAW SE, Hempel A/S, Axalta Coating Systems Ltd., Birla Opus

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Residential Architectural Coatings Market Segmentation

By Resin Type

- Acrylic

- Alkyd

- Vinyl Acetate-Ethylene

- Polyurethane

- Epoxy

- Polyester

- Sustainable

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Powder Coatings

- UV-Cured Coatings

By Application Area

- Interior Coatings

- Exterior Coatings

- Floor Coatings

By Function and Performance

- Decorative

- Protective

- Functional

By Project Type

- New Residential Construction

- Repaint and Maintenance

By Distribution Channel

- Specialty Paint Stores

- Home Improvement Centers

- Direct-to-Consumer

- Wholesale

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Residential Architectural Coatings Industry

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- Masco Corporation

- Benjamin Moore & Co.

- Kansai Paint Co., Ltd.

- Jotun Group

- RPM International Inc.

- Berger Paints India Limited

- DAW SE

- Hempel A/S

- Axalta Coating Systems Ltd.

- Birla Opus

*- List not Exhaustive