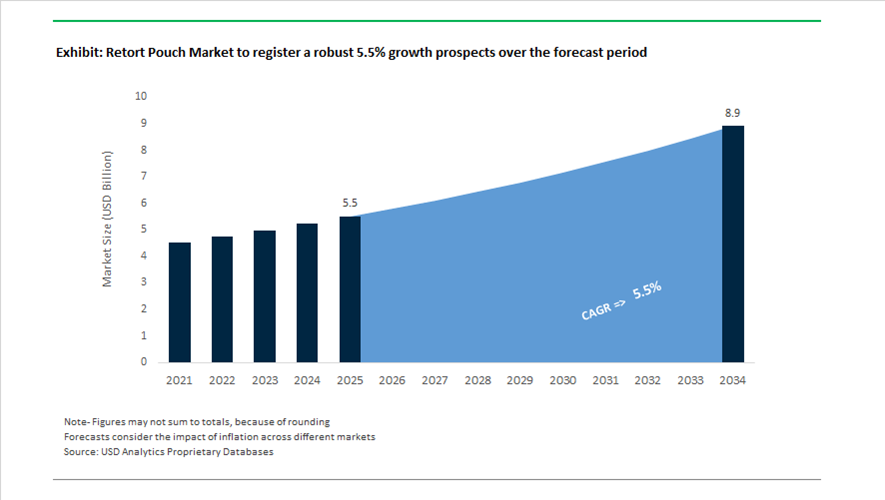

Retort Pouch Market Valued at $5.5 Billion in 2025, Projected to Reach $8.9 Billion by 2034 at 5.5% CAGR

The global retort pouch market is valued at $5.5 billion in 2025 and is projected to reach $8.9 billion by 2034, registering a CAGR of 5.5%. Demand is driven by growth in ready-to-eat (RTE) meals, shelf-stable pet food packaging, high-barrier multilayer laminates, aluminum foil retort pouches, mono-material polypropylene pouches, and recycle-ready flexible packaging solutions. Retort packaging remains essential for thermally processed foods requiring high heat resistance, oxygen and moisture barrier protection, and extended shelf life without refrigeration. Brand owners are prioritizing lightweight flexible formats over rigid cans to reduce logistics costs, improve consumer convenience, and meet sustainability targets.

Industry consolidation accelerated in 2024 and 2025, reshaping competitive positioning. In late 2024, Amcor announced its approximately $8.4 billion acquisition of Berry Global, progressing through 2025 to form a dominant flexible packaging entity with consolidated R&D in high-barrier retort technologies for pet food and convenience meals. In June 2024, Sonoco completed its $3.9 billion acquisition of Eviosys, enabling a multi-material packaging strategy that integrates metal and flexible retort solutions for shelf-stable food producers. In September 2024, Sonoco initiated a strategic review of its Thermoformed & Flexible Packaging business, signaling potential restructuring of retort-focused assets to streamline portfolio efficiency. In November 2025, Mondi acquired Schumacher Packaging to strengthen its European supply chain, integrating secondary paperboard packaging capabilities with its primary retort pouch production. In November 2025, Sealed Air Corporation agreed to a $10.3 billion acquisition by Clayton, Dubilier & Rice, with closing expected in mid-2026, marking a shift toward private ownership for Cryovac® retort solutions.

Sustainability innovation is reshaping material design. In October 2024, ProAmpac launched RT-4000, a polypropylene-based mono-material retort pouch engineered to deliver high-barrier performance without aluminum foil, enabling compatibility with existing recycling streams. In November 2024, Huhtamaki introduced a smooth molded fiber lid production line, advancing fiber-based components that can integrate into hybrid retort tray-and-pouch formats. In late 2025, Constantia Flexibles received the Green Packaging Star Award for ComforLid, a die-cut retort lidding solution using Low Carbon Aluminum that reduces carbon emissions by 43% compared to conventional grades. Amcor’s October 2024 sustainability update confirmed progress toward incorporating 10% post-consumer recycled plastic across its portfolio by fiscal 2025, including pilot integration of PCR layers within retort pouch structural plies.

The retort pouch market is increasingly characterized by mono-material recyclable laminates, aluminum-to-polypropylene substitution, fiber-based hybrid packaging, low-carbon aluminum lidding systems, PCR content integration, multi-material packaging consolidation, and private equity-driven restructuring within flexible packaging leaders. As shelf-stable food demand rises globally and sustainability mandates intensify, high-barrier retort innovation remains central to balancing product safety, recyclability, and supply chain efficiency.

Key Trends and High-Value Opportunities in the Retort Pouch Market

Pet Food Premiumization Driving Automated Retort Pouch Production Scale-Up

The retort pouch market is experiencing structurally accelerated growth due to the premiumization of pet food, a direct outcome of the global “humanization of pets” trend. Pet owners are increasingly demanding gourmet, single-serve, and nutritionally differentiated wet food formats that mirror human convenience meals. This has triggered a decisive shift away from traditional 400 g metal cans toward lightweight retort pouches that support portion control, brand storytelling, and premium shelf positioning. For manufacturers, the economics are equally compelling, as pouches enable higher margin realization through differentiated SKUs and reduced material intensity.

Between 2024 and 2025, global leaders such as Mars Petcare and Nestlé Purina significantly accelerated the conversion of legacy wet food canning lines to flexible retort pouch formats. Nestlé Purina’s recyclable-first strategy, including the launch of the industry’s first mono-material retort pouch under the Felix brand, highlights how sustainability and premiumization are converging. The shift delivers an estimated 60% reduction in packaging weight versus steel cans, directly lowering transportation costs and improving pallet efficiency across global distribution networks.

To support this volume and complexity, manufacturers are investing heavily in automated horizontal form-fill-seal systems. Advanced retort pouch filling lines, typically priced between 180,000 and 280,000 US dollars per line, are now designed to address historical failure points such as corner thinning and seal deformation during high-pressure sterilization. According to 2025 assessments referenced in U.S. Army DEVCOM technical evaluations, these next-generation machines significantly improve yield consistency and reduce post-retort rejection rates, making large-scale premium pouch production economically viable.

Commercial Breakthrough of Recyclable Mono-Material Retort Pouch Structures

A second transformative trend is the rapid commercialization of recyclable mono-material retort pouch structures, driven primarily by regulatory mandates and brand sustainability commitments. Historically, retort pouches relied on complex multi-layer laminates incorporating aluminum foil, which offered excellent barrier performance but rendered the packaging non-recyclable. This structural limitation is now being addressed through all-polypropylene and all-polyethylene barrier solutions that align with circular economy objectives.

The entry into force of the EU Packaging and Packaging Waste Regulation on February 11, 2025 has been a decisive catalyst. The regulation requires all packaging placed on the EU market to be designed for cost-effective recycling by 2030, effectively forcing brand owners and converters to move away from foil-based retort formats. In response, 2025 witnessed a wave of material science innovation aimed at maintaining oxygen and moisture barrier integrity under sterilization conditions of 121 degrees Celsius.

At the K 2025 trade fair, a landmark collaboration between Bobst, Brückner, and Mitsui Chemicals showcased the world’s first recyclable mono-material retort solution using opaque metallization instead of aluminum foil. This technology employs an ultra-thin, stretchable barrier primer that preserves shelf-life performance while enabling mechanical recycling. In parallel, Huhtamaki expanded its blueloop portfolio with mono-material polypropylene retort pouches containing approximately 95% mono-polymer content, positioning these formats as recycle-ready within existing European collection and sorting infrastructure. For global food and pet food brands, such solutions are rapidly becoming a prerequisite rather than a differentiation lever.

Lightweight Retort Pouches for Military Rations and Humanitarian Logistics

A high-volume, regulation-driven opportunity is emerging in military and humanitarian food logistics, where retort pouches are being adopted to optimize payload efficiency and supply chain resilience. Defense agencies and relief organizations are actively replacing foil-heavy packaging with lightweight polymer-based retort pouches to reduce shipment weight while maintaining strict shelf-life requirements of up to three years at ambient temperatures.

By late 2025, the U.S. Department of Defense publicly reported successful field trials of advanced polymer-blend retort pouches that significantly reduce pack weight compared to traditional foil-lined formats. While ongoing material development continues to optimize water vapor resistance, the immediate transition toward flat retort pouch geometries has already delivered measurable gains in pallet density. This allows more Meals Ready-to-Eat units per airlift, a critical advantage during rapid deployment and global humanitarian missions.

Durability requirements in this segment remain exceptionally high. Modern military retort pouches are subjected to rigorous tensile, burst, and drop testing to withstand four-high pallet stacking and air-drop scenarios. Recent 2025 Army reports indicate that packaging system redesigns now extend beyond the pouch itself, with rigid components being replaced by flexible polymer packets to prevent seal damage during automated filling and packing. Suppliers that can demonstrate consistent seal integrity under extreme mechanical stress are well positioned to secure long-term government supply contracts.

Culinary Differentiation in Premium Home Meal Replacement Formats

The rapid expansion of premium Home Meal Replacements and ready-to-heat offerings represents one of the most attractive growth avenues for retort pouch suppliers. As consumers seek restaurant-quality meals with extended shelf life, food manufacturers are increasingly favoring retort pouches over cans due to superior heat transfer, texture retention, and visual appeal.

By the end of 2025, the U.S. HMR market alone is projected to surpass 20 billion dollars in value, with stand-up retort pouches becoming the preferred format for chef-inspired sauces, proteins, and complete meals. Unlike metal cans, retort pouches enable gradient heating during sterilization, significantly reducing thermal damage to delicate ingredients and preserving flavor complexity and nutritional profiles. This capability is particularly valuable for premium ethnic cuisines, plant-based meals, and sous-vide style proteins that are sensitive to overprocessing.

E-commerce and direct-to-consumer meal subscription models are further amplifying this opportunity. Shelf-stable components are increasingly being packaged in paperboard-laminated retort pouches that balance sustainability aesthetics with functional performance. Although these formats typically offer slightly shorter shelf life compared to all-plastic pouches, their tactile feel and natural appearance resonate strongly with health-conscious consumers. For brands operating at the intersection of convenience, sustainability, and culinary authenticity, retort pouches have become a strategic enabler rather than a secondary packaging choice.

Retort Pouch Market Share Share and Segmentation Insights

Stand-Up Pouches Dominate Retort Packaging Demand Driven by Shelf Presence and Premium Food Packaging

Stand-up pouches accounted for 52.80% of the retort pouch market in 2025, establishing them as the most widely adopted format for shelf-stable food packaging. Their leadership is driven by strong retail shelf visibility, structural stability, and efficient filling compatibility, making them highly suitable for ready-to-eat meals, pet food, and liquid food packaging. The upright design enhances consumer convenience while enabling brands to maximize retail display impact in competitive food categories. A major 2025 innovation trend is the premiumization of stand-up retort pouches, where packaging incorporates matte finishes, transparent window patches, shaped pouch profiles, and enhanced graphics. These features improve product differentiation while maintaining the high-temperature retort processing performance and barrier properties required for long shelf-life food products.

Ready-to-Eat Meals Lead Retort Pouch Consumption as Shelf-Stable Convenience Foods Expand

Ready-to-eat meals represent the largest application segment in the retort pouch market, capturing 38.60% of total demand in 2025 due to rising consumer preference for convenient, shelf-stable meal solutions. Retort pouch packaging allows fully cooked foods to be stored at ambient temperatures without refrigeration, offering the convenience of canned foods while delivering improved taste, texture, and portion control. Growth is particularly strong across urban households, travel food products, and emergency food supplies. A key 2025 market trend is the expansion of premium ready-to-eat meal offerings, including ethnic cuisine varieties, plant-based meal solutions, and chef-inspired packaged dishes. These premium products require retort pouches with advanced barrier structures and strong aesthetic appeal that preserve product quality through high-temperature sterilization.

Retort Pouch Market Competitive Landscape

The 2026 retort pouch market is transitioning toward mono-material polypropylene laminates, aluminum-free high-barrier films, and recycle-ready packaging solutions. Growth is driven by PPWR regulations, EPR mandates, and demand for lightweight, shelf-stable packaging across ready meals, pet food, and infant nutrition.

Amcor advances recycle-ready retort pouch innovation with AmLite HeatFlex and North America capacity expansion

Amcor PLC is strengthening its leadership in retort pouch packaging through large-scale capacity expansion and advanced recyclable film technologies. Investment in North American protein packaging includes new lamination and converting lines to support meat and seafood applications. AmLite HeatFlex™ technology replaces aluminum layers with high-barrier, recycle-ready films capable of withstanding high-temperature retort processes. Integration with Berry Global enhances its polyethylene-based flexible packaging portfolio and secondary packaging capabilities. R&D initiatives such as the Lift-Off Challenge support development of compostable OTR barriers and adhesives. Focus on lightweight, high-barrier structures supports sustainable packaging for shelf-stable food products.

Mondi scales mono-material retort pouches with validated recyclability and circular packaging strategy

Mondi Group is expanding its retort pouch portfolio through mono-material polypropylene solutions aligned with circular economy goals. The RetortPouch Recyclable line replaces multi-layer laminates with high-barrier films suitable for wet pet food and processed meat applications. Validation by the National Test Centre Circular Plastics confirms accurate sorting and compatibility with existing recycling streams. Integrated operations across raw materials and film production ensure supply stability and cost efficiency. MAP2030 strategy drives commitment to fully recyclable or reusable packaging solutions. Focus on aluminum-free barrier films supports compliance with EU sustainability regulations.

Huhtamaki accelerates mono-PP retort packaging adoption with blueloop innovation and global manufacturing footprint

Huhtamaki Oyj is advancing sustainable retort pouch solutions through its blueloop™ platform focused on mono-material PP laminates. The blueloop™ PP retort pouch offers 90% mono-material composition with high oxygen and vapor barrier performance comparable to traditional laminates. Manufacturing presence in India and other high-growth markets supports demand for dairy, baby food, and pharmaceutical packaging. Sustainability targets include increasing renewable and recycled material usage beyond 80% and transitioning to renewable energy production. Product differentiation includes transparent and SuperWhite aesthetics alongside functional features such as easy-open designs. Focus on high-barrier recyclable packaging supports growth in regulated food and healthcare segments.

Sonoco optimizes retort pouch production with AI-driven manufacturing and portfolio transformation strategy

Sonoco Products Company is enhancing its retort pouch capabilities through operational restructuring and advanced manufacturing technologies. The company reported $7.5 billion in 2025 sales and targets up to $1.35 billion EBITDA in 2026. Portfolio simplification into core packaging segments improves focus on high-value flexible and metal packaging solutions. AI integration in lamination processes enhances precision and reduces material waste in retort pouch production. Divestiture of non-core businesses strengthens capital allocation toward consumer packaging growth. Strategic focus on private label and premium packaged foods supports demand for advanced retort pouch formats.

Sealed Air integrates automation and high-performance films with CRYOVAC retort packaging systems

Sealed Air Corporation is strengthening its retort pouch market position through automation and advanced flexible packaging technologies. The CRYOVAC® VPP 3002 FlexPrep system enables high-speed vertical form-fill-seal processing for liquid and pumpable food products. Integration of Liquibox® and CRYOVAC® technologies enhances efficiency and scalability in food packaging operations. The company leverages a global footprint across 117 countries to deploy sustainable materials and reduce operational costs. Installed base of over 4,000 vacuum chamber systems supports adoption of next-generation retort pouch films. Focus on automation and digital visualization tools enhances value for food processors and retail partners.

United States: Foil-Free Barrier Migration and Automation-Led Capacity Scaling

The United States retort pouch industry is undergoing a decisive material and process reset driven by tariff volatility and automation economics. Following the 2025 reinstatement of 25% federal duties on aluminum and steel derivatives, U.S. converters accelerated the transition toward foil-free, clear high-barrier structures using SiOx and AlOx coatings to stabilize input costs and improve supply chain resilience. This shift has materially expanded the adoption of nylon and polypropylene-based multilayer films that can withstand retort temperatures while maintaining clarity and puncture resistance. In parallel, Amcor announced a late-2025 ramp-up of its North American flexible packaging footprint to localize production of Liquiflex® Advance™ films, targeting zero-headspace foodservice applications that demand precise fill control and thermal stability.

Operational efficiency is increasingly defined by automation and compliance readiness. At IPPE 2025, AI-vision integrated vacuum pouching systems capable of real-time product scanning and customized bag dispensing were introduced, delivering up to 30% packaging cost savings for protein processors. Regulatory progress has also unlocked circularity pathways. New U.S. FDA No Objection Letters issued for chemically recycled PCR-PP in direct food-contact retort applications, effective 2026, have catalyzed brand trials with recycled-content stand-up pouches. With grocery e-commerce scaling, ISTA 6-Amazon.com durability benchmarks drove a 15% increase in demand for high-puncture nylon/PP blends in 2025. Publicly listed U.S. packaging firms collectively invested an estimated $450 million in 2025 to install specialized autoclaves and high-speed rotary fillers optimized for stand-up retort formats.

Germany: Mono-Material Leadership and Bio-Based Barrier Industrialization

Germany is setting the pace in circular design and policy-aligned material innovation for retort pouches. In late 2024 and early 2025, Mondi completed independent sortability trials at the National Test Centre Circular Plastics, validating that its mono-material PP retort pouches can be accurately identified and processed within advanced recycling streams. This proof point has accelerated downstream adoption as converters prepare for 2026 reporting obligations under the German Packaging Act. Mondi further strengthened its Western European retort capabilities by finalizing the €634 million acquisition of Schumacher Packaging assets in 2025, expanding pre-made stand-up pouch capacity and shortening lead times for food brands.

Material science advances are reducing reliance on conventional barrier chemistries. In 2025, German researchers industrialized nature-based barrier additives that enable oxygen transmission rates below 0.1 cc per square meter per day without EVOH layers, improving recyclability while preserving shelf life. These innovations have supported a reported 90% compliance rate among German converters for mono-material retort formats ahead of regulatory deadlines, positioning Germany as a reference market for circular-ready, high-performance retort packaging.

India: Food Park Expansion and Active Barrier Customization

India’s retort pouch market is scaling on the back of retail deregulation, export momentum, and targeted incentives. The May 2025 removal of licensing requirements for specified foodstuffs unlocked investment across regional Mega Food Parks, lifting demand for shelf-stable retort pouches by an estimated 18% year over year. Indian converters responded with application-specific innovation. UFlex introduced multilayer films in 2025 incorporating active oxygen scavengers tailored to high-oil ready-to-eat meals, addressing oxidation risks common in regional cuisines.

Government incentives have reinforced capacity build-out. Under the Production Linked Incentive scheme for food processing, more than ₹800 crore was disbursed in 2025 to firms expanding retort processing and aseptic filling lines. India also consolidated its role as an export hub for private-label retort pouches, with 2025 trade data indicating a 12% volume increase for spouted and gusseted formats destined for the Middle East and the United Kingdom. This export orientation is pushing converters to standardize barrier performance and sterilization robustness to meet diverse regulatory regimes.

China: Scale Advantage and Smart Factory Yield Optimization

China retains its position as the world’s largest retort pouch producer, with policy and digitalization reinforcing scale economics. The 2025 Petrochemical Growth Plan incentivized domestic production of high-clarity RCPP films to replace imported specialty resins, lowering costs for converters while improving supply security. Converter clusters in Guangdong integrated digital twin technologies into pouch-making lines by early 2026, reducing material waste by approximately 12% during high-temperature qualification runs and accelerating time to stable production.

Retail dynamics are also reshaping formats. In 2025, more than 60% of new ready-meal launches in Tier 1 cities adopted retort pouches with integrated QR codes to support farm-to-fork traceability and consumer transparency. This convergence of scale, smart manufacturing, and data-enabled retail is reinforcing China’s competitiveness across both domestic and export-oriented retort applications.

Japan: Premium Functionality and Senior-Centric Ergonomics

Japan’s retort pouch innovation is characterized by premium functionality and demographic responsiveness. Manufacturers such as Otsuka Holdings advanced microwavable-retort technologies featuring patented steam-release venting, enabling safe in-pouch heating without secondary containers. These designs support portion control and convenience while maintaining retort integrity.

Policy support has aligned packaging ergonomics with societal needs. In 2025, the Ministry of Economy, Trade and Industry backed the development of easy-tear, high-grip retort pouches tailored to the Silver Economy. Senior-friendly features such as tactile grips and low-force opening are now influencing design standards, reinforcing Japan’s leadership in user-centric retort packaging.

Retort Pouch Industry: Country-Level Strategic Snapshot

Retort Pouch Market County Level Snapshot

|

Country / Region

|

Primary Strategic Driver

|

Operational Impact on Retort Pouches

|

|

United States

|

Tariff pressure and automation

|

Foil-free barriers, AI-enabled filling, recycled-content approvals

|

|

Germany

|

Circular compliance leadership

|

Mono-material PP, bio-based barriers, recyclability validation

|

|

India

|

Food park expansion and exports

|

Active barrier films, capacity incentives, private-label growth

|

|

China

|

Scale and smart manufacturing

|

RCPP localization, digital twins, traceability integration

|

|

Japan

|

Premium convenience and aging demographics

|

Microwavable retort, senior-friendly ergonomics

|

Retort Pouch Market Report Scope

Retort Pouch Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.5 Billion

|

|

Market Size (2034)

|

$8.9 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Pouch Type (Stand-Up Pouches, Flat Pouches, Spouted Pouches, Side Gusseted Pouches, Resealable Pouches), By Material Structure (Aluminum Foil Laminates, Mono-Material Structures, Non-Foil Barrier Structures, Nylon & Polyamide Blends), By Application (Ready-to-Eat Meals, Pet Food, Baby Food, Meat Poultry & Seafood, Soups & Sauces, Beverages & Liquid Foods)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Sealed Air Corporation, Huhtamaki Oyj, Sonoco Products Company, Berry Global Group Inc., Constantia Flexibles, Coveris Management GmbH, Winpak Ltd., ProAmpac LLC, UFlex Limited, Otsuka Holdings Co. Ltd., Flair Flexible Packaging Corporation, Korozo Group, Clifton Packaging Group Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Retort Pouch Market Segmentation

By Pouch Type

- Stand-Up Pouches

- Flat Pouches

- Spouted Pouches

- Side Gusseted Pouches

- Resealable Pouches

By Material Structure

- Aluminum Foil Laminates

- Mono-Material Structures

- Non-Foil Barrier Structures

- Nylon & Polyamide Blends

By Application

- Ready-to-Eat Meals

- Pet Food

- Baby Food

- Meat Poultry & Seafood

- Soups & Sauces

- Beverages & Liquid Foods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Retort Pouch Industry

- Amcor plc

- Mondi Group

- Sealed Air Corporation

- Huhtamaki Oyj

- Sonoco Products Company

- Berry Global Group Inc.

- Constantia Flexibles

- Coveris Management GmbH

- Winpak Ltd.

- ProAmpac LLC

- UFlex Limited

- Otsuka Holdings Co. Ltd.

- Flair Flexible Packaging Corporation

- Korozo Group

- Clifton Packaging Group Ltd.

*- List not Exhaustive