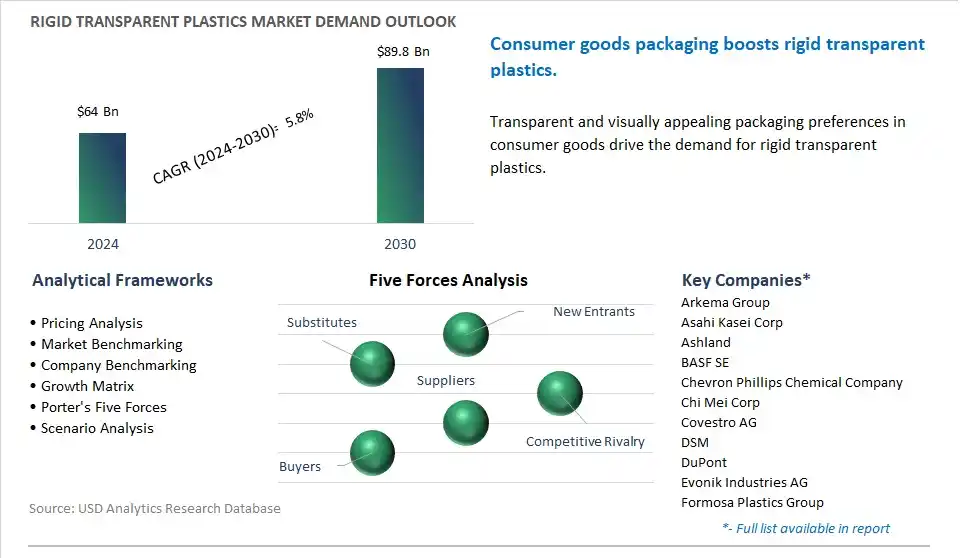

The global Rigid Transparent Plastics Market is poised to register a 5.8% CAGR from $64 Billion in 2024 to $89.8 Billion in 2030.

The global Rigid Transparent Plastics Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Polymer (Polycarbonate (PC), Polyvinyl Chloride (PVC), Polystyrene (PS), Acrylonitrile Butadiene Styrene (ABS) & Styrene Acrylonitrile (SAN), Polypropylene (PP), Polymethyl Methacrylate (PMMA), Styrene Block Copolymers (SBC), Others), By End-User (Packaging, Healthcare, Electrical and Electronics, Automotive, Buildings and Construction, Others).

An Introduction to Global Rigid Transparent Plastics Market in 2024

The future of the rigid transparent plastics market is influenced by key trends such as consumer electronics, automotive, medical devices, and packaging applications. Rigid transparent plastics, including materials such as polycarbonate, acrylic, and PETG, offer optical clarity, impact resistance, and design flexibility for a wide range of products and industries. In the consumer electronics sector, rigid transparent plastics are used for smartphone screens, display panels, and protective covers, providing scratch resistance and durability while maintaining visual clarity. In the automotive industry, these materials are employed for headlamp lenses, instrument panels, and interior trim components, enhancing aesthetics and safety features. Moreover, in medical devices and equipment, rigid transparent plastics are utilized for surgical instruments, diagnostic tools, and medical packaging, ensuring sterilizability, biocompatibility, and visibility. Additionally, in the packaging sector, rigid transparent plastics are preferred for food containers, beverage bottles, and cosmetic packaging, allowing product visibility and brand differentiation on store shelves. As industries continue to innovate and demand high-performance materials for their applications, the rigid transparent plastics market will witness advancements in material properties, processing technologies, and sustainability initiatives to meet evolving industry needs and consumer preferences.

Rigid Transparent Plastics Market Competitive Landscape

The market report analyses the leading companies in the industry including Arkema Group, Asahi Kasei Corp, Ashland, BASF SE, Chevron Phillips Chemical Company, Chi Mei Corp, Covestro AG, DSM, DuPont, Evonik Industries AG, Formosa Plastics Group, Huntsman Corp, Idemitsu Kosan, Ineos Chlorvinyls Ltd, Lanxess AG, LG Chem, Lotte Chemical Corp, Mitsubishi Engineering Plastics Corp, SABIC, Samyang, Shin-Etsu Chemical Co. Ltd, Solvay SA, Teijin Ltd, Trinseo, Westlake Chemical Corp.

Rigid Transparent Plastics Market Dynamics

Rigid Transparent Plastics Market Trend: Increasing Demand for Transparent Packaging Solutions

A significant trend in the market for rigid transparent plastics is the increasing demand for transparent packaging solutions across various industries. Transparency in packaging offers several benefits, including product visibility, aesthetic appeal, and consumer trust. As consumers seek more information about the products they purchase, transparent packaging allows them to inspect the contents, verify quality, and make informed decisions. The trend is driving the adoption of rigid transparent plastics in sectors such as food and beverage, cosmetics, electronics, and healthcare, where product visibility and presentation play crucial roles in consumer perception and purchasing behavior.

Rigid Transparent Plastics Market Driver: Advancements in Packaging Technology and Design

A primary driver for the market of rigid transparent plastics is the continuous advancements in packaging technology and design. With ongoing innovations in material science, manufacturing processes, and packaging design techniques, manufacturers can now produce rigid transparent plastics with improved clarity, strength, and versatility. These advancements enable the creation of packaging solutions that offer enhanced product protection, extended shelf life, and innovative features such as tamper-evident seals, resealable closures, and ergonomic designs. The constant evolution of packaging technology drives the demand for rigid transparent plastics as brands and retailers seek packaging solutions that meet the ever-changing needs and expectations of consumers.

Rigid Transparent Plastics Market Opportunity: Expansion into Sustainable Alternatives

An opportunity in the market for rigid transparent plastics lies in the expansion into sustainable alternatives. While transparency remains a desirable feature in packaging, there is a growing concern over the environmental impact of traditional plastics. Manufacturers have the opportunity to capitalize on The trend by developing and offering rigid transparent plastics made from sustainable and recyclable materials such as bio-based polymers, recycled content, and biodegradable plastics. By investing in research and development to innovate sustainable alternatives, manufacturers can address growing consumer demand for eco-friendly packaging solutions while maintaining the transparency and functionality that customers value. Embracing sustainability presents a strategic opportunity for companies to differentiate their products, attract environmentally conscious consumers, and contribute to a more sustainable future for the packaging industry.

Rigid Transparent Plastics Market Share Analysis: Polymethyl Methacrylate (PMMA) generated the highest revenue in 2024

The largest segment in the Rigid Transparent Plastics Market is Polymethyl Methacrylate (PMMA). PMMA, also known as acrylic or acrylic glass, is widely used in various applications requiring transparent or clear materials. Diverse factors contribute to PMMA's dominance in the rigid transparent plastics market. PMMA offers exceptional optical clarity, comparable to glass, making it an ideal choice for applications where transparency and aesthetics are essential, such as automotive components, signage, displays, and optical lenses. Additionally, PMMA has excellent weatherability and UV resistance, retaining its clarity and color stability even after prolonged exposure to sunlight, making it suitable for outdoor applications. Further, PMMA is lightweight, shatter-resistant, and easy to fabricate, allowing for versatile design possibilities and cost-effective manufacturing processes. Furthermore, PMMA's recyclability and sustainability credentials appeal to environmentally conscious consumers and industries seeking eco-friendly materials. The combination of these factors positions PMMA as the largest segment in the Rigid Transparent Plastics Market.

Rigid Transparent Plastics Market Share Analysis: Healthcare segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Rigid Transparent Plastics Market is the Healthcare sector. The increasing demand for transparent medical devices, packaging, and equipment in the healthcare industry drives the adoption of rigid transparent plastics. Transparent plastics such as polycarbonate and polymethyl methacrylate (PMMA) are commonly used in medical applications due to their clarity, biocompatibility, and sterilizability. These materials are utilized in the production of items such as medical packaging, IV components, surgical instruments, diagnostic equipment, and medical implants. Additionally, advancements in medical technology and procedures require innovative materials that offer high optical clarity, impact resistance, and chemical stability, qualities that rigid transparent plastics provide. Further, the growing aging population worldwide and the rising prevalence of chronic diseases drive the demand for healthcare services and medical products, further boosting the growth of the Healthcare segment in the Rigid Transparent Plastics Market.

Rigid Transparent Plastics Market Report Segmentation

By Polymer

Polycarbonate (PC)

Polyvinyl Chloride (PVC)

Polystyrene (PS)

Acrylonitrile Butadiene Styrene (ABS) & Styrene Acrylonitrile (SAN)

Polypropylene (PP)

Polymethyl Methacrylate (PMMA)

Styrene Block Copolymers (SBC)

Others

By End-User

Packaging

Healthcare

Electrical and Electronics

Automotive

Buildings and Construction

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Rigid Transparent Plastics Companies Profiled in the Market Study

Arkema Group

Asahi Kasei Corp

Ashland

BASF SE

Chevron Phillips Chemical Company

Chi Mei Corp

Covestro AG

DSM

DuPont

Evonik Industries AG

Formosa Plastics Group

Huntsman Corp

Idemitsu Kosan

Ineos Chlorvinyls Ltd

Lanxess AG

LG Chem

Lotte Chemical Corp

Mitsubishi Engineering Plastics Corp

SABIC

Samyang

Shin-Etsu Chemical Co. Ltd

Solvay SA

Teijin Ltd

Trinseo

Westlake Chemical Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Rigid Transparent Plastics Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Rigid Transparent Plastics Market Size Outlook, $ Million, 2021 to 2030

3.2 Rigid Transparent Plastics Market Outlook by Type, $ Million, 2021 to 2030

3.3 Rigid Transparent Plastics Market Outlook by Product, $ Million, 2021 to 2030

3.4 Rigid Transparent Plastics Market Outlook by Application, $ Million, 2021 to 2030

3.5 Rigid Transparent Plastics Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Rigid Transparent Plastics Industry

4.2 Key Market Trends in Rigid Transparent Plastics Industry

4.3 Potential Opportunities in Rigid Transparent Plastics Industry

4.4 Key Challenges in Rigid Transparent Plastics Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Rigid Transparent Plastics Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Rigid Transparent Plastics Market Outlook by Segments

7.1 Rigid Transparent Plastics Market Outlook by Segments, $ Million, 2021- 2030

By Polymer

Polycarbonate (PC)

Polyvinyl Chloride (PVC)

Polystyrene (PS)

Acrylonitrile Butadiene Styrene (ABS) & Styrene Acrylonitrile (SAN)

Polypropylene (PP)

Polymethyl Methacrylate (PMMA)

Styrene Block Copolymers (SBC)

Others

By End-User

Packaging

Healthcare

Electrical and Electronics

Automotive

Buildings and Construction

Others

8 North America Rigid Transparent Plastics Market Analysis and Outlook To 2030

8.1 Introduction to North America Rigid Transparent Plastics Markets in 2024

8.2 North America Rigid Transparent Plastics Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Rigid Transparent Plastics Market size Outlook by Segments, 2021-2030

By Polymer

Polycarbonate (PC)

Polyvinyl Chloride (PVC)

Polystyrene (PS)

Acrylonitrile Butadiene Styrene (ABS) & Styrene Acrylonitrile (SAN)

Polypropylene (PP)

Polymethyl Methacrylate (PMMA)

Styrene Block Copolymers (SBC)

Others

By End-User

Packaging

Healthcare

Electrical and Electronics

Automotive

Buildings and Construction

Others

9 Europe Rigid Transparent Plastics Market Analysis and Outlook To 2030

9.1 Introduction to Europe Rigid Transparent Plastics Markets in 2024

9.2 Europe Rigid Transparent Plastics Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Rigid Transparent Plastics Market Size Outlook by Segments, 2021-2030

By Polymer

Polycarbonate (PC)

Polyvinyl Chloride (PVC)

Polystyrene (PS)

Acrylonitrile Butadiene Styrene (ABS) & Styrene Acrylonitrile (SAN)

Polypropylene (PP)

Polymethyl Methacrylate (PMMA)

Styrene Block Copolymers (SBC)

Others

By End-User

Packaging

Healthcare

Electrical and Electronics

Automotive

Buildings and Construction

Others

10 Asia Pacific Rigid Transparent Plastics Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Rigid Transparent Plastics Markets in 2024

10.2 Asia Pacific Rigid Transparent Plastics Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Rigid Transparent Plastics Market size Outlook by Segments, 2021-2030

By Polymer

Polycarbonate (PC)

Polyvinyl Chloride (PVC)

Polystyrene (PS)

Acrylonitrile Butadiene Styrene (ABS) & Styrene Acrylonitrile (SAN)

Polypropylene (PP)

Polymethyl Methacrylate (PMMA)

Styrene Block Copolymers (SBC)

Others

By End-User

Packaging

Healthcare

Electrical and Electronics

Automotive

Buildings and Construction

Others

11 South America Rigid Transparent Plastics Market Analysis and Outlook To 2030

11.1 Introduction to South America Rigid Transparent Plastics Markets in 2024

11.2 South America Rigid Transparent Plastics Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Rigid Transparent Plastics Market size Outlook by Segments, 2021-2030

By Polymer

Polycarbonate (PC)

Polyvinyl Chloride (PVC)

Polystyrene (PS)

Acrylonitrile Butadiene Styrene (ABS) & Styrene Acrylonitrile (SAN)

Polypropylene (PP)

Polymethyl Methacrylate (PMMA)

Styrene Block Copolymers (SBC)

Others

By End-User

Packaging

Healthcare

Electrical and Electronics

Automotive

Buildings and Construction

Others

12 Middle East and Africa Rigid Transparent Plastics Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Rigid Transparent Plastics Markets in 2024

12.2 Middle East and Africa Rigid Transparent Plastics Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Rigid Transparent Plastics Market size Outlook by Segments, 2021-2030

By Polymer

Polycarbonate (PC)

Polyvinyl Chloride (PVC)

Polystyrene (PS)

Acrylonitrile Butadiene Styrene (ABS) & Styrene Acrylonitrile (SAN)

Polypropylene (PP)

Polymethyl Methacrylate (PMMA)

Styrene Block Copolymers (SBC)

Others

By End-User

Packaging

Healthcare

Electrical and Electronics

Automotive

Buildings and Construction

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Arkema Group

Asahi Kasei Corp

Ashland

BASF SE

Chevron Phillips Chemical Company

Chi Mei Corp

Covestro AG

DSM

DuPont

Evonik Industries AG

Formosa Plastics Group

Huntsman Corp

Idemitsu Kosan

Ineos Chlorvinyls Ltd

Lanxess AG

LG Chem

Lotte Chemical Corp

Mitsubishi Engineering Plastics Corp

SABIC

Samyang

Shin-Etsu Chemical Co. Ltd

Solvay SA

Teijin Ltd

Trinseo

Westlake Chemical Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Polymer

Polycarbonate (PC)

Polyvinyl Chloride (PVC)

Polystyrene (PS)

Acrylonitrile Butadiene Styrene (ABS) & Styrene Acrylonitrile (SAN)

Polypropylene (PP)

Polymethyl Methacrylate (PMMA)

Styrene Block Copolymers (SBC)

Others

By End-User

Packaging

Healthcare

Electrical and Electronics

Automotive

Buildings and Construction

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)