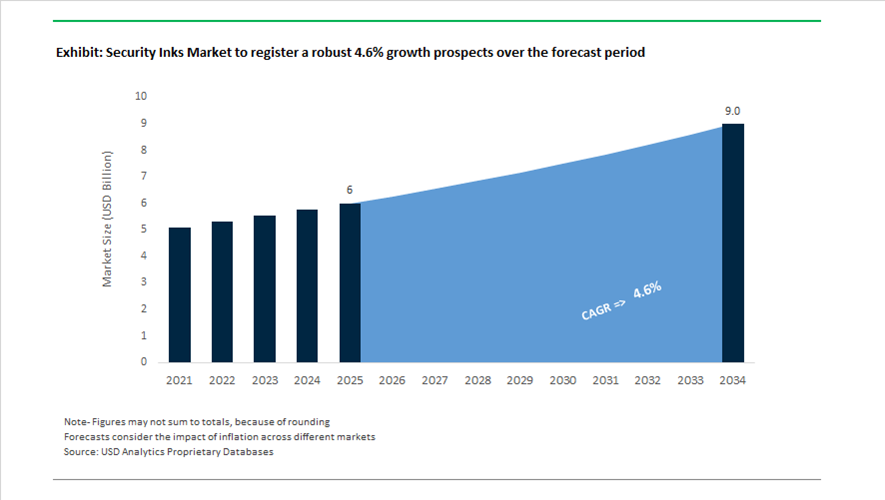

Security Inks Market Valued at $6 Billion in 2025, Projected to Reach $9 Billion by 2034 at 4.6% CAGR

The global security inks market is valued at $6 billion in 2025 and is projected to reach $9 billion by 2034, expanding at a CAGR of 4.6%. Growth is driven by rising demand for anti-counterfeiting inks, optically variable inks (OVI), infrared (IR) and ultraviolet (UV) reactive inks, intaglio inks, taggant-based forensic inks, variable data printing (VDP) inks, and digital-physical authentication systems used in banknotes, passports, tax stamps, pharmaceuticals, luxury goods, and secure packaging. Governments and brand owners are increasingly adopting multilayered security architectures that combine physical ink markers with digital verification platforms to combat illicit trade, document fraud, and supply chain diversion.

Strategic consolidation reshaped the competitive landscape in 2024–2025. In early 2024, NanoMatriX launched MatriX-Intaglio, an IR-transparent, high-security ink engineered for financial and government printing applications, designed to resist duplication through high-resolution scanning or reproduction technologies. In 2024, IN Groupe finalized the acquisition of Gleitsmann Security Inks as part of its Digital Odyssey 2025 plan, vertically integrating critical ink capabilities into sovereign identity document and banknote production. In April 2025, the MAVNU consortium acquired hubergroup, followed by a September 2025 European operational realignment focusing on high-margin specialty and security ink segments. Throughout 2025, Microtrace expanded its forensic taggant ink systems, integrating them with proprietary machine-vision platforms to enable item-level authentication in electronics and pharmaceutical supply chains.

Technology integration accelerated in 2025. Kao Collins introduced SIGMA+ and Pitch Black inkjet systems compatible with HP platforms, enabling serialized, tamper-evident variable data printing for secure labels and transactional documents. Luminescence Sun Chemical debuted advanced inks linked to digital wallet authentication systems, supporting emerging “digital travel credential” pilots between Hong Kong and Tokyo, where printed security elements are verified via smartphone-based cryptographic interfaces. In September 2025, SICPA formed a joint venture with Commstack to deploy physical marker-based traceability solutions for high-value minerals, reinforcing sovereign chain-of-custody frameworks.

Cost pressures intensified entering 2026. Sun Chemical implemented significant price increases on nitrocellulose-containing products across Latin America in January 2026 due to global supply constraints linked to defense-sector diversion. Earlier, in January 2025, global pigment price adjustments reflected escalating raw material costs and stricter environmental compliance expenditures. In January 2026, hubergroup confirmed full compliance with the German Printing Ink Ordinance (GIO), underscoring regulatory alignment in food-contact and packaging inks.

The security inks market is increasingly defined by digital-physical authentication convergence, sovereign supply chain integration, forensic taggant innovation, IR/UV-responsive formulations, variable data inkjet systems, regulatory-driven pigment reformulation, and raw material supply volatility management. As counterfeiting sophistication rises and geopolitical risks influence secure document production, advanced specialty inks remain central to global anti-fraud infrastructure and high-value asset protection.

Key Trends and Strategic Opportunities Shaping the Global Security Inks Market

Central Bank–Led Indigenization and Next-Generation Banknote Security Programs

Central banks are increasingly positioning security inks as a strategic national asset rather than a commoditized printing input. Across major economies, banknote authorities are channeling capital toward domestic production capabilities and next-generation ink formulations to reduce exposure to geopolitical supply risks and escalating counterfeiting sophistication. In India, the Reserve Bank of India reported a 25% increase in security printing expenditure for FY25, reaching ₹6,372.8 crore, with a clear mandate to indigenize offset, numbering, and color-shifting intaglio inks. This shift signals a broader transition toward vertically controlled ink supply chains where performance specifications, traceability, and sovereign control outweigh pure cost considerations.

In the United States, the U.S. Bureau of Engraving and Printing has embedded security ink innovation at the core of its Catalyst banknote program, supported by a $936 million multi-year modernization budget. The investment in hot foil presses and advanced intaglio systems reflects rising demand for inks that support machine-readable, multi-spectral, and tactile features simultaneously. For ink manufacturers, this trend translates into longer qualification cycles but significantly higher switching costs once embedded into national currency platforms.

Escalation of Covert and Forensic Ink Adoption for Brand-Level Supply Chain Defense

Beyond currencies, security inks are becoming central to brand protection strategies in pharmaceuticals, electronics, and personal care, where counterfeiting now extends deep into last-mile distribution networks. By late 2025, brand owners are moving decisively away from overt features such as holograms toward covert and forensic inks that remain invisible to consumers but verifiable under regulatory or legal scrutiny. UV-reactive, thermochromic, and taggant-based inks with microscopic chemical signatures are increasingly specified at the SKU level to enable item-by-item authentication during investigations.

In the United States, demand for anti-counterfeit packaging solutions that rely heavily on secure printing technologies has been valued at approximately $6.7 billion in late 2025, with strong momentum driven by electronics and personal care manufacturers seeking legal-grade proof of product origin. This trend is structurally favorable for security ink suppliers with in-house chemical authentication capabilities, as buyers now prioritize evidentiary strength and chain-of-custody validation over visual complexity alone.

Monetizing the Physical–Digital Authentication Layer Through Secure QR Integration

The convergence of physical security inks with digital identity systems represents one of the highest-value growth opportunities in the security inks market. Governments and enterprises are increasingly deploying QR codes for identity verification, product traceability, and regulatory compliance, creating demand for inks that make these codes physically unforgeable. Advanced formulations using nanoparticles and infrared-visible coatings enable scanners to verify not only the digital payload of a QR code but also its underlying chemical fingerprint.

In March 2025, researchers at the Institute of Nano Science and Technology demonstrated strontium bismuth fluoride nanoparticle-based security inks designed specifically for smart authentication environments. As QR scanning volumes reached billions per month in early 2025, compliance with ISO 18004:2024 has emerged as a commercial differentiator, favoring ink suppliers capable of delivering smartphone-readable codes with embedded covert layers accessible only to authorized inspection devices. This positions security ink vendors as critical enablers of physical-digital twins rather than downstream printing suppliers.

Scaling Sustainable and ESG-Compliant Security Ink Platforms

Environmental compliance is rapidly evolving from a reputational issue into a procurement requirement for both central banks and brand owners, creating a parallel opportunity for sustainable security ink innovation. The historical reliance on mineral oils, solvents, and heavy metals is increasingly incompatible with public-sector ESG mandates and sustainable packaging initiatives. In response, leading suppliers are commercializing mineral-oil-free, water-wipe, and compostable security ink systems that preserve high barrier performance while reducing lifecycle emissions.

Industry leader SICPA reported the successful circulation of banknotes printed with mineral-oil-free offset inks featuring high biorenewable content, alongside the deployment of water-wiping intaglio inks to reduce solvent usage. At the specialty end of the market, Zanasi has introduced OK Compost INDUSTRIAL certified Thinkz inks compliant with EN 13432, enabling secure marking of compostable packaging without compromising microbial degradation. As ESG-linked procurement criteria tighten, sustainable security inks are transitioning from niche innovation to a decisive bidding requirement across currencies, packaging, and regulated goods markets.

Security Inks Market Share and Segmentation Insights

Overt Security Inks Dominate the Market as Visible Authentication Features Remain Critical

Overt security inks accounted for 42.80% of the security inks market in 2025, making them the most widely deployed technology for document and currency authentication. These inks include optically variable inks, color-shifting inks, and metameric inks that allow immediate visual verification without specialized detection equipment. Their use is critical in banknotes, passports, and high-value official documents, where public verification serves as the first line of defense against counterfeiting. A major 2025 technology advancement is the evolution of optically variable pigment systems, which create complex color changes when viewed at different angles. Modern overt security inks also incorporate magnetic and machine-readable properties, strengthening their role in both visual authentication and automated verification systems used in financial and governmental security printing.

Currency & Banking Sector Drives Security Ink Demand as Central Banks Strengthen Anti-Counterfeiting Measures

Currency and banking remain the largest application segment in the security inks market, capturing 38.60% of global demand in 2025 due to the widespread circulation of banknotes and financial instruments. Modern banknotes incorporate multiple layers of security printing technologies including overt, covert, and machine-readable inks to prevent counterfeiting and maintain public confidence in currency systems. Central banks continually upgrade security features to stay ahead of increasingly sophisticated counterfeiting techniques. A key 2025 industry trend is the ongoing transition toward polymer banknotes, which offer improved durability and enhanced security feature integration. Security ink formulations have been adapted for polymer substrates, requiring optimized adhesion, flexibility, and resistance to abrasion while maintaining the visual and machine-readable properties essential for currency authentication.

Security Inks Market Competitive Landscape

The 2026 security inks market is driven by optically variable inks (OVI), machine-readable taggants, and AI-enabled authentication systems. Growth is fueled by polymer banknotes, tax stamp mandates, and pharmaceutical traceability, with increasing adoption of thermochromic, IR-invisible inks, and blockchain-backed track-and-trace technologies.

SICPA dominates sovereign security inks with SPARK Flow innovation and global central bank partnerships

SICPA Holding SA maintains a dominant position in the security inks market through extensive global operations and advanced forensic ink technologies. The company serves over 100 central banks and government entities with a workforce exceeding 3,000 across 30 locations. SPARK® Flow technology delivers dynamic optically variable effects that enhance banknote authentication and anti-counterfeiting protection. Participation in global anti-counterfeiting initiatives highlights its leadership in combating illicit trade across pharmaceuticals and luxury goods. Integration of security inks with digital public ecosystems supports identity protection and document authentication. Focus on machine-readable and Level 3 security features strengthens its role in sovereign currency and tax systems.

Sun Chemical advances compliant security printing with UV LED inks and digital color management systems

Sun Chemical is strengthening its position in security inks through sustainable formulations and digital printing integration. SolarScreen Wave UV LED inks enable migration-compliant printing on food and pharmaceutical packaging, supporting regulatory compliance. SunColorBox technology enhances precision in managing complex spot colors and confidential ink formulations across production networks. Expansion of manufacturing capabilities in Shanghai improves supply chain responsiveness in high-growth Asian markets. Integration with DIC Corporation provides access to advanced degassing technologies that optimize inkjet printing performance. Focus on packaging security and digital ink management supports growth in labeling and authentication applications.

De La Rue accelerates polymer banknote security with ASSURE feature and strengthened currency order pipeline

De La Rue plc is reinforcing its leadership in banknote security through polymer substrate innovation and strategic restructuring. Acquisition by Atlas Holdings provides financial stability to focus on its currency business and long-term growth strategy. ASSURE™ technology introduces a Level 3 forensic security feature embedded within polymer banknotes for advanced authentication. A strong £347 million order book supports growth through new contracts with central banks in emerging markets. Partnership with Canadian Bank Note enhances capabilities in secure document manufacturing, including passports. Focus on high-security substrates and integrated ink technologies supports evolving global currency standards.

Kao Collins pioneers taggant-based authentication with invisible ink technologies and industrial inkjet integration

Kao Collins is advancing the security inks market through taggant-based authentication and industrial inkjet solutions. Collaboration with Honeywell Authentication Technologies enables development of customized inks readable only by specific detection systems. Product portfolio includes UV, IR, and invisible fluorescent inks tailored for thermal and piezo inkjet applications. Clear UV curable inks provide covert security layers for ID cards and financial instruments. Strategic focus on specialized environments supports applications in aerospace, defense, and high-security labeling. Emphasis on “lock and key” authentication enhances brand protection and anti-counterfeiting capabilities.

Microtrace delivers AI-powered forensic taggant systems with spectral fingerprinting and real-time authentication

Microtrace, LLC is strengthening its role in security inks through advanced taggant chemistry and AI-driven verification platforms. Spectral Taggant™ technology creates unique molecular signatures embedded in inks and labels for forensic authentication. Integration with the Summit™ platform and Alerion™ AI enables real-time counterfeit detection using handheld devices. IR-to-IR phosphor technology provides covert protection layers for sensitive applications such as military equipment and pharmaceuticals. Expansion of customized risk assessment services enhances supply chain security strategies for global brands. Focus on digital-physical convergence supports next-generation authentication ecosystems.

Switzerland: Global Benchmark for Forensic and Phygital Security Inks

Switzerland occupies a structurally dominant position in the global security inks industry, anchored in forensic science leadership, standards-setting influence, and deep integration with sovereign security systems. In late 2025, SICPA, headquartered in Prilly, expanded its Fuel Integrity program, deploying invisible forensic markers across more than 60 billion liters of petroleum products annually to combat tax evasion and fuel adulteration. This application alone highlights Switzerland’s ability to scale covert security inks into mission-critical national infrastructure. Beyond fuels, Swiss R&D capabilities continue to advance covert taggants, including high-refractive-index inks that respond to specific laser wavelengths, enabling instantaneous authentication in high-speed sorting and inspection environments such as customs and currency processing.

Switzerland is also shaping the future convergence of physical and digital security. SICPA’s Series A-extension investment in Metaco has accelerated the development of “phygital” security solutions that link physical security inks with digital asset custody frameworks, a priority area for central banks exploring hybrid cash–CBDC ecosystems. Government-backed laboratories in Lausanne remain global centers of excellence for DNA-based and molecular security inks, reinforcing Switzerland’s role as a hub for next-generation covert authentication. Regulatory leadership further amplifies this position, as Switzerland continues to act as a principal drafter within ISO/TC 247, influencing global standards for machine-readable and forensic anti-counterfeiting technologies. As of early 2026, Swiss-manufactured security inks are embedded in passport and national ID programs of more than 80 countries, underscoring their global trust and adoption.

India: Rapid Scale-Up Driven by National Security and Traceability Mandates

India represents one of the fastest-expanding security inks markets, propelled by national security priorities, anti-counterfeiting mandates, and export-oriented traceability requirements. In March 2025, the Bhabha Atomic Research Centre, in collaboration with the Institute of Nano Science and Technology, unveiled a novel security ink based on strontium bismuth fluoride nanoparticles. This development directly targets high-value document forgery and signals India’s growing capability in advanced nanomaterial-based authentication technologies. Parallel to public-sector innovation, industry coordination has intensified, with the Authentication Solution Providers’ Association hosting the 6th Traceability and Authentication Forum in New Delhi to push for mandatory security ink adoption in pharmaceutical and agricultural packaging.

Manufacturing capacity has expanded in response to regulatory pressure. Sun Chemical introduced its expanded digital textile and security ink portfolio at GTTES India 2025, aligning with rising brand-protection requirements across consumer goods. At the sovereign level, the Security Printing and Minting Corporation of India Ltd upgraded its Dewas Ink Factory to incorporate advanced Optically Variable Ink production lines, strengthening domestic self-reliance for currency and secure documents. Regulatory drivers are decisive. India’s Track and Trace mandate for pharmaceutical exports has tripled domestic demand for UV-fluorescent and infrared-responsive batch-coding inks, while intensified banking fraud mitigation efforts in 2025 have resulted in compulsory enhanced security features across financial instruments.

United Kingdom: Currency-Centric Innovation with Sustainability Integration

The United Kingdom remains a critical innovation center for banknote and identity-related security inks, with strong spillover into sustainability-compliant printing technologies. In late 2025, De La Rue confirmed that its Enhanced GEMINI™ UV print feature had been integrated into more than 150 banknote denominations globally, offering dual-color hidden patterns visible under ultraviolet light. This reinforces the UK’s entrenched position in currency-grade overt and covert ink technologies. Government demand continues to underpin the market, with the UK Home Office extending its use of biometric-linked security inks for next-generation residency permits through 2027.

Sustainability and advanced materials are becoming differentiators. Sun Chemical’s UK division launched the Xennia Sapphire pigment ink range in 2025, embedding authentication layers while meeting stringent ZDHC environmental standards. UK-designed security features are also gaining traction internationally, with central banks such as the Central Bank of Samoa transitioning to polymer substrates enhanced with ARGENTUM™ and ROTATE™ iridescent ink technologies. On the innovation front, collaborations between UK universities and private firms have entered pilot phases for smart inks that respond to environmental tampering or time-delay triggers, expanding the functional scope of security inks beyond static authentication.

Germany: Industrial-Grade Security Inks and IoT-Enabled Authentication

Germany’s security inks market is defined by its integration into currency technology, industrial anti-counterfeiting, and emerging IoT-based authentication systems. Giesecke+Devrient expanded its Currency Technology segment in 2025, emphasizing Banknote Fiber Extraction and high-durability intaglio inks designed to extend the lifecycle of physical cash in circulation. Beyond currency, German manufacturers such as Siegwerk and Marabu have scaled production of thermochromic and reactive inks for automotive and aerospace components, directly addressing grey-market spare part risks.

Regulatory compliance is a structural advantage. German security ink formulations lead in adherence to the German Ink Ordinance, ensuring migration resistance and non-toxicity for food-contact and pharmaceutical packaging. Innovation is increasingly intersecting with digital infrastructure. G+D’s work on Massive IoT security involves conductive security inks printed as antennas or sensors on labels, enabling real-time product authentication and traceability. Supporting this shift, Germany has invested in automated falling film sulfonation systems to produce ultra-pure chemical intermediates required for liquid security inks with consistent optical performance.

United States: Bio-Based Transition and Federal Procurement Momentum

In the United States, security ink demand is being reshaped by federal procurement standards, sustainability programs, and advanced taggant technologies. The EPA Safer Choice and USDA BioPreferred programs are increasingly certifying security inks formulated with bio-based solvents, driving adoption across packaging and government documentation. Capacity expansion reflects this momentum, with Stepan Company and Kao Collins expanding facilities in Pasadena and Cincinnati respectively to boost output of magnetic and invisible inkjet inks.

Technological differentiation is accelerating. U.S.-based firms such as Flint Group are advancing nano-taggants and energy-sensitive microtaggants that can be decoded using low-cost handheld scanners, reducing authentication barriers for inspectors and retailers. Policy alignment further reinforces demand. New 2025 federal guidelines for secure government documents mandate the use of at least three layers of security inks overt, covert, and forensic cementing long-term institutional demand across federal agencies.

China: Scale Manufacturing and Nano-Structural Innovation

China combines scale manufacturing with aggressive investment in next-generation security ink chemistries. Domestic leaders such as Winnerjet and Sinopec have expanded production of C14–C17 alkane-based specialty inks, forming the backbone for high-volume security labeling across consumer goods and logistics. Regulatory shifts are shaping formulation strategies. The Ministry of Ecology and Environment’s 2025 update to its Priority Controlled Chemical Substances list favors water-based security inks, accelerating substitution away from solvent-heavy systems.

China’s competitive edge increasingly lies in materials science. Concentration of production within Jiangsu and Zhejiang chemical parks has created an integrated supply ecosystem spanning electronic cleaning, security marking, and advanced coatings. Strategic R&D investments are targeting nano-structure color-changing inks that rely on physical light interference rather than pigments, making them exceptionally difficult to replicate through conventional chemical analysis. This positions China not only as a volume supplier but also as a future leader in structurally complex, high-barrier security ink technologies.

Security Inks Industry: Country-Level Strategic Summary

Security Inks Market County Level Snapshot

|

Country

|

Core Strategic Focus

|

Structural Impact on Market

|

|

Switzerland

|

Forensic markers, DNA inks, global standards

|

Global reference point for sovereign-grade security

|

|

India

|

National security, pharma traceability, capacity build-up

|

Fastest growth driven by regulation and exports

|

|

United Kingdom

|

Currency inks, sustainability, smart inks

|

Leadership in banknote and ID innovation

|

|

Germany

|

Industrial anti-counterfeiting, IoT inks

|

High-value integration with Industry 4.0

|

|

United States

|

Bio-based inks, federal procurement, nano-taggants

|

Policy-driven demand with tech differentiation

|

|

China

|

Scale manufacturing, nano-structural inks

|

Transition from volume to advanced materials leader

|

Security Inks Market Report Scope

Security Inks Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6 Billion

|

|

Market Size (2034)

|

$9 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Type (Overt Security Inks, Covert Security Inks, Forensic Security Inks, Specialized Security Inks), By Printing Method (Intaglio Printing, Flexographic Printing, Offset Printing, Screen Printing, Letterpress Printing, Digital Printing), By Application (Currency & Banking, Official Documents, Product Authentication, Taxation, Logistics & Supply Chain)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SICPA Holding SA, Giesecke Devrient GmbH, DIC Corporation, De La Rue plc, Flint Group, Siegwerk Druckfarben AG, Toyo Ink SC Holdings Co. Ltd., Kao Collins Corporation, INX International Ink Co., Hubergroup, Chromatic Technologies Inc., Microtrace LLC, Winnerjet Digital Post Printing Technology Co. Ltd., T K TOKA Corporation, Marabu GmbH Co. KG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Security Inks Market Segmentation

By Type

- Overt Security Inks

- Covert Security Inks

- Forensic Security Inks

- Specialized Security Inks

By Printing Method

- Intaglio Printing

- Flexographic Printing

- Offset Printing

- Screen Printing

- Letterpress Printing

- Digital Printing

By Application

- Currency & Banking

- Official Documents

- Product Authentication

- Taxation

- Logistics & Supply Chain

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Security Inks Industry

- SICPA Holding SA

- Giesecke Devrient GmbH

- DIC Corporation

- De La Rue plc

- Flint Group

- Siegwerk Druckfarben AG

- Toyo Ink SC Holdings Co. Ltd.

- Kao Collins Corporation

- INX International Ink Co.

- Hubergroup

- Chromatic Technologies Inc.

- Microtrace LLC

- Winnerjet Digital Post Printing Technology Co. Ltd.

- T K TOKA Corporation

- Marabu GmbH Co. KG

*- List not Exhaustive