Selenium Market Valuation 2025–2034: $529.1 Million to $871.4 Million at 5.7% CAGR Driven by Refining Expansion and High-Purity Demand

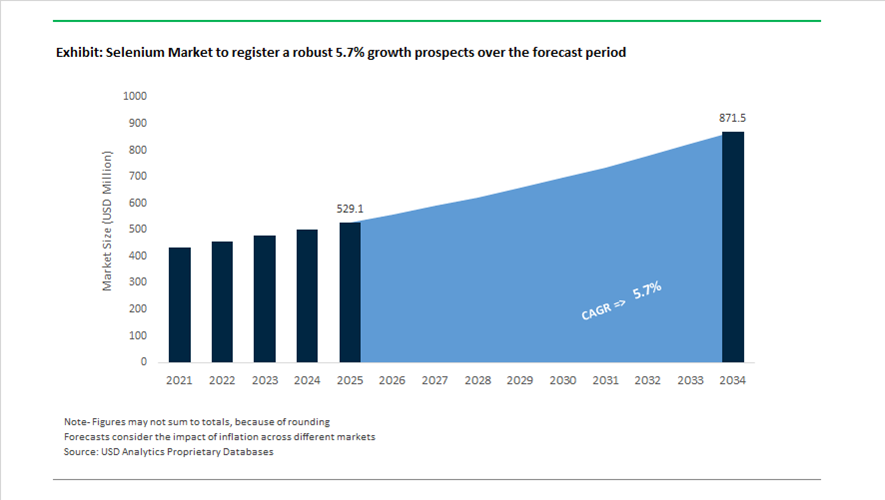

The global selenium market is valued at $529.1 million in 2025 and is projected to reach $871.4 million by 2034, expanding at a CAGR of 5.7%. Growth is closely linked to rising demand for high-purity selenium in semiconductor manufacturing, photovoltaic (PV) systems, specialty glass production, medical imaging components, and advanced metallurgy. Selenium, primarily recovered as a byproduct of copper refining from anode slimes, is increasingly benefiting from global investments in electrolytic copper capacity and secondary smelting infrastructure. Supply dynamics remain structurally tied to copper production trends, making capacity expansions in copper refineries a central driver of refined selenium availability.

In 2024, China maintained a dominant position in global selenium production. According to the 2025 USGS Mineral Commodity Summary, China accounted for nearly 50% of global refined selenium output in 2024. This leadership is directly associated with a 60% increase in electrolytically refined copper capacity over the past decade, strengthening the country’s position in selenium recovery. The structural link between copper refining throughput and selenium output underscores how copper smelting investments are shaping global selenium market balance, pricing trends, and export flows.

The market landscape between 2024 and 2026 reflects a coordinated wave of refining expansions and technological upgrades across Europe, Central Asia, and North America. In 2024, Serbia’s Bor refinery completed a major technical upgrade, leading to a significant increase in refined selenium output derived from copper anode slimes. This positioned Serbia as a more competitive European supplier. In early 2025, Kazakhmys Progress LLP commercialized a novel eco-friendly high-purity selenium production method at its new Balkhash plant, with an annual capacity of 75 tons. The facility targets semiconductor and advanced electronics applications, signaling a structural shift toward high-margin specialty selenium grades rather than bulk metallurgical output.

Further strengthening the supply base, Aurubis AG initiated expansion of its Bulgaria tankhouse between 2025 and 2026, aiming to increase capacity by 50% to 340,000 metric tons. This expansion significantly enhances its capability to recover high-grade selenium byproducts. In early 2026, Aurubis also reported the scheduled ramp-up of its Richmond plant in the United States, the first secondary multimetal smelter in the country. Designed to process 180,000 metric tons of complex recycling materials annually, the facility is expected to improve domestic availability of recovered selenium and reduce reliance on imports. Meanwhile, Sweden’s Rönnskär refinery is progressing through rebuilding efforts following the June 2023 fire that halted production, with selenium output normalization anticipated through 2025 and 2026. These developments collectively reinforce the selenium supply chain resilience across multiple geographies while supporting the projected 5.7% CAGR through 2034.

Strategic Trends and High-Conviction Opportunities in the Global Selenium Market

Sovereign Supply Chain Fortification and Critical Mineral Policy Integration

The selenium market is undergoing a structural re-rating as governments formally embed selenium into national security, clean energy, and semiconductor supply frameworks. Once treated as a by-product commodity, selenium is now classified as a policy-prioritized critical material due to its concentrated refining base and irreplaceable role in solar photovoltaics, advanced electronics, and specialty glass manufacturing. In late 2024, the U.S. Department of the Interior, through the U.S. Geological Survey, finalized the 2025 Critical Minerals List, reaffirming selenium’s strategic status alongside rare earths and battery metals. This designation enables accelerated permitting, federal funding access, and project visibility under the FAST-41 framework, materially lowering development risk for domestic selenium recovery initiatives linked to copper refining.

A similar policy shift is evident in India, where the Ministry of Mines has placed selenium on its 30 Critical Minerals list. Reports from the Council on Energy, Environment and Water in September 2025 indicate active government consideration of stockpiling mandates and Production Linked Incentives to upgrade domestic selenium refining purity. This move directly supports India’s 495 GW renewable energy ambition, as selenium purity constraints remain a bottleneck for advanced solar and power electronics manufacturing.

Precision Selenium Doping in Energy-Efficient Architectural and Smart Glass

Beyond policy, selenium demand is being structurally reinforced by its growing role in high-performance architectural glass, where energy efficiency standards are tightening rapidly across Europe and North America. Glass manufacturers are moving beyond basic iron neutralization and increasingly deploying selenium as a precision dopant to control solar heat gain coefficient, visible light transmission, and aesthetic neutrality in advanced glazing systems. In October 2025, Saint-Gobain announced its five-year Lead & Grow strategy, committing €12 billion in growth capex and acquisitions through 2030. A central pillar of this plan is the expansion of its Oraé low-carbon glass platform across Europe and India, which relies on selenium-based decolorization and doping to achieve high thermal performance without compromising clarity.

At GlassBuild 2025, manufacturers showcased a marked increase in triple-pane insulated glass units incorporating selenium-enhanced coatings, aligned with 2025 building energy codes. These systems are projected to reduce building operational emissions by up to 40%, reinforcing selenium’s role as an enabling material in Net Zero 2050 building decarbonization pathways promoted by the International Energy Agency.

Optimization of Hydrometallurgical Selenium Recovery from Copper Assets

With more than 90% of global selenium supply derived from copper anode slimes, recovery efficiency represents one of the most attractive near-term value creation levers in the selenium market. Advances in hydrometallurgical processing are enabling higher and more consistent selenium yields from variable-grade feedstocks, transforming selenium from a marginal by-product into a meaningful revenue stream. Industrial research published in 2025 demonstrates that alkaline oxidizing leaching systems using ClO and OH media can achieve selenium dissolution rates approaching 90% from decopperized anode slimes.

This opens significant opportunity for mining and equipment leaders such as Sandvik and Rio Tinto to deploy advanced flowsheets across existing copper operations. At the Copper to the World 2025 conference, the South Australian Department for Energy and Mining reaffirmed its strategy to position South Australia as a global copper and by-product hub, with innovation programs targeting selenium recovery from tailings and legacy waste streams for electronics-grade supply.

Scaling Selenium-Based Thin-Film PV for Building-Integrated Solar Applications

A second high-conviction opportunity lies in the acceleration of selenium-based thin-film photovoltaics for Building-Integrated Photovoltaics applications. Technologies based on Copper Indium Gallium Selenide and emerging CZTSe kesterite compounds are gaining traction due to superior low-light performance, mechanical flexibility, and faster energy payback times compared with crystalline silicon. Peer-reviewed studies published in November 2025 indicate that CdTe and CIGS modules achieve energy payback periods of 0.8 to 1.5 years, versus 2 to 3 years for conventional silicon, making them well suited for active facades and transparent solar glazing.

In India, the Central Electricity Authority reported that national PV manufacturing capacity expanded from 2.3 GW in 2014 to over 100 GW by 2025. National energy roadmaps increasingly highlight perovskite-selenium tandem modules as a pathway to unlock urban BIPV markets and overcome efficiency ceilings in standard silicon technologies, positioning selenium as a cornerstone material in the next phase of distributed solar adoption.

Selenium Market Share and Segmentation Insights

Commercial Grade Selenium Leads Market Consumption Across Glass, Metallurgy, and Agricultural Applications

Commercial grade selenium accounted for 48.60% of the selenium market in 2025, making it the most widely consumed grade across industrial sectors. With typical purity levels ranging from 99% to 99.5%, commercial grade selenium provides a cost-effective solution for large-scale applications including glass manufacturing, metallurgical alloying, and agricultural feed additives. In glass production, selenium is used for decolorization and color control, while in metallurgy it improves steel machinability and alloy performance. A major 2025 market dynamic is the strong supply chain linkage between selenium production and copper refining, as more than 90% of global selenium supply originates from copper anode slimes generated during electrolytic copper refining, making selenium availability closely tied to global copper production activity.

Agriculture & Feed Applications Drive Global Selenium Demand

Agriculture and animal feed represent the largest application segment in the selenium market, accounting for 34.80% of global demand in 2025 due to the essential nutritional role selenium plays in livestock health. Selenium compounds such as sodium selenite and sodium selenate are widely incorporated into feed formulations to prevent selenium deficiency diseases, improve immune response, and support reproductive performance in poultry, cattle, and swine production. The scale of global livestock farming ensures consistent demand for selenium-based feed additives. A key 2025 industry trend is the shift toward precision livestock nutrition, where supplementation levels are adjusted according to regional soil selenium concentrations, feed composition, and species-specific nutritional requirements, with organic selenium sources such as selenomethionine and selenium yeast gaining adoption in premium livestock production systems.

Selenium Market Competitive Landscape

The 2026 selenium market is driven by high-purity refining (99.9%–99.999%), copper byproduct dependency, and rising demand from photovoltaics, semiconductors, and energy storage. Growth is supported by sustainable recovery technologies, bio-leaching innovations, and government-backed critical mineral supply chain strategies.

KGHM strengthens high-purity selenium supply through integrated copper refining and byproduct optimization

KGHM Polska Miedź S.A. maintains a strong position in the selenium market through vertically integrated copper mining and refining operations. Electrolytic copper production reached 50.3 thousand tonnes in January 2026, ensuring a steady flow of selenium-rich anode slimes. EBITDA of PLN 7.2 billion in 2025 supports continued investment in recovery optimization. Upgrades at the Głogów facility enhance extraction efficiency for selenium and associated critical metals. Control across the value chain enables consistent production of high-purity selenium exceeding 99.5%. Focus on metallurgy and glass applications reinforces its role as a stable global supplier.

Rio Tinto advances circular selenium recovery with Kennecott expansion and solar-integrated mining operations

Rio Tinto is strengthening its selenium production through circular mining practices at its Kennecott operations in the United States. A 25 MW solar plant integrates tellurium-based materials, demonstrating scalable byproduct utilization models applicable to selenium photovoltaics. The Apex underground expansion increases ore throughput and supports continuous generation of selenium-bearing slimes. Collaboration with downstream partners enhances conversion into semiconductor-grade materials. Strategic focus on domestic supply aligns with U.S. critical mineral policies and energy transition goals. Investment in refining innovation supports high-purity selenium applications in thin-film solar technologies.

Southern Copper maximizes selenium byproduct efficiency amid production variability and large-scale capital expansion

Southern Copper Corporation is optimizing selenium recovery through efficient smelting and refining operations across Latin America. Record 2025 sales of $13.4 billion highlight strong byproduct contribution to revenue growth. Despite projected copper output decline in 2026, the company is enhancing recovery rates to stabilize byproduct margins. A $1.925 billion capital investment plan supports advanced processing technologies and new mining projects. Operating cash cost of $0.58 per pound underscores the financial impact of byproducts such as selenium. Focus on cost efficiency and production resilience supports long-term competitiveness in the global market.

Sumitomo integrates sustainable smelting and advanced materials to enhance high-purity selenium applications

Sumitomo Metal Mining Co., Ltd. is advancing selenium production through sustainable smelting and materials innovation. The Toyo Smelter achieved Copper Mark certification, validating responsible byproduct recovery practices. Integration with its Materials Business enables development of high-purity selenium compounds for electronics and battery applications. Financial strategy updates reflect strong profitability across refining and advanced materials segments. R&D initiatives focus on next-generation materials including nano-scale compounds for energy and electronics. Emphasis on ESG compliance and downstream integration strengthens its position in high-value selenium applications.

Mitsubishi Materials accelerates circular selenium recovery with e-waste integration and materials informatics innovation

Mitsubishi Materials Corporation is transforming selenium supply through a circular resource recovery model. Establishment of a Resource Circulation Division and acquisition of Elemental USA expand its e-waste recycling capabilities. Strategy focuses on recovering selenium from electronic scrap to reduce dependency on primary mining. Materials Informatics tools enable discovery of advanced selenium-based compounds for photocatalysis and environmental applications. Integration across recycling, refining, and electronic materials supports a closed-loop supply chain. Expansion into Western markets strengthens access to sustainable feedstock and high-purity selenium production.

Kazakhstan: Emergence as a High-Purity Selenium Origin with Asian Supply Linkages

Kazakhstan has moved decisively from a by-product supplier to a value-added selenium producer, supported by indigenous process innovation and state-backed critical mineral strategy. In March 2025, Kazakhmys Progress at the Balkhash complex successfully produced the country’s first ST-1 technical-grade selenium using a proprietary vacuum distillation method. Developed in collaboration with the Institute of Metallurgy and Ore Beneficiation, this process increased the value-added margin from approximately 30% to 97%, fundamentally changing the economics of selenium recovery from anode slimes. The first commercial batch reached 100 tons at 99.5% purity, meeting international non-ferrous metallurgy benchmarks and enabling direct participation in export-oriented specialty markets.

This production capability is underpinned by scale and continuity in upstream copper operations. KAZ Minerals reported record ore throughput of 50.6 million tonnes in H1 2025, ensuring a stable flow of selenium-bearing anode slimes for domestic refining. On the innovation side, Satbayev University’s late-2025 partnership with the Korea Institute of Industrial Technology has established a joint research center focused on advanced mineral processing, reinforcing Kazakhstan’s alignment with South Korean semiconductor supply chains. The government’s designation of selenium as a strategic critical mineral further supports long-term export positioning into high-purity electronics and alloy markets.

China: Scale Leadership with Policy-Driven Clean Recovery and New Applications

China remains the structural anchor of global selenium supply, benefiting from a decade-long expansion in electrolytic copper refining that has lifted selenium recovery volumes alongside primary metal output. A 60% increase in refining capacity over the past ten years has consolidated China’s dominance, particularly within the integrated industrial clusters of Jiangsu and Jiangxi provinces, where selenium production feeds directly into domestic glass manufacturing, electronics, and chemical synthesis. Major smelters such as Jiangxi Copper have optimized anode slime treatment systems to handle higher impurity loads while consistently achieving 99.9% selenium purity, strengthening reliability for downstream users.

Policy has become a key shaping force. The Ministry of Ecology and Environment’s 2025 update to the Priority Controlled Chemical Substances list incentivizes cleaner selenium recovery technologies to curb emissions, accelerating capital upgrades across smelting operations. At the same time, China is expanding demand-side applications. The 2025–2030 Bio-fortification Plan mandates selenium-enriched fertilizers in central grain-producing regions to address soil deficiencies, creating a structurally stable domestic outlet. In parallel, Shanghai-based R&D zones have advanced nano-selenium catalysts into large-scale pilot phases, opening higher-value pathways in specialty chemical synthesis beyond traditional pigment and glass uses.

United States: Import Dependence Driving Recovery Innovation and Clean-Energy Demand

The United States remains structurally reliant on selenium imports, with over 50% dependency identified by the U.S. Geological Survey as of 2025. This reliance has elevated selenium’s profile in federal critical mineral discussions, particularly as clean-energy and advanced manufacturing applications expand. Domestic production is concentrated, with Rio Tinto Kennecott in Utah standing as one of only two major producers, recovering crude selenium through its integrated copper smelting operations. Federal funding under the Bipartisan Infrastructure Law is now supporting the development of dedicated selenium and tellurium recovery circuits to reduce exposure to East Asian supply risks.

Demand-side momentum is strengthening. Expansion of CIGS solar cell manufacturing in the U.S. Southwest has increased localized demand for ultra-high-purity selenium at 99.999% levels, while the EPA’s 2025 effluent guidelines for steam electric power plants have driven adoption of selenium capture technologies, creating a secondary recycled supply stream. Operational alignment with sustainability goals is also notable. Rio Tinto Kennecott’s 2025 roadmap targets a 15% reduction in Scope 1 and 2 emissions, positioning selenium output within broader “green copper” certification frameworks that are increasingly valued by downstream clean-tech customers.

Japan: Precision Refining and Electronics-Centric Selenium Applications

Japan’s selenium market is defined by precision refining and deep integration into electronics, sensor, and automotive electrification value chains. Leading refiners Sumitomo Metal Mining and JX Nippon Mining & Metals upgraded their Toyo and Hitachi refineries to supply electronic-grade selenium pellets tailored for global sensor and optoelectronic markets. These upgrades reflect Japan’s emphasis on consistency, traceability, and ultra-tight impurity control, which remain critical differentiators in high-end applications.

Strategically, Sumitomo Metal Mining’s Three-Year Business Plan 2027, launched in May 2025, identifies the stable supply of minor metals including selenium as a core pillar supporting vehicle electrification. Technological collaboration between refiners and Japanese electronics firms has also delivered selenium-based thin-film coatings for next-generation LiDAR systems in 2025, signaling continued application diversification. Sustainability credentials reinforce competitiveness. The Toyo Smelter & Refinery’s achievement of The Copper Mark in late 2025 verifies that selenium by-products are responsibly sourced, supporting Japan’s strong export position in high-purity selenium dioxide for European glass and pharmaceutical industries.

Poland: Europe’s Anchor Supplier with Circular Economy Alignment

Poland plays a pivotal role as the European selenium supply hub, anchored by KGHM Polska Miedź and its Głogów Copper Smelter. The facility operates large-scale selenium recovery units, supplying consistent material flows to European downstream industries, particularly automotive and architectural glass manufacturers. In 2025, KGHM initiated a €150 million refinery modernization program to enhance recovery rates for precious and minor metals, including selenium and rhenium, improving both yield and process efficiency.

Regulatory alignment is shaping Poland’s strategic positioning. Transition toward compliance with the EU Circular Economy Action Plan has accelerated efforts to recover selenium from electronic waste streams, complementing primary production. Poland has also specialized in producing minimum 99.5% purity selenium flakes designed for European metallurgical alloy applications, while serving as a preferred supplier to Germany’s automotive glass sector for UV-tinted windshield formulations. This combination of scale, modernization, and regulatory readiness reinforces Poland’s role as a stabilizing force in the European selenium supply landscape.

Strategic Summary of Country-Level Dynamics

Selenium Market County Level Snapshot

|

Country

|

Strategic Focus

|

Structural Impact on Selenium Market

|

|

Kazakhstan

|

High-purity production, export alignment with Asia

|

Emerging value-added supplier with critical mineral status

|

|

China

|

Scale recovery, clean processing, new applications

|

Global volume leader with expanding specialty uses

|

|

United States

|

Domestic recovery, clean-energy demand

|

Innovation-driven supply security with secondary sources

|

|

Japan

|

Precision refining, electronics integration

|

High-purity exporter for sensors and advanced coatings

|

|

Poland

|

European hub, circular recovery

|

Stabilized EU supply with modernization and compliance

|

Selenium Market Report Scope

Selenium Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$529.1 Million

|

|

Market Size (2034)

|

$871.4 Million

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Grade (Commercial Grade, Pigment Grade, Electronic Grade, Food & Pharmaceutical Grade), By Form (Selenium Powder, Selenium Pellets & Granules, Selenium Flakes, Selenium Dioxide, Sodium Selenite & Selenate), By Source (Copper Anode Slimes, Lead & Nickel Refinery Residues, Secondary & Recycled Sources), By Application (Metallurgy, Glass Manufacturing, Agriculture & Feed, Electronics & Photovoltaics, Chemicals & Pigments, Pharmaceuticals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Rio Tinto Group, KGHM Polska Miedź SA, Sumitomo Metal Mining Co. Ltd., MMC Norilsk Nickel, Glencore plc, Ural Mining and Metallurgical Company, JX Nippon Mining & Metals Corporation, Sinopec Group, Jiangxi Copper Co. Ltd., Kazakhmys Progress LLC, Boliden AB, Mitsubishi Materials Corporation, Asarco LLC, Aurubis AG, Guangzhou Fineton Chemical Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Selenium Market Segmentation

By Grade

- Commercial Grade

- Pigment Grade

- Electronic Grade

- Food & Pharmaceutical Grade

By Form

- Selenium Powder

- Selenium Pellets & Granules

- Selenium Flakes

- Selenium Dioxide

- Sodium Selenite & Selenate

By Source

- Copper Anode Slimes

- Lead & Nickel Refinery Residues

- Secondary & Recycled Sources

By Application

- Metallurgy

- Glass Manufacturing

- Agriculture & Feed

- Electronics & Photovoltaics

- Chemicals & Pigments

- Pharmaceuticals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Selenium Industry

- Rio Tinto Group

- KGHM Polska Miedź SA

- Sumitomo Metal Mining Co. Ltd.

- MMC Norilsk Nickel

- Glencore plc

- Ural Mining and Metallurgical Company

- JX Nippon Mining & Metals Corporation

- Sinopec Group

- Jiangxi Copper Co. Ltd.

- Kazakhmys Progress LLC

- Boliden AB

- Mitsubishi Materials Corporation

- Asarco LLC

- Aurubis AG

- Guangzhou Fineton Chemical Co. Ltd.

*- List not Exhaustive