Market Overview: Rapid-Activation SMPs Reshaping Medical, Aerospace, and Smart Material Engineering

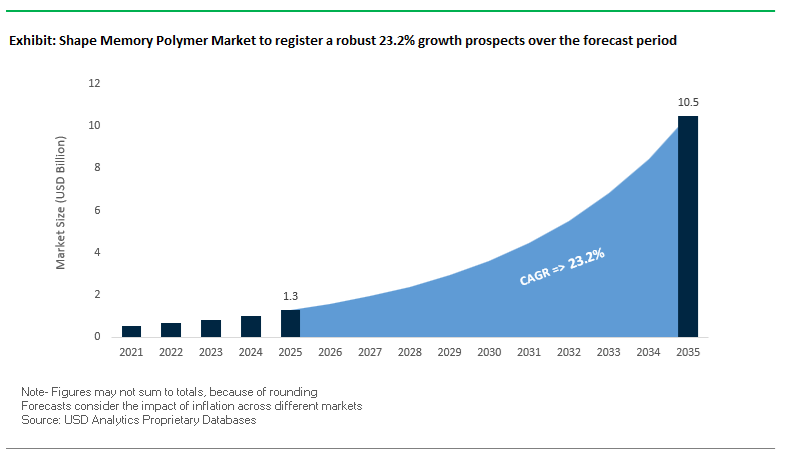

The Shape Memory Polymer Market is projected to grow exponentially from USD 1.3 billion in 2025 to USD 10.5 billion by 2035, registering an impressive CAGR of 23.2%. This steep growth curve is driven by the accelerated adoption of minimally invasive medical implants, aerospace morphing structures, advanced robotics, and 4D printing applications. Manufacturers and material suppliers are increasingly prioritizing strain recovery efficiency, glass transition temperature (Tg) tuning, multi-stimuli responsiveness, and composite reinforcement capabilities, which determine SMP performance in real-world conditions.

Shape Memory Polymers provide capabilities far beyond traditional materials. State-of-the-art polyurethane and methacrylate SMPs deliver ultimate reversible strains above 800%, more than 100× greater than Shape Memory Alloys (SMAs) which are limited to less than 8%. This performance advantage is transforming categories such as deployable implants, adaptive components in vehicles, soft robotics, and aerospace mechanisms. In medical applications, polyurethane SMPs engineered with Tg values near 37°C achieve >95% shape recovery within 30 seconds, a critical requirement for self-expanding stents, vascular embolization devices, and orthopedic implants. Composite SMP-CFR materials used in morphing aerospace structures maintain >98% shape recovery consistency over 10+ thermo-mechanical cycles, enabling repeatable, fatigue-resistant actuation.

Key insights for manufacturers and vendors

- 800%+ strain recovery creates new design freedom in medical implants, soft robotics, and dynamic actuators.

- Tg engineering near physiological temperature is becoming a core requirement for implantable SMP devices.

- Carbon-fiber reinforced SMP composites (SMPC-CFR) ensure >98% cycle repeatability, meeting aerospace reliability thresholds.

- Rapid recovery materials (≤30 seconds at 37°C) are now standard for next-generation vascular and structural implants.

- Sustainability focus increasing: strong industry shift toward biodegradable PCL/PLA SMPs for medical consumables and green packaging.

Market Analysis: Breakthrough Medical Approvals, 4D-Printing Progress, and Multi-Stimuli SMP Innovations

The Shape Memory Polymer industry has entered a high-momentum phase marked by regulatory milestones, 4D-printing advances, multi-stimuli material breakthroughs, and rising adoption in medical and aerospace systems. A landmark milestone occurred in January 2024, when the U.S. FDA granted marketing clearance for the IMPEDE-FX Embolization Plug, validating SMP technology as clinically reliable for peripheral vascular embolization. This approval has strengthened investor and OEM confidence in SMP-based implants, accelerating commercialization across cardiology, orthopedics, and regenerative medicine.

The innovation trajectory intensified further in August 2025, when researchers developed a multi-stimuli responsive SMP containing thermoplastic polyurethane blended with magnetic nanoparticles. This breakthrough enabled non-contact actuation via magnetic induction, opening new possibilities in soft robotics, micro-actuators, active surgical tools, and minimally invasive procedures requiring remote activation. The automotive sector is also recognizing SMP potential: in Q3 2025, a major automotive supplier committed USD 50 million to a new facility dedicated to lightweight composite parts incorporating SMPs for self-tightening seals, adaptive vents, and aerodynamic actuators.

Academic progress similarly underscores SMP adoption in biomedical engineering. In November 2024, the University of Texas published a study demonstrating 95% cell viability in 3D-printed SMP scaffolds loaded with growth factors, validating their applicability in tissue regeneration, implantable scaffolds, and soft biological structures. Parallel advancements in additive manufacturing are emerging. In May 2024, researchers successfully fabricated magnetic-responsive SMP grippers via SLS 4D printing, enabling programmable, noninvasive manipulation systems for robotics and precision assembly.

Defense and aerospace sectors continue to leverage SMP advantages. In Q4 2025, the U.S. Department of Defense continued funding SMP composites for adaptive winglets and reconfigurable antennas on UAVs, capitalizing on SMPs’ high shape fixity and low density. Finally, sustainability initiatives gained traction. In February 2024, leading polymer manufacturers expanded R&D programs dedicated to biodegradable PCL and PLA SMPs, supporting the shift toward eco-friendly medical consumables and sustainable packaging systems.

Clinical, Photothermal, Aerospace, and Sustainable Material Innovations Re-Shaping SMP Commercialization

Market Trend 1: Accelerating Clinical Adoption of Body-Temperature Responsive SMPs for Minimally Invasive Implants

A pivotal trend driving the Shape Memory Polymer Market is the rapid clinical adoption of body-temperature-responsive SMPs engineered for next-generation implantable medical devices, stents, occlusion systems, and self-expanding scaffolds. SMPs outperform Shape Memory Alloys (SMAs) due to their extremely high recoverable deformation; SMPs deliver recovery strains up to 400%, whereas SMAs exhibit less than 8% recoverable strain. This vast deformation range enables ultra-compact device designs that can be inserted through narrow catheters and deployed atraumatically inside the body.

To achieve safe in vivo operation, SMP formulations are precisely synthesized with glass transition temperatures (Tg) tuned to 37°C, enabling seamless actuation using only body heat, without external heating elements or mechanical triggers. The clinical benefit is significant: these materials exhibit low recovery stress (1–10 MPa) compared to the ~1,000 MPa generated by SMAs, reducing the risk of vessel wall irritation, tissue tearing, or inflammation during device deployment.

Biomedical-grade SMPs must also demonstrate exceptional shape-memory performance, with shape fixity and shape recovery rates both >90%, ensuring reliable in situ expansion and structural stability throughout the device’s operational life. These parameters—and the inherent biodevice compatibility of polymer-based systems—are positioning SMPs as a cornerstone material for next-generation soft implants, drug delivery platforms, and patient-tailored medical technologies.

Market Trend 2: Rapid Development of Light-Activated and Magnetically Triggered SMPs for Programmable Actuation

A second major trend is the emergence of light-activated (UV/NIR) and magnetic field-activated SMPs, enabling remote, programmable, and spatially selective actuation for advanced robotics, smart textiles, reconfigurable optics, and minimally invasive tools. By embedding highly efficient photothermal fillers such as gold nanoparticles or polydopamine (PDA) into the polymer matrix, near-infrared responsive SMPs achieve full shape recovery within 60 seconds under modest laser irradiation (1 W/cm² at 808 nm), enabling rapid, non-contact activation even inside opaque structures.

Light-based control also allows precise spatial manipulation; experimental SMP metamaterials have demonstrated controlled 10% bandgap shifts after 90 seconds of UV exposure, enabling programmable stiffness and vibration characteristics for smart structures.

Magnetically responsive SMPs—typically loaded with Fe₃O₄ nanoparticles—also unlock extremely fast actuation, achieving complete recovery in ~28 seconds under alternating magnetic fields or microwave heating. Notably, these effects can be achieved with filler concentrations as low as 0.1 wt%, highlighting the efficiency of photothermal and magnetic absorption mechanisms. These next-generation activation strategies are expanding the relevance of SMPs into fields requiring wireless control, high precision, and multifunctional material behavior.

Market Opportunity 1: High-Strength, Fiber-Reinforced SMP Composites for Deployable Space and Aerospace Structures

One of the highest-value opportunities in the Shape Memory Polymer Market lies in the development of structural SMP composites engineered for deployable space architectures—including booms, panels, antennas, solar arrays, and morphing aerospace components. Pure SMPs offer low stiffness (~1 GPa at room temperature), but when reinforced with continuous carbon fibers, the stiffness and strength can increase by an order of magnitude, enabling SMP-based composites to function as load-bearing aerospace materials.

A critical engineering requirement is that reinforcement must not compromise shape-memory function. Advanced CF-SMP composites retain exceptional shape-memory behavior, with shape recoverability up to 95% even under large bending deformations. During deployment, SMP structures must soften significantly; above Tg, axial stiffness can drop by 50% and flexural stiffness by up to 90%, ensuring low-force activation that minimizes shock loads on spacecraft.

SMP matrices used in aerospace composites typically generate maximum recovery stresses of ~4 MPa, providing sufficient force to deploy lightweight structures while preventing damage to delicate satellite components. As space agencies and private aerospace companies accelerate development of compact, lightweight, origami-style deployable structures, SMP composites are emerging as a strategically important enabling material.

Market Opportunity 2: Recyclable and Self-Healing SMPs for Circular, Durable, and Intelligent Consumer Products

The surge in sustainability-driven material innovation is creating unprecedented opportunities for recyclable and self-healing Shape Memory Polymers, particularly Covalent Adaptable Network (CAN) SMPs and vitrimers. These dynamic network polymers can undergo repeated reshaping and reprocessing, with certain vinylogous urethane vitrimers maintaining mechanical integrity through 10 recycling cycles at 150°C.

Self-healing functionality is also advancing quickly. CAN networks incorporating dynamic disulfide bonds show self-healing efficiencies up to 86.92% after 20 hours at 100°C, enabling recovery of strength and integrity in damaged consumer products, automotive trims, electronic housings, and wearables. Importantly, introducing disulfide bonds drops the activation energy for bond exchange from 94 kJ/mol to 51 kJ/mol, dramatically improving reprocessing speed and reducing manufacturing energy requirements.

For low-temperature applications, innovative elastomeric SMPs can complete self-healing at only 60°C within one hour, making them suitable for everyday consumer goods that demand durability without compromising end-of-life recyclability. As circular economy policies tighten globally, these recyclable, repairable, and reprocessable SMP chemistries position the market for long-term growth across consumer electronics, sporting goods, automotive interiors, and sustainable packaging.

Shape Memory Polymer Market Share Analysis

Market Share by Material Type: Polyurethane SMPs Lead Through Tunability and Biomedical Compatibility

Polyurethane (PU) Shape Memory Polymers command the largest market share—approximately 45%—because they offer the most versatile and application-ready combination of mechanical strength, strain recovery, and thermal responsiveness among all SMP material classes. Their intrinsic segmented molecular structure (hard segments for memory retention and soft segments for reversible switching) allows PU SMPs to achieve highly repeatable shape memory performance while remaining flexible enough for dynamic, load-bearing applications. A key factor driving their market dominance is their ability to be precisely engineered to activate at biologically relevant temperatures, especially the 30–40°C window required for minimally invasive medical devices. This tunability, combined with high fatigue resistance and excellent elongation-to-break values, makes PU SMPs ideal for cardiovascular stents, customizable prosthetic components, orthopedic devices, and self-expanding implants that demand reliable deployment in the human body. Their compatibility with large-scale manufacturing processes—such as extrusion, injection molding, and 3D printing—positions polyurethane SMPs as the preferred material for high-value medical and industrial applications. Because PU can be formulated into foams, elastomers, films, and engineered solids, it supports a broader product ecosystem than epoxy-, PLA-, or PVC-based SMPs, reinforcing its leadership as the highest-volume and highest-revenue segment in the global SMP market.

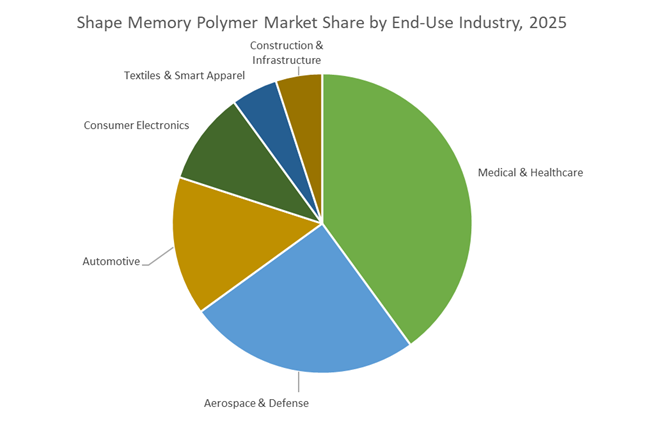

Market Share by End-Use Industry: Medical & Healthcare Dominates Due to Minimally Invasive Device Adoption

The Medical & Healthcare sector, holding roughly 40% of total market share, is the leading end-user of Shape Memory Polymers because SMPs uniquely enable minimally invasive therapies—a central trend shaping modern healthcare. SMP-based devices can be inserted into the body in a compact, low-profile temporary configuration and then expand or transform into their functional shape upon exposure to body temperature, hydration, or pH. This capability drastically reduces surgical trauma, shortens patient recovery time, and enhances procedural outcomes, making SMPs indispensable for next-generation stents, occlusion devices, self-tightening sutures, and tissue scaffolds. The sector’s dominance is further reinforced by stringent regulatory demands for biocompatibility and performance stability, which elevate the value of advanced polyurethane- and PLA-based SMP formulations that meet USP Class VI and ISO 10993 standards. As the global burden of cardiovascular disease, respiratory complications, orthopedic injuries, and chronic conditions increases, hospitals and device manufacturers are shifting toward customizable, responsive materials that can enhance device integration within the human body. Medical applications typically command higher unit prices and involve advanced engineering and regulatory validation, significantly boosting the segment’s revenue contribution. With clinical innovation accelerating—particularly in bioresorbable SMP scaffolds and smart polymer implants—the Medical & Healthcare sector remains the clear growth engine and the dominant end-use category shaping the long-term trajectory of the Shape Memory Polymer market.

Country Analysis: Global SMP Innovation and Industrial Adoption Hotspots

United States: Scaling Biocompatible SMP Implants and Aerospace-Grade Adaptive Structures

The United States stands at the forefront of the global Shape Memory Polymer Market, driven by strong momentum in biomedical device commercialization and next-generation aerospace systems. The clinical transition of SMP technology accelerated significantly with MedShape Inc.’s launch of a thermally activated orthopedic implant in early 2025, offering superior precision, durability, and minimally invasive deployment capabilities. This aligns with a broader movement within U.S. healthcare to integrate biocompatible SMPs into orthopedics, cardiovascular devices, and interventional tools. The FDA’s clearance of the IMPEDE-FX Embolization Plug, a landmark SMP-based aneurysm treatment solution, demonstrates a reliable regulatory pathway—an essential factor supporting SMP adoption in high-risk medical settings.

Beyond healthcare, the United States continues to dominate SMP innovation in aerospace, defense, and advanced manufacturing. NASA and the DoD are investing heavily in morphing wings, adaptive skins, and SMP-reinforced self-healing structures, leveraging the materials’ lightweight, fatigue-resistant, and stimuli-responsive characteristics. Leading companies such as Cornerstone Research Group are pushing the sustainability frontier with recyclable, carbon-fiber-reinforced SMP lines responsive to multiple stimuli, including photonic and thermal triggers. This positions the U.S. as a major hub for multifunctional, sustainable SMP solutions tailored for high-performance engineering sectors.

China: High-Volume Industrialization and Automotive Lightweighting with Thermo-Responsive SMPs

China represents one of the fastest-scaling SMP markets globally due to its immense manufacturing capacity and government-driven demand across automotive and industrial sectors. The country’s aggressive target of 35 million vehicle units by 2025 directly fuels the adoption of polyurethane-based SMPs for lightweight components—such as adaptive interior parts, morphing air vents, seating systems, and next-generation sealing/gasket applications. Chinese R&D teams are applying thermo-responsive SMPs to functional automotive components like automatic choke elements and airflow control systems, eliminating mechanical complexity while improving cost efficiency across mass-produced vehicle platforms.

Industrialization efforts are supported by rising investments from domestic leaders such as Guangzhou Manborui Materials Technology, which continue expanding capacity for both consumer and industrial SMP formulations. China’s rapid establishment of large-scale SMP supply chains allows it to support Asia-Pacific’s ballooning demand for self-healing materials, adaptive polymer systems, and energy-efficient product designs. Together, these factors establish China as a central force in SMP mass manufacturing and application diversification.

Germany/European Union: Sustainable SMP Formulations and High-Precision Integration into Advanced Robotics

Germany and the EU are steering the SMP market toward sustainability, recyclability, and advanced engineering integration. Under the EU’s Horizon Europe program, R&D initiatives prioritize bio-based, low-carbon, and recyclable SMP materials, cementing the region’s leadership in sustainable polymer science. These initiatives align with strict European ESG frameworks, accelerating adoption of eco-friendly SMPs in packaging, consumer goods, medical devices, and high-performance engineering applications.

Germany’s industrial automation and robotics sectors are rapidly integrating thermoset SMPs into adaptive grippers, robotic end-effectors, and programmable actuation systems. These materials provide soft, compliant gripping during handling, then transition to a locked, rigid state upon cooling—delivering higher precision and reduced mechanical complexity. With Covestro AG expanding production of advanced thermoplastic polyurethanes (TPUs)—a major SMP segment—Europe remains a powerhouse for high-performance, self-healing films and coatings, including automotive paint protection films (PPF). The combination of sustainable innovation and advanced automation positions Europe as a major epicenter for premium SMP technologies.

Japan: High-Precision SMP Composites and High-Temperature Actuation for Industrial Systems

Japan maintains a specialized leadership position in the Shape Memory Polymer Market, particularly in precision SMP composites, high-temperature actuation technologies, and advanced optical components. Regulatory approval by the Japanese Pharmaceuticals and Medical Devices Agency (PMDA) for products like Shape Memory Medical’s IMPEDE-FX plug underscores Japan’s strict quality expectations and the country’s adoption of SMPs in medical treatment systems.

In industrial manufacturing and high-temperature equipment, Japanese companies are engineering SMP composites designed for adaptive optical reflectors, precision fastening mechanisms, and high-temperature actuators. These solutions address critical needs in manufacturing automation, precision tooling, and next-generation semiconductor equipment. Japan’s ability to blend polymer chemistry, micro-engineering, and precision manufacturing continues to fuel its influence in niche, high-performance SMP markets.

South Korea: Thin-Film SMPs for Wearable Electronics, Flexible Displays, and Haptic Systems

South Korea is emerging as a global innovation hub for flexible SMP thin films, electro-responsive SMPs, and materials engineered for next-generation consumer electronics. R&D institutions are advancing body-heat-activated SMP structures for wearable medical devices and smart textiles, enabling personalized pressure distribution and enhanced physiological monitoring. These innovations support Korea’s broader push toward medical-grade wearables, home diagnostics, and continuous-monitoring technologies.

Korean display and electronics companies are integrating SMP thin-films into bendable displays, rollable screens, and haptic-feedback systems, leveraging SMPs for their tunable stiffness, self-healing capabilities, and actuation responsiveness. The convergence of SMP materials science with Korea’s leadership in displays and mobile devices is creating new opportunities across haptics, flexible touch interfaces, and multi-functional electronic skins.

United Kingdom: Defense-Driven Innovation in Graphene-Reinforced SMP Composites

The United Kingdom is developing a strong high-performance SMP ecosystem centered around academic–industrial partnerships and advanced composite engineering. UK researchers are pioneering graphene-reinforced SMP composites, delivering enhanced mechanical strength, thermal stability, and shape-recovery performance—attributes particularly attractive to defense OEMs and aerospace integrators. These materials contribute to lightweight, adaptive structures for protective armor, morphing aerospace components, and blast-resistant systems.

With leading universities collaborating closely with industrial partners, the UK is expanding its capability to transition SMP research into deployable defense technologies. This positions the UK as a strategic hub for high-strength, multifunctional SMP composites tailored for national security and high-reliability engineering applications.

Competitive Landscape: Global SMP Leaders Driving Smart Materials, Biocompatible Polymers & Aerospace-Grade Composites

The competitive environment in the Shape Memory Polymer industry is defined by companies specializing in polyurethane engineering, biocompatible polymers, aerospace-grade SMP composites, and customizable thermo-mechanical formulations. Leadership is determined by the ability to tailor glass transition temperatures, integrate SMPs into high-performance composites, and scale production for automotive, medical, and aerospace applications.

BASF SE develops high-performance polyurethane SMPs for automotive and construction applications

BASF SE is a major player in polyurethane-based SMPs, offering thermoplastic and acrylate SMP formulations and SMP foams engineered for adaptive components. The company is actively advancing SMP-based actuators for self-adjusting vehicle interiors and smart building envelopes designed to enhance energy efficiency through dynamic response capabilities. BASF’s global chemical production footprint enables it to deliver large-volume custom SMP masterbatches, positioning the company as a preferred supplier for high-scale industrial manufacturing and emerging additive manufacturing applications.

Covestro AG expands its leadership in biocompatible SMPs for long-term implants

Covestro’s SMP portfolio, built on Desmopan® TPU and waterborne urethane SMPs, is strongly aligned with the biomedical market. The company develops ISO 10993-certified SMP grades optimized for long-term implants and drug delivery systems, including vascular devices and orthopedic implants requiring precise Tg tuning near human body temperature. Covestro’s core advantage lies in its mastery of polyurethane chemistry, enabling highly controlled Tg ranges from 0°C to 100°C, and delivering SMPs that combine biocompatibility, durability, and rapid activation.

Evonik Industries AG drives biodegradable and aerospace-grade SMP innovation

Evonik’s SMP portfolio spans VESTAMELT® polyamide SMPs, Resomer® biodegradable SMPs (PCL/PLA), and advanced epoxy-based SMPs for aerospace applications. Its Resomer® line is central to the development of temporary orthopedic supports, degradable implants, and drug delivery components. Meanwhile, Evonik’s high-temperature polyamide and epoxy SMPs support aerospace morphing structures and structural actuation systems, benefiting from their superior mechanical strength, thermal stability, and controlled recovery behavior.

SMP Technologies Inc. pioneers tailored SMP formulations for electronics and actuators

SMP Technologies is one of the earliest specialized SMP providers, offering MM-Series polyurethane SMPs and custom epoxy-based thermoset SMPs. The company is heavily involved in consumer electronics, supplying materials for foldable devices, deformable haptic interfaces, and adaptive components requiring highly stable thermal activation cycles. SMP Technologies’ core strength is its ability to customize Tg and mechanical behavior to client specifications, enabling widespread adoption in specialized actuators and adaptive assemblies.

Composite Technology Development (CTD) advances aerospace-grade SMP composites for space and defense

CTD specializes in epoxy and thermoplastic SMPs engineered for extreme environments, including space missions and defense applications. Its flagship composites, such as CTD-420, meet the stringent requirements of NASA and DoD programs for deployable space structures, morphing aerodynamics, and high-precision actuation mechanisms. CTD’s materials exhibit high stiffness, strength, and glass transition temperatures exceeding 120°C, making them ideal for structural SMP applications subjected to repeated thermal cycling and mechanical loading.

Shape Memory Polymer Market Report Scope

Shape Memory Polymer Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.3 Billion

|

|

Market Size (2035)

|

$10.5 Billion

|

|

Market Growth Rate

|

23.2%

|

|

Segments

|

By Material Type (Polyurethane, Epoxy SMPs, Polylactide, Polyvinyl Chloride, Others), By Activation/Stimulus Type (Temperature-Activated, Light-Activated, Electrically-Activated, Magnetically-Activated, Other Stimuli), By End-Use Industry (Medical & Healthcare, Aerospace & Defense, Automotive, Consumer Electronics, Textiles & Smart Apparel, Construction & Infrastructure)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Covestro, Lubrizol, Evonik, DuPont, Asahi Kasei, MedShape, Shape Memory Medical, Composite Technology Development (CTD), Cornerstone Research Group (CRG), SMP Technologies, Nanoshel, Spintech, Guangzhou Manborui Materials Technology, Huntsman, NatureWorks

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Shape Memory Polymer (SMP) Market Segmentation

By Material Type

- Polyurethane (PU)

- Epoxy SMPs

- Polylactide (PLA)

- Polyvinyl Chloride (PVC)

- Others

By Activation / Stimulus Type

- Temperature-Activated SMPs

- Light-Activated SMPs

- Electrically-Activated SMPs

- Magnetically-Activated SMPs

- Other Stimuli

By End-Use Industry

- Medical & Healthcare

- Aerospace & Defense

- Automotive

- Consumer Electronics

- Textiles & Smart Apparel

- Construction & Infrastructure

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Shape Memory Polymer Market

- Covestro

- Lubrizol

- Evonik

- DuPont

- Asahi Kasei

- MedShape

- Shape Memory Medical

- Composite Technology Development (CTD)

- Cornerstone Research Group (CRG)

- SMP Technologies

- Nanoshel

- Spintech

- Guangzhou Manborui Materials Technology

- Huntsman

- NatureWorks.

*- List not Exhaustive

Research Coverage

The latest Shape Memory Polymer Market study from USDAnalytics provides a deep technical and strategic view of how rapidly activating SMPs are moving from lab-scale curiosities to mission-critical materials in medical, aerospace, automotive, electronics, and smart textile systems. Drawing on quantitative and qualitative evidence, this report investigates how SMP chemistry, composite design, and processing innovation are converging to unlock 800%+ strain recovery, body-temperature actuation, 4D printing, and multi-stimuli responsiveness at commercial scale. It tracks regulatory approvals, aerospace qualification programs, and sustainability-driven material substitution as key breakthroughs that are redefining competitive positioning across the value chain. Through rigorous analysis reviews of clinical case studies, defense programs, and industrial pilot lines, the report highlights how polyurethane, PLA, epoxy and advanced composite SMP platforms are being tuned for Tg, fatigue life, recovery stress, and recyclability to meet demanding OEM specifications. By linking technical performance metrics with market adoption curves, supply-chain risks, and capex plans, this report is an essential resource for material scientists, device engineers, procurement leaders, strategy teams, and investors evaluating the next decade of smart material innovation in SMPs, covering technology roadmaps, partnership models, commercialization bottlenecks, risk factors, etc……

Scope Highlights

- Segmentation

- By Material Type: Polyurethane (PU), Epoxy SMPs, Polylactide (PLA), Polyvinyl Chloride (PVC), Others

- By Activation / Stimulus Type: Temperature-Activated SMPs, Light-Activated SMPs, Electrically-Activated SMPs, Magnetically-Activated SMPs, Other Stimuli

- By End-Use Industry: Medical & Healthcare, Aerospace & Defense, Automotive, Consumer Electronics, Textiles & Smart Apparel, Construction & Infrastructure

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe Coverage: Historic data from 2021 to 2025 and robust forecast projections from 2026 to 2034.

- Companies Covered: Analysis / profiles of 15+ key companies across the global Shape Memory Polymer ecosystem.