Silanes Market Valuation 2025–2034: $6.2 Billion to $11.3 Billion at 6.9% CAGR Powered by Semiconductor Purity, EV Batteries, and Low-VOC Formulations

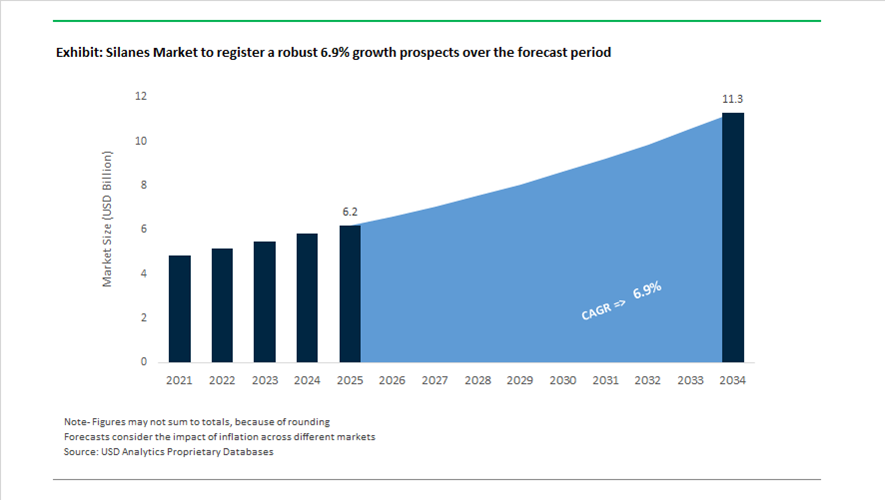

The global silanes market is valued at $6.2 billion in 2025 and is forecast to reach $11.3 billion by 2034, expanding at a CAGR of 6.9%. Growth is being shaped by accelerating demand for high-purity silanes in semiconductor fabrication, silicon-anode battery technologies, advanced adhesives and sealants, green construction materials, and automotive lightweighting. Silanes serve as essential precursors and functional additives in silicon-based chemistries, enabling surface modification, adhesion promotion, moisture resistance, and dielectric performance. Increasing localization of electronics manufacturing, rapid EV adoption, and tightening global low-VOC and PFAS-related regulations are structurally elevating the strategic value of specialty silanes and monosilane gas across industrial supply chains.

In May 2024, KCC Corporation finalized its acquisition of Momentive Performance Materials, consolidating high-end specialty silane technologies under a broader silicone and advanced materials portfolio. This transaction strengthened KCC’s positioning in automotive electronics, semiconductor encapsulation materials, and performance construction sealants. In 2024, Shin-Etsu Chemical announced the construction of a 2.1 billion yen silicone and silane plant in Zhejiang Province, China, scheduled for completion in February 2026. The facility is designed to supply functional silanes and environmentally optimized silicone materials to China’s electronics and electric mobility sectors. In parallel, Sicona Battery Technologies secured $22 million in funding in 2024 to accelerate commercialization of silicon-carbon anode materials that utilize silane gas as a precursor, reinforcing the linkage between silane demand and next-generation EV battery chemistry.

During 2025, portfolio restructuring and regulatory adaptation gained momentum. In late 2025, DuPont completed the spinoff of its electronics business into Qnity Electronics, transferring high-purity silane and silicon-based semiconductor materials into a focused growth platform. Throughout 2025, manufacturers such as Zhejiang Jinhua New Material advanced oximino silane formulations designed to comply with stringent low-VOC standards in North America, delivering 18–22% improvement in bonding efficiency between organic polymers and inorganic substrates. Kao Collins introduced PFAS-free security ink technologies during 2024–2025 using silane-based adhesion promoters, aligning with tightening EU and U.S. restrictions on persistent fluorinated compounds in coatings and packaging systems. These developments underscore how environmental compliance and performance optimization are reshaping product development strategies across the silanes value chain.

In early 2026, Evonik confirmed progress under its “Evonik Tailor Made” efficiency program, restructuring its silanes and silica divisions to better serve high-growth sectors such as green energy and electric vehicles. The company also announced expanded global production of hydroxyl-terminated polybutadiene, a material frequently used alongside silane coupling agents in high-performance adhesives, including a new Shanghai facility established in 2025 and a Germany expansion scheduled for 2027. REC Silicon reported in February 2026 that while polysilicon production at its Butte facility was halted in mid-2024, monosilane gas production continues, pivoting toward silicon-anode battery supply chains. Wacker Chemie, addressing energy cost pressures and utilization challenges in 2025, provisioned €100 million for its PACE optimization project in early 2026 to enhance cost efficiency across European silicones and silanes operations.

Regulation-Led Demand Shifts and High-Conviction Opportunities in the Global Silanes Market

Regulatory Mandates Institutionalizing Silane-Based Infrastructure Protection

Public infrastructure authorities are formally embedding silane chemistry into construction and maintenance standards as the economic cost of concrete deterioration escalates. What was once an optional surface treatment is now becoming a mandatory specification across bridge decks, highways, and marine-adjacent assets, structurally lifting baseline demand for penetrating silane sealers. In the United States, state Departments of Transportation are codifying minimum performance thresholds that only high-purity silane and siloxane systems can meet. As of late 2025, procurement frameworks such as PennDOT Bulletin 15 issued by the Pennsylvania Department of Transportation require one-component penetrating sealers with at least 40% silane or siloxane content. These materials must demonstrate a minimum 85% reduction in chloride ion penetration under AASHTO T 259 testing, effectively excluding lower-cost acrylic or epoxy alternatives from compliance-driven projects.

From an asset economics perspective, 2025 industry performance assessments show that although high-quality silane sealers command average bid prices near $140 per gallon, they deliver validated service lives of five to ten years. On new bridge decks, silane application is now recognized as a best-practice preventive measure for crack widths below 0.002 inches, materially reducing moisture ingress and corrosion risk. This regulatory normalization is transforming silanes into a recurring, specification-locked consumable within multi-billion dollar transportation maintenance budgets.

High-Purity Organosilanes as Enablers of Advanced Functional Glass

Parallel to infrastructure, demand momentum in the silanes market is being reinforced by the global glass industry’s shift toward high-performance architectural and automotive glazing. Organofunctional silanes are emerging as critical precursors in coatings that deliver electrochromic behavior, self-cleaning functionality, and long-term durability under increasingly stringent building energy codes. In September 2025, NSG Group announced a major capital investment to establish an advanced glass coating line in Poland, designed to serve next-generation architectural and automotive applications across Europe. These coating systems rely on silane-based chemistries to achieve adhesion stability and functional longevity under thermal and UV stress.

Strategically, Saint-Gobain has reinforced this trend through its 2025 strategic roadmap, highlighting that roughly three quarters of group sales now originate from differentiated and innovative systems. Acquisitions of construction chemical specialists such as Cemix and Fosroc have allowed Saint-Gobain to internalize silane-modified technologies, accelerating deployment in high-growth markets including India and Mexico. This vertical integration underscores how silanes are shifting from commodity intermediates to value-defining components in advanced building material ecosystems.

Compatibilizing Silanes for High-Performance Recycled Plastics

European circular economy policy is opening a structurally significant growth avenue for compatibilizing silanes as manufacturers struggle to reconcile recycled content mandates with performance requirements. The EU Packaging and Packaging Waste Regulation, effective February 11, 2025, mandates 30% recycled plastic content in packaging by 2030, creating a technical gap as most post-consumer recyclates lack the mechanical consistency of virgin polymers. Silane coupling agents are increasingly deployed to improve interfacial adhesion between degraded recycled polymers and inorganic fillers, effectively upgrading low-grade recyclate for higher-value applications.

Regulatory momentum is set to intensify as the European Commission finalizes delegated acts on design-for-recycling criteria, expected in 2026 and 2027. These standards are likely to favor VOC-free, high-efficiency compatibilizers that improve recyclate performance without compromising emissions targets. For silane producers, this represents a scalable opportunity driven less by price sensitivity and more by compliance necessity, where supply shortages of quality recyclate remain the primary bottleneck to regulatory adherence.

Silane-Enhanced Encapsulants Enabling Commercial-Scale Perovskite Solar

The commercialization trajectory of perovskite solar cells is increasingly dependent on silane chemistry to overcome durability and stability limitations associated with moisture and thermal stress. With laboratory efficiencies reaching 34.85% in April 2025, attention has shifted from performance gains to operational longevity, where silane-based cross-linkers play a central role in protecting perovskite grain boundaries. In February 2025, the Government of Japan committed $1.5 billion to accelerate flexible perovskite solar development, explicitly prioritizing silane-enhanced encapsulation systems that function as airtight barriers against water ingress and photothermal degradation.

This chemistry is also enabling the integration of perovskite photovoltaics into building materials. By late 2025, smart glass applications accounted for more than 36% of perovskite-related revenues, reflecting strong demand for building-integrated solutions that combine energy generation with architectural function. Silane-doped encapsulant films are emerging as a critical enabler of 20-year-plus operational lifespans, positioning silanes at the core of next-generation building-integrated photovoltaics and advanced energy-efficient construction systems.

Silanes Market Share and Segmentation Insights

Functional Silanes Lead the Silanes Market Driven by Tire Reinforcement and Polymer Coupling Technologies

Functional silanes accounted for 52.80% of the silanes market in 2025, making them the dominant product category across advanced materials and polymer modification applications. Functional silanes including amino, epoxy, vinyl, methacryloxy, and sulfur silanes serve as critical coupling agents that enable strong interfacial bonding between organic polymers and inorganic substrates such as glass fibers, silica, and mineral fillers. This functionality is essential for improving the performance of rubber compounds, reinforced plastics, adhesives, and protective coatings. A major 2025 demand driver is the continued growth of silica-reinforced tire technologies, where sulfur-functional silanes enable polymer–silica bonding required for low rolling resistance tires that enhance fuel efficiency, wet traction, and durability.

Rubber & Plastics Applications Drive Global Silane Consumption Through Lightweight Composite Materials

Rubber and plastics represent the largest application segment in the silanes market, accounting for 38.60% of total demand in 2025 due to the extensive use of silane coupling agents in reinforced rubber and composite plastic systems. In rubber compounding, silanes improve filler dispersion, polymer compatibility, and mechanical strength, particularly in tire manufacturing. In plastics, silanes enable stronger bonding between glass fibers or mineral fillers and polymer matrices, supporting the development of high-performance composite materials. A key 2025 industry trend is the increasing focus on lightweight materials in automotive and transportation sectors, where silane-treated fillers enable durable glass fiber reinforced plastics and mineral-filled composites that replace heavier metal components while maintaining structural strength and long-term durability.

Silanes Market Competitive Landscape

The 2026 silanes market is defined by ultra-high purity requirements for semiconductor manufacturing and sustainable organofunctional silanes for EV and construction applications. Leading players are advancing PFAS-free coatings, AI-driven materials discovery, and localized production hubs to mitigate trichlorosilane volatility and enable next-generation performance materials.

Evonik strengthens PFAS-free silane coatings and specialty portfolio through SYNEQT restructuring

Evonik Industries AG continues to lead the silanes market through its Protectosil® and Dynasylan® portfolios, targeting sustainable functionalization and high-performance additives. The company reported 2025 adjusted EBITDA of €1.87 billion and maintains a 2026 outlook of €1.7–€2.0 billion, supported by its Advanced Technologies segment. The spin-off of SYNEQT in early 2026 enables sharper capital allocation toward specialty silanes and high-margin applications. Evonik introduced PFAS-free silane coatings for construction and packaging, addressing stringent EU environmental mandates. Its Smart Effects business synchronizes upstream chlorosilane production with customized coupling agents for tire and adhesive markets. This integrated model ensures supply chain resilience and strengthens its position in green mobility and infrastructure.

Shin-Etsu expands global silane capacity with $1.2 billion investment and semiconductor integration strategy

Shin-Etsu Chemical is scaling its leadership in semiconductor-grade silanes through a cumulative investment exceeding $1.2 billion across Japan, Thailand, Hungary, and the United States. The company strengthened vertical integration by acquiring full ownership of Mimasu Semiconductor Industry, linking silane gas production with wafer manufacturing. Expansion at the Gunma Complex and global facilities supports rising demand for eco-friendly silanes in EV batteries and electronics. Its Electronics Materials segment continues to generate strong cash flows, enabling a 40% dividend payout target for 2026. Shin-Etsu’s focus on ultra-high purity monosilanes supports sub-3nm chip fabrication and advanced node technologies. This positions the company as a cornerstone supplier in AI and semiconductor ecosystems.

Dow accelerates AI-driven silane innovation for EV mobility and circular polymer systems

Dow Inc. is executing its Transform to Outperform strategy, targeting $2 billion in EBITDA uplift through AI-enabled process optimization and automation. The company is advancing silane-modified materials under its MobilityScience™ platform, enhancing durability and lightweighting in EV battery enclosures and automotive components. Its REVOLOOP™ recycled polymers incorporate silane additives to enable high-performance PCR applications in cables and infrastructure. Dow reported approximately $40 billion in 2025 sales, with sustainability-driven projects expected to generate $1 billion in NPV by 2026. Strategic investments of $800 million to $1,000 million in 2026 are focused on streamlining operations and expanding specialty materials. This positions Dow at the intersection of circular economy and advanced mobility.

Wacker drives semiconductor-grade silane growth with PACE efficiency program and GENIOSIL® leadership

Wacker Chemie AG is prioritizing hyperpure silane production for semiconductor and advanced polymer applications under its PACE efficiency program, targeting over €300 million in annual savings by 2026. The company forecasts EBITDA between €550 million and €700 million in 2026, supported by growth in Silicones and Polymers divisions. Its GENIOSIL® STP-E technology remains a benchmark for silane-terminated adhesives, enabling isocyanate-free, high-performance bonding solutions. Wacker is reallocating resources from solar-grade polysilicon to electronic-grade silanes to capture higher-margin opportunities. Despite a 2025 impairment-driven loss, its 45% equity ratio ensures strong financial stability. This strategic pivot reinforces its leadership in construction chemicals and semiconductor materials.

Momentive advances green tire silane systems and PFAS-free coatings for EV and aerospace applications

Momentive Performance Materials is accelerating adoption of sulfur-functional silanes aligned with Euro 7 regulations, enabling up to 12% reduction in rolling resistance for EV tires. Its NXT™ silane portfolio enhances manufacturing efficiency by reducing ethanol emissions and simplifying processing steps. The Silquest™ product line dominates silane-modified polymer binders, holding approximately 40% share in the polyether-based SMP segment. Momentive is expanding PFAS-free coating technologies for flame-retardant silicone elastomers in EV battery systems. The company showcased advanced silane solutions at K 2025, reinforcing its innovation pipeline. Its global footprint supports aerospace, automotive, and infrastructure markets with high-performance interface solutions.

China: Integrated Scale, Semiconductor Purity, and Policy-Driven Consolidation

China remains the structural center of gravity for the global silanes industry, underpinned by deep upstream integration from silicon metal to chlorosilanes and downstream organofunctional silanes. This integration is reinforced by national mandates around solar deployment, semiconductor self-sufficiency, and green mobility. In December 2025, Wacker Chemie AG and SICO Performance Material inaugurated a 2,300-square-meter application development center in Jining, strengthening local formulation capabilities for high-performance silanes used in coatings and adhesives. Parallel to this, domestic producers such as Zhejiang Sailin Silicon have scaled 6N ultra-high-purity silane gas output to support the rapid build-out of 12-inch wafer fabrication lines.

End-use demand in China is increasingly standards-driven. Tire manufacturers are accelerating the transition from carbon black to silica–silane systems to comply with Green Tire requirements targeting materially lower rolling resistance. In electronics, joint venture activity has intensified, highlighted by Shin‑Etsu Chemical establishing Shin-Etsu Silicone (Pinghu) to localize high-performance silane and silicone intermediates. At the regulatory level, 2025 enforcement actions by the Ministry of Ecology and Environment have forced consolidation across the chlorosilane sector, structurally favoring players with closed-loop waste recovery and by-product recycling capabilities.

Japan: High-Purity Specialization and Battery-Led Demand

Japan’s silanes industry is defined by precision manufacturing and a concentration on ultra-high-purity applications. In January 2025, Wacker Chemie AG commenced operations at its new Tsukuba specialty silane and silicone facility, designed to serve advanced automotive sensors and industrial electronics. A major demand vector is next-generation energy storage. Silane gas is increasingly specified for silicon–carbon composite anodes, which now represent a substantial share of specialized silane gas consumption in Japan due to their higher energy density requirements.

Japanese producers continue to anchor global supply chains. Shin‑Etsu Chemical remains the benchmark supplier of high-end functional silanes and expanded its 2025 mercapto-silane portfolio for high-durability EV tires. Export infrastructure is equally strategic, with Japan maintaining leadership in ultra-pure monosilane shipments to Taiwanese and South Korean foundries using dedicated cryogenic ISO-tank logistics. Government backing under the Critical Mineral and Material Security framework has further designated silane precursors as strategic inputs, unlocking R&D incentives for tin-free curing and low-emission silane chemistries.

South Korea: Memory-Centric Growth and Vertical Integration

South Korea’s silanes market is tightly coupled with its dominance in memory and advanced packaging. In early 2025, Wacker Chemie AG opened a specialty silane plant in Jincheon to directly serve High Bandwidth Memory packaging demand, where deposition consistency and impurity control are critical. Structural consolidation has reshaped the competitive landscape following KCC Corporation completing the full integration of Momentive Performance Materials, creating a vertically integrated supplier across functional silanes and silicones.

Technology requirements are tightening further with node migration. SK Materials expanded silane gas purification capacity in 2025 to support 3 nm gate-all-around transistor architectures, which demand higher deposition frequencies and narrower impurity tolerances. Outside semiconductors, South Korean solar manufacturers are pivoting toward TOPCon and HJT cell architectures, both of which rely more heavily on silane-based thin-film deposition than legacy P-type technologies, reinforcing cross-sector demand stability.

United States: Reshoring, Infrastructure Pull, and Clean-Energy Exposure

The U.S. silanes industry is undergoing strategic reshoring as suppliers respond to trade policy changes and federal investment cycles. Following 2025 tariff updates, domestic optimization of Gulf Coast assets by Dow and Momentive Performance Materials has reduced exposure to imported intermediates and improved supply resilience for specialty silanes. Public infrastructure spending is a major downstream driver, with IIJA-funded bridge and highway programs lifting demand for silane-based water repellents and anti-corrosive concrete treatments.

Clean-energy deployment is adding a second growth axis. Expansion in onshore wind and energy storage has increased consumption of silane-treated fiberglass and composites used in turbine blades. In parallel, CHIPS Act incentives are encouraging chemical suppliers to install on-site ultra-high-purity silane delivery systems at new mega-fabs in Arizona and Ohio, embedding silane suppliers directly into fab operating models rather than treating them as off-site commodity inputs.

Germany: Regulatory Leadership and Performance-Driven Reformulation

Germany plays a disproportionate role in shaping the technical and regulatory trajectory of the silanes industry in Europe. In 2025, Evonik Industries expanded its Next Generation silane research platform with a focus on sulfur-based silanes that eliminate ethanol emissions during tire compounding, directly addressing both occupational exposure and environmental scrutiny. On the manufacturing side, Wacker Chemie AG advanced European supply through its Karlovy Vary facility, emphasizing room-temperature-curing silane-modified polymers for construction and refurbishment markets.

Germany also remains the principal driver of EU regulatory alignment. Its leadership in shaping the 2025 REACH updates has accelerated the shift toward labeling-free and low-hazard silane adhesion promoters across the Eurozone. This has structurally favored innovation-led suppliers capable of reformulating without performance loss, particularly in construction sealants, industrial coatings, and mobility-linked applications.

Strategic Comparison: Silanes Industry by Country

Silanes Market County Level Snapshot

|

Country

|

Core Demand Driver

|

Technical Focus

|

|

China

|

Solar, semiconductors, green tires

|

UHP silane gas, water-borne and integrated systems

|

|

Japan

|

Batteries and precision electronics

|

Ultra-pure and specialty functional silanes

|

|

South Korea

|

Memory and advanced packaging

|

High-purity deposition silanes

|

|

United States

|

Infrastructure and clean energy

|

Reshored specialty silanes, UHP delivery systems

|

|

Germany

|

Regulation and performance reformulation

|

Low-emission, labeling-free silanes

|

Silanes Market Report Scope

Silanes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.2 Billion

|

|

Market Size (2034)

|

$11.3 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Product Type (Functional Silanes, Mono and Chloro Silanes, Specialty Silanes), By Purity Level (Industrial Grade, High Purity Grade, Ultra-High Purity Grade), By Application (Rubber & Plastics, Paints & Coatings, Adhesives & Sealants, Electronics & Semiconductors, Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Evonik Industries AG, Shin-Etsu Chemical Co. Ltd., Wacker Chemie AG, Dow Inc., Momentive Performance Materials Inc., Hubei Jianghan New Materials Co. Ltd., REC Silicon ASA, Air Liquide SA, Linde plc, SK Materials Co. Ltd., Gelest Inc., Jiangxi Chenguang New Materials Co. Ltd., Zhejiang Xinan Chemical Industrial Group, Mitsui Chemicals Inc., Hubei BlueSky New Material Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silanes Market Segmentation

By Product Type

Sulfur Silanes

Amino Silanes

Vinyl Silanes

Epoxy Silanes

Alkyl Silanes

Methacryloxy Silanes

- Mono and Chloro Silanes

- Specialty Silanes

By Purity Level

- Industrial Grade

- High Purity Grade

- Ultra-High Purity Grade

By Application

- Rubber & Plastics

- Paints & Coatings

- Adhesives & Sealants

- Electronics & Semiconductors

- Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silanes Industry

- Evonik Industries AG

- Shin-Etsu Chemical Co. Ltd.

- Wacker Chemie AG

- Dow Inc.

- Momentive Performance Materials Inc.

- Hubei Jianghan New Materials Co. Ltd.

- REC Silicon ASA

- Air Liquide SA

- Linde plc

- SK Materials Co. Ltd.

- Gelest Inc.

- Jiangxi Chenguang New Materials Co. Ltd.

- Zhejiang Xinan Chemical Industrial Group

- Mitsui Chemicals Inc.

- Hubei BlueSky New Material Inc.

*- List not Exhaustive