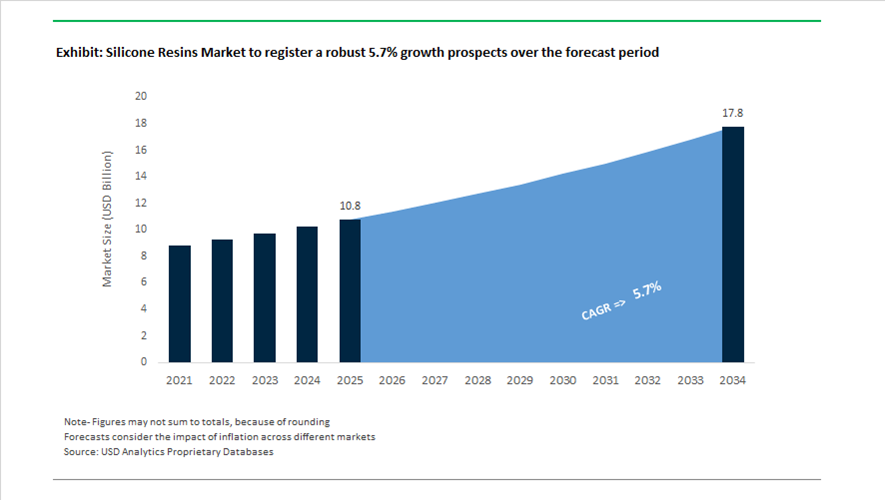

Silicone Resins Market Valuation 2025–2034: $10.8 Billion to $17.8 Billion at 5.7% CAGR Supported by High-Temperature Coatings and Medical-Grade Innovation

The global silicone resins market is valued at $10.8 billion in 2025 and is projected to reach $17.8 billion by 2034, expanding at a CAGR of 5.7%. Market growth is driven by increasing demand for high-temperature resistant coatings, weatherable construction materials, automotive electronics encapsulation, industrial protective coatings, medical-grade silicone components, and specialty 3D printing resins. Silicone resins provide exceptional thermal stability, UV resistance, dielectric strength, moisture repellency, and long-term durability, making them indispensable in infrastructure protection, renewable energy systems, and advanced electronics packaging. The shift toward low-VOC formulations, water-based silicone technologies, and medical-compliant materials is reshaping product development strategies across major producers.

In March 2024, Shin-Etsu Chemical introduced the KRW-6000 Series, recognized as the industry’s first emulsifier-free, water-based fast-curing silicone resin. The formulation is fully VOC-free and delivers hardness levels up to 4H, addressing environmental regulations in industrial coatings while lowering greenhouse gas emissions during curing. In April 2024, KCC Corporation completed the full acquisition of Momentive Performance Materials, consolidating advanced silicone resin technologies for automotive and electronics applications. In August 2024, Trelleborg AB acquired the Baron Group, expanding its liquid silicone rubber and specialized resin component capabilities across the Asia-Pacific medical sector. During 2024–2025, Wacker Chemie reported €266.3 million in capital expenditure within its Silicones division, including new production lines at Zhangjiagang, China for functional resins and elastomer gels.

Strategic alliances and product innovation accelerated through 2025. In March 2025, Momentive and Hungpai formed a joint venture to expand silane and resin precursor production capacity in Asia, targeting high-performance materials for green tire manufacturing and electronics applications. In April 2025, Dow implemented a global 5%–10% price increase across its silicone portfolio, including resins, as part of a broader strategic reshaping toward higher-margin medical and semiconductor-grade products. In July 2025, Stratasys launched P3™ Silicone 25A, developed in collaboration with Shin-Etsu, engineered for the Origin® DLP platform to produce specialized industrial and medical-grade silicone resin parts. In November 2025, Dow introduced DOWSIL™ FC-5012 ID Resin Gum at in-cosmetics Asia, delivering breathable, flexible film-forming properties for premium cosmetic applications with enhanced water and sebum resistance.

Cost pressures and structural portfolio shifts defined early 2026. In February 2026, Wacker announced price increases of up to 25% across its silicone resins portfolio, citing the doubling of platinum catalyst prices essential for addition-curing resin systems. The same month, Elkem ASA signed a definitive agreement to divest the majority of its global Silicones division to Bluestar through a cash-free transaction involving the redemption of Bluestar’s 52.9% stake, repositioning Elkem as a metals-focused materials company. These developments underscore how catalyst cost volatility, medical and electronics-grade material demand, regional precursor capacity expansion, and sustainability-driven resin innovation are shaping competitive dynamics in the silicone resins market through 2034.

Key Trends and High-Value Opportunities in the Global Silicone Resins Market

Utility-Scale Grid Hardening Accelerating Adoption of Silicone Resin Coatings

The silicone resins market is being structurally reshaped by unprecedented global investment in power grid modernization and climate resilience. Utilities are increasingly specifying silicone resin based high-temperature coatings for transformers, insulators, and overhead distribution hardware as wildfire risk, heat stress, and extreme weather events intensify. Unlike organic coatings, silicone resins maintain dielectric integrity, hydrophobicity, and adhesion under sustained thermal and UV exposure, making them a preferred material for grid hardening programs.

According to the Grid Investment Outlook 2025 published by BloombergNEF, global grid capital expenditure is expected to surpass $470 billion in 2025, representing a 16% year-on-year increase. In the United States alone, nearly $115 billion is being allocated to transmission and distribution upgrades, with a strong emphasis on network hardening. Programs such as the Grid Resilience and Innovation Partnerships initiative led by the U.S. Department of Energy are channeling $3.46 billion into projects that deploy fire-resistant poles and silicone-coated electrical components. Major utilities including Pacific Gas and Electric and Xcel Energy have collectively committed more than $25 billion through 2025 toward wildfire mitigation, prioritizing silicone resin coatings that suppress thermal tracking and prevent catastrophic equipment failure in high-risk corridors.

Automotive Qualification of Silicone Resins for Advanced LED Optics

A second structural demand driver is emerging from automotive lighting systems, where the shift toward Matrix LED and Adaptive Driving Beam technology is displacing traditional thermoplastics. Silicone resins are now being formally qualified as the primary material for injection-molded primary optics due to their superior thermal stability, optical clarity, and resistance to yellowing. These properties are essential as LED headlamp modules generate higher localized heat while requiring precise light control for safety compliance.

By early 2025, safety frameworks implemented by the National Highway Traffic Safety Administration and the European Commission had normalized Adaptive Driving Beam systems across premium vehicle platforms. This regulatory alignment has accelerated adoption of optical-grade silicone resins capable of producing complex free-form lenses that are roughly 30% lighter than glass alternatives. Modern LED headlamp assemblies can emit up to 10,000 lumens per set, requiring materials that remain stable at operating temperatures approaching 200 degrees Celsius. OEMs such as Audi and BMW are integrating methyl-phenyl silicone resins to ensure optical performance and durability over service lifetimes exceeding 50,000 hours.

Silicone Resin Binders Enabling Fire-Safe Building Facades

The tightening of global fire safety regulations is opening a high-conviction growth opportunity for silicone resins as inorganic binders in non-combustible facade systems. Building codes such as NFPA 285 in the United States and Euroclass A1 and A2 standards in Europe are driving a rapid shift away from organic adhesives toward silicone-based systems that retain mechanical strength and water repellency without contributing to fire load.

Industry assessments from late 2025 indicate that consumption of silicone-based fire-resistant binders and adhesives has increased by more than 42% in high-temperature construction applications. This growth is closely linked to rising use of mineral wool and non-combustible facade panels, where silicone resins provide critical cohesion and durability. Nearly half of global fire-resistant adhesive demand is now concentrated in construction and infrastructure, prompting manufacturers to accelerate development of VOC-free silicone resin formulations. These materials are increasingly mandated in smart city and public works projects across the Asia Pacific and Middle East regions, where facade systems must withstand temperatures exceeding 1,200 degrees Celsius during fire exposure while maintaining structural integrity.

High-Refractive-Index Silicone Resins for AR, VR, and Advanced Optoelectronics

A second high-value opportunity is emerging at the intersection of silicone chemistry and next-generation optics. The commercialization of lightweight augmented reality glasses and virtual reality headsets has exposed a critical shortage of high-refractive-index materials that combine optical clarity with low density and processability. Phenyl-modified silicone resins are gaining attention as a solution, offering refractive indices above 1.6 while enabling precision molding at wafer scale.

In early 2024, leading optical manufacturers identified high-index waveguides as the primary bottleneck to immersive AR device adoption, creating a clear pathway for silicone resin innovation. Strategic industry analyses in 2025 project that emerging applications such as AR eyewear and neuro-optical sensing platforms will consume an additional 2,000 tons of high-refractive-index resins by 2026. These applications increasingly rely on UV-curable silicone resins used in nanoimprint lithography, where silicone’s inherent release properties deliver superior yield compared with epoxy-based systems. For resin formulators, this represents a premium niche characterized by high qualification barriers, strong intellectual property protection, and long-term supply agreements with optoelectronics manufacturers.

Silicone Resins Market Share and Segmentation Insights

Methyl Silicone Resins Lead the Silicone Resins Market for Heat-Resistant Industrial Coatings

Methyl silicone resins accounted for 42.80% of the silicone resins market in 2025, reflecting their strong performance in high-temperature and weather-resistant coating applications. These resins deliver excellent thermal stability up to approximately 250°C, strong UV resistance, and durable film formation, making them widely used in industrial coatings, protective coatings, and high-temperature binder systems. Their balance of performance and cost efficiency supports broad adoption across coatings formulations. A key 2025 demand driver is the increasing requirement for heat-resistant industrial coatings used on chimneys, exhaust systems, boilers, and industrial process equipment, where coatings must maintain structural integrity and corrosion protection under repeated thermal cycling and harsh operating environments.

Paints & Coatings Industry Drives Silicone Resin Consumption for Durable Protective Coatings

Paints and coatings represent the largest end-use industry in the silicone resins market, accounting for 42.80% of total demand in 2025 due to the critical role silicone resins play in high-performance protective coatings. Silicone resin-based coatings deliver heat resistance, long-term weather durability, corrosion protection, and UV stability, making them suitable for architectural coatings, marine coatings, and industrial maintenance coatings. The large scale of global coatings production continues to support strong silicone resin consumption. A key 2025 industry trend is the growing specification of durable infrastructure coatings, particularly for bridges, industrial plants, and marine structures, where silicone resin technologies help extend coating lifespan and reduce maintenance frequency while improving overall lifecycle cost efficiency.

Silicone Resins Market Competitive Landscape

The 2026 silicone resins market is shaped by demand for high-heat-resistant binders, VOC-compliant coatings, and carbon-neutral silicone chemistries. Leading players are balancing cost optimization with innovation in MQ resins, hybrid silanes, and sustainable production to address EV, aerospace, and semiconductor-driven growth.

Wacker accelerates bio-based silicone resin innovation and pricing strategy under Project PACE

Wacker Chemie AG is strengthening its silicone resins portfolio through its Project PACE efficiency program, targeting €550 million to €700 million EBITDA in 2026. The company implemented price increases up to 25% to offset rising platinum catalyst and silicon input costs. Its China Technology Center enables customized silicone resins for 5G infrastructure and EV battery applications. Wacker is advancing mass-balance certified silicone resins by replacing fossil coal with biogenic carbon, supporting Scope 3 emission reduction goals. With 2025 sales at €5.49 billion, the company is pivoting toward high-growth semiconductor and specialty coatings segments. This positions Wacker as a leader in sustainable, high-performance silicone resin solutions.

Shin-Etsu scales high-purity silicone resins with $1.2 billion global expansion and vertical integration

Shin-Etsu Chemical is investing over $1.2 billion to expand advanced silicone resin production across Japan, Thailand, and the U.S. Its Sustainable Silicone Business Development Department drives commercialization of carbon-neutral and eco-friendly resin systems. The company’s vertical integration ensures control from silicon metal to high-refractive-index resins used in LED packaging and optical electronics. Forecasted revenue of ¥2.4 trillion highlights strong growth in its Functional Materials segment. Shin-Etsu’s resins are critical for power electronics, EV components, and high-performance coatings. This integrated approach secures its dominance in ultra-high-purity silicone resin markets.

Dow drives PFAS-free silicone resin adoption and decarbonized production through Decarbia platform

Dow Inc. is advancing silicone resin innovation through its Transform to Outperform initiative, targeting $2 billion EBITDA improvement. The Decarbia™ platform introduces low-carbon silicone resins supported by Environmental Product Declarations and verified carbon neutrality pathways. Dow’s DOWSIL™ 5-1050 polymer processing aid replaces fluoropolymer-based additives, aligning with global PFAS restrictions. With approximately $43 billion in annual sales, the company leverages global integration to deliver food-contact-compliant and high-performance resin systems. AI-driven automation is optimizing production efficiency across its specialty materials network. This positions Dow as a leader in sustainable, regulatory-compliant silicone resins.

Evonik advances PFAS-free silicone-hybrid resins for coatings and building protection applications

Evonik Industries is focusing on high-margin silicone-hybrid resins within its Advanced Technologies segment, targeting €1.7 billion to €2.0 billion EBITDA in 2026. The SYNEQT spin-off enables sharper focus on specialty resin innovation and operational efficiency. Its Protectosil ECO-TRETE® anti-graffiti coating sets a benchmark for PFAS-free, environmentally compliant silicone resin systems. Evonik’s VISIOMER® methacrylates play a key role in hybrid resin synthesis for industrial coatings and adhesives. Expanded distribution partnerships enhance market penetration in North America. This strategy reinforces Evonik’s leadership in sustainable, high-performance silicone resin chemistries.

Elkem pioneers MQ resin technology and circular silicone resin systems amid strategic portfolio realignment

Elkem Silicones is advancing MQ resin technology with its PURESIL™ TMS series, offering superior oil resistance and abrasion performance for cosmetics and coatings. The company is transitioning toward a circular silicone economy, achieving over 50% recycling rates in resin and HCR applications. Its strategic divestment of the Silicones division enables greater focus on upstream silicon and biocarbon production. With operating income of NOK 33 billion, Elkem maintains strong financial resilience despite pricing pressures. Its CDP “A” rating enhances competitiveness in ESG-driven procurement markets. This positions Elkem as a pioneer in circular, high-performance silicone resin innovation.

Japan Silicone Resins Market Anchored by Semiconductor-Grade Purity and Functional Materials Leadership

Japan continues to function as a global benchmark for high-purity silicone resins, driven by deep integration with advanced semiconductor manufacturing and functional materials innovation. In late 2025, Shin-Etsu Chemical finalized a major expansion of its Gunma manufacturing complex, investing approximately ¥83 billion to support semiconductor lithography materials, including EUV-compatible silicone resin photoresists. This expansion reinforces Japan’s role as a critical supplier of ultra-high-purity silicone resins aligned with next-generation logic and memory nodes, where impurity tolerance is measured at 7N and 8N levels.

Beyond semiconductors, Japan’s silicone resins ecosystem is benefiting from cross-industry deployment. In July 2025, Shin-Etsu partnered with Stratasys Ltd. to commercially launch P3™ Silicone 25A, a DLP-enabled silicone resin supporting complex, elastomeric parts for medical devices and automotive components. Concurrently, Japanese automotive suppliers are accelerating the use of silicone resins for EV motor coil impregnation, where thermal stability, flame retardancy, and dielectric strength are decisive performance factors. From a policy standpoint, Japan’s Critical Material Security initiatives continue to provide R&D tax incentives for domestic production of ultra-pure silicone precursors, while Shin-Etsu’s transition to biomass cogeneration in 2025 demonstrates how decarbonization strategies are being embedded directly into functional silicone resin manufacturing.

United States Silicone Resins Market Defined by Decarbonization Platforms and CHIPS-Driven Electronics Demand

The United States silicone resins market is increasingly shaped by sustainability-led product innovation and strategic semiconductor reindustrialization. In mid-2025, Dow introduced its Decarbia™ reduced-carbon platform, featuring low-carbon silicone resin gum film formers such as DOWSIL™ MQ-1610 ID, produced using decarbonized silicon metal feedstocks. This initiative positions silicone resins as a compliant material class for ESG-driven procurement, reinforced by third-party Environmental Product Declarations and Life Cycle Analyses released alongside Dow’s 2025 product launches.

On the demand side, the CHIPS Act has catalyzed new “mega-fab” investments, prompting domestic silicone manufacturers to expand ultra-high-purity chemical delivery systems for on-site semiconductor use. Silicone resins are increasingly specified for advanced conformal coatings in logic and memory fabs due to their dielectric reliability and chemical resistance. Additionally, Dow’s late-2025 launch of DOWSIL™ FC-5012 ID Resin Gum underscores the diversification of U.S. silicone resin demand into high-performance cosmetics, where breathable, water-repellent film formers support long-wear formulations. At an infrastructure level, the U.S. Department of Energy has prioritized silicone-based resins for grid-scale battery protection, particularly in coastal environments where humidity-driven degradation risks remain high.

Germany Silicone Resins Market Strengthened by Bio-Based Chemistry and Energy Infrastructure Applications

Germany represents a mature yet rapidly adapting silicone resins market, characterized by regulatory-driven reformulation and energy infrastructure investment. In 2025, Wacker Chemie AG expanded its ELASTOSIL® eco portfolio, introducing silicone resins produced with plant-based methanol. These materials reduce fossil dependency while preserving the high-purity and biocompatibility requirements of lifestyle and medical applications, aligning closely with Germany’s sustainability benchmarks.

Energy transmission and electrification remain structural demand drivers. At the K 2025 International Trade Fair, Wacker emphasized the role of silicone resins as outdoor insulation materials for European grid expansion, where long-term weather resistance and dielectric integrity are critical. In parallel, Wacker debuted a ceramifying silicone resin system for busbars that forms a protective ceramic layer under fire exposure, preventing short circuits in traction batteries. Capacity expansions at integrated “Verbund” sites by Wacker and Evonik further support the European solar PV sector, particularly for junction box potting resins. Regulatory pressure is also reshaping portfolios, as updated EU REACH limits on D4, D5, and D6 siloxanes below 0.1% have necessitated full reformulation of consumer-facing silicone resin systems in Germany.

China Silicone Resins Market Accelerated by Regulation, Infrastructure Scale, and Semiconductor Packaging

China’s silicone resins market is undergoing rapid structural upgrading, driven by tighter regulatory standards and large-scale domestic demand. In September 2025, China issued GB 4806.16-2025, a mandatory national standard governing food-contact silicone materials. Effective from September 2026, the regulation introduces stringent VOC limits, compelling producers to redesign silicone resin formulations for compliance while improving safety credentials.

Semiconductor packaging represents a high-growth application area. Domestic producers such as Zhejiang Xinan Chemical have scaled production of ultra-fine viscosity silicone resins tailored for High Bandwidth Memory encapsulation, supporting China’s AI chip supply chain. Infrastructure remains another defining factor, with silicone resin-based water repellents deployed across more than 100,000 kilometers of reinforced concrete under the 14th Five-Year Plan. Environmental policy is reinforcing this shift, as a 2025 VOC tax pilot program has driven a reported 35% year-on-year increase in R&D focused on water-borne silicone resin systems. In automotive electronics, China retains leadership in volume consumption for LED encapsulation and ADAS sensor protection, where optical clarity and thermal stability up to 200°C are essential.

South Korea Silicone Resins Market Driven by HBM Packaging and Battery Safety Integration

South Korea’s silicone resins market is tightly coupled with its advanced electronics and battery manufacturing ecosystem. In early 2025, Wacker Chemie AG inaugurated a new specialty silicone resins facility in Jincheon, supplying high-performance materials to domestic semiconductor and automotive manufacturers. This investment aligns with the “K-Semiconductor Belt” strategy, which prioritizes localized supply chains for critical materials.

Demand is particularly strong in memory packaging. With SK Hynix reporting HBM products accounting for more than 40% of DRAM revenue in late 2024, the requirement for low-metal, ultra-clean silicone resins used in chip encapsulation has intensified. Corporate consolidation has further reshaped the supply landscape, as KCC Corporation completed the integration of Momentive Performance Materials, creating a vertically integrated silicone resin supplier serving the APAC battery market. In EV manufacturing, Tier-1 suppliers are rapidly adopting dielectric silicone potting resins to enhance moisture resistance and thermal stability in next-generation prismatic battery packs.

Comparative Snapshot: Silicone Resins Country-Level Dynamics

Silicone Resins Market County Level Snapshot

|

Country

|

Key Demand Drivers

|

Strategic Focus Areas

|

Policy and Regulatory Influence

|

|

Japan

|

Semiconductors, EV motors, 3D printing

|

Ultra-high purity resins, biomass-powered production

|

R&D tax credits for critical materials

|

|

United States

|

Semiconductor fabs, cosmetics, energy storage

|

Low-carbon silicone platforms, ESG compliance

|

CHIPS Act, DOE grid resilience priorities

|

|

Germany

|

Grid expansion, EV safety, solar PV

|

Bio-based resins, ceramifying technologies

|

EU REACH siloxane reformulation

|

|

China

|

Infrastructure protection, AI chips, automotive LEDs

|

Water-borne systems, HBM encapsulation

|

Food-contact standards, VOC taxation

|

|

South Korea

|

HBM memory, EV batteries, electronics

|

Vertical integration, specialty low-metal resins

|

Semiconductor industrial policy

|

Silicone Resins Market Report Scope

Silicone Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.8 Billion

|

|

Market Size (2034)

|

$17.8 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Product Type (Methyl Silicone Resins, Methylphenyl Silicone Resins, Phenyl Silicone Resins, Alkyl Silicone Resins, Modified Silicone Resins), By Form (Liquid Resins, Powder Resins, Water-Borne Emulsions, Silicone Resin Gums), By Function (Binding Agents, Encapsulants & Potting Compounds, Adhesion Promoters, Film Formers, Hydrophobing Agents, Crosslinkers), By End-Use Industry (Paints & Coatings, Electronics & Semiconductors, Automotive, Personal Care, Construction, Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shin-Etsu Chemical Co. Ltd., Dow Inc., Wacker Chemie AG, Evonik Industries AG, Momentive Performance Materials Inc., Elkem ASA, Zhejiang Xanan Chemical Industrial Group, Gelest Inc., Siltech Corporation, CHT Group, Hoshine Silicon Industry Co. Ltd., Kaneka Corporation, Specialty Silicone Products Inc., Arkema SA, Innospec Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silicone Resins Market Segmentation

By Product Type

- Methyl Silicone Resins

- Methylphenyl Silicone Resins

- Phenyl Silicone Resins

- Alkyl Silicone Resins

- Modified Silicone Resins

By Form

- Liquid Resins

- Powder Resins

- Water-Borne Emulsions

- Silicone Resin Gums

By Function

- Binding Agents

- Encapsulants & Potting Compounds

- Adhesion Promoters

- Film Formers

- Hydrophobing Agents

- Crosslinkers

By End-Use Industry

- Paints & Coatings

- Electronics & Semiconductors

- Automotive

- Personal Care

- Construction

- Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silicone Resins Industry

- Shin-Etsu Chemical Co. Ltd.

- Dow Inc.

- Wacker Chemie AG

- Evonik Industries AG

- Momentive Performance Materials Inc.

- Elkem ASA

- Zhejiang Xinan Chemical Industrial Group

- Gelest Inc.

- Siltech Corporation

- CHT Group

- Hoshine Silicon Industry Co. Ltd.

- Kaneka Corporation

- Specialty Silicone Products Inc.

- Arkema SA

- Innospec Inc.

*- List not Exhaustive