Smart Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Smart Packaging Market Set to Surge to $51.1 Billion by 2034, Driven by Safety, Traceability, and Consumer Engagement

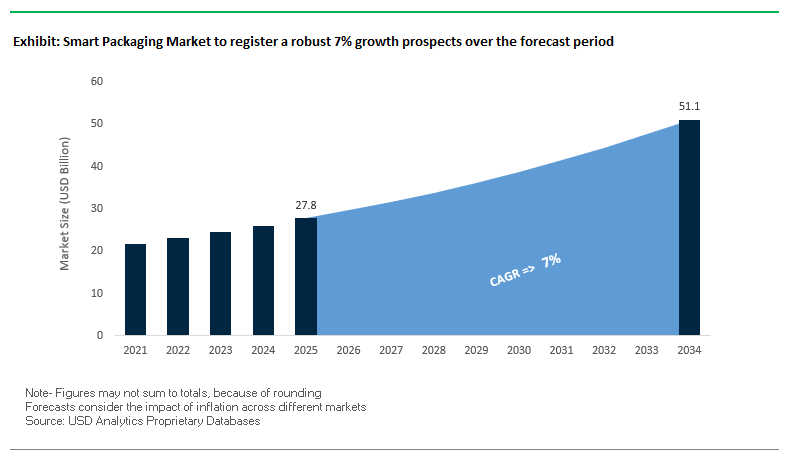

The global smart packaging market is projected to grow from $27.8 billion in 2025 to $51.1 billion by 2034, representing a CAGR of 7%. The industry is evolving rapidly, integrating advanced technologies such as sensors, indicators, RFID, NFC, and QR codes into packaging to provide real-time monitoring, enhanced safety, and interactive consumer engagement. Smart packaging is redefining the way brands communicate with consumers, improving supply chain efficiency while enhancing product integrity and market responsiveness.

Key Insights for Industry Professionals:

- Enhanced Product Safety: Smart packaging uses time-temperature indicators, tamper-evident seals, and contamination sensors, ensuring product integrity across food, beverage, and pharmaceutical industries.

- Supply Chain Efficiency and Traceability: RFID tags and QR codes enable real-time tracking, reducing losses due to spoilage, theft, or recalls.

- Consumer Engagement and Personalization: Technologies like NFC and AR provide interactive product information, enhancing brand trust and loyalty.

- Data-Driven Insights: Smart packaging interactions allow companies to collect consumer behavior and usage data, informing marketing strategies and product development.

- Sustainability Focus: Adoption of smart and recyclable materials aligns with regulatory pressures and environmental goals, enhancing brand reputation.

Market Analysis: Recent Strategic Moves Highlight Smart Packaging Innovations, Sustainability, and Market Consolidation

The smart packaging market has experienced substantial innovation and strategic activity in recent years, with companies focusing on sustainable materials, intelligent packaging technologies, and market consolidation. In August 2025, Klöckner Pentaplast received the German Packaging Award for its kp 100% Tray2Tray® innovation, a sustainable material breakthrough that demonstrates the sector’s commitment to environmental responsibility. In the same month, Aquapak Polymers Ltd reported that 86% of FMCG brands are willing to invest in sustainable packaging, underscoring rising demand for eco-conscious solutions. Additionally, Sealed Air Corporation introduced a new Bubble Wrap® embossed paper, enhancing its capabilities in protective and intelligent packaging.

In July 2025, Amcor, in collaboration with Volpak and Menshen, launched an inverted pouch designed for recyclability and reduced CO2 emissions, highlighting the push for eco-efficient packaging innovations. Earlier, in May 2025, DOW introduced a lightweight shrink sleeve film that reduces plastic use, ideal for high-volume beverage applications. In April 2024, Stora Enso launched Trayforma BarrPeel, a barrier-coated paperboard for recyclable vacuum skin packaging, reflecting industry efforts to reduce environmental footprints.

The market also saw strategic acquisitions and consolidation. In October 2024, Constantia Flexibles completed the Aluflexpack buyout, expanding its flexible packaging capabilities, while International Paper acquired UK-based DS Smith, positioning itself as a global leader in paper-based smart packaging.

Smart Packaging Market: Digital Engagement, Authentication, and Functional Innovation Driving Growth

Strategic Integration of QR Codes for Direct-to-Consumer Engagement

The smart packaging market is experiencing a surge in the adoption of QR codes as brands seek to build direct digital connections with consumers and bypass reliance on third-party platforms. In April 2025, Coca-Cola revived its iconic “Share a Coke” campaign with a modern twist by embedding QR codes on cans and bottles. When scanned, these codes directed consumers to a personalized digital hub, enabling customized product experiences and exclusive access to Coke Studio content. The campaign’s success, generating over 1 billion content streams, demonstrates the power of QR-enabled packaging as an owned media channel that fosters loyalty, engagement, and measurable return on marketing investment.

The strategic importance of QR codes also lies in their ability to facilitate first-party data collection at a time when third-party cookies are being phased out. According to the State of QR Codes 2025 report, 95% of businesses now use QR technology to capture behavioral and preference data directly from consumers. This permission-based model not only enhances data transparency but also enables hyper-personalized marketing strategies. For consumer goods companies, QR-driven smart packaging is becoming both a marketing enabler and a compliance tool, helping to balance consumer privacy with the need for actionable insights.

Deployment of NFC for Luxury Authentication and Resale Verification

The luxury goods sector is accelerating adoption of Near-Field Communication (NFC) technology to combat counterfeiting and enable secure resale verification. The global counterfeit trade—valued in the hundreds of billions annually—is a direct threat to brand equity. To mitigate this, leading luxury houses are embedding ultra-thin NFC chips within handbags, watches, and limited-edition packaging. When tapped with a smartphone, the NFC tag provides instant authentication, delivering consumer confidence and safeguarding brand reputation.

NFC also plays a critical role in the booming secondary luxury resale market. Technical reports highlight how NFC-enabled tags serve as a digital product passport, carrying immutable details on product origin, ownership history, and authenticity verification. This not only protects buyers and sellers but also strengthens the brand’s involvement in the resale lifecycle. For luxury packaging, NFC is not just a security layer—it is an ecosystem enabler, allowing circular ownership models and reducing fraud while maintaining consumer trust.

Compliance-Driven Adoption of Smart Food Freshness Indicators

Global food waste regulations are creating a strong incentive for the development of smart freshness indicators that go beyond static expiration dates. With the UN’s Sustainable Development Goal (SDG) 12.3 targeting a 50% reduction in food waste by 2030, and the EU advancing reforms to date labeling under the Packaging and Packaging Waste Regulation (PPWR), retailers and producers are under pressure to provide real-time product condition data.

Smart Time-Temperature Indicators (TTIs) represent one of the most promising technologies. A February 2025 study introduced advanced TTIs made from silver and gold nanoparticle nanodispersions, which visually change color based on the product’s cumulative exposure to temperature variations. These indicators can reliably detect breaches in the cold chain for perishable items like seafood, dairy, and ready-to-eat meals. For manufacturers and retailers, TTIs can reduce spoilage-related losses, enhance food safety, and demonstrate compliance with upcoming anti-waste policies, positioning them as a critical enabler of circular food systems.

Smart Packaging as an Enabler of Pharmaceutical Adherence and Reimbursement

In healthcare, smart packaging is redefining how pharmaceutical companies and providers address the global adherence challenge. Studies show that smart blister packs and pill bottles achieve 97% accuracy in tracking medication intake, compared to just 27% accuracy from patient self-reporting. This data provides healthcare providers with real-time adherence monitoring, enabling early interventions to improve patient outcomes and reduce hospitalizations.

Beyond healthcare delivery, smart packaging is opening doors to new reimbursement models. With adherence data integrated into digital health platforms, pharmaceutical companies can support outcome-based reimbursement schemes—where insurers and payers reimburse based on demonstrated patient outcomes rather than just prescriptions filled. This not only aligns financial incentives but also creates a value-based ecosystem where packaging innovation directly impacts drug efficacy, reimbursement policies, and patient trust.

Competitive Landscape: Key Global Players Are Leading Smart Packaging Innovation, Sustainability, and Operational Excellence

The smart packaging industry is dominated by global companies leveraging material science expertise, technological innovation, and strategic acquisitions to deliver high-performance, sustainable packaging solutions for multiple end-use industries.

Avery Dennison Corporation: Driving Consumer Engagement Through Intelligent Labeling and RFID Solutions

Avery Dennison offers a wide portfolio of intelligent labels and RFID-enabled packaging solutions, providing real-time product tracking, authentication, and interactive consumer engagement. The company’s Innovations strategy includes partnerships with Velocys to advance CO2-derived e-SAF production, reflecting a commitment to sustainability and technological advancement. Avery Dennison leverages brand recognition and a vertically integrated business model to serve diverse regions and industries.

CCL Industries Inc.: Transforming Product Authentication and Traceability with Next-Gen Smart Labels

CCL Industries specializes in RFID and NFC-enabled labeling solutions, delivering authentication, traceability, and logistics optimization. In February 2024, the company launched recycling-friendly polyolefin shrink sleeves, supporting circular economy goals. CCL’s vertically integrated operations and expertise in specialty labels allow it to maintain market leadership and global reach.

Amcor PLC: Leading Sustainable Packaging with Sensor-Enabled Smart Solutions

Amcor provides recyclable, reusable, and bio-based packaging solutions integrated with sensors for real-time monitoring and environmental tracking. In July 2025, the company launched an inverted pouch for recyclability and reduced CO2 emissions, alongside its Liquiflex AmPrima pouches in Europe, achieving 79% carbon footprint reduction. Amcor combines brand strength and manufacturing expertise to deliver innovative smart packaging across global markets.

Sealed Air Corporation: Pioneering Sensor-Integrated Packaging for Protection and Sustainability

Sealed Air integrates temperature, humidity, and motion sensors into protective packaging. In August 2025, it introduced Bubble Wrap® embossed paper, improving recyclability and sustainability. The company emphasizes circular economy practices, vertical integration, and innovation, enabling it to maintain a leadership position in intelligent and protective packaging markets.

WestRock Company: Merging Paper-Based Expertise with Smart Packaging Technologies

WestRock provides paper-based packaging solutions with integrated traceability and digital interactivity. Following its July 2024 merger with Smurfit Kappa, WestRock emerged as a global packaging powerhouse with enhanced capabilities in containerboard, corrugated boxes, and smart packaging solutions. The company combines technological innovation with sustainability initiatives to meet evolving consumer and supply chain demands.

Smart Packaging Market Share Insights, 2025-2034

Healthcare & Pharmaceuticals Lead Smart Packaging Market Share by End-Use Industry

The healthcare and pharmaceuticals sector holds 30% of the smart packaging market, making it the single largest driver of adoption. This dominance stems from the non-negotiable requirements of safety, compliance, and authenticity in a highly regulated industry. Smart packaging here goes far beyond branding—it is a tool for patient protection and regulatory adherence. Temperature-sensitive labels for vaccines, NFC-enabled authentication for high-value drugs, and smart blister packs that track patient adherence all illustrate how these technologies are indispensable. With counterfeit medicines costing the global industry billions annually, pharmaceutical firms are prioritizing anti-counterfeiting solutions integrated into packaging. Furthermore, the rollout of advanced biologics and personalized medicines increases the need for packaging that monitors storage conditions in real time, securing the pharmaceutical industry’s continued leadership in smart packaging adoption.

Plastics Dominate Smart Packaging Market Share by Material Integration

Plastics account for 55% of smart packaging substrates, cementing their position as the backbone of technological integration. Their moldability and adaptability allow embedding of RFID tags, printed electronics, and conductive inks directly into containers and films. Plastic films provide the flexibility required for pressure-sensitive labels and NFC antennas, making them the most compatible material with emerging digital applications. Beyond their technical suitability, plastics also remain the preferred choice due to their lightweight nature, durability, and ability to incorporate recycled content, which aligns with sustainability regulations. As mono-material films and rPET gain traction in packaging sustainability strategies, plastics’ dominance is expected to remain intact. However, competition from paper-based smart labels is increasing, particularly in industries seeking recyclable substrates to balance sustainability with digital functionality.

United States: Recycling Targets and Innovation in Digital Monitoring

The United States smart packaging market is being shaped by ambitious recycling and sustainability targets set by the U.S. Environmental Protection Agency (EPA), which aims to raise the national recycling rate to 50% by 2030. This regulatory push is encouraging investments in recycling infrastructure and the use of sustainable materials across smart packaging applications. The country is witnessing significant adoption of digital twin technology and real-time monitoring systems, particularly in the pharmaceutical and food sectors, where traceability and anti-counterfeiting measures are critical.

Additionally, demand for high-performance smart labels with integrated NFC tags, RFID chips, and embedded sensors is surging in logistics, e-commerce, and food and beverage industries. Companies like ProAmpac are pioneering sustainable materials, including plant-based plastics and paper-based flexible packaging, under their ProActive Recyclable® portfolio. At the same time, the Association of Plastic Recyclers (APR) is guiding the adoption of washable inks and floatable films, enhancing recyclability in smart packaging. This mix of innovation and regulatory momentum makes the U.S. a leader in the development of sustainable, intelligent packaging systems.

European Union: PPWR, ESPR, and Circular Economy Integration

The European Union smart packaging market is undergoing a major transformation under the Packaging and Packaging Waste Regulation (PPWR), which came into effect in February 2025. The regulation mandates that all plastic components in packaging, including smart films and labels, must incorporate minimum levels of post-consumer recycled content by 2030. This aligns with the Ecodesign for Sustainable Products Regulation (ESPR), which promotes mono-material flexible packaging to streamline recycling processes.

From August 2026, the EU will also restrict the use of PFAS in food contact materials, prompting innovation in barrier coatings and adhesives for smart packaging. Furthermore, the EU is encouraging refill and reuse systems, which will directly affect the design of durable, intelligent packaging solutions. These combined initiatives are accelerating the shift toward digitally enabled and eco-friendly packaging in industries such as pharmaceuticals, cosmetics, and premium foods, where smart labels and interactive packaging are becoming essential tools for compliance and consumer engagement.

China: Regulatory Mandates and Premium Smart Packaging Demand

The China smart packaging market is advancing rapidly, driven by both government regulations and consumer demand for high-end packaging. From June 1, 2025, new rules require express delivery companies to use eco-friendly, reduced, and reusable packaging, which includes smart-enabled packaging solutions. The NDRC and MEE, under the 14th Five-Year Plan, are also leading initiatives to reduce plastic waste and accelerate adoption of sustainable solutions across logistics and e-commerce.

Simultaneously, there is a sharp rise in demand for luxury and technologically advanced smart packaging, fueled by growth in premium food, cosmetics, and electronics markets. Manufacturers are integrating sensors, advanced printing technologies, and tamper-evident features to appeal to consumer preferences for both convenience and authenticity assurance. Government support for the remanufacturing industry, backed by tax incentives for green technologies, is further catalyzing investment in intelligent, sustainable packaging formats.

India: EPR Regulations and National Mission for Sustainable Smart Packaging

The India smart packaging market is being shaped by the Plastic Waste Management (Amendment) Rules, 2024, which became effective in April 2025. These rules enforce Extended Producer Responsibility (EPR) for packaging manufacturers, compelling the industry to take responsibility for recycling and disposal. From July 1, 2025, all packaging must also be traceable through barcodes or QR codes, a regulation that is particularly relevant for smart packaging technologies that naturally integrate traceability features.

In addition, the Council of Scientific and Industrial Research (CSIR) has launched a National Mission for sustainable packaging, with a strong focus on homegrown smart packaging innovations to support India’s net-zero ambitions. The rapid growth of e-commerce and retail, combined with rising demand for traceability and product authentication, is fueling adoption of NFC-enabled labels, freshness sensors, and QR-based traceability systems. This makes India one of the fastest-growing markets for digitally integrated sustainable packaging.

Japan: Plastic Circulation Laws and Intelligent Packaging in Beauty Sector

The Japan smart packaging market is being transformed by the Plastic Resource Circulation Strategy, which requires all packaging to be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law, also effective in 2025, targets the reduction or redesign of 12 categories of single-use plastic products, encouraging companies to develop compostable and reusable smart packaging formats.

Japanese brands, particularly in the beauty and personal care sector, are leading in the adoption of intelligent packaging solutions. Companies are incorporating NFC-enabled smart packaging, blockchain integration, and interactive features to combat counterfeiting and enhance consumer engagement in the fast-growing e-commerce sector. With its strong regulatory framework and innovation-driven industries, Japan is positioning itself as a pioneer in sustainable, high-tech smart packaging.

Brazil: Reverse Logistics and Regulatory Support for Food Contact Packaging

The Brazil smart packaging market is supported by strong environmental policies, led by the National Solid Waste Policy (PNRS), which emphasizes reuse, recycling, and responsible waste disposal. The implementation of Law No. 15,088 in January 2025, banning the import of solid waste including plastics, is pushing domestic companies to develop sustainable smart packaging solutions locally.

Additionally, Anvisa (Brazil’s Health Regulatory Agency) revised food contact packaging regulations in February 2025, adding new substances to the positive list for food-grade plastics. This directly influences the selection of materials used in smart packaging, particularly in the food and beverage sector. Combined with government-backed reverse logistics initiatives, these regulations are reinforcing the shift toward recyclable, intelligent packaging solutions that meet both sustainability and safety requirements.

Smart Packaging Market Report Scope

Smart Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$27.8 Billion

|

|

Market Size (2034)

|

$51.1 Billion

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Technology (Active Packaging, Intelligent Packaging, Modified Atmosphere Packaging), By End-Use Industry (Food & Beverages, Healthcare & Pharmaceuticals, Personal Care & Cosmetics, Logistics & Transportation, Automotive & Industrial Products, Consumer Electronics, Home & Industrial Chemicals), By Material (Plastics, Paper & Paperboard, Glass, Metal, Bioplastics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Huhtamaki Oyj, Berry Global, Inc., Sealed Air Corporation, Avery Dennison Corporation, Mondi Group, ProAmpac, Sonoco Products Company, Crown Holdings Inc., BASF SE, Stora Enso Oyj, WestRock Company, Tetra Pak Inc., DuPont, Klöckner Pentaplast

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Smart Packaging Market Segmentation

By Technology

- Active Packaging

- Intelligent Packaging

- Modified Atmosphere Packaging

By End-Use Industry

- Food & Beverages

- Healthcare & Pharmaceuticals

- Personal Care & Cosmetics

- Logistics & Transportation

- Automotive & Industrial Products

- Consumer Electronics

- Home & Industrial Chemicals

By Material

- Plastics

- Paper & Paperboard

- Glass

- Metal

- Bioplastics

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Smart Packaging Market

- Amcor plc

- Huhtamaki Oyj

- Berry Global, Inc.

- Sealed Air Corporation

- Avery Dennison Corporation

- Mondi Group

- ProAmpac

- Sonoco Products Company

- Crown Holdings Inc.

- BASF SE

- Stora Enso Oyj

- WestRock Company

- Tetra Pak Inc.

- DuPont

- Klöckner Pentaplast

* List Not Exhaustive

Methodology

The research methodology for the Smart Packaging Market combines primary and secondary research approaches to ensure accurate, actionable, and data-driven insights. Primary research involved interviews with industry executives, packaging engineers, supply chain specialists, sustainability experts, and technology innovators across North America, Europe, Asia-Pacific, India, Japan, and Brazil. Secondary research included analysis of annual reports, regulatory databases, patent filings, sustainability disclosures, trade journals, and verified industry publications. USDAnalytics applied advanced data triangulation to validate market sizing, growth projections, and technology adoption trends, integrating factors such as smart sensor deployment, NFC/RFID integration, QR code engagement, and regulatory compliance. Forecasts were built using both top-down and bottom-up approaches, while regional insights were contextualized against policy frameworks, Extended Producer Responsibility (EPR) mandates, consumer preferences for digital interactivity, and supply chain optimization. This multi-layered methodology ensures the report delivers fact-based, real-world intelligence on smart packaging innovations, sustainability adoption, and market consolidation trends for industry professionals and decision-makers.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.