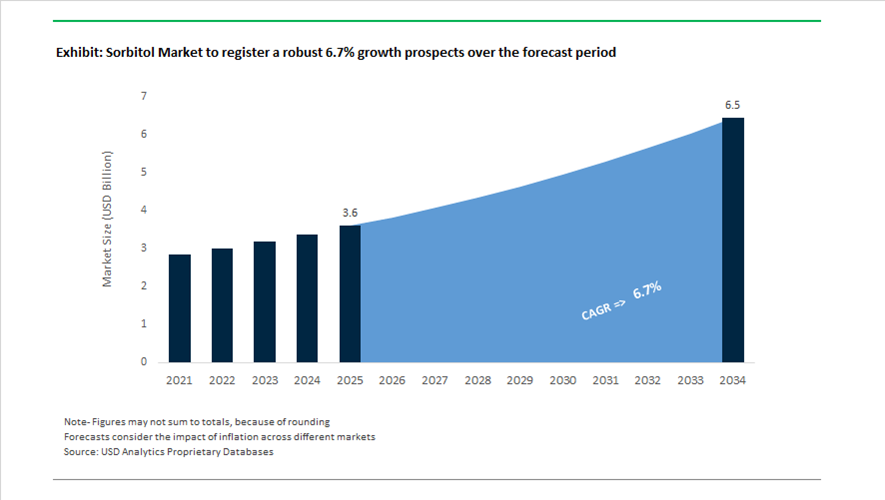

Sorbitol Market Valuation 2025–2034: $3.6 Billion to $6.5 Billion at 6.7% CAGR Driven by Pharma Excipients, Sugar Reduction, and Clean-Label Polyols

The global sorbitol market is valued at $3.6 billion in 2025 and is projected to reach $6.5 billion by 2034, expanding at a CAGR of 6.7%. Growth is underpinned by increasing demand for sorbitol syrup and sorbitol powder across pharmaceutical excipients, sugar-free confectionery, oral care, personal care humectants, and industrial surfactants. Sorbitol’s multifunctional properties including sweetness, moisture retention, plasticizing ability, and low glycemic response make it central to sugar-reduction strategies and chewable tablet formulations. Expansion in bio-based sweeteners, pharmaceutical-grade polyols, and clean-label food reformulation programs is reshaping capacity allocation and R&D priorities across leading producers.

In February 2024, Gujarat Ambuja Exports commissioned a 100 TPD sorbitol unit at its Hubli facility, raising total installed capacity to 500 TPD across four sites and establishing the company as India’s largest sorbitol producer. In early 2024, Roquette expanded production at its Lestrem, France site by approximately 15% to address rising European demand for bio-based sweeteners and pharmaceutical excipients. In July 2024, Ingredion EMEA launched FIBERTEX CF citrus fibers, often formulated alongside sorbitol to maintain texture and moisture in sugar-reduced applications. During 2024, more than 600 new global food and beverage launches incorporated organic or clean-label sorbitol, reflecting strong growth in naturally derived polyols. In August 2024, a Turkish starch derivatives producer upgraded its sorbitol line with RHEWUM’s RHEsono® screening technology to enhance particle precision for pharmaceutical and high-spec food grades.

Strategic restructuring and portfolio optimization intensified in 2025. In May 2025, Roquette finalized its acquisition of IFF Pharma Solutions, significantly expanding its excipient portfolio and reinforcing leadership in pharmaceutical-grade sorbitol and drug delivery systems. Following this acquisition, Roquette reorganized into two global business groups, Pharma Solutions and Core Ingredients, to enhance agility in serving health and nutrition markets. In early 2024, Ingredion divested its South Korean operations to reallocate capital toward high-growth Texture & Healthful Solutions, including specialty polyols such as sorbitol. In late 2025, manufacturers introduced pan-agglomerated and spray-dried high-purity sorbitol powder grades with improved flowability and solubility, targeting chewable tablets and fast-dissolve pharmaceutical formats.

Sustainability and innovation pathways are shaping the 2025–2026 outlook. Throughout 2025, producers initiated pilot-scale fermentation-based sorbitol production using microorganisms such as Zymomonas mobilis, exploring lower-carbon alternatives to conventional catalytic hydrogenation. In 2025 and 2026, ADM completed a $26 million two-phase investment at its Erlanger Innovation Campus focused on sugar-reduction and mouthfeel solutions where sorbitol plays a core formulation role. These investments indicate growing emphasis on bio-based polyol production, pharmaceutical excipient specialization, and advanced texture engineering, positioning sorbitol as a critical ingredient platform in both healthcare and functional nutrition markets through 2034.

Key Trends and Strategic Opportunities in the Global Sorbitol Market

Aggressive Portfolio Reformulation Driven by Global Sugar Taxes and HFSS Regulations

The sorbitol market is being structurally reshaped by the rapid expansion of sugar taxes and High Fat, Sugar, and Salt regulations across both developed and emerging economies. By mid-2025, more than 50 countries had implemented or formally proposed sugar-related levies, transforming sweetener selection from a formulation preference into a regulatory necessity. Sorbitol has emerged as a primary bulk sweetener of choice because it enables manufacturers to reduce free sugar content without compromising texture, moisture retention, or shelf stability in confectionery, bakery, and beverage formulations.

Regulatory tightening in the United Kingdom provides a clear signal of this shift. In April 2025, the UK Government published its consultation summary on strengthening the Soft Drinks Industry Levy, lowering the taxation threshold from 5 grams to 4.5 grams of sugar per 100 milliliters. This change has already driven an average 47% reduction in sugar content among affected products, accelerating the substitution of sucrose with polyols. Sorbitol is increasingly specified in diet beverages and plant-based milk alternatives because it delivers bulk sweetness while supporting clean taste profiles and caloric reduction.

Supply-side behavior is adjusting accordingly. In the Asia-Pacific region, Q4 2025 trading data indicates that food manufacturers are locking in multi-year contracts for liquid sorbitol to hedge against starch price volatility. This trend is especially pronounced in India and Indonesia, where localized corn and tapioca processing has enabled the food and beverage segment to account for roughly 35.5% of regional sorbitol consumption by volume, reinforcing sorbitol’s role as a strategic ingredient rather than a commodity sweetener.

Pharmaceutical Expansion into Patient-Centric Solid Dosage Forms

In pharmaceuticals, sorbitol is transitioning from a conventional excipient to a core enabler of patient-centric drug delivery. Its non-reactive chemistry, cooling mouthfeel, and excellent compressibility make it particularly well suited for orally disintegrating tablets, chewables, and pediatric formulations. These dosage forms are gaining traction as healthcare systems prioritize adherence, ease of administration, and improved patient experience.

Strategic capacity expansion underscores this trend. In March 2021, with operational integration updates continuing through May 2025, Roquette completed the acquisition of IFF Pharma Solutions, significantly expanding its excipient portfolio and U.S. manufacturing footprint. This move positioned pharmaceutical-grade sorbitol at the center of a broader excipient platform, supporting demand that now represents approximately 27% of global consumption for crystalline pharmaceutical grades.

Formulation science is also evolving. Updates to USP-NF and European Pharmacopoeia standards in 2025 have intensified R&D around crystalline sorbitol with purity levels exceeding 98%. These low-hygroscopicity grades are increasingly preferred for moisture-sensitive active pharmaceutical ingredients, as they reduce degradation risk and extend product stability compared with more hygroscopic polyols. As solid oral dosage innovation accelerates, pharmaceutical-grade sorbitol is becoming a specification-driven input with long qualification cycles and strong pricing resilience.

Transition to Sorbitol-Based Non-Phthalate Bio-Plasticizers

One of the most attractive growth opportunities for the sorbitol market lies in bio-based plasticizers, driven by tightening restrictions on phthalates under REACH in Europe and parallel regulatory scrutiny in the United States. Sorbitol esters are emerging as leading non-phthalate alternatives for medical-grade PVC, food-contact materials, and flexible packaging applications due to their low migration behavior and proven biocompatibility.

By December 2025, bio-based plasticizers were outperforming phthalate-based products in growth rates, particularly in the medical device segment. Sorbitol-derived plasticizers align closely with sustainability frameworks such as the United Nations Global Plastics Treaty objectives, positioning them as future-proof solutions for regulated applications. Upstream integration is reinforcing this opportunity. Major starch processors including ADM and Ingredion allocated nearly 29% of their 2025 North American capital expenditure toward upgrading processing technologies. These investments are aimed at producing high-purity sorbitol syrups that serve as feedstocks for biodegradable surfactants and non-toxic polymer additives, strengthening vertical integration and margin capture.

Sorbitol as a Primary Feedstock for Renewable Isosorbide

The conversion of sorbitol into isosorbide represents one of the most strategically significant growth pathways in the market. Isosorbide is a renewable diol used in high-performance engineering plastics, including bio-based polycarbonates and polyesters that offer superior heat resistance, rigidity, and optical clarity. This pathway allows manufacturers to replace petroleum-derived Bisphenol-A while leveraging existing carbohydrate supply chains.

Technological progress is accelerating commercialization. Research published in September 2025 highlights sulfated zirconia and advanced zeolite catalysts capable of achieving up to 99.3% conversion efficiency from sorbitol to isosorbide. These advances materially lower production costs, narrowing the price gap between bio-based and fossil-based engineering plastics. Investment patterns reflect this momentum. Asia-Pacific accounts for more than 41% of new capital expenditure directed toward sorbitol-to-isosorbide facilities, driven by regional strategies to dominate global supply of sustainable monomers for automotive and electronics applications. As regulatory pressure on BPA intensifies, sorbitol-derived isosorbide is positioned as a cornerstone building block for the next generation of bio-based materials.

Sorbitol Market Share and Segmentation Insights

Liquid Sorbitol Dominates the Sorbitol Market Through Efficient Processing and Bulk Handling Advantages

Liquid sorbitol accounted for 68.40% of the sorbitol market in 2025, making it the most widely used product form across food processing, pharmaceutical formulations, and personal care products. Typically supplied as a 70% aqueous solution, liquid sorbitol offers advantages including ease of handling, precise dosing, and direct incorporation into liquid and semi-solid formulations without the need for dissolution. These characteristics support efficient manufacturing processes in large-scale production environments. A key 2025 industry development is the advancement of high-concentration liquid sorbitol production technologies, where manufacturers optimize solution stability to prevent crystallization during storage and transport while offering specialty liquid grades tailored for specific food, pharmaceutical, and personal care applications.

Food & Confectionery Industry Drives Global Sorbitol Consumption for Sugar-Free Products

Food and confectionery represent the largest application segment in the sorbitol market, accounting for 48.60% of global demand in 2025 due to the widespread use of sorbitol as a low-calorie sweetener and humectant in sugar-free products. Sorbitol provides bulk sweetness, moisture retention, and improved texture stability in products such as chewing gum, sugar-free candies, chocolates, baked goods, and diet foods. Its functionality supports reduced-sugar product development while maintaining desirable taste and mouthfeel characteristics. A major 2025 market trend is the expansion of clean label confectionery products, where sorbitol benefits from its natural occurrence in fruits and plant-based production from corn feedstocks, enabling food manufacturers to market reduced-sugar products with recognizable and consumer-friendly ingredient profiles.

Sorbitol Market Competitive Landscape

The global sorbitol market in 2026 is driven by pharmaceutical-grade excipients, non-cariogenic sweeteners, and bio-based humectants. Industry leaders are advancing enzymatic hydrogenation efficiency, clean-label certifications, and high-purity sorbitol solutions to meet regulatory demands across oral care, dietetic foods, and pharmaceutical applications.

Roquette Strengthens Pharma-Grade Sorbitol Portfolio Through IFF Integration and Shift & Lead Strategy

Roquette Frères is reinforcing its leadership in the sorbitol market with a 12.6% EBITDA margin in 2025, driven by strong performance in Health & Pharma Solutions. Its “Shift & Lead” strategy focuses on operational excellence and high-value innovation in plant-based excipients. Integration of IFF Pharma Solutions enhances its sorbitol portfolio with cellulose and alginate-based multifunctional binders for pharmaceutical applications. The company is targeting advanced excipient systems aligned with GLP-1 support products and regulated drug formulations. Roquette’s sustainability recognition strengthens its positioning in bio-based polyols and clean-label ingredients. Its focus on high-purity sorbitol and pharmaceutical-grade solutions supports growth in regulated markets.

ADM Expands Corn-Based Sorbitol Production with Cost Optimization and Industrial Biosolutions Diversification

Archer Daniels Midland Company (ADM) is leveraging its carbohydrate solutions platform with a 2026 EPS guidance of $3.60 to $4.25 and a $500 million to $750 million cost-saving program. Its sorbitol production is fully integrated with U.S.-sourced corn, providing supply chain stability amid global volatility. ADM is expanding applications beyond food into industrial biosolutions, including textiles, detergents, and contact lens stabilizers. Operational efficiency improvements and safety milestones enhance plant productivity and cost competitiveness. Clean fuel tax credits provide additional financial support for its bio-based chemical portfolio. ADM’s diversification strategy strengthens its position in both industrial and specialty sorbitol applications.

Cargill Scales C☆Sorbidex® Portfolio for Sugar Reduction, Oral Care, and Sustainable Humectant Applications

Cargill is advancing its sorbitol market presence through its C☆Sorbidex® portfolio, offering tailored powders and syrups for over 175 applications across food, pharma, and personal care. Its focus on sugar reduction and non-cariogenic formulations aligns with growing demand for tooth-friendly and low-calorie products. Sorbitol’s humectant properties support moisture retention and texture stability in confectionery and oral care products. The company is expanding sustainable sourcing practices for corn and wheat to meet clean-label and traceability requirements. Investments in starch-based sorbitol production capacity support rising demand in cosmetics and skincare formulations. Cargill’s product versatility and sustainability focus strengthen its competitive positioning.

Ingredion Expands Pharmaceutical and Personal Care Sorbitol Applications Through Texture and Wellness Strategy

Ingredion Incorporated is strengthening its role in the sorbitol market through its “Texture and Wellness” strategy, integrating sugar-reduction technologies and pharmaceutical excipients. Its investment in Better Juice highlights innovation in hybrid sugar-reduction systems using sorbitol. The company is scaling injectable-grade sorbitol stabilizers to support global vaccine production and pharmaceutical demand. Refinement of sorbitol-based humectants enables tailored viscosity for high-end skincare and oral care applications. Favorable corn pricing enhances cost competitiveness of its starch-derived sorbitol. Ingredion’s focus on functional polyols and clean-label solutions aligns with evolving consumer and regulatory trends.

Tereos Optimizes Starch-Based Sorbitol Production Through Debt Reduction and Flexible Manufacturing Strategy

Tereos is strengthening its competitive position in the sorbitol market through financial restructuring and operational efficiency improvements. The company reduced net debt by €106 million and secured €300 million in refinancing, supporting long-term investment in starch and sweetener production. Its Starch, Sweeteners & Renewables division accounts for 31% of total revenue, with sorbitol as a key value-added product. Decarbonization and energy efficiency projects across 38 industrial sites enhance sustainability and cost control. Tereos’ flexible production model allows rapid shifts toward high-margin pharmaceutical-grade sorbitol based on market demand. Its strong European presence supports supply to regulated food and pharma markets.

United States Sorbitol Market Positioned as a High-Purity Pharma and Nutrition Hub

The United States sorbitol industry is undergoing structural elevation driven by pharmaceutical consolidation, feedstock traceability, and formulation-led innovation. In May 2025, Roquette completed the acquisition of IFF Pharma Solutions, consolidating sorbitol-based excipients with advanced drug delivery technologies. This integration has strengthened the U.S. position as a manufacturing and formulation hub for high-purity Pearlitol® and METHOCEL™ sorbitol blends used in controlled-release tablets, oral suspensions, and chewable dosage forms. Parallel to pharma integration, the U.S. Department of Energy’s Climate-Smart Commodities grants announced in late 2024 have incentivized domestic producers such as ADM to transition toward fully traceable, non-GMO corn feedstocks, reinforcing supply resilience and sustainability credentials for fermented sorbitol.

Trade dynamics and application innovation are reshaping downstream demand. Following the escalation of U.S. import tariffs on chemical intermediates in spring 2025, food and confectionery brands accelerated reformulation toward domestically produced liquid sorbitol to reduce exposure to Asian polyol price volatility. Product differentiation is visible in oral care, where Ingredion launched its Clean Taste Solubility Solution in late 2024, a liquid sorbitol system engineered to enhance clarity and stability in premium translucent toothpaste gels. Regulatory alignment is also influencing grades. U.S. manufacturers introduced low-nitrite sorbitol fillers such as Avicel LN to comply with the FDA’s 2025 nitrosamine guidance, while SPI Pharma expanded production of highly compactible crystalline sorbitol in 2025 to serve the fast-growing chewable supplement segment.

China Sorbitol Market Anchored by Vitamin C Integration and Capacity Scale

China remains the world’s most integrated sorbitol market, with demand anchored in vitamin C synthesis and reinforced by state-led industrial policy. Sorbitol continues to serve as the primary intermediate in glucose-to-ascorbic acid value chains, with the National Development and Reform Commission advancing the Green Chemical Industrial Park policy in 2025 to centralize and optimize these pathways. This clustering approach improves energy efficiency, waste heat utilization, and logistics across sorbitol and downstream vitamin C production. Capacity optimization is accelerating, particularly in Shandong province, where state-aligned producers announced cumulative upgrades totaling 200,000 tons per year in late 2024, focused on enzymatic conversion efficiency and yield stability.

Regulatory and purity requirements are rising sharply. Implementation of GB 4806.16-2025 in late 2025 has compelled Chinese sorbitol manufacturers to eliminate trace volatile contaminants, bringing domestic food-contact quality closer to U.S. and EU benchmarks. At the same time, domestic firms have scaled production of 99.9% purity crystalline sorbitol to support emerging applications in semiconductor cleaning and precision chemical processing. Trade policy signals are also being closely monitored. The April 2025 Ministry of Commerce Announcement No. 18, while centered on rare earths, reflected a broader tightening of export licensing for dual-use chemical intermediates, increasing strategic emphasis on domestic downstream utilization of high-purity sorbitol.

Germany and European Union Sorbitol Market Driven by Regulatory Scrutiny and Circular Chemistry

Germany anchors the European sorbitol landscape through regulatory leadership, pharmaceutical logistics strength, and bio-based material innovation. As of July 2025, the European Food Safety Authority initiated an active re-evaluation of E 420 sorbitols, prompting German producers to expand toxicological data packages and process transparency to safeguard clean-label status across food and nutrition applications. Sustainability reporting is also becoming operationally embedded. Under the Corporate Sustainability Reporting Directive, chemical leaders such as BASF have integrated carbon-tracking software into sorbitol production lines, enabling precise disclosure of CO2 intensity per ton.

Germany is also advancing circular use cases. In 2025, biotech clusters successfully piloted commercial-scale production of sorbitol-derived isosorbide, a high-performance bio-monomer used in BPA-free plastics for medical devices and durable consumer goods. Verification of renewable origin has become a market differentiator. Following the EU Green Claims Directive, German brands are adopting Isotope Ratio Mass Spectrometry to certify that sorbitol inputs are fully plant-derived. Logistically, the expansion of clean-room-grade storage and handling hubs in Frankfurt and Hamburg has strengthened Germany’s role as an export gateway for pharmaceutical-grade sorbitol destined for emerging markets.

India Sorbitol Market Scaling Through BioE3 Policy and Export Orientation

India’s sorbitol industry is transitioning from domestic substitution to export-led growth, supported by biotechnology policy and trade protection. The BioE3 Policy approved in August 2024 introduced capital subsidies for bio-foundries converting surplus sugar and starch into high-value polyols, including sorbitol. This policy has accelerated capacity creation among domestic producers, improving fermentation yields and enabling consistent pharmacopeial-grade output. Trade defense has reinforced pricing stability. In November 2025, the Ministry of Industry and Trade concluded its review of anti-dumping measures on sorbitol imports from China and Indonesia, strengthening the competitive position of local players such as Gulshan Polyols.

Export capability is now a defining characteristic. Major facilities in Gujarat and Maharashtra achieved USP-NF and European Pharmacopoeia certifications in 2025, positioning India as a reliable supplier of crystalline sorbitol to regulated pharmaceutical markets in North America and Europe. Domestic demand is also expanding through public health programs. The Pradhan Mantri Bhartiya Janaushadhi Pariyojana has increased procurement of liquid sorbitol as a base for affordable pediatric iron and vitamin syrups, embedding sorbitol into India’s essential medicines supply chain.

Comparative Snapshot: Country-Level Sorbitol Industry Dynamics

Sorbitol Market County Level Snapshot

|

Country / Region

|

Primary Demand Drivers

|

Strategic Focus Areas

|

Structural Impact

|

|

United States

|

Pharmaceuticals, oral care, supplements

|

High-purity excipients, non-GMO feedstocks

|

Pharma-led value upgrading

|

|

China

|

Vitamin C synthesis, industrial scale

|

Integrated chemical parks, enzymatic efficiency

|

Global volume leadership

|

|

Germany / EU

|

Clean-label foods, medical materials

|

Regulatory compliance, isosorbide derivatives

|

Premium, traceable production

|

|

India

|

Exports, public health formulations

|

BioE3 bio-foundries, trade protection

|

Cost-competitive global supplier

|

Sorbitol Market Report Scope

Sorbitol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.6 Billion

|

|

Market Size (2034)

|

$6.5 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Product Form (Liquid Sorbitol, Crystalline Sorbitol), By Purity & Grade (Pharmaceutical Grade, Food & Beverage Grade, Industrial Grade, Oral Care Grade), By Source (Corn-Based, Wheat-Based, Cassava-Based, Sugarcane-Based), By Application (Food & Confectionery, Pharmaceuticals, Personal Care, Chemical & Industrial)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Roquette Frères, Cargill Incorporated, Archer Daniels Midland Company, Ingredion Incorporated, Tereos S.A., SPI Pharma Inc., Gulshan Polyols Ltd., Sunar Misir, Sukhjit Starch & Chemicals Ltd., Kasyap Sweeteners Ltd., Shandong Lianmeng Chemical Group, Baisheng Chemical Co. Ltd., PT Sorini Agro Asia Corporindo Tbk, Merck KGaA, Sayaji Industries Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sorbitol Market Segmentation

By Product Form

- Liquid Sorbitol

- Crystalline Sorbitol

By Purity & Grade

- Pharmaceutical Grade

- Food & Beverage Grade

- Industrial Grade

- Oral Care Grade

By Source

- Corn-Based

- Wheat-Based

- Cassava-Based

- Sugarcane-Based

By Application

- Food & Confectionery

- Pharmaceuticals

- Personal Care

- Chemical & Industrial

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Sorbitol Industry

- Roquette Frères

- Cargill Incorporated

- Archer Daniels Midland Company

- Ingredion Incorporated

- Tereos S.A.

- SPI Pharma Inc.

- Gulshan Polyols Ltd.

- Sunar Misir

- Sukhjit Starch & Chemicals Ltd.

- Kasyap Sweeteners Ltd.

- Shandong Lianmeng Chemical Group

- Baisheng Chemical Co. Ltd.

- PT Sorini Agro Asia Corporindo Tbk

- Merck KGaA

- Sayaji Industries Ltd.

*- List not Exhaustive