Specialty Gas Market Valuation 2025–2034: $3.1 Billion to $6.4 Billion at 8.3% CAGR Driven by Semiconductor Expansion, Helium Security, and Hydrogen Decarbonization

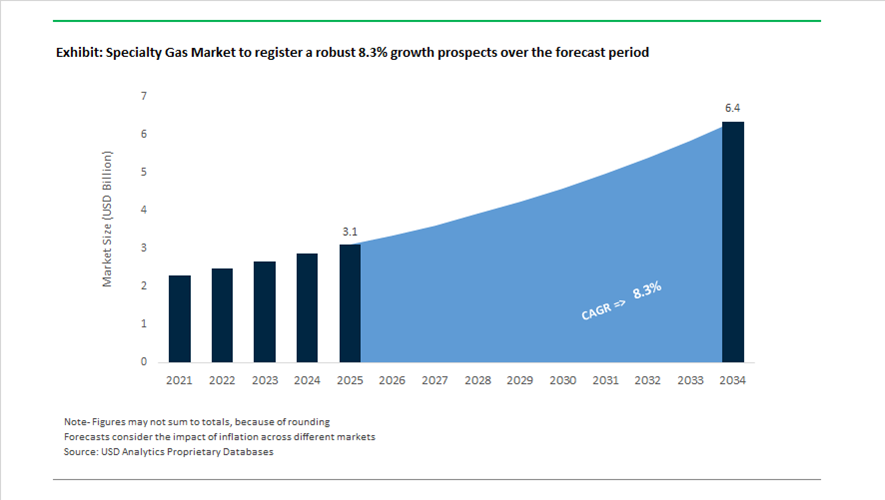

The global specialty gas market is valued at $3.1 billion in 2025 and is projected to reach $6.4 billion by 2034, expanding at a strong CAGR of 8.3%. Growth is being fueled by semiconductor fabrication scaling, electric vehicle power module manufacturing, advanced battery materials processing, MRI imaging demand, hydrogen-based industrial decarbonization, and calibration gas requirements for environmental compliance. Specialty gases such as ultra-high-purity nitrogen, argon, hydrogen, helium, silane, specialty mixtures, and electronic-grade gases are critical for wafer fabrication, plasma etching, chemical vapor deposition, and contamination-sensitive applications. As semiconductor nodes shrink and EV battery gigafactories proliferate, purity thresholds and supply reliability have become decisive competitive factors.

Strategic capital realignment began in September 2024 when Air Products completed the sale of its LNG process technology and equipment business to focus exclusively on core industrial and specialty gas investments, including low-carbon hydrogen and high-purity nitrogen. In November 2024, Messer refinanced €500 million of acquisition debt, strengthening its balance sheet for future specialty gas expansion. In May 2025, Messer inaugurated its new Electronics & Specialty Gases facility in Coolbaugh, Pennsylvania, targeting high-purity gases and specialty blends for semiconductor and healthcare applications. In September 2025, Messer secured a long-term agreement with QatarEnergy for 100 million cubic feet annually of high-purity helium, stabilizing supply for MRI imaging systems and semiconductor manufacturing.

Semiconductor-focused investments accelerated in Asia during 2025. In May 2025, Showa Denko announced a major expansion of its specialty gas production sites in Japan to meet rising demand for advanced semiconductor materials used in EVs and renewable energy modules. In April 2025, Air Products launched an advanced ultra-high-purity gas delivery system with real-time contamination monitoring, designed to enhance yield reliability in next-generation semiconductor fabrication plants. In September 2025, Linde increased its stake in Airtec to over 90%, strengthening specialty gas production and CO2 supply capabilities across the Gulf Cooperation Council region. In November 2025, PetroVietnam Chemical and Messer signed a $37 million joint venture agreement to build an industrial and specialty gas plant in Cai Mep, Vietnam, leveraging LNG regasification cold energy to produce 200,000 tonnes annually, with construction slated to begin in late 2026.

Market consolidation intensified in 2026. In January 2026, Air Liquide completed its €2.85 billion acquisition of South Korea’s DIG Airgas, significantly expanding its footprint in the Asian electronics and battery manufacturing ecosystem. In September 2025, Taiyo Nippon Sanso announced its rebranding to Nippon Sanso Corporation effective April 1, 2026, alongside headquarters relocation to centralize global gas development operations. In late 2025, Taiyo Nippon Sanso successfully demonstrated hydrogen-oxygen combustion technology at an ArcelorMittal steel facility, showcasing specialty gas-enabled decarbonization for high-temperature industrial processes. These acquisitions, helium security agreements, hydrogen combustion milestones, semiconductor gas expansions, and high-purity delivery innovations are defining the specialty gas market’s trajectory toward $6.4 billion by 2034.

Key Trends and High-Impact Opportunities in the Specialty Gas Market

Ultra-High Purity Gas Infrastructure Becomes Mission-Critical for Semiconductor Mega-Fabs

The global transition toward sub-3nm and emerging 2nm semiconductor nodes has elevated specialty gases from a utility input to a mission-critical manufacturing asset. Advanced logic and memory fabrication now require uninterrupted supplies of ultra-high purity nitrogen, argon, and helium, typically at 6N purity or higher, as even trace contaminants can lead to yield loss in Gate-All-Around transistor architectures. This requirement is driving gas majors to accelerate Build-Own-Operate infrastructure models, embedding gas production and purification assets directly within fab boundaries to eliminate contamination risks and logistics dependencies.

In July 2025, Air Liquide announced investments exceeding €250 million to support semiconductor expansion in Europe, specifically targeting next-generation UHP gas systems for advanced nodes. This was followed by an additional €130 million commitment in Singapore in September 2025 to supply high-volume, on-site UHP nitrogen for a major semiconductor manufacturer. These investments reflect a broader industry shift toward capital-intensive, long-duration supply contracts where gas infrastructure is amortized over multi-decade fab lifecycles rather than short-term demand cycles.

The scale of demand is further amplified by TSMC’s March 2025 announcement to expand its U.S. investment footprint to $165 billion, adding three new fabs and two advanced packaging facilities. Each of these mega-fabs requires redundant, on-site specialty gas plants capable of continuous delivery at extreme purity thresholds. As a result, specialty gas supply is increasingly synchronized with semiconductor capital expenditure cycles, reinforcing high entry barriers and long-term revenue visibility for incumbent suppliers.

Non-Substitutable Noble Gas Demand Accelerates with EUV and High-NA Lithography

The semiconductor industry’s migration to Extreme Ultraviolet and emerging High-NA EUV lithography has created a rigid, non-substitutable demand profile for noble gases such as xenon and krypton. These gases are essential for plasma generation, optical path protection, and chamber purging in EUV tools, making demand directly proportional to tool uptime rather than discretionary production volumes. As leading-edge fabs scale EUV deployments, noble gas consumption is becoming structurally embedded in wafer throughput economics.

By mid-2025, Intel was aggressively deploying its 18A node, which relies heavily on EUV lithography. Each EUV scanner requires a continuous flow of ultra-high purity noble gas mixtures, creating a baseline demand that scales with installed tool count. Concurrently, TSMC projected a 60% increase in 3nm production capacity during 2025, directly translating into higher xenon and krypton consumption across its fab network.

Supply chain resilience has therefore become a strategic priority. In December 2024, SK Specialty restructured its ownership by selling an 85% stake in its gas unit to Hahn & Company for approximately 1.86 trillion won. This transaction underscored the premium valuation attached to stable, high-purity noble gas assets and highlighted a market-wide shift toward long-term, direct supply agreements between gas producers and semiconductor manufacturers to mitigate pricing volatility.

Certified Calibration Gases Enable CCUS and Emissions Compliance

The global rollout of carbon capture, utilization, and storage projects and the tightening of carbon accounting frameworks are creating a high-value niche for certified calibration gas mixtures. Regulatory regimes increasingly mandate precise, traceable emissions data, elevating calibration gases from a compliance cost to a regulated revenue stream. Continuous Emissions Monitoring Systems rely on high-accuracy gas mixtures to validate sensor performance, making supplier credibility and certification a critical differentiator.

In December 2025, the European Commission adopted new rules under its voluntary certification framework for carbon removals, requiring harmonized monitoring and reporting standards. These rules depend on calibration gases such as carbon monoxide in nitrogen or carbon dioxide in methane to ensure the integrity of emissions and removal measurements. Suppliers capable of delivering ISO 17025-certified mixtures are therefore positioned at the center of Europe’s emerging carbon credit verification ecosystem.

In the United States, the Environmental Protection Agency approved multiple Class VI permits for large-scale carbon storage projects during 2025, including Occidental Petroleum’s Stratos project. Each injection site requires continuous leak detection and plume monitoring, reinforcing recurring demand for high-precision calibration gases and positioning specialty gas blenders as long-term partners in CCUS infrastructure.

Atmospheric Processing Gases Power the Scale-Up of EV Battery Gigafactories

Beyond electronics, battery manufacturing has emerged as the fastest-growing specialty gas application, driven by the global expansion of lithium-ion and solid-state battery gigafactories. The production of lithium-iron phosphate cathode materials and advanced solid electrolytes requires tightly controlled inert or reducing atmospheres during calcination and sintering, making specialty gas supply integral to material quality and yield.

As highlighted in October 2025, the battery industry is rapidly shifting from nickel-rich chemistries toward LFP for cost stability and safety. LFP synthesis is gas-intensive, requiring high-purity nitrogen or argon atmospheres to prevent oxidation of iron and lithium during high-temperature processing. New gigafactories in the United States and South Korea are also adopting forming gas and argon-oxygen blends to fine-tune cathode crystal structures and electrochemical performance.

In response, Air Liquide announced a $50 million hydrogen supply expansion on the U.S. Gulf Coast in October 2025 to support battery material production clusters. This localized “gas island” model reduces logistics risk and aligns gas supply directly with gigafactory ramp-up schedules, reinforcing specialty gases as a foundational input for next-generation energy storage manufacturing.

Specialty Gas Market Share and Segmentation Insights

Electronic Specialty Gases Dominate the Specialty Gas Market Due to Semiconductor Manufacturing Demand

Electronic specialty gases accounted for 38.60% of the specialty gas market in 2025, making them the largest product category across high-tech industrial applications. These gases include silane, ammonia, tungsten hexafluoride, hydrogen chloride, nitrous oxide, and various organometallic precursor gases, which are essential for semiconductor manufacturing processes such as chemical vapor deposition, plasma etching, doping, and wafer cleaning. Semiconductor fabrication facilities require ultra-high purity gases with tightly controlled specifications to ensure consistent chip performance. A major 2025 industry driver is the ongoing global expansion of semiconductor fabrication capacity, supported by government investment programs and new manufacturing facilities being developed in major semiconductor production regions.

Semiconductor & Electronics Industry Drives Specialty Gas Consumption for Advanced Chip Manufacturing

Semiconductor and electronics represent the largest application segment in the specialty gas market, accounting for 42.80% of total demand in 2025 due to the complex chemical processes involved in integrated circuit manufacturing. Semiconductor fabrication requires numerous specialty gases for etching, deposition, doping, and wafer cleaning processes, with each manufacturing node requiring precise gas chemistries and ultra-high purity standards. As semiconductor technology advances, the number of processing steps continues to increase. A key 2025 industry trend is the growing complexity of advanced semiconductor nodes approaching 3 nanometers and below, where technologies such as atomic layer deposition and extreme ultraviolet lithography require specialized precursor gases and highly controlled gas delivery systems, increasing overall specialty gas consumption per wafer.

Specialty Gas Market Competitive Landscape

The global specialty gas market in 2026 is dominated by ultra-high purity (UHP) gases for semiconductor fabrication, with Tier-1 players scaling on-site generation, EUV lithography support gases, and hydrogen infrastructure. Competition intensifies around electronics-grade purity, long-term supply contracts, and decarbonization-linked gas technologies.

Linde Strengthens Semiconductor Gas Leadership with $5.5 Billion Capex and $10 Billion Project Backlog

Linde plc leads the specialty gas market with 2025 sales of $34 billion and a 29.8% operating margin, supported by a project backlog exceeding $10 billion. Its 2026 capex plan of $5.0–$5.5 billion prioritizes ultra-high purity specialty gases for semiconductor manufacturing. The company’s supply agreements are anchored in long-term sale-of-gas contracts, ensuring stable revenue streams. Strong demand from EUV lithography and advanced node chip fabrication in APAC and the Americas drives growth. Linde’s vertically integrated engineering model enables ownership of production assets, enhancing cost efficiency and supply reliability. Its dominance in electronics gases positions it at the center of next-generation semiconductor ecosystems.

Air Liquide Expands Semiconductor Gas Dominance Through €3 Billion Korea Acquisition and High-Purity Facility Investments

Air Liquide S.A. is accelerating growth in specialty gases through strategic acquisitions and electronics-focused investments. The €3 billion acquisition of DIG Airgas in South Korea strengthens its leadership in semiconductor-grade gases. Expansion in India via NovaAir enhances its presence across automotive, healthcare, and industrial segments. Contracts worth €200 million in Singapore support high-purity gas production for advanced electronics manufacturing. The company’s €4.9 billion investment backlog underpins its margin expansion strategy targeting +100 basis points by 2027. Its focus on ultra-high purity gases and regional capacity expansion strengthens its position in global semiconductor supply chains.

Air Products Scales Hydrogen and Aerospace Gas Supply with Strong Earnings Growth and NASA Contracts

Air Products and Chemicals, Inc. is leveraging specialty gas expertise to expand into hydrogen and energy transition markets. The company reported a 14% increase in operating income to $735 million in early FY2026, driven by strong pricing and business mix. Its $140 million NASA contracts highlight leadership in high-purity liquid hydrogen supply for aerospace applications. Strategic collaboration with Yara targets low-emission ammonia production, integrating specialty gas processing with global distribution. Despite helium supply challenges, Air Products maintains strong EPS guidance of $12.85–$13.15. Its focus on hydrogen, ammonia, and process gases positions it at the intersection of clean energy and specialty gas demand.

Nippon Sanso Accelerates Semiconductor Gas Innovation with Tsukuba R&D Hub and Global Brand Unification

Nippon Sanso Holdings is strengthening its specialty gas portfolio through global rebranding and semiconductor-focused R&D. The transition to a unified corporate identity enhances global recognition and operational alignment. Its Advanced Electronics Materials Development Building in Tsukuba drives innovation in specialty gases for next-generation semiconductors. The company demonstrated oxygen-enriched combustion technology achieving 24.1% CO2 reduction, supporting industrial decarbonization. Its leadership in MOCVD equipment and precursor gases enables critical contributions to compound semiconductor and LED manufacturing. The company’s integrated approach to advanced materials and gas technologies reinforces its competitiveness in electronics applications.

Messer Expands Electronics Gas Infrastructure and Industrial Efficiency with AMOLED Projects and OXYBOOST Technology

Messer Group is expanding its specialty gas footprint through targeted investments in electronics and industrial applications. Its RMB 250 million project with BOE supports AMOLED production, strengthening its position in Asia’s display manufacturing ecosystem. The launch of Nitric Acid OXYBOOST technology improves plant throughput by over 10% while reducing NOx emissions by up to 30%. Expansion of its Pennsylvania facility enhances supply capacity for high-purity gases in the U.S. technology sector. Messer’s joint ventures in China enable end-to-end management of gas systems, from construction to operations. Its focus on operational efficiency and electronics-grade gases supports sustained growth.

Resonac Strengthens Semiconductor Materials Leadership with Advanced Etching Gases and 20.7% EBITDA Margin

Resonac Holdings Corporation is reinforcing its position in specialty gases through a strong focus on semiconductor materials and advanced packaging. The company achieved a 20.7% EBITDA margin in 2025, driven by robust demand for electronics materials. Its leadership in the JOINT3 consortium supports development of next-generation semiconductor packaging technologies. Increased R&D investment targets specialty etching gases and materials for AI-driven chip manufacturing. Government-backed hydrogen co-firing initiatives support its long-term carbon neutrality goals. Resonac’s integration of specialty gases with semiconductor materials positions it as a key player in advanced electronics value chains.

South Korea Specialty Gas Market: €3 Billion Air Liquide Acquisition and AI-Driven Semiconductor Gas Demand Surge

South Korea has firmly established itself as a Tier 1 global hub for specialty gases, driven by semiconductor dominance, strategic acquisitions, and government-backed technology investments. The €3 billion acquisition of DIG Airgas by Air Liquide (January 2026) marks a transformative consolidation, creating a combined entity with ~€900 million in annual sales focused on logic and memory chip manufacturing. This positions South Korea at the forefront of the ultra-high purity (UHP) specialty gas market, particularly for advanced semiconductor fabrication processes below 2nm nodes.

Government support remains a critical growth lever, with the Ministry of Science and ICT allocating 8.6 trillion won ($5.77 billion) in 2026 to strengthen semiconductor material sovereignty, including molybdenum-based precursors and next-generation etching gases. Companies like SK Specialty are accelerating their shift toward high-value gases such as monosilane (SiH₄) and nitrogen trifluoride (NF₃), integrating AI-driven purification systems to meet zero-defect manufacturing standards. The rapid rise of AI chips and High Bandwidth Memory (HBM) is further fueling demand for ultra-pure cleaning and etching gases, reinforcing South Korea’s leadership in high-performance semiconductor specialty gas applications.

China Specialty Gas Market: Electrification, Localization Strategy, and Photovoltaic-Grade Gas Expansion

China’s specialty gas market is undergoing rapid transformation through localization, electrification of gas production, and large-scale infrastructure investments, aimed at reducing reliance on imports and ensuring supply chain resilience. Air Liquide’s electrified specialty gas production project in Shaanxi (2026) reflects China’s dual focus on decarbonization and industrial self-sufficiency, aligning with national mandates for low-carbon chemical manufacturing.

Strategic partnerships are accelerating capacity expansion, with Linde’s supply agreement with CNOOC and Shell Petrochemicals (CSPC) enabling the construction of air separation units in Huizhou Daya Bay, supporting the South China electronics and semiconductor corridor. Additional investments such as Linde’s RMB 165 million specialty gas hub in Suzhou are strengthening supply to high-tech manufacturing clusters in the Yangtze River Delta. China is also aggressively scaling photovoltaic-grade specialty gases, including high-purity silane and phosphine, to support next-generation N-type solar cell production. Regulatory initiatives like CIGIE 2026 in Wuxi are further promoting standardization of gas purity levels and high-quality industry development, cementing China’s role as a global leader in specialty gas production and consumption.

Japan Specialty Gas Market: Green Transformation (GX), Carbon Pricing, and Low-Carbon Gas Innovation

Japan is leading the evolution of the specialty gas market toward decarbonization and high-value innovation, underpinned by its Green Transformation (GX) strategy and strong policy framework. The global rebranding of Nippon Sanso Holdings (effective April 2026) unifies operations across 30 countries, enhancing R&D collaboration in ultra-high purity (UHP) gases and specialty gas technologies. The company’s NS Vision 2026 strategy targets revenues approaching ¥1 trillion, with a focus on carbon-neutral gas production and advanced industrial applications.

Policy-driven transformation is evident with the introduction of a carbon pricing corridor (JPY 1,700–4,300/tonne CO₂) by METI, mandating participation in emissions trading for large gas producers starting fiscal 2026. This is accelerating investment in low-carbon specialty gas synthesis and hydrogen-based production systems. Japan’s issuance of ¥20 trillion in GX Economy Transition Bonds is further supporting companies like Sumitomo Chemical and Tokyo Gas in developing next-generation specialty gases for low-emission manufacturing. Technological innovation is also expanding into emerging applications, such as cryogenic cooling gases for superconducting power cables, with projects like SupraMarine highlighting Japan’s leadership in advanced energy infrastructure and specialty gas integration.

United States Specialty Gas Market: Semiconductor Reshoring, NASA Contracts, and Cyber-Resilient Gas Infrastructure

The United States specialty gas market is being reshaped by semiconductor reshoring, aerospace demand, and advanced infrastructure investments, positioning the country as a key player in high-purity gas production and distribution. A notable development is Air Products securing over $140 million in NASA contracts (2026) to supply liquid hydrogen and specialty atmospheric gases to Kennedy Space Center and Cape Canaveral, reinforcing demand in the aerospace and defense sectors.

The SEMI U.S. Policy Strategy (2026) is advocating for regulatory harmonization and synchronized export controls, ensuring competitiveness of U.S. specialty gas firms while safeguarding national security interests. Investments such as Air Liquide’s $50 million expansion in the Gulf Coast are strengthening infrastructure for hydrogen and refinery-grade specialty gases. Additionally, the industry is advancing in digital and operational resilience, with Air Products Membrane Solutions achieving cybersecurity certifications (IACS E26/E27) for maritime gas systems, setting new standards for secure gas delivery networks. Adoption of UL Environmental Claim Validation (ECV) is also increasing, reflecting a shift toward energy-efficient and environmentally compliant gas purification processes, aligning with evolving 2026 sustainability benchmarks.

India Specialty Gas Market: Merchant Gas Expansion, Electronics Manufacturing Push, and Healthcare Gas Modernization

India is emerging as the fastest-growing specialty gas market globally, driven by industrial expansion, electronics manufacturing growth, and strategic acquisitions. The acquisition of NovaAir by Air Liquide (October 2025) significantly strengthens its footprint across South and East India, enabling deeper penetration into automotive, electronics, and semiconductor supply chains. This expansion aligns with the rapid growth of electronics manufacturing hubs, particularly those supporting Apple and Samsung supply chains, boosting demand for high-purity specialty gases used in assembly, testing, and fabrication processes.

Domestic players are also scaling aggressively, with companies like Shivtek Spechemi Industries targeting ₹5,000 crore revenue by 2030, supported by new specialty gas capacity expansions scheduled for 2026. Government-backed PLI schemes for electronics and semiconductors are creating a strong demand pull, encouraging the development of on-site gas generation plants at OSAT facilities, enhancing supply chain efficiency and cost optimization. Additionally, India is witnessing increased adoption of medical-grade specialty gases, supported by EPC-driven modernization of healthcare gas infrastructure, positioning the country as a key growth engine in both industrial and healthcare specialty gas segments.

Specialty Gas Market Report Scope

Specialty Gas Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.1 Billion

|

|

Market Size (2034)

|

$6.4 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Product Type (Electronic Specialty Gases, High-Purity Industrial Gases, Rare and Noble Gases, Calibration and Laboratory Gases, Medical Specialty Gases, Carbon Gases, Halogen Gases), By Application (Semiconductor and Electronics, Healthcare and Life Sciences, Energy and Environment, Manufacturing and Metallurgy, Aerospace and Defense, Chemicals and Petrochemicals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Linde plc, Air Liquide S.A., Air Products and Chemicals, Inc., Nippon Sanso Holdings Corporation, Messer Group GmbH, Resonac Holdings Corporation, Iwatani Corporation, Air Water Inc., SOL Group, Matheson Tri-Gas, Inc., Electronic Fluorocarbons, SK Specialty, Peric Special Gas Co., Ltd., Advanced Specialty Gases

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Gas Market Segmentation

By Product Type

- Electronic Specialty Gases

- High-Purity Industrial Gases

- Rare and Noble Gases

- Calibration and Laboratory Gases

- Medical Specialty Gases

- Carbon Gases

- Halogen Gases

By Application

- Semiconductor and Electronics

- Healthcare and Life Sciences

- Energy and Environment

- Manufacturing and Metallurgy

- Aerospace and Defense

- Chemicals and Petrochemicals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Gas Industry

- Linde plc

- Air Liquide S.A.

- Air Products and Chemicals, Inc.

- Nippon Sanso Holdings Corporation

- Messer Group GmbH

- Resonac Holdings Corporation

- Iwatani Corporation

- Air Water Inc.

- SOL Group

- Matheson Tri-Gas, Inc.

- Electronic Fluorocarbons

- SK Specialty

- Peric Special Gas Co., Ltd.

- Advanced Specialty Gases

*- List not Exhaustive