Specialty Paper Market Valuation 2025–2034: $31.4 Billion to $43.5 Billion at 3.7% CAGR Driven by Sustainable Packaging, Filtration Media, and Decorative Laminates

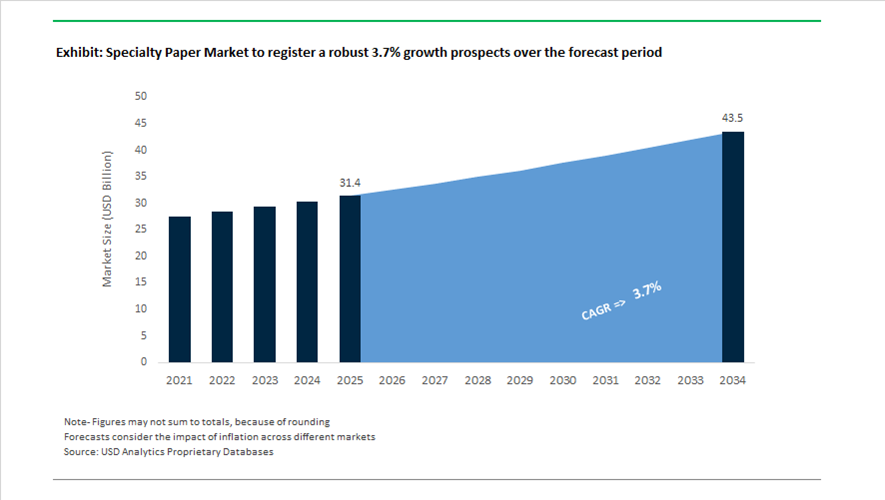

The global specialty paper market is valued at $31.4 billion in 2025 and is projected to reach $43.5 billion by 2034, expanding at a CAGR of 3.7%. Growth is supported by rising demand for pressure-sensitive label papers, release liners, decorative laminates, food-grade parchment, filtration media, abrasive backings, flexible packaging substrates, and high-performance industrial papers. Specialty paper manufacturers are reallocating capital from declining graphic paper segments toward high-margin, application-specific grades aligned with circular economy mandates, plastic substitution strategies, and advanced filtration standards. Demand momentum is strongest in sustainable packaging solutions, PSA label liners, synthetic filter materials, and decorative laminate backings for furniture and construction.

Strategic consolidation began in early 2024 when Munksjö completed the acquisition of Ahlstrom’s abrasive paper business, reinforcing its leadership in specialty backing papers for industrial and automotive sectors. In November 2024, Ahlstrom expanded into life sciences filtration by acquiring ErtelAlsop, strengthening its depth filtration media portfolio for pharmaceutical and biotechnology applications. In the first quarter of 2025, Munksjö’s 175 million reais ExpanDecor project in Caieiras, Brazil modernized and converted the PM7 machine, doubling production capacity for decorative and laminate papers. In April 2025, Koehler Paper received the French PAP’AWARD for NexPlus® Seal Pure, a 100% paper-based packaging solution that replaces plastic windows with linen mesh in organic walnut bags.

Capacity expansion and packaging innovation accelerated through 2025. In May 2025, Ahlstrom finalized the acquisition of the Stevens Point specialty paper facility in Wisconsin, significantly expanding its North American footprint for pressure-sensitive adhesive labels and flexible packaging papers. In May 2025, Ahlstrom also inaugurated a new parchmentizer at its Saint-Séverin plant in France, enhancing output of sustainable parchment papers for food and industrial uses. In September 2025, Mondi introduced white digital printing capability for brown corrugated packaging, enabling high-contrast branding on recycled substrates without requiring laminated white top layers. In December 2025, Ahlstrom announced the extension of its advanced synthetic filter manufacturing operations in the U.S., targeting increased demand from HVAC and industrial filtration markets.

Structural repositioning intensified heading into 2026. In December 2025, Sappi and UPM signed a non-binding letter of intent to form a 50/50 joint venture combining their European graphic paper businesses, freeing both companies to redirect capital toward specialty paper and biorefining investments, with closing anticipated by late 2026. JK Paper is constructing a 125,000 ADMT Bleached Chemi-Thermomechanical Pulp mill at its Gujarat unit, expected to be commissioned in the second half of 2025–26, strengthening raw material integration for specialty paper grades in India. In February 2026, Ahlstrom launched Acti-V® RRF Natural recyclable release liners designed for standard paper recycling streams, reinforcing circular packaging strategies. These investments in filtration media, decorative laminates, recyclable liners, digital printing capabilities, and pulp integration are shaping the specialty paper market trajectory through 2034.

Key Trends and Opportunity Landscape in the Specialty Paper Market

PFAS-Free Regulatory Mandates Accelerating Circular Barrier Paper Adoption

The Specialty Paper Market is undergoing a structural transformation as regulatory pressure eliminates fluorochemical-based performance shortcuts in food-contact applications. The EU Packaging and Packaging Waste Regulation has formalized a ban on intentionally added PFAS in food packaging from August 2026, while U.S. regulatory actions confirmed in early 2025 have removed grease-proofing PFAS from the food-contact supply chain. These developments have turned PFAS-free compliance from a sustainability preference into a non-negotiable market entry requirement.

As a result, brand owners are reengineering global packaging strategies around fiber-based, recyclable barrier papers. Major QSR operators such as McDonald’s and Starbucks have committed to eliminating PFAS across their global packaging portfolios by late 2025. This has triggered a surge in demand for aqueous dispersion coatings, starch-based barriers, and bio-polymer technologies that preserve grease resistance while remaining repulpable within existing recycling streams.

Manufacturers are responding with capacity-led repositioning. Ahlstrom completed the acquisition of its Stevens Point, Wisconsin operations hub in May 2025 to accelerate scale-up of specialty food packaging materials. This investment reflects a broader industry shift away from polyethylene-lined and fluorochemical-treated papers toward mono-material, circular barrier papers that satisfy both regulatory scrutiny and brand-level ESG scorecards.

Decentralized Diagnostics Driving Demand for High-Purity Specialty Substrates

Healthcare decentralization has emerged as a durable growth driver for specialty paper beyond pandemic-era demand. Point-of-Care diagnostics and home testing are now embedded within mainstream healthcare delivery models, elevating the importance of high-precision paper substrates such as nitrocellulose membranes and absorbent wicking layers. These materials must deliver tightly controlled capillary flow behavior to ensure diagnostic accuracy across large-scale test kit production.

From a technical standpoint, modern lateral flow assays require flow rate tolerances within plus or minus ten% to avoid signal distortion and false readings. By December 2025, demand for these substrates expanded alongside rapid growth in at-home testing for infectious diseases, cardiac markers, and chronic condition monitoring. This has repositioned specialty paper as a critical input into regulated medical supply chains rather than a commodity filtration medium.

Strategic consolidation is reinforcing this trend. Ahlstrom expanded its life sciences footprint through the acquisition of ErtelAlsop in late 2024, integrating depth filtration expertise directly into its diagnostic paper platform. This capability supports the development of ultra-clean, molecularly consistent substrates required for next-generation diagnostics, where reproducibility and regulatory traceability are as important as throughput.

Industrial Digital Printing Substrates for Direct-to-Shape Manufacturing

Digital printing has evolved from a branding tool into a core industrial production technology, opening a high-margin opportunity for specialty paper engineered for automated manufacturing environments. Direct-to-Shape and Direct-to-Film printing processes require heavy-weight, dimensionally stable papers that can tolerate UV curing, thermal stress, and high-speed inkjet deposition without deformation or ink migration.

Industrial printhead platforms from suppliers such as Fujifilm Dimatix and Kyocera now operate at firing frequencies above 30,000 droplets per second. At these speeds, substrate surface energy and porosity control become decisive performance variables. Specialty paper producers that can engineer controlled absorption profiles while maintaining mechanical integrity are capturing demand from electronics overlays, membrane switches, and industrial labeling applications.

Customization economics further reinforce this opportunity. In 2025, Canon highlighted the rapid expansion of digital manufacturing workflows that enable short production runs and rapid prototyping. This shift creates recurring demand for premium specialty paper backings that function as structural components rather than disposable print media.

Fiber-Based High-Barrier Solutions for Premium Secondary Packaging

Luxury and premium consumer brands are redefining secondary packaging expectations by combining plastic-free material mandates with elevated tactile and aesthetic standards. This has created a strong opportunity for dense barrier paperboard and molded fiber solutions that replicate the stiffness, smoothness, and protective qualities of plastics while remaining fully recyclable.

Lifecycle performance is a key differentiator in this segment. In December 2025, Metsä Board published a verified Life Cycle Assessment demonstrating that its paperboard trays can deliver up to 91% lower carbon emissions compared with fossil-based polypropylene trays under full incineration scenarios. These quantified environmental advantages are increasingly used by premium brands to substantiate sustainability claims at the point of sale.

Adoption signals are already visible. Brands such as SALT! Supplements have selected MetsäBoard Pro FBB Bright for premium sachet packaging, citing its stiffness-to-weight efficiency and premium hand-feel. This underscores a broader market shift where specialty paper value is defined not only by barrier performance, but by its role in delivering a high-quality unboxing experience that aligns sustainability with brand perception.

Specialty Paper Market Share and Segmentation Insights

Packaging Papers Lead the Specialty Paper Market as Sustainable Packaging Adoption Accelerates

Packaging papers accounted for 34.80% of the specialty paper market in 2025, making them the leading product category across high-performance paper applications. These papers are engineered to provide enhanced barrier properties, mechanical strength, and printability, supporting uses such as flexible packaging, protective industrial wraps, and premium product packaging. Growth is strongly linked to expanding e-commerce logistics and brand-driven packaging innovation. A major 2025 market trend is the increasing replacement of plastic packaging with paper-based alternatives, where specialty packaging papers are designed with moisture barriers, wet strength, and heat-sealable coatings to meet functional performance requirements previously dominated by plastic materials.

Packaging and Labeling Applications Drive Global Specialty Paper Demand

Packaging and labeling represent the largest application segment in the specialty paper market, accounting for 48.60% of global demand in 2025 due to the widespread use of specialty papers in labels, flexible packaging, folding cartons, and brand packaging materials. These applications require papers with excellent printability, adhesion compatibility, die-cutting performance, and barrier functionality. The rapid growth of e-commerce packaging and premium retail branding continues to support demand for high-quality specialty paper grades. A key 2025 industry development is the evolution of sustainable labeling technologies, including recyclable release liners, compostable adhesive systems, and papers sourced from certified sustainable forestry, enabling improved packaging recyclability while maintaining the functional performance required for product labeling and brand identification.

Specialty Paper Market Competitive Landscape

The global specialty paper market in 2026 is driven by bio-based barrier coatings, nanocellulose technologies, and recyclable fiber solutions replacing plastics. Leading players are scaling high-performance packaging papers, optimizing circular supply chains, and integrating advanced fiber engineering to meet food safety, e-commerce, and sustainability mandates.

International Paper Restructures into Dual Packaging Entities to Accelerate $3.7 Billion EBITDA Specialty Packaging Growth

International Paper is transforming into a high-value specialty packaging leader through structural reorganization and portfolio optimization. The planned 2026 split into two regional packaging companies enhances operational focus across North America and EMEA. Divestment of its Global Cellulose Fibers unit redirects capital toward specialty packaging solutions. The integration of DS Smith strengthens its footprint in e-commerce and food-service packaging across Europe. The company reported $23.6 billion in 2025 sales with EBITDA of $2.98 billion, targeting up to $3.7 billion in 2026. Its 80/20 commercial excellence model supports margin expansion in specialty fiber-based packaging.

Mondi Leads Functional Barrier Paper Innovation with Plastic-Equivalent Performance and 88% Sustainable Revenue Mix

Mondi Group is advancing specialty paper innovation through high-performance barrier coatings and circular design principles. Its FunctionalBarrier Paper Ultimate delivers oxygen and moisture resistance comparable to plastic, targeting food and instant packaging applications. The company secured nine WorldStar Packaging Awards in 2026, reinforcing its leadership in sustainable packaging innovation. Mondi reported that 88% of revenue comes from recyclable or compostable products, alongside a 48% reduction in emissions from 2019 levels. Ongoing ramp-up of specialty kraft paper lines supports growth in e-commerce and construction sectors. Its lifecycle assessment tools ensure compliance with FSC and PEFC certifications.

Sappi Expands High-Barrier Specialty Paper Portfolio with Heat-Sealable Packaging Solutions and Strategic JV Optimization

Sappi Limited is accelerating its transition toward specialty packaging and biomaterials under its Thrive strategy. The planned JV with UPM reduces exposure to graphic paper and reallocates capital to high-growth specialty segments. Its Guard Pro OMH and OHS papers provide advanced grease resistance and heat-sealability for food packaging applications. The company is scaling barrier paper production compatible with existing Form-Fill-Seal systems, enabling cost-efficient adoption. Valuation of its European graphic assets at €320 million reflects strategic portfolio monetization. Sappi’s focus on scalable innovation strengthens its position in functional packaging materials.

Stora Enso Strengthens Renewable Packaging Focus with Forest Asset Separation and High-Tech Consumer Board Expansion

Stora Enso is positioning itself as a pure-play renewable materials company through strategic divestments and capacity expansion. The planned separation of Swedish forest assets enhances focus on specialty packaging and biomaterials. The company achieved a 61% reduction in emissions, surpassing long-term sustainability targets ahead of schedule. Expansion of its Oulu consumer board facility supports premium food packaging demand. A new reporting structure aligns specialty paper innovation with targeted end-user segments. Its emphasis on renewable fiber solutions strengthens competitiveness in sustainable packaging markets.

Ahlstrom Advances Recyclable Specialty Materials with 16.1% EBITDA Margin and Next-Generation Release Liner Innovation

Ahlstrom Oyj is strengthening its specialty paper leadership through high-performance fiber-based materials and sustainable innovation. The company achieved a 16.1% EBITDA margin in 2025, driven by pricing discipline and portfolio optimization. Its Acti-V® RRF Natural release liner offers full recyclability within paper streams, addressing adhesive industry waste challenges. Strategic right-sizing of U.S. operations supports investment in advanced paper machine technologies. Approximately 33% of revenue is derived from new innovative products. Its "Safe and Sustainable by Design" framework aligns product development with circular economy standards.

Nippon Paper Expands Nanocellulose and Biomass-Based Specialty Paper Applications with CNF Integration and Capacity Growth

Nippon Paper Industries is transforming into a biomass-based materials leader through advanced cellulose technologies. Its large-scale production of cellulose nanofibers supports applications in food packaging, cosmetics, and functional coatings. The company targets ¥500 billion in revenue from daily-life products by 2026, driven by packaging and healthcare paper demand. Expansion through its Opal subsidiary strengthens presence in international packaging markets. Investment in high-efficiency paper machines enhances production capacity and cost efficiency. Its genomic selection technology improves biomass yield, supporting sustainable feedstock supply for specialty paper manufacturing.

United States Specialty Paper Market Repositioning Toward Packaging, Security, and PFAS-Free Performance

The United States specialty paper industry is undergoing a structural reallocation away from legacy graphic grades toward high-value packaging and functional papers. In early 2025, Sappi North America completed the conversion of Paper Machine No. 2 at its Somerset Mill in Maine, removing roughly 470 million pounds of coated freesheet capacity and redirecting output toward solid bleached sulfate specialty packaging. This move reflects a broader industry trend where domestic mills are prioritizing SBS, food-service boards, and premium folding carton substrates aligned with brand owners’ sustainability and sourcing requirements.

Supply chain localization has further strengthened U.S. operating rates. Following April 2025 tariffs of 20% to 37% on select imported paper grades, domestic mills reported utilization rates exceeding 90%, as converters shifted to tariff-exempt local specialty papers. At the same time, Ahlstrom expanded U.S. release liner capacity through its May 2025 acquisition of the Stevens Point, Wisconsin facility, reinforcing domestic supply for pressure-sensitive adhesive liners used in e-commerce and logistics. Regulatory forces are also shaping product design. State-level PFAS bans in California and New York have accelerated the adoption of aqueous grease-resistant coatings, while updates to the USDA BioPreferred Program in 2025 are channeling federal procurement toward compostable, fiber-based specialty packaging. Parallel innovation is visible in security papers, where the Bureau of Engraving and Printing has driven private-sector development of polymer-paper hybrid substrates for next-generation counterfeit deterrence.

China Specialty Paper Market Balancing Recycling Controls and Technical Paper Scale-Up

China’s specialty paper industry is increasingly shaped by tighter feedstock regulation and rapid scaling of technical grades. In October 2025, the General Administration of Customs implemented stricter recycled pulp import rules, requiring disclosure of dry versus wet processing. This policy effectively filters out low-grade waste pulp, favoring high-purity inputs suitable for specialty and technical papers. As a result, domestic mills with integrated recycling and purification capabilities are gaining a competitive edge.

Downstream, specialty paper investment is closely aligned with national industrial priorities. To support the semiconductor and power equipment ecosystem, mills in Zhejiang have scaled production of ultra-low-ion battery separator papers and transformer insulation grades since late 2024. Packaging regulation is another major catalyst. Under the Ministry of Industry and Information Technology 2025 roadmap, 85% of e-commerce packaging in tier-1 cities must be recyclable, triggering capital deployment into water-resistant kraft and specialty fluting. Innovation in aqueous barrier technologies has followed, with players such as Nine Dragons Paper introducing nano-mineral coatings in mid-2025 that deliver moisture resistance while maintaining repulpability, a key differentiator under circular packaging mandates.

Germany Specialty Paper Market Anchored in Barrier Coatings and Asset Optimization

Germany remains a central innovation hub for high-barrier and functional specialty papers, while also rationalizing legacy assets. In December 2025, Sappi and UPM announced a non-binding plan to form a 50/50 joint venture for graphic and specialty paper assets, valued at approximately €1.42 billion. The proposed structure aims to optimize machine utilization across Europe by late 2026, reflecting a disciplined approach to capacity management.

At the innovation frontier, Germany is accelerating alternatives to plastic-coated papers. In 2025, Darmstadt-based CeraSleeve brought industrial-scale silica-based paper additives online, enabling plastic-free, food-grade specialty papers. Functional applications are also expanding. Ahlstrom commissioned a new advanced molecular filtration unit in Turin serving the DACH region in June 2025, targeting cleanroom and precision air purification markets. Meanwhile, Mondi and Sappi showcased home-compostable barrier papers at FACHPACK 2025, underscoring Germany’s leadership in compliant fiber-based food packaging.

India Specialty Paper Market Scaling Aseptic, Tissue, and Fiber-Based Substitutes

India’s specialty paper sector is transitioning from fragmented capacity to integrated, high-value production. A major milestone was reached in late 2025 when SIG completed Phase 1 of its ₹880 crore investment in Ahmedabad, establishing the country’s first large-scale aseptic carton packaging facility to serve dairy and juice processors. This development significantly reduces reliance on imported carton stock and supports food security objectives.

Modernization is also evident upstream. Andhra Paper Ltd. partnered with Valmet in late 2024 to install a new tissue and specialty line in Andhra Pradesh, targeting 100 tons per day by early 2026. Capital inflows reinforce this trend. Data from the Department for Promotion of Industry and Internal Trade shows cumulative FDI of ₹10,159 crore through March 2025, largely directed toward high-value specialty grades. Complementing production, Sappi Limited launched an innovation center in India in August 2025 focused on fiber-based alternatives to single-use plastics, positioning the country as a regional development hub rather than only a manufacturing base.

Poland Specialty Paper Market Emerging as a High-Barrier and E-Commerce Production Base

Poland has emerged as a strategic production hub for specialty papers serving European packaging and logistics markets. In August 2025, Mondi expanded output of FunctionalBarrier Paper Ultimate at its Solec plant following a €16 million investment, achieving oxygen transmission rates below 0.5 cm³/m²/day. This positions Poland as a key supplier of high-barrier papers for food packaging requiring extended shelf life without plastic layers.

The country’s role in e-commerce logistics is also expanding. Polish mills have invested heavily in fanfold paper, tamper-evident label stock, and specialty liner grades. Facilities such as Świecie completed machine upgrades in late 2024, adding 55,000 tonnes of capacity dedicated to logistics and labeling applications. These investments align Poland closely with pan-European supply chains seeking cost-efficient, high-performance specialty paper sources.

Comparative Snapshot: Specialty Paper Industry by Country

Specialty Paper Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Developments

|

Competitive Position

|

|

United States

|

Packaging, release liners, PFAS-free papers

|

SBS conversions, tariffs, BioPreferred procurement

|

High-value domestic substitution

|

|

China

|

Technical papers and recyclable packaging

|

Recycled pulp controls, nano-mineral coatings

|

Scale with regulatory leverage

|

|

Germany

|

Barrier innovation and asset optimization

|

Plastic-free coatings, JV rationalization

|

Premium functional leader

|

|

India

|

Aseptic cartons and tissue modernization

|

SIG investment, FDI inflows

|

High-growth regional hub

|

|

Poland

|

High-barrier and logistics papers

|

FunctionalBarrier expansion, e-commerce grades

|

Cost-efficient EU supplier

|

Specialty Paper Market Report Scope

Specialty Paper Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$31.4 Billion

|

|

Market Size (2034)

|

$43.5 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Product Type (Label and Release Papers, Packaging Papers, Technical and Industrial Papers, Décor Papers, Printing and Writing Specialty Papers, Food Service Papers), By Raw Material (Wood Pulp, Non-Wood Fibers, Additives and Coatings), By Application (Packaging and Labeling, Industrial Use, Commercial and Retail, Banking and Government)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sappi Limited, Mondi Group, Ahlstrom, UPM-Kymmene Corporation, Stora Enso Oyj, Nippon Paper Industries Co., Ltd., Oji Holdings Corporation, International Paper Company, ITC Limited, Fedrigoni S.p.A., Koehler Group, Burgo Group S.p.A., JK Paper Ltd., Delfort Group, Felix Schoeller Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Paper Market Segmentation

By Product Type

- Label and Release Papers

- Packaging Papers

- Technical and Industrial Papers

- Décor Papers

- Printing and Writing Specialty Papers

- Food Service Papers

By Raw Material

- Wood Pulp

- Non-Wood Fibers

- Additives and Coatings

By Application

- Packaging and Labeling

- Industrial Use

- Commercial and Retail

- Banking and Government

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Paper Industry

- Sappi Limited

- Mondi Group

- Ahlstrom

- UPM-Kymmene Corporation

- Stora Enso Oyj

- Nippon Paper Industries Co., Ltd.

- Oji Holdings Corporation

- International Paper Company

- ITC Limited

- Fedrigoni S.p.A.

- Koehler Group

- Burgo Group S.p.A.

- JK Paper Ltd.

- Delfort Group

- Felix Schoeller Group

*- List not Exhaustive