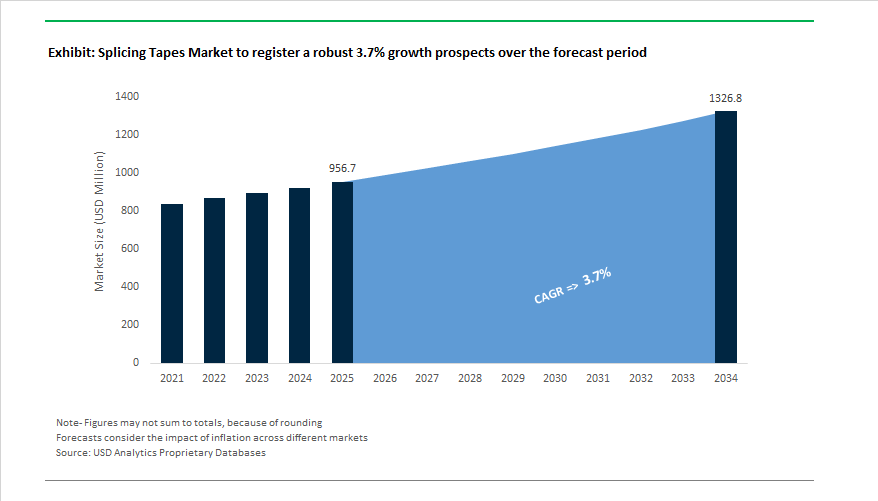

The Global Splicing Tapes Market is projected to grow from $956.7 million in 2025 to $1,326.7 million by 2034, at a CAGR of 3.7%. The steady expansion is being fueled by technological advancements in high-speed production systems, repulpable adhesive formulations, and precision-engineered thin-film splicing solutions. Demand is rising sharply across paper manufacturing, flexible packaging, electronics lamination, and film converting industries, where continuous production uptime and adhesive reliability directly determine profitability and yield.

Professionals in the paper and packaging sectors increasingly prefer TAPPI UM-213-A certified repulpable splicing tapes, which ensure clean dissolution during the recycling process, meeting stringent sustainability mandates across Europe and North America. In the film and extrusion industries, high-performance splicing tapes with thermal resistance up to 200°C are essential to secure high-strength splices in lamination, coating, and extrusion lines. Additionally, the introduction of modified acrylic and silicone-based adhesive systems enables strong adhesion to low surface energy (LSE) materials like silicone liners and polymer films—crucial for nonwoven and specialty coating operations.

The market’s growth is also driven by the rapid adoption of automation in web handling systems and AI-based adhesive coating control in modern converting facilities. Splicing tapes are increasingly replacing mechanical joints and manual overlap methods to eliminate downtime and improve production efficiency in continuous web processes for printing, electronics, and flexible packaging.

The Splicing Tapes Market continues to evolve through strategic innovation, portfolio expansion, and sustainability integration across key industrial sectors. Recent market developments reflect strong momentum in renewable energy applications, operational excellence initiatives, and circular manufacturing.

In April 2025, Avery Dennison Performance Tapes launched a new PSA line for solar panel bonding, marking its entry into the renewable energy assembly adhesives market. The product range offers UV resistance, high peel adhesion, and automation compatibility, supporting large-scale solar module and junction box assembly—showcasing how splicing technology is migrating from traditional web processing to energy infrastructure manufacturing.

Meanwhile, 3M Company finalized its healthcare business spinoff in April 2024, focusing its operational capital toward its Safety and Industrial Group—the division responsible for advanced splicing tapes and industrial adhesives. By May 2025, 3M’s CEO confirmed the rollout of the ‘3M eXcellence’ operational model, aimed at increasing on-time and in-full delivery performance to 90%, underscoring the company’s commitment to operational reliability in high-demand industrial supply chains.

In February 2024, Avery Dennison expanded its appliance-grade PSA portfolio, designed for high-durability bonding and noise/vibration/harshness (NVH) damping—an indication of the company’s strategy to diversify its adhesive technology platforms into cross-sectoral applications beyond printing and packaging.

Sustainability remains a dominant industry theme. Tesa SE advanced its Debonding on Demand technology throughout 2024, an innovation allowing controlled de-adhesion for easy component recycling—critical for circular economy compliance in electronics and packaging. Parallelly, ORAFOL Europe GmbH introduced the ORAFLEX® 1250QS Quick Splice tape (September 2024), specifically optimized for high-speed paper mills, achieving instant bonding while guaranteeing full repulpability—a breakthrough in reducing roll change time and waste.

On the manufacturing front, 3M announced consolidation plans (May 2025) to enhance global efficiency, reporting 58% capacity utilization, which will increase production scalability for splicing and industrial tape lines. Avery Dennison, on the sustainability side, introduced rBG Pure Liners (October 2024), featuring recycled and unbleached fibers to minimize carbon footprint—aligning product innovation directly with ESG reporting standards.

Market Trend 1: Adoption of Low-Voltage, Electronically Conductive Splicing Tapes for Lithium-Ion Battery Electrode Manufacturing

The global acceleration of EV battery gigafactory expansions is driving demand for electronically conductive splicing tapes engineered for electrode manufacturing lines. In these settings, precision and electrical reliability are paramount, as splices must maintain conductivity and mechanical integrity under continuous tension and extreme temperatures.

Industry leaders such as tesa and 3M are commercializing electrically conductive adhesive tapes featuring XYZ-axis conductivity and non-woven carbon scrim carriers, ensuring seamless current transfer at the splice interface. The feature is crucial in lithium-ion battery production, where even minor electrical inconsistencies can elevate internal resistance and reduce cycle life.

The rise of high-speed automated flying splice systems is further boosting the adoption of specialized conductive tapes for anode, cathode, and separator webs. By delivering robust adhesion at full machine speeds, these solutions minimize material waste and reduce production downtime in billion-dollar gigafactory operations. Academic studies reinforce the demand, emphasizing that conductive binders and graphene-based adhesive networks directly contribute to lower resistance and enhanced electrode cycling stability—validating the vital role of splicing tapes in optimizing energy density and lifespan.

In addition, as manufacturers transition toward Dry Battery Electrode (DBE) processes—eliminating solvent-based slurries—companies like Henkel are developing thin conductive coatings compatible with both traditional slurry and dry processes. The alignment ensures that conductive splicing tapes can integrate across the next generation of sustainable, solvent-free electrode manufacturing systems.

Market Trend 2: Development of High-Temperature, Carrier-Less Tapes for High-Speed Converting and Packaging

In flexible packaging, label converting, and film lamination, the demand for carrier-less, high-temperature splicing tapes is accelerating. These products are engineered to perform under extreme mechanical and thermal loads, ensuring reliable operation at web speeds exceeding 1000 meters per minute.

Validated field tests from leading converters demonstrate that high-tack flying splice tapes can sustain continuous operations with zero web breaks—a critical achievement for high-throughput packaging lines. These systems enable rapid reel changeovers while ensuring precise adhesion and controlled release, directly enhancing overall equipment efficiency (OEE) in packaging plants.

Film producers increasingly incorporate slip agents such as waxes into BOPP and HDPE substrates, which can compromise traditional tape adhesion. To counter the, manufacturers are innovating new high-tack, wetting-enhanced adhesives capable of bonding even to low-surface-energy materials. Advanced acrylic and silicone chemistries are preferred over rubber-based systems due to their superior UV, oxidation, and high-temperature resistance, which are essential in environments like UV-curing tunnels and hot-air dryers.

The impact of these materials extends beyond mechanical performance. Each failed splice can cause production stoppages of 15 minutes to 2 hours, leading to significant material waste. Thus, high-temperature splicing solutions are being positioned as cost-saving performance products, combining thermal durability, chemical stability, and clean release—attributes indispensable in high-value packaging and converting operations.

Market Opportunity 1: Engineering of Low-Ooze, Precision Tapes for Narrow-Web Digital Printing Applications

The digital label printing revolution is generating strong demand for low-ooze precision splicing tapes tailored for narrow-web operations. As the industry pivots toward short-run, on-demand printing, the cost of downtime or contamination from adhesive residue has grown exponentially, particularly given the high capital investment in digital press equipment.

Traditional splicing tapes often “bleed” or release adhesive under heat and pressure, posing a contamination risk to print heads, imaging drums, and tension rollers. The opportunity lies in ultra-clean removable tapes engineered with high-shear, low-ooze adhesive layers that ensure flawless web continuity without residue transfer.

In high-value digital presses, where web tension control and splice precision are critical, these advanced tapes prevent burst or failed splices, ensuring uninterrupted operations even during frequent job changes. Adhesive systems developed for butt-splicing in high-speed applications provide gap-free joining, preventing web snags or alignment shifts before the substrate enters the print module.

With the global digital printing market projected to expand due to customization and short-run demand, precision-engineered, clean-release splicing tapes represent an essential enabler of uptime reliability, protecting multi-million-dollar assets and ensuring consistent print quality.

Market Opportunity 2: Formulation of Solvent-Resistant, Chemically Inert Tapes for Medical and Pharmaceutical Packaging

The medical device and pharmaceutical packaging industry represents a lucrative niche for chemically inert and solvent-resistant splicing tapes that ensure product integrity, sterility, and regulatory compliance under extreme process conditions.

Pharmaceutical packaging often involves exposure to solvents and sterilization agents such as isopropanol, ethanol, or iodine. Conventional adhesives can dissolve or degrade under such exposure, compromising packaging barriers. The next frontier involves chemically inert splicing solutions using high-purity acrylic or silicone adhesives designed to resist these solvents while maintaining adhesion to sterile laminates and barrier films.

Medical diagnostics applications—such as microfluidic and lateral flow assay devices—already rely on medical-grade, PFAS-free, non-interacting adhesives, providing a natural extension for use in medical packaging web splicing. The demand for zero-residue and particle-free adhesives that are cleanroom-compatible drives the precision standards governing the niche.

Regulatory compliance is another value driver. Splicing tapes designed for healthcare manufacturing must align with ISO 10993 (biocompatibility) and USP Class VI standards, ensuring that no toxic leachables or outgassing can compromise the packaged product. These requirements open a premium market segment where sterile, chemically inert, and residue-free splicing tapes can deliver unmatched performance for medical and pharmaceutical converters.

Splicing Tapes Market Share Insights, 2025-2034

Market Share by Type

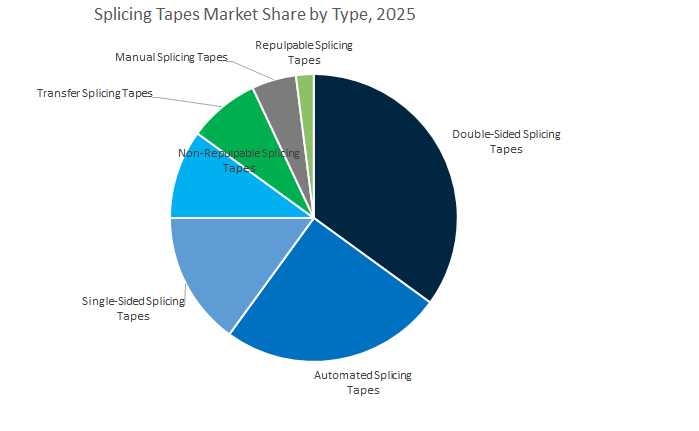

Double-sided splicing tapes dominate the global splicing tapes market, capturing an estimated 36.4% market share by 2025, primarily due to their exceptional versatility, high adhesion strength, and reliable performance across a wide range of industrial substrates. These tapes are extensively used in printing presses, paper mills, packaging lines, and converting applications, where uninterrupted operations and quick reel changeovers are vital to efficiency. Their double-sided construction ensures secure bonding between overlapping materials, minimizing downtime and material waste during high-speed production runs. The growing emphasis on automation, precision, and high-speed processing across industries such as paper, packaging, and electronics continues to fuel their adoption. Manufacturers favor double-sided variants for their compatibility with diverse substrates like coated papers, plastics, foils, and films.

Automated splicing tapes are witnessing accelerated growth as industries increasingly shift toward digitized and automated manufacturing environments. These tapes are engineered for seamless integration with automatic splicing systems, offering enhanced temperature and pressure resistance for high-speed performance. Their use in flexible packaging, film converting, and electronics manufacturing aligns with the broader industrial move toward operational efficiency and process reliability. Meanwhile, single-sided and transfer splicing tapes maintain important positions for applications requiring minimal adhesive residue, clean removal, and protection of sensitive substrates in processes such as coating and lamination. Non-repulpable and repulpable splicing tapes address distinct niches—while the former remains essential for film and foil-based applications, the latter is increasingly favored by eco-conscious paper and packaging manufacturers pursuing sustainable production solutions.

Market Share by End-Use Industry

The paper and printing industry remains the dominant end-use sector, accounting for approximately 42.3% of the global splicing tapes market by 2025. This leadership stems from the continuous, high-speed nature of modern paper production and printing operations, where unbroken web continuity is essential for cost efficiency and product quality. Splicing tapes enable seamless roll-to-roll transitions during newsprint, magazine, and packaging paper production, reducing downtime and waste. The demand is further reinforced by the revival of high-quality packaging print applications and ongoing upgrades in press technologies that demand splicing materials with high shear strength, temperature tolerance, and residue-free removal.

Packaging represents the second-largest and one of the fastest-growing segments, driven by booming global e-commerce, food packaging, and flexible packaging industries. Splicing tapes are critical for ensuring continuous lamination, coating, and slit-to-rewind operations in packaging film production. Their contribution to process efficiency, reduced machine stoppage, and improved yield rates makes them indispensable in high-volume production environments. The electronics sector is emerging as a high-value growth area, where precision splicing is crucial for display films, battery electrode materials, and cleanroom-compatible processes in semiconductors and EV battery manufacturing.

The converting industry, encompassing film, foil, and textile processing, relies heavily on high-performance splicing tapes that withstand high temperatures, chemicals, and tension variations. Similarly, the automotive sector utilizes splicing tapes for efficient interior trim, insulation, and surface finishing operations in component assembly lines. In textiles, construction, and other industrial applications, splicing tapes facilitate continuous material joining, lamination, and waterproofing, ensuring operational reliability and material integrity.

The Global Splicing Tapes Industry is consolidated among five leading players—tesa SE, 3M Company, Avery Dennison Performance Tapes, Nitto Denko Corporation, and Intertape Polymer Group (IPG)—each leveraging specialized adhesive chemistries, sustainable production models, and strong technical service networks. Their differentiation lies in precision adhesion performance, repulpable certifications, film thickness control, and substrate versatility.

Tesa SE maintains one of the most comprehensive repulpable splicing tape portfolios, featuring innovations like tesa® 61914 that dissolve completely in the papermaking process (pH 3–9). Its Hamburg cleanroom facility specializes in thin-film adhesive production, providing a foundation for its optically clear and low-thickness splicing solutions. Sustainability is central to its business, with 20%+ of annual sales from products under five years old, reflecting strong R&D velocity. Debonding on Demand and high-temperature splicing lines like tesa® 51917 underscore its leadership in balancing sustainability with durability across paper, film, and composite web applications.

3M leverages its Safety and Industrial Group and Transportation & Electronics Division to lead in industrial splicing solutions for high-speed lamination and converting. With over 100,000 patents, 3M offers rubber, silicone, and advanced acrylic chemistries tailored for specific thermal and substrate challenges. The company’s $1.5 billion free cash flow (Q3 2024) reinforces strong R&D investment capacity, while its ‘3M eXcellence’ operational model launched in 2025 aims to enhance global supply reliability—critical for industries requiring uninterrupted production uptime.

Avery Dennison is strategically expanding into renewable energy and appliance assembly sectors, leveraging its pressure-sensitive adhesive (PSA) expertise for automation-friendly, durable splicing and bonding. Its Solar Bonding Portfolio (April 2025) exemplifies cross-market application of tape technology into solar and clean energy manufacturing. Sustainability drives innovation—its rBG Pure Liners launched in October 2024 incorporate recycled fibers to lower carbon intensity. Avery’s high-adhesion PSA formulations are recognized for multi-substrate bonding, providing high durability under heat, moisture, and chemical exposure across industrial lines.

Nitto Denko dominates the Asian electronics and film processing market, known for its ultra-thin, high-precision splicing tapes that meet the demands of flexible display manufacturing and film lamination. The company’s pressure-sensitive adhesion technology delivers exceptional plasticizer and chemical resistance, ensuring stability for vinyl and polymer substrates. With strong R&D investment in EV materials and advanced electronics, Nitto continues to pioneer heat-resistant and multi-layered film splicing solutions, supporting industrial applications where micron-level thickness and flawless adhesion are critical.

Intertape Polymer Group (IPG) is a key North American leader offering single- and double-sided splicing tapes tailored for paper, corrugated board, and flexible film industries. Its vertically integrated operations provide superior cost efficiency and product consistency, enabling wide-scale deployment of manual and automated splicing systems. IPG’s industrial presence in core starting, roll finishing, and web processing positions it as an essential supplier to printing and packaging converters seeking high-tack and heavy-duty bonding performance. The company’s robust regional manufacturing network ensures fast turnaround and optimized distribution within its core U.S. and Canadian markets.

Country Analysis: Regional Developments Driving the Global Splicing Tapes Industry

China – Industrial Expansion and Packaging Innovation Fuel Demand for High-Tack and Sustainable Splicing Tapes

China continues to lead the global splicing tapes market, driven by its expansive packaging, electronics, and printing industries. The surge in high-speed automatic splicers within the packaging and label converting sectors has created a robust demand for high-tack, flying splice tapes that ensure zero production downtime. Rapid adoption of PET-based and non-woven splicing tapes for precision film joining is strengthening China’s domestic manufacturing capacity, reducing dependence on imports.

Government initiatives like “Made in China 2025” are boosting downstream industries—especially electric vehicles (EVs), flexible packaging, and battery assembly—that require high-tolerance, silicone-based splicing tapes for delicate lamination and thermal applications. Meanwhile, the corrugated board industry continues to expand, pushing demand for repulpable kraft splicing tapes used in continuous web processing. Domestic producers are also embracing global sustainability goals by developing bio-based and solvent-free adhesive splicing solutions, aligning with international VOC reduction and circular economy standards.

United States – Advanced Manufacturing and Material Science Propel Specialty Splicing Tape Innovation

The United States splicing tapes market is characterized by technological innovation, stringent quality standards, and strong participation from major automotive, aerospace, and electronics manufacturers. Leading players have launched high-performance splicing tapes engineered for EV battery production, lightweight automotive materials, and aerospace assembly, where superior thermal resistance, shear strength, and adhesion reliability are essential.

Growing demand for UV- and temperature-resistant formulations has driven R&D in rubber-based and acrylic adhesive chemistries, catering to industrial, defense, and construction sectors. The U.S. is also pioneering in clean-room compatible splicing tapes for semiconductor and display manufacturing, emphasizing ultra-clean, residue-free adhesion. Additionally, the integration of RFID-enabled splicing tapes is emerging as a digital transformation milestone, enhancing real-time production monitoring, inventory control, and logistics traceability across complex industrial supply chains.

Germany – European Center for Precision Splicing and VOC-Compliant Adhesive Engineering

Germany remains the European hub for precision-engineered splicing tape solutions, emphasizing low-VOC and sustainable adhesive technologies in compliance with the EU Industrial Emissions and VOC Directives. German manufacturers are spearheading the transition toward solvent-free hot-melt adhesive systems, meeting both environmental and performance criteria for automotive, packaging, and industrial assembly applications.

The German automotive and wire harness industries represent major demand centers for high-temperature-resistant splicing tapes capable of maintaining mechanical integrity under continuous stress. Simultaneously, Germany’s advanced printing and label converting industries rely on precision-slitted, non-repulpable film splicing tapes designed for flawless web transitions and invisible splicing lines. R&D programs funded by government and academic clusters are exploring recycled-content backings and adhesion-enhancing surface treatments to ensure compatibility with next-generation polymer substrates, positioning Germany as a benchmark for sustainable adhesive innovation in Europe.

Japan – Technological Leadership in Ultra-Thin, Bio-Based, and Electronic Splicing Tape Development

Japan’s splicing tapes market is highly advanced, shaped by innovation in electronics, flexible displays, and sustainability-driven adhesive chemistry. Industry pioneers such as Nitto Denko are developing bio-based adhesives for high-performance splicing tapes, contributing to carbon reduction efforts across Japan’s precision manufacturing sectors. The country leads in ultra-thin, double-sided transfer splicing tapes for high-speed paper, film, and electronic substrate processing, minimizing production downtime and material waste.

In the OLED and flexible electronics industry, manufacturers are deploying precision splicing tapes with exceptional thermal and chemical resistance to enable defect-free film joining. Japan’s focus on automated dispensing and roll-to-roll processing systems is also driving demand for precision-wound splicing rolls, ensuring high uniformity and adhesive consistency for delicate materials used in semiconductor and battery production.

India – Expanding Packaging, Printing, and Infrastructure Sectors Drive Market Growth

India’s splicing tapes market is witnessing exponential growth due to rapid industrialization, booming e-commerce logistics, and the expansion of paper and flexible packaging industries. High-speed converting lines in the packaging sector increasingly require durable, high-tack splicing tapes to ensure uninterrupted operations during roll changes. The paper and board industries, vital for newsprint and corrugated packaging, are adopting repulpable splicing tapes that maintain performance consistency while supporting recyclability.

Government-backed programs like ‘Make in India’ and Smart Infrastructure Initiatives are stimulating local adhesive manufacturing and import substitution. Domestic players are investing in rubber-based splicing tapes engineered for India’s varied climatic conditions—ensuring reliability in both humid and arid environments. As infrastructure projects and logistics networks expand, industrial-grade splicing tapes are becoming critical in construction, pipeline insulation, and large-scale packaging operations, firmly positioning India as a high-growth market for specialty adhesive tapes in Asia.

South Korea – Advanced Display and EV Battery Manufacturing Power Splicing Tape Evolution

South Korea’s specialty splicing tape market thrives on its global leadership in display technology and electric vehicle manufacturing. The flat-panel and flexible display sectors dominate domestic demand, with manufacturers utilizing high-shear splicing tapes for large-format screen film joining and precision material lamination. The country’s major conglomerates are investing in electrically insulating splicing tapes tailored for lithium-ion battery assembly, where thermal resistance and electrical integrity are paramount.

The growth of automated roll-to-roll processing technologies across electronics and advanced materials production is fueling demand for ultra-thin, clean-removal film splicing tapes that ensure zero web distortion during high-speed transitions. Supported by national R&D initiatives and an advanced manufacturing ecosystem, South Korea continues to emerge as a strategic hub for next-generation adhesive innovation, particularly in the EV, electronics, and optical film industries.

Splicing Tapes Market Report Scope

Splicing Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$956.7 Million

|

|

Market Size (2034)

|

$1326.7 Million

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Type (Repulpable, Non-Repulpable, Single-Sided, Double-Sided, Transfer, Automated, Manual), By Adhesive Technology (Pressure Sensitive, Hot Melt, Solvent-Based, Water-Based), By Adhesive Resin Type (Acrylic-based, Rubber-based, Silicone-based), By Carrier Material (Paper/Tissue, Film, Non-Woven, Foil, Fabric/Cloth), By End-User (Paper and Printing, Packaging, Electronics, Automotive, Converting, Textiles, Construction, Others), By Splicing Application Type (Flying, Manual/Stationary, Core Starting, Roll Finishing/Tabbing, Overlap, Butt

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, tesa SE, Nitto Denko Corporation, Avery Dennison Corporation, Intertape Polymer Group Inc. (IPG), Scapa Group plc, Lohmann GmbH & Co. KG, Lintec Corporation, Shurtape Technologies, LLC, Berry Global Inc., Saint-Gobain Performance Plastics, Teraoka Seisakusho Co., Ltd., Adhesives Research, Inc., Sika AG, H.B. Fuller Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Type

- Repulpable

- Non-Repulpable

- Single-Sided

- Double-Sided

- Transfer

- Automated

- Manual

By Adhesive Technology

- Pressure Sensitive

- Hot Melt

- Solvent-Based

- Water-Based

By Adhesive Resin Type

- Acrylic-based

- Rubber-based

- Silicone-based

By Backing/Carrier Material

- Paper/Tissue

- Film

- Non-Woven

- Foil

- Fabric/Cloth

By End-Use Industry

- Paper and Printing

- Packaging

- Electronics

- Automotive

- Converting

- Textiles

- Construction

- Others

By Splicing Application Type

- Flying

- Manual/Stationary

- Core Starting

- Roll Finishing/Tabbing

- Overlap

- Butt

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Splicing Tapes Market

- 3M Company

- tesa SE

- Nitto Denko Corporation

- Avery Dennison Corporation

- Intertape Polymer Group Inc. (IPG)

- Scapa Group plc

- Lohmann GmbH & Co. KG

- Lintec Corporation

- Shurtape Technologies, LLC

- Berry Global Inc.

- Saint-Gobain Performance Plastics

- Teraoka Seisakusho Co., Ltd.

- Adhesives Research, Inc.

- Sika AG

- H.B. Fuller Company

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Splicing Tapes Market, connecting materials science breakthroughs with high-speed converting, battery manufacturing, and circular packaging requirements; our analysis reviews qualification data, OEM specification shifts, and factory-floor performance to benchmark flying splice reliability, thermal endurance, dielectric assurance, and clean removability under real production conditions. It highlights how repulpable chemistries, heat-resistant thin films, and LSE-compatible adhesives are enabling uptime gains and sustainability compliance across paper, flexible packaging, electronics lamination, and film extrusion—while automation and AI-driven coating control reframe cost-to-serve and waste reduction. Designed for operations leaders, process engineers, sourcing teams, and product strategists, this report is an essential resource for sizing opportunities, de-risking material transitions, and prioritizing roadmap investments in a market where splice integrity directly impacts yield, safety, and profitability.

Scope Highlights

Segmentation:

- By Type: Repulpable; Non-Repulpable; Single-Sided; Double-Sided; Transfer; Automated; Manual

- By Adhesive Technology: Pressure Sensitive; Hot Melt; Solvent-Based; Water-Based

- By Adhesive Resin Type: Acrylic-based; Rubber-based; Silicone-based

- By Backing/Carrier Material: Paper/Tissue; Film; Non-Woven; Foil; Fabric/Cloth

- By End-Use Industry: Paper and Printing; Packaging; Electronics; Automotive; Converting; Textiles; Construction; Others

- By Splicing Application Type: Flying; Manual/Stationary; Core Starting; Roll Finishing/Tabbing; Overlap; Butt

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies: Analysis/profiles of 15+ companies (3M Company; tesa SE; Nitto Denko Corporation; Avery Dennison Corporation; Intertape Polymer Group Inc. (IPG); Scapa Group plc; Lohmann GmbH & Co. KG; Lintec Corporation; Shurtape Technologies, LLC; Berry Global Inc.; Saint-Gobain Performance Plastics; Teraoka Seisakusho Co., Ltd.; Adhesives Research, Inc.; Sika AG; H.B. Fuller Company).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.