Sports Helmet Market Overview: Safety Innovation, Material Science, and Smart Integration

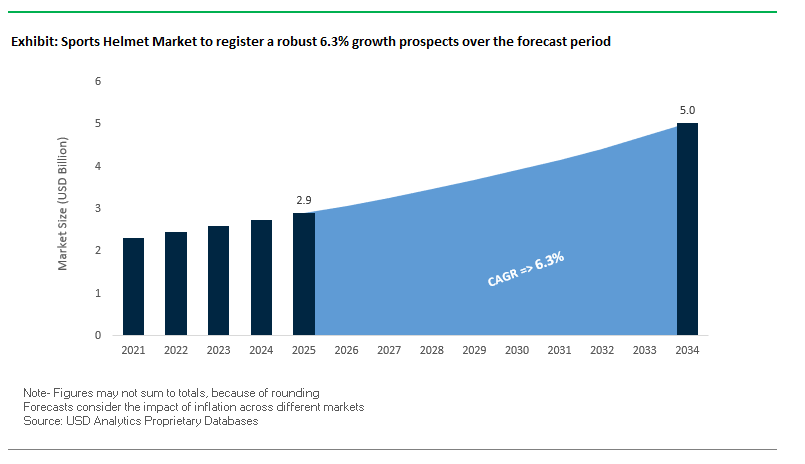

The global sports helmet market is expected to grow from $2.9 billion in 2025 to $5 billion in 2034 with a steady CAGR of 6.3%. The market is growing at a rapid rate due to the safety of players being the priority of professional, amateur, and recreational players. As there is growing awareness of concussions worldwide and tougher safety regulations being enforced by sporting bodies, manufacturers are creating helmets with innovative materials, enhanced impact protection systems, and integrated technology.

For trade experts, each market of the diverse sports segments of cycling, football, snow sports, motorsports, and new urban sports has its own performance and safety needs. New materials of carbon fiber, Kevlar, and high-grade polycarbonate are opening the way for lighter and stronger helmets, and additional smart helmet technologies like Bluetooth connectivity, GPS, health sensors, and built-in cameras are changing product expectations. Compliance with standards like DOT, ECE, and Snell is a minimum, and quality assurance is therefore a competitive requirement.

Key Insights for Industry Stakeholders:

- Safety-Driven Demand: Rising concussion and injury awareness is influencing purchasing behavior and product design.

- Technology Infusion: Bluetooth, GPS, MIPS, and AI-enabled monitoring are becoming mainstream.

- Material Innovation: Lightweight yet impact-resistant materials are improving comfort and safety.

- Regulatory Compliance: Global certifications are critical to market acceptance.

- Diverse End-Use Growth: Expanding adoption across both traditional and new-age sports segments.

Recent Developments and Strategic Shifts in Sports Helmet Industry

Recent developments in the sports helmet industry came in the form of key product launches, safety features, and market entry. In July 2025, MET launched the Revo helmet with MIPS AIR technology for enhanced impact protection and a 23.5% improvement in cooling effectiveness via wind-tunnel-tested designs to emphasize both the importance of safety and performance. In July 2025, POC launched the Cytal and Cularis helmets, at the pinnacle of Virginia Tech's safety ratings and featuring Venturi-effect ventilation for maximum comfort.

Urban convenience and mobility also received upgrades. In May 2025, UK's Newlane launched the world's first MIPS foldable helmet that was designed for commuters who wanted portability without losing on safety. The launch of Ather Halo smart helmets in April 2025 brought consumer electronics and sports safety integration into the picture, and the features included Bluetooth connectivity, in-built intercom, and music control for riders.

Trends towards AI adoption were observed in February 2025, when Honeywell introduced AI-based safety products, which could be utilized in sports helmets to track impacts in real time. Forays into emerging markets are also picking up pace NHK Helmets entered India in January 2025 with polycarbonate helmets and carbon fiber helmets, capitalizing on the uptick in the sports and mobility segment in the country. Brand positioning and marketing activities, such as Under Armour's "Protect This House" initiative in October 2024, reflect the utilization of emotional attachment in creating loyalty and creating demand for protective equipment.

Trends and Opportunities Shaping the Global Sports Helmet Market

Multi-Impact Foam Technology Driving MIPS Integration Across Sports

The adoption of Multi-directional Impact Protection Systems (MIPS) has been a trend-defining force in the global sports helmet industry, countering the gaping safety gap in safeguarding against rotational brain injury. In comparison to conventional helmets designed to be resilient against linear impacts, MIPS boasts a low-friction layer that enables the helmet to shift slightly against the head when the impact is made at an angle. This diminishes the rotational force imparted on the brain, drastically reducing the threat of concussion. Its application in cycling, skiing, motorsport, and equestrian helmets is a testament to its efficacy. More than 150 worldwide helmet brands feature MIPS, using its iconic yellow-dot branding to promote consumer confidence. Third-party endorsement by organizations like Virginia Tech's helmet safety ratings further increases its credibility and take-up rate. Growing consumer awareness of concussion risk, combined with regulatory and sporting federation approvals, is driving MIPS penetration in the premium and mid-range segments of helmets.

Rise of Custom 3D-Printed Helmets for Professional and High-Performance Sports

3D-printed helmets tailored to individual athletes are revolutionizing athletes' safety and comfort with a scan-to-fit, bespoke solution. High-performance sports such as American football, cycling, and motor sports are at the forefront of this revolution, with companies such as Riddell's Tru-Fit system providing helmets tailored to the precise head geometry of an athlete. This precise fit enhances impact stability, maximizes protection, and reduces discomfort from poorly fitting designs. 3D printing also enables sport-specific optimization, producing lattice structures optimized for various patterns of impact such as high-speed frontal impacts in the bobsled or cumulative sub-concussive impacts in contact sports. New materials such as Thermoplastic Polyurethane (TPU) optimize energy absorption and durability, enabling lightweight yet highly protective designs. As costs reduce with production volume, the technology is ready to transition from professional sports to recreational premium markets.

Expanding Affordable, High-Safety Cricket Helmets in Emerging Markets

The cricket segment presents a high-growth opportunity, particularly in India, Pakistan, Sri Lanka, and Bangladesh, where the player population is huge but exposure to high-standard helmets is negligible. With growing awareness of injury risk of cricket following the 2014 Phillip Hughes tragedy, governing bodies like the ICC and ECB have imposed tighter helmet safety standards, including the requirement of mandatory neck guards. The challenge lies in providing helmets capable of resisting fastball impacts in excess of 90 mph while being visible and comfortable. Suppliers who can offer low-cost but certified cricket helmets to the grassroots and amateur players can command huge market share in these price-sensitive, high-volume markets.

Smart Equestrian Helmets with Emergency SOS and Fall Detection

The equestrian market represents a high-end safety opportunity in the form of intelligent helmets that incorporate fall detection and SOS systems via GPS. Remote falls are potentially life-threatening risks, and helmets that incorporate impact sensors can immediately alert emergency contacts, as well as the rider's exact location. Integration with other safety gear, including air vests, can be used to design an overall system for injury prevention that can be sold to professional and recreational riders. The high correlation of equestrian sports with luxury and high-end gear translates to high willingness to pay for technology that enhances safety as well as peace of mind. This high-margin, niche opportunity aligns with higher demand for connected sport equipment in the high-end outdoor sports market.

Market Share Analysis of the Global Sports Helmet Market

Market Share by Application: Cycling and Motorsports Lead, Action Sports Accelerate

Cycling leads the world market for sports helmets with a 35% share on the back of urban mobility patterns, the boom in e-bike sales, and growing road and mountain biking participation. Government spending on cycling infrastructure and commuter safety initiatives is underpinning helmet uptake in city spaces. Motorsports, at 25%, is also a high-ticket business segment because of tight safety regulation and the use of cutting-edge technologies such as HUDs (heads-up displays) and in-helmet communication. Snow sports helmets are seeing consistent expansion, fueled by features that include built-in audio, incorporated goggles, and thermal control, while skateboarding and scootering helmets are growing with increasing youth activity and international safety regulations. Water sports helmets, although smaller in market share, are picking up in wakeboarding and kayaking circles as safety consciousness increases.

.png)

Market Share by End-User: Recreational Users Drive Volume, Professionals Influence Innovation

60% of the world's demand for sports helmets comes from recreational users, who value comfort, fashion, and price without sacrificing essential safety standards. This segment's purchasing power lies in mass participation in sports like cycling, snow sports, and skateboarding, where lifestyle attraction drives purchases. Professional players, with 25% of the market, comprise a smaller but very powerful base, driving innovation in aerodynamics, weight saving, and fit-to-fit technologies. The children's helmet market is growing very rapidly as parents' safety consciousness and school-level sporting regulations require head protection for youth players. Market growth in this segment is also underpinned by design advances that compromise safety with child-appropriate appearance to promote regular usage.

Sports Helmet Market Competitive Landscape – Leading Players Defining Performance and Safety Standards

The sports helmet market is shaped by global leaders with strong brand heritage, innovative R&D pipelines, and targeted expansion strategies. Key players included are Arai Helmet, Ltd., Shoei Co., Ltd., Bell Sports Inc. (BRG Sports), HJC Corp., Fox Racing, Inc., LS2 Helmets, AGV (Dainese S.p.A), KASK S.p.A., MIPS AB, Troy Lee Designs, Studds Accessories Ltd., Steelbird Hi-Tech India Ltd., Leatt Corporation, Sena Technologies, Inc., Rudy Project S.p.A., Others.

Bell Sports, Inc. – High-Performance Helmets Across Multiple Sports

Bell has a legacy in racing, cycling, and action sports, manufacturing helmets with high Virginia Tech safety ratings on a consistent basis. Its lineup includes smart, half-shell, and full-face helmets for both amateur and professional athletes. Maximum protection with ergonomic fit is provided in every attempt, and thus it is a well-known brand in numerous sports.

Specialized Bicycle Components, Inc. – Integrated Cycling Ecosystem with Safety at Core

Specialized uses its expertise in cycling to design helmets like the S-Works Prevail and Ambush, striking a balance between aerodynamic capability and elements like the ANGi crash sensor. This fusion provides real-time crash alert to emergency contacts, and by doing so, Specialized is at the forefront of connected cycling safety.

Giro Sport Design – Style, Comfort, and Advanced Impact Protection

Giro, a Vista Outdoor company, offers a style, ventilation, and protective balance. With MIPS technology integrated into its whole lineup, Giro minimizes the threat of rotational forces in the event of a crash. Its helmets for cycling, skiing, and snowboarding are popular for fit and performance value.

Riddell, Inc. – Football Helmet Safety Leader with Data-Driven Protection

Riddell is the market leader in football helmets, outfitting the NFL and leading the way with lines like the InSite Training Tool, which tracks the impacts players experience to avoid injury. Its SpeedFlex and Axiom products focus on research-driven biomechanical safety.

Studds Accessories Ltd. – Mass-Market Reach with International Certifications

Studds sells domestic and international markets under its Studds and premium SMK helmet brands. With 38+ countries of presence, the brand strikes a balance between affordability and global safety standards, providing high-volume output and mass accessibility.

United States: Innovation-Driven Growth and Expanding Multi-Sport Adoption

The United States sport helmet market is shaped by a strong emphasis on technological safety enhancements and a culture that prioritizes protective gear across multiple sports categories. Leading brands such as Fox Racing, Troy Lee Designs, Bell, and Giro are integrating systems like MIPS Integra Split to mitigate rotational forces during angled impacts, a feature now widely adopted in cycling, motocross, and snow sports. In addition, the market is witnessing the rapid integration of Bluetooth connectivity, GPS navigation, and crash detection sensors features that enable emergency alerts and enhance user safety. High-impact sports such as skiing, snowboarding, and mountain biking are key demand drivers, while collaboration between helmet manufacturers and safety tech firms ensures continuous improvement in protective performance.

A growing consumer demand for wearable impact trackers and AI-assisted helmet designs is pushing innovation beyond core safety functions. Professional sports leagues, collegiate programs, and extreme sports events in the U.S. increasingly mandate certified, high-tech helmets, contributing to steady market expansion. The appeal is not limited to professionals recreational athletes and fitness enthusiasts are also investing in advanced helmets for everyday use. E-commerce channels, driven by specialist sports retailers and direct-to-consumer brand websites, have expanded accessibility nationwide. With its mature sports culture, strong regulatory environment, and willingness to embrace premium technologies, the U.S. remains a leading global hub for sport helmet innovation and adoption.

India: Regulatory Enforcement and Shift Toward Branded, Certified Products

The Indian sport helmet market is undergoing a significant transformation, driven by government-mandated safety regulations and rising public awareness of the risks associated with uncertified products. The Bureau of Indian Standards (BIS) continues to enforce the IS 4151:2015 safety standard, ensuring that only certified helmets can be legally sold. National campaigns backed by both public agencies and private organizations are positioning helmets as lifesaving equipment rather than optional accessories, leading to higher adoption rates across cycling, motorsports, and recreational activities.

Domestic manufacturing giants such as Steelbird and Studds are responding with R&D investments aimed at producing helmets that meet both national and international standards (ECE, DOT). These manufacturers are expanding their offerings to include full-face, motocross, and Bluetooth-enabled models targeting urban commuters, professional racers, and youth segments. Changing consumer preferences are favoring branded, comfort-oriented, and aerodynamically advanced helmets, often with aesthetic customization options. While price sensitivity remains a factor, the shift toward safety, certification, and feature-rich designs is expected to solidify India’s position as both a high-growth consumer market and a competitive global manufacturing base for sport helmets.

Germany: Engineering Excellence and Performance-Driven Demand

Germany’s sport helmet market benefits from its heritage of engineering precision and commitment to high safety standards across professional and amateur sports. German manufacturers are leveraging carbon fiber composites, Kevlar reinforcements, and fiber-reinforced plastics to deliver helmets that combine ultra-lightweight performance with superior impact resistance. Sports like cycling, skiing, and motorsports dominate the demand profile, with consumers both professional athletes and enthusiasts seeking top-tier protective gear that meets stringent EU safety regulations.

The rise of online retail platforms has made high-quality German-engineered helmets more accessible both domestically and internationally, with brands optimizing SEO and e-commerce strategies to attract discerning buyers. Increasing participation in endurance sports and competitive racing has created opportunities for custom-fitted helmets tailored to specific disciplines. Germany’s focus on functional design, premium material sourcing, and durability not only sustains its reputation for excellence but also positions it as a trend leader in performance-driven helmet technology across Europe.

Japan: High-Precision Craftsmanship and Motorsports-Driven Demand

Japan’s sport helmet market is globally recognized for its uncompromising quality and material innovation, led by industry leaders such as Arai and Shoei. These brands are known for handcrafted, aerodynamically refined helmets that undergo rigorous safety testing, often exceeding international certification standards. Japan’s strong motorsports culture, supported by events like MotoGP and Super GT, fuels demand for high-performance racing helmets, while cycling, skiing, and equestrian sports contribute to a diversified market base.

Technological integration is an emerging trend, with Japanese companies developing helmets featuring noise reduction systems, advanced ventilation channels, and lightweight composite shells that enhance rider comfort without sacrificing safety. Precision manufacturing ensures long product lifecycles, appealing to both professional athletes and casual sports participants. Coupled with a deep-rooted cultural emphasis on craftsmanship and reliability, Japan continues to hold a premium position in the global sport helmet market, balancing traditional expertise with cutting-edge innovation.

China: Manufacturing Powerhouse and Expanding Domestic Market

China stands as the largest global manufacturing hub for sport helmets, supported by an extensive supply chain and advanced production capabilities that enable high-volume output for both domestic use and export markets. The government’s helmet-wearing mandates for e-bike riders, along with growing participation in cycling, motorsports, and adventure sports, are fueling domestic consumption. Chinese manufacturers are increasingly investing in smart helmet technologies, incorporating integrated cameras, Bluetooth communication, and GPS tracking to meet evolving consumer expectations.

Domestic brands are gaining traction alongside global imports, leveraging localized marketing strategies, competitive pricing, and product customization to target specific user groups. E-commerce dominates distribution, with platforms like Tmall, JD.com, and Taobao serving as primary sales channels for both mass-market and premium helmets. With its combination of mass manufacturing capabilities, rapid technology adoption, and a rising middle-class sports culture, China is set to remain both a supply leader and a major consumer market in the sport helmet industry.

United Kingdom: Cycling Growth and Sustainability-Led Innovation

The United Kingdom sport helmet market is benefiting from government-backed cycling initiatives, increased urban mobility adoption, and growing interest in competitive racing. Cycling helmets are leading the segment, but demand for skiing, equestrian, and motorsport helmets is also growing. Brands are responding with eco-friendly materials, recyclable shells, and inclusive sizing options, catering to an audience that values sustainability and accessibility.

Technological advancements are also shaping the UK market, with products featuring enhanced aerodynamics, superior ventilation, and integrated LED visibility systems for improved safety in low-light conditions. Online retail remains a dominant channel, with brands investing in digital marketing and direct-to-consumer strategies to capture a tech-savvy customer base. As sustainability, innovation, and inclusivity converge, the UK is positioning itself as one of Europe’s most progressive and consumer-conscious sport helmet markets.

Sports Helmet Market Report Scope

Sports Helmet Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.9 Billion

|

|

Market Size (2034)

|

$5 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Helmet Type (Full Face, Open Face, Modular, Off-Road, Half Helmet, Smart Helmet), By Application (Motorsports, Cycling, Snow Sports, Water Sports, Equestrian Sports, Skateboarding/Scootering), By End-User (Professional Athletes, Recreational Users, Children), By Material (Thermoplastics (Polycarbonate, ABS), Composites (Carbon Fiber, Fiberglass), EPS Foam), By Distribution Channel (Specialty Sports Stores, Online Retail, Mass Merchandisers, Direct-to-Consumer)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Arai Helmet, Ltd., Shoei Co., Ltd., Bell Sports Inc. (BRG Sports), HJC Corp., Fox Racing, Inc., LS2 Helmets, AGV (Dainese S.p.A), KASK S.p.A., MIPS AB, Troy Lee Designs, Studds Accessories Ltd., Steelbird Hi-Tech India Ltd., Leatt Corporation, Sena Technologies, Inc., Rudy Project S.p.A., Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sports Helmet Market Segmentation

By Helmet Type

- Full Face

- Open Face

- Modular

- Off-Road

- Half Helmet

- Smart Helmet

By Application

- Motorsports

- Cycling

- Snow Sports

- Water Sports

- Equestrian Sports

- Skateboarding/Scootering

By End-User

- Professional Athletes

- Recreational Users

- Children

By Material

- Thermoplastics (Polycarbonate, ABS)

- Composites (Carbon Fiber, Fiberglass)

- EPS Foam

By Distribution Channel

- Specialty Sports Stores

- Online Retail

- Mass Merchandisers

- Direct-to-Consumer

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Sport Helmet Market

- Arai Helmet Ltd.

- Shoei Co. Ltd.

- Bell Sports Inc. (BRG Sports)

- HJC Corp.

- Fox Racing Inc.

- LS2 Helmets

- AGV (Dainese S.p.A)

- KASK S.p.A.

- MIPS AB

- Troy Lee Designs

- Studds Accessories Ltd.

- Steelbird Hi-Tech India Ltd.

- Leatt Corporation

- Sena Technologies Inc.

- Rudy Project S.p.A.

* List Not Exhaustive

Research Coverage

This report investigates the Sports Helmet Market in depth, offering industry professionals a detailed understanding of emerging trends, technological breakthroughs, material advancements, and competitive strategies shaping the sector. USDAnalytics’ analysis reviews safety innovations, regulatory compliance frameworks, and the integration of smart technologies such as Bluetooth, GPS, and AI-enabled monitoring. Highlighting shifts in material science—from lightweight composites to multi-impact foam systems—this report is an essential resource for stakeholders seeking to navigate dynamic changes in consumer demand, product safety standards, and market expansion opportunities. The coverage spans key geographic regions, diverse sports applications, and leading brands influencing the global sports helmet landscape. Scope includes-

- Segmentation:

- By Helmet Type: Full Face, Open Face, Modular, Off-Road, Half Helmet, Smart Helmet

- By Application: Motorsports, Cycling, Snow Sports, Water Sports, Equestrian Sports, Skateboarding/Scootering

- By End-User: Professional Athletes, Recreational Users, Children

- By Material: Thermoplastics (Polycarbonate, ABS), Composites (Carbon Fiber, Fiberglass), EPS Foam

- By Distribution Channel: Specialty Sports Stores, Online Retail, Mass Merchandisers, Direct-to-Consumer

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, Middle East & Africa

- Historic Data: 2021–2024

- Forecast Data: 2025–2034

- Companies Covered: Profiles and strategic analysis of 15+ leading companies including Arai Helmet Ltd., Shoei Co. Ltd., Bell Sports Inc., HJC Corp., Fox Racing Inc., LS2 Helmets, and others.

Methodology

The research methodology integrates both qualitative and quantitative approaches to ensure a comprehensive market understanding. Primary research involved interviews with industry experts, manufacturers, distributors, and regulatory authorities across multiple geographies. Secondary research incorporated industry journals, safety certification databases, trade association publications, and company press releases. Market sizing and forecasts were derived using bottom-up and top-down models, factoring in production volumes, adoption rates across sports categories, regulatory impacts, and consumer behavior patterns. Trend analysis leveraged real-world product launches, technology integration data, and competitive benchmarking to provide a fact-based outlook from 2025 to 2034.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.