Stretch and Shrink Films Market Size, Overview, and Growth Outlook (2025–2034)

Stretch and Shrink Films Market Poised to Reach $31.8 Billion by 2034 with Focus on Logistics Efficiency and Product Protection

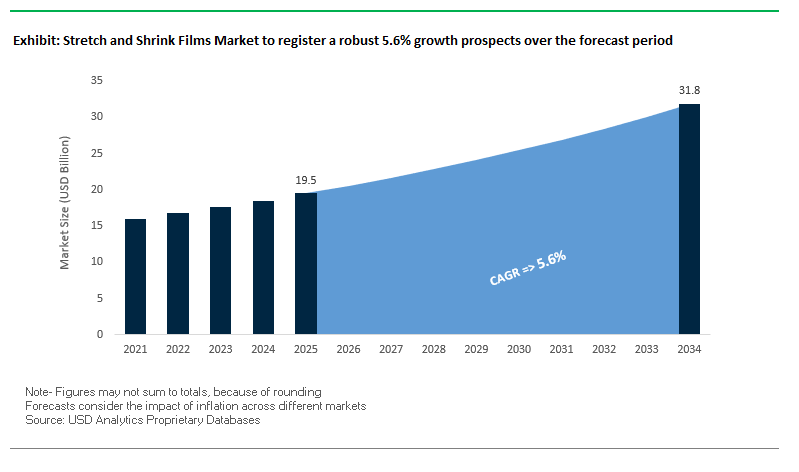

The global stretch and shrink films market is projected to grow from $19.5 billion in 2025 to $31.8 billion by 2034, achieving a CAGR of 5.6%. This market, which includes pallet wrap and retail shrink films, plays a crucial role in product protection, load stability, and logistics efficiency across industries.

Key Insights for Industry Professionals:

- Logistics efficiency and damage prevention drive demand, with stretch films ensuring pallet stability and reducing losses due to shifting, moisture, and dust.

- Material science innovations focus on high-strength, thin-gauge films, incorporating post-consumer recycled (PCR) content and exploring bio-based polymers to meet sustainability goals.

- Advanced film properties such as nano-layer technology enhance puncture resistance, load retention, and overall pallet security.

- Brand-enhancing and tamper-evident features in shrink films are increasingly used for multi-packs and retail products to combine marketing and security.

- Growing adoption of eco-friendly alternatives reflects the industry’s commitment to sustainable packaging solutions.

The market continues to evolve through innovation, sustainability initiatives, and enhanced logistics support, positioning stretch and shrink films as a core enabler of efficient supply chains and product integrity.

Market Analysis: Recent Innovations and Strategic Moves Highlight Sustainability and Technological Advancement in Stretch and Shrink Films

The stretch and shrink films industry has witnessed transformative developments in 2024–2025. In August 2025, Mondi and Krones announced Hug&Hold, a paper-based alternative to plastic shrink wrap for beverage bottles, underscoring the sector’s pivot toward sustainable materials. In the same month, ProAmpac acquired PAC Worldwide, expanding its flexible packaging capabilities and global footprint. Earlier, in July 2025, Sigma Stretch Film announced a $39 million expansion in Columbus, Georgia, including new manufacturing and warehouse facilities, signaling investment in production capacity and job creation.

Sustainability and eco-friendly materials remain a central focus. In June 2025, Mondi and Saga Nutrition launched a paper-based stand-up pouch for pet food, while Mondi ramped up FunctionalBarrier Paper Ultimate in May 2025 to address the demand for high-barrier, sustainable packaging. In April 2025, Berry Global added a second flexible pouch production line in the UK, ensuring supply for high-performance, recyclable-ready packaging solutions.

The integration of recycled content and recyclable materials is a key trend. Berry Global launched its Bontite Sustane Stretch Film with 30% PCR content in February 2025, while Sherwin-Williams adopted Mondi spouted pouches for paint refills, emphasizing material reduction and convenience. Strategic launches like Amcor’s recyclable stand-up pouch in October 2024 and Klöckner Pentaplast’s kpNext® MDR1 and recyclable barrier films demonstrate the industry’s commitment to innovation, sustainability, and scaling up eco-conscious flexible packaging formats.

Trends and Opportunities Reshaping the Stretch and Shrink Films Market

Strategic Down-Gauging with High-Performance Resins

One of the most prominent trends in the stretch and shrink films market is the adoption of down-gauging strategies enabled by advanced resin technologies. With increasing regulatory and corporate pressure to reduce plastic consumption, manufacturers are engineering films that use 15–20% less material while maintaining the same load stability and puncture resistance. A 2025 announcement from a major resin producer introduced new LLDPE resins designed specifically for ultra-thin films that deliver equivalent or superior strength compared to conventional products.

Material science innovation underpins this shift. Dow’s ELITE™ and DOWLEX™ resins exemplify how advanced polymers enable lighter, thinner films that still perform well across a variety of pallet sizes. These high-performance films ensure exceptional stretch properties, providing a secure and tight fit around loads while reducing transportation emissions due to lighter weight. Additionally, a technical brief from a film producer highlights that ultra-high-performance films can achieve 30% or more down-gauging potential, directly translating into cost savings per pallet while reducing raw material consumption.

This dual impact of economic efficiency and sustainability benefits is accelerating adoption across industries including FMCG, food & beverage, and logistics, where large-scale pallet wrapping demands significant material usage. By leveraging engineered resins, companies are simultaneously lowering carbon footprints and improving supply chain cost efficiency.

Incorporation of Post-Consumer Recycled (PCR) Content

Another major trend reshaping the market is the integration of post-consumer recycled (PCR) plastics into shrink and stretch films. Corporate sustainability commitments are fueling this transformation. For example, PepsiCo’s ESG roadmap targets the use of 40% or more recycled content in plastic packaging by 2035, creating a strong pull for high-PCR packaging solutions.

Collaborations are key to scaling this trend. A joint effort between Borealis and a food company has resulted in a shrink film containing 65% PCR content, functioning as a drop-in solution that requires no modification to existing packaging lines. This proves that high-PCR films can meet both operational and sustainability standards. Further, a case study by Dow and RKW Group demonstrated shrink films with up to 85% PCR sourced from household waste, overcoming technical hurdles such as odor, gels, and color through advanced extrusion and resin engineering.

The ability to incorporate high PCR percentages without compromising clarity or mechanical strength is a breakthrough, as it allows global brands to meet recyclability goals while delivering reliable packaging performance. With consumer and regulatory pressure intensifying, PCR integration is becoming a central differentiator for suppliers in the stretch and shrink films industry.

Development of Performance-Engineered E-commerce Films

The exponential rise of e-commerce logistics is creating a new growth frontier for stretch and shrink films. Unlike conventional palletized loads, e-commerce shipments consist of smaller, irregularly shaped parcels that require enhanced durability, puncture resistance, and tamper-evidence features. High-value products such as electronics, appliances, and tools demand films with superior tear resistance to withstand multiple touchpoints in complex supply chains.

Manufacturers are innovating films specifically for direct-to-consumer (DTC) fulfillment, where optimized stretch wrap eliminates the need for bulky corrugated boxes and excessive void fill. This lightweight protection reduces freight costs by minimizing dimensional weight charges and helps brands lower last-mile delivery expenses—an increasingly critical metric in competitive e-commerce markets.

As e-commerce penetration continues to grow globally, the demand for fit-for-purpose stretch and shrink films designed for package-level protection will surge, creating a high-value opportunity for packaging producers to diversify beyond pallet applications.

Advanced Resins for Compatibility with Plastic Film Recycling Streams

Designing films for circularity represents another transformative opportunity. Current recycling systems face significant challenges in processing flexible films due to mixed plastic contamination and incompatibility. Innovations in resin formulations are addressing this issue by creating polyethylene-based films engineered for full recyclability.

A leading chemical company recently introduced new resins specifically designed to be reprocessed seamlessly within existing PE recycling streams, closing the loop for shrink and stretch films. Furthermore, the development of compatibilizer additives is acting as a breakthrough, serving as molecular bridges that allow different plastics to blend more effectively during reprocessing. This results in recycled materials with improved mechanical properties, expanding their applications across packaging and industrial uses.

Competitive Landscape: Leading Companies in Stretch and Shrink Films Are Driving Sustainability, Innovation, and Operational Excellence

The stretch and shrink films market is dominated by global players focusing on material innovation, sustainable solutions, and operational scalability, delivering products that meet the evolving demands of industrial and retail packaging.

Amcor plc: Driving Circular Economy Through Recyclable and High-Performance Stretch Films

Amcor provides a wide range of stretch and shrink films for food, beverages, and industrial applications, emphasizing sustainability and recyclable-ready solutions. The company is committed to making all packaging recyclable or reusable by 2025 and has launched high-performance films with spouts for bulk products. Amcor’s strengths include global manufacturing reach, material expertise, and vertical integration, with a strategic focus on circular economy initiatives while ensuring product protection and branding.

Berry Global Group, Inc.: Expanding Sustainable Stretch Films With Post-Consumer Recycled Content

Berry Global offers a portfolio of stretch and shrink films, including Bontite pallet films and printed consumer shrink wraps. In February 2025, the company introduced Bontite Sustane Stretch Film with 30% PCR content and added a second production line in the UK for recyclable pouches. Berry’s strengths lie in global manufacturing footprint, material expertise, and vertically integrated operations, with a strategy centered on sustainable, high-performance packaging solutions for the food and industrial sectors.

Mondi Group: Pioneering Eco-Friendly Paper-Based Packaging Alternatives

Mondi focuses on sustainable stretch and shrink film solutions, including paper-based alternatives like Hug&Hold for beverage bottles. Its FunctionalBarrier Paper Ultimate offers ultra-high performance for demanding applications. Mondi’s strengths include R&D capabilities, sustainability focus, and customizable packaging solutions, with a strategy aimed at leading the market in environmentally responsible, high-quality packaging innovations.

Klöckner Pentaplast Group: Advancing Recyclable Films With High-Barrier Performance

Klöckner Pentaplast provides rigid and flexible films for medical and food applications, emphasizing sustainability. In October 2024, it launched kp FlexiFlow® EH 155 R and PH 255 R, recyclable barrier flow wrap films, complementing its kpNext® medical device film. The company’s strengths include materials science expertise, sustainability commitment, and broad packaging portfolio, with a strategy focused on innovative and eco-friendly packaging solutions for global markets.

Sigma Stretch Film: Expanding Capacity to Meet Growing Industrial Demand

Sigma Stretch Film, part of Sigma Plastics Group, produces blown and cast stretch films for industrial applications. In July 2025, it announced a $39 million expansion in Columbus, Georgia, adding new production lines and warehouse capacity. Sigma’s core strengths include vertical integration, resin control, and high-quality film production, with a strategic focus on innovation, sustainability, and maintaining leadership in industrial stretch film solutions.

Stretch and Shrink Films Market Share Insights, 2025-2034

Stretch Films Dominate Market Share by Product Type in Stretch and Shrink Films Industry

Stretch films represent 65% of the global stretch and shrink films market, solidifying their position as the workhorse of pallet unitization and load stabilization. Linear low-density polyethylene (LLDPE) stretch films are indispensable across industries, ensuring secure transit of palletized goods while reducing damage, improving safety, and enabling efficient warehouse operations. Their dominance is reinforced by advancements in pre-stretched and high-performance films that allow companies to achieve source reduction—using less film per load—while still meeting load-retention standards. The ability to balance cost-effectiveness with sustainability targets makes stretch films the cornerstone of industrial logistics, far outpacing shrink films and stretch hoods in volume share.

Food & Beverages Lead Market Share by End-Use Industry in Stretch and Shrink Films Industry

Food and beverages represent 25% of the stretch and shrink films market, making them the largest end-use sector due to the sheer volume of packaged goods requiring stabilization and protection throughout global supply chains. This industry relies heavily on stretch films for palletizing bulk shipments and shrink films for multi-pack bundling of beverages, frozen foods, and convenience items. The demand is reinforced by strict hygiene standards, where films provide tamper evidence, high clarity for visual inspection, and barrier protection against contamination. With the growing importance of cold-chain logistics and rising global food trade, the food and beverage sector continues to anchor demand for both stretch and shrink films, driving innovation in recyclable and downgauged film solutions.

United States: Recycling Goals and Bio-Based Film Innovation

The United States stretch and shrink films market is evolving under strong regulatory and sustainability drivers. The U.S. Environmental Protection Agency (EPA) has set a target to increase the national recycling rate to 50% by 2030, compelling manufacturers to invest in circular economy packaging solutions. Partnerships such as the ExxonMobil–Shantou Mingca collaboration have introduced next-generation polyolefin shrink films using Exceed XP performance polyethylene, suitable for diverse industries including personal care and electronics.

The industry is also seeing rapid adoption of bioplastics and renewable resins derived from corn and sugarcane. LyondellBasell’s joint venture announced in July 2024 will deliver recycled LLDPE films by 2025, while IPG launched a shrink film with 35% recycled content in February 2024, reflecting strong momentum toward PCR integration. The Association of Plastic Recyclers (APR) continues to influence material choices with guidelines promoting washable inks and floatable films. Coupled with the e-commerce boom, demand for lightweight, space-efficient stretch and shrink films remains robust, especially as companies prioritize eco-friendly logistics solutions.

European Union: Circular Economy and Digital Product Passport Compliance

The European Union stretch and shrink films market is shaped by the Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates recycled content requirements for plastic packaging by 2030. The regulation, alongside the Ecodesign for Sustainable Products Regulation (ESPR), pushes producers toward mono-material flexible packaging to ease recyclability. In addition, the Digital Product Passport requirement will create transparency on recyclability, biodegradability, and material origin.

The restriction on PFAS substances by August 2026 is accelerating R&D in alternative barrier coatings, a critical area for food-grade shrink and stretch films. The EU has also set reuse targets for transport packaging, boosting the use of reusable shrink wraps for palletization in logistics. Collectively, these rules are driving packaging suppliers to design next-generation recyclable and reusable films, positioning Europe as a leader in sustainable film adoption.

China: Green Regulations and High-End Packaging Demand

The China stretch and shrink films market is advancing under the government’s “14th Five-Year Plan” and new regulations effective June 1, 2025, requiring express delivery companies to adopt eco-friendly, reduced, and reusable packaging. This regulatory momentum is particularly relevant for e-commerce and logistics sectors, which are heavy users of shrink films.

A growing preference for high-end packaging with advanced oxygen barriers and UV stabilization is influencing R&D, as consumers increasingly value durability and premium aesthetics. The Ellen MacArthur Foundation’s joint report with Tsinghua University emphasized the need to develop a high-quality recycled plastics market, signaling policy support for domestic recycling capacity. With tax incentives for remanufacturing and green technology adoption, local producers are scaling production of sophisticated, sustainable stretch and shrink films to meet rising consumer and regulatory expectations.

India: EPR Regulations and Reverse Logistics Systems

The India stretch and shrink films market is strongly shaped by the Plastic Waste Management (Amendment) Rules, 2024, effective April 2025, which introduced Extended Producer Responsibility (EPR) mandates for packaging producers and importers. From July 1, 2025, all plastic packaging, including stretch and shrink films, must carry barcode or QR-based traceability, ensuring accountability throughout the lifecycle.

While MSMEs are exempt from direct EPR responsibilities, larger manufacturers and importers supplying raw materials must comply. Additionally, the government is investing in reverse logistics infrastructure, ensuring producers are responsible for post-consumer collection and recycling. These policies are accelerating the adoption of sustainable packaging innovations, while also fueling demand for films in retail, e-commerce, and food sectors, where durable, lightweight packaging formats are indispensable.

Japan: Plastic Resource Circulation and Positive List Regulation

The Japan stretch and shrink films market is undergoing rapid transformation under the Plastic Resource Circulation Strategy, which mandates that all packaging must be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law, also effective in 2025, enforces reduction or redesign of 12 types of single-use plastic products, further driving adoption of compostable and bio-based films.

In addition, the Ministry of Health, Labor and Welfare (MHLW) has implemented a positive list system effective June 1, 2025, identifying which synthetic materials are approved for food contact applications. This regulation is particularly critical for shrink and stretch films used in meat, dairy, and ready-to-eat food packaging, pushing manufacturers toward compliant, recyclable, and safe film formulations.

Brazil: Reverse Logistics and Circular Economy Practices

The Brazil stretch and shrink films market is evolving under the National Solid Waste Policy (PNRS), which enforces responsible disposal, reuse, and recycling. The enactment of Law No. 15,088 in January 2025, banning the import of plastic waste, has shifted focus toward domestic recycling and sustainable packaging practices.

The government’s reverse logistics initiatives are holding producers accountable for the post-consumer recycling of films, ensuring waste is reintroduced into the production cycle. The launch of the Recircula Brasil Platform, backed by the Brazilian Agency for Industrial Development and the Brazilian Association of the Plastics Industry, enables certification and traceability of recycled plastics. These frameworks are fostering a transparent and circular market ecosystem, encouraging adoption of recyclable and bio-based stretch and shrink films for both industrial and consumer packaging.

Stretch and Shrink Films Market Report Scope

Stretch and Shrink Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$19.5 Billion

|

|

Market Size (2034)

|

$31.8 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Resin Type (LDPE, LLDPE, PVC, PP, PET, Others), By Product Type (Stretch Films, Shrink Films, Stretch Hoods), By End-Use Industry (Food & Beverages, Consumer Goods, Logistics & Transportation, Pharmaceuticals & Medical Devices, Industrial Manufacturing, Building & Construction, Automotive)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Berry Global, Inc., Amcor plc, Sealed Air Corporation, Mondi Group, ProAmpac, Dow Inc., ExxonMobil Corporation, Mitsubishi Chemical Corporation, Sigma Plastics Group, Intertape Polymer Group Inc., Coveris Holdings S.A., Innovia Films, Bolloré S.E., Paragon Films, AEP Industries Inc. (part of Berry Global)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Stretch and Shrink Films Market Segmentation

By Resin Type

- LDPE

- LLDPE

- PVC

- PP

- PET

- Others

By Product Type

- Stretch Films

- Shrink Films

- Stretch Hoods

By End-Use Industry

- Food & Beverages

- Consumer Goods

- Logistics & Transportation

- Pharmaceuticals & Medical Devices

- Industrial Manufacturing

- Building & Construction

- Automotive

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Stretch and Shrink Films Market

- Berry Global, Inc.

- Amcor plc

- Sealed Air Corporation

- Mondi Group

- ProAmpac

- Dow Inc.

- ExxonMobil Corporation

- Mitsubishi Chemical Corporation

- Sigma Plastics Group

- Intertape Polymer Group Inc.

- Coveris Holdings S.A.

- Innovia Films

- Bolloré S.E.

- Paragon Films

- AEP Industries Inc. (part of Berry Global)

* List Not Exhaustive

Methodology

The Stretch and Shrink Films Market report by USDAnalytics has been developed using a comprehensive research methodology that combines primary and secondary data sources to deliver actionable insights for industry professionals. Primary research involved discussions with packaging engineers, R&D specialists, sustainability officers, and supply chain managers from leading companies such as Berry Global, Amcor, Mondi, and Sigma Stretch Film, focusing on innovations in resin technology, eco-friendly films, and high-performance applications. Secondary research included analysis of corporate filings, press releases, regulatory documents, trade publications, and scientific journals, with particular attention to trends in post-consumer recycled (PCR) content, down-gauging, and e-commerce-specific films. Market sizing and forecasts were derived through both top-down and bottom-up approaches, incorporating product types, resin types, end-use industries, and regional dynamics, while cross-verifying data through triangulation to ensure accuracy. The methodology also considered evolving regulations, sustainability mandates, and technological advancements in nanolayer, barrier, and tamper-evident films, providing a complete view of market drivers, opportunities, and competitive positioning for global stakeholders.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.