The global Structural Insulated Panels Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Facing Material (OSB, MgO Board, Others), By Insulation Material (EPS, XPS, Others), By Application (Floor, Wall, Roof), By End-User (Residential, Non-residential).

Structural insulated panels (SIPs) are prefabricated building components consisting of foam insulation sandwiched between oriented strand board (OSB) or plywood facings, offering superior thermal performance and structural strength compared to traditional construction methods. The future of the structural insulated panels market is influenced by several key trends, including advancements in construction technology, energy efficiency regulations, and sustainability initiatives. One significant trend is the growing demand for energy-efficient and sustainable building materials to meet stringent building codes and green building certifications. SIPs offer excellent thermal insulation properties, airtightness, and reduced thermal bridging, resulting in energy savings and improved indoor comfort in residential, commercial, and industrial buildings. Manufacturers are focusing on developing innovative SIP designs and production techniques that enhance structural integrity, fire resistance, and moisture management while reducing material waste and construction time. Additionally, the integration of renewable and recycled materials in SIP production, such as foam insulation derived from soy-based polyols and engineered wood products from sustainably managed forests, is addressing sustainability concerns and reducing the environmental impact of construction. Moreover, advancements in digital design and manufacturing technologies, such as computer-aided design (CAD) software and robotic fabrication, are enabling the customization and mass production of SIPs with complex geometries and high precision, further driving their adoption in modern construction practices. Furthermore, collaborations between SIP manufacturers, architects, and contractors are driving innovation and market expansion by offering integrated building systems that optimize energy performance, durability, and occupant comfort while reducing construction costs and environmental footprint.

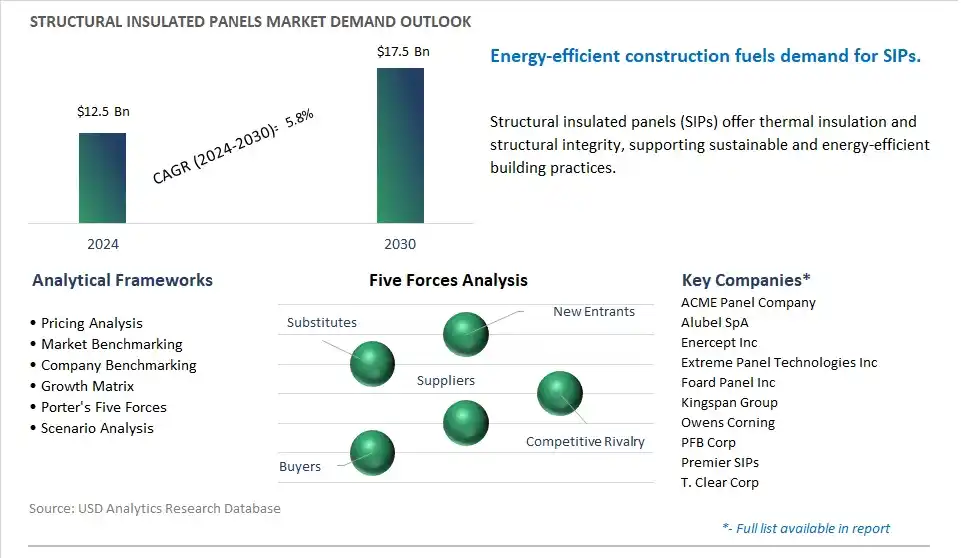

The market report analyses the leading companies in the industry including ACME Panel Company, Alubel SpA, Enercept Inc, Extreme Panel Technologies Inc, Foard Panel Inc, Kingspan Group, Owens Corning, PFB Corp, Premier SIPs, T. Clear Corp.

A prominent trend in the structural insulated panels (SIPs) market is the growing preference for energy-efficient construction materials. Structural insulated panels are composite building materials consisting of an insulating foam core sandwiched between two structural facings, typically made of oriented strand board (OSB) or plywood. SIPs offer superior thermal insulation properties compared to traditional construction materials, helping to reduce heating and cooling costs in buildings. With increasing awareness of environmental sustainability and energy conservation, there's a rising demand for building materials that contribute to energy-efficient and sustainable construction practices. This is driven by factors such as stricter building codes, green building certifications, and consumer preferences for energy-efficient homes and commercial buildings. Accordingly, the SIPs market is experiencing steady growth as architects, builders, and developers increasingly specify SIPs for new construction and retrofit projects.

The primary driver behind the structural insulated panels (SIPs) market's growth is the construction industry's emphasis on speed and efficiency. SIPs offer several advantages over traditional construction methods, including faster installation times, reduced labor costs, and simplified construction processes. The prefabricated nature of SIPs allows for rapid assembly on-site, leading to shorter construction timelines and faster project completions. In today's fast-paced construction environment, where project schedules are critical and labor shortages are common, SIPs provide a viable solution to meet tight deadlines and achieve efficient project delivery. This driver is significant as it aligns with the construction industry's priorities for productivity, cost-effectiveness, and project management, driving the adoption of SIPs in various residential, commercial, and industrial construction projects.

An attractive opportunity within the structural insulated panels (SIPs) market lies in the expansion into high-rise and multi-story buildings. While SIPs are commonly used in single-family homes, low-rise buildings, and commercial structures, there's potential to leverage SIP technology for taller and more complex construction projects. With advancements in SIP manufacturing processes, structural engineering design, and building code approvals, SIPs can now be engineered and tested for use in mid-rise and high-rise buildings. By targeting the high-rise construction market, SIP manufacturers can capitalize on the benefits of SIPs, such as lightweight construction, structural strength, and energy efficiency, to offer innovative solutions for urban development, affordable housing, and sustainable building projects. Additionally, there's an opportunity to collaborate with architects, engineers, and developers to showcase the advantages of SIPs in multi-story construction, thus expanding market reach and driving growth in the SIPs market.

The largest segment in the Structural Insulated Panels (SIPs) Market is OSB (Oriented Strand Board). OSB is widely recognized and accepted as a reliable and cost-effective facing material for SIPs. It provides excellent structural strength, dimensional stability, and moisture resistance, making it suitable for various building applications. Additionally, OSB is readily available and manufactured from sustainable wood resources, contributing to its popularity in the construction industry. Further, OSB offers compatibility with a wide range of insulation materials, such as expanded polystyrene (EPS) or polyisocyanurate (PIR), allowing for customized thermal performance to meet specific building requirements. Furthermore, OSB's versatility and ease of installation make it a preferred choice for both residential and commercial construction projects. Accordingly, the OSB segment is the largest in the Structural Insulated Panels Market due to its widespread availability, structural performance, and cost-effectiveness compared to other facing materials like MgO board or alternatives.

The fastest-growing segment in the Structural Insulated Panels (SIPs) Market is EPS (Expanded Polystyrene) insulation material. This growth is driven by Diverse key factors. EPS offers excellent thermal insulation properties, effectively reducing heat transfer and improving energy efficiency in buildings. With increasing emphasis on sustainable and energy-efficient construction practices, EPS has gained popularity as a preferred insulation material among builders, architects, and homeowners. Additionally, EPS is lightweight, easy to handle, and cost-effective compared to other insulation materials like XPS (Extruded Polystyrene) or alternatives, making it an attractive choice for SIPs manufacturing. Further, EPS is highly versatile and compatible with various facing materials and construction methods, allowing for customized solutions to meet specific project requirements. Furthermore, EPS insulation panels can contribute to green building certifications and compliance with energy codes and standards, further driving their adoption in the construction industry. Accordingly, the EPS segment is experiencing rapid growth in the Structural Insulated Panels Market, propelled by its superior thermal performance, affordability, and versatility in sustainable building applications.

The fastest-growing segment in the Structural Insulated Panels (SIPs) Market is the Wall application. This growth is driven by Diverse key factors. walls represent a significant portion of a building's envelope and play a crucial role in providing structural support, thermal insulation, and weather resistance. SIPs used for wall applications offer numerous advantages over traditional building materials, including faster construction times, improved energy efficiency, and enhanced structural performance. Additionally, the rising demand for sustainable and energy-efficient construction solutions has led to increased adoption of SIPs for wall construction in residential, commercial, and industrial buildings. Further, advancements in SIPs technology, such as improved panel designs, insulation materials, and installation methods, have further fueled their popularity for wall applications. Furthermore, regulatory incentives, building codes, and green building certifications promoting energy-efficient building practices have contributed to the growing adoption of SIPs for wall construction. Accordingly, the wall application segment is experiencing rapid growth in the Structural Insulated Panels Market, driven by its importance in building construction and the numerous benefits SIPs offer for wall applications.

By Facing Material

OSB

MgO Board

Others

By Insulation Material

EPS

XPS

Others

By Application

Floor

Wall

Roof

By End-User

Residential

Non-residential

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

ACME Panel Company

Alubel SpA

Enercept Inc

Extreme Panel Technologies Inc

Foard Panel Inc

Kingspan Group

Owens Corning

PFB Corp

Premier SIPs

T. Clear Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Structural Insulated Panels Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Structural Insulated Panels Market Size Outlook, $ Million, 2021 to 2030

3.2 Structural Insulated Panels Market Outlook by Type, $ Million, 2021 to 2030

3.3 Structural Insulated Panels Market Outlook by Product, $ Million, 2021 to 2030

3.4 Structural Insulated Panels Market Outlook by Application, $ Million, 2021 to 2030

3.5 Structural Insulated Panels Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Structural Insulated Panels Industry

4.2 Key Market Trends in Structural Insulated Panels Industry

4.3 Potential Opportunities in Structural Insulated Panels Industry

4.4 Key Challenges in Structural Insulated Panels Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Structural Insulated Panels Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Structural Insulated Panels Market Outlook by Segments

7.1 Structural Insulated Panels Market Outlook by Segments, $ Million, 2021- 2030

By Facing Material

OSB

MgO Board

Others

By Insulation Material

EPS

XPS

Others

By Application

Floor

Wall

Roof

By End-User

Residential

Non-residential

8 North America Structural Insulated Panels Market Analysis and Outlook To 2030

8.1 Introduction to North America Structural Insulated Panels Markets in 2024

8.2 North America Structural Insulated Panels Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Structural Insulated Panels Market size Outlook by Segments, 2021-2030

By Facing Material

OSB

MgO Board

Others

By Insulation Material

EPS

XPS

Others

By Application

Floor

Wall

Roof

By End-User

Residential

Non-residential

9 Europe Structural Insulated Panels Market Analysis and Outlook To 2030

9.1 Introduction to Europe Structural Insulated Panels Markets in 2024

9.2 Europe Structural Insulated Panels Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Structural Insulated Panels Market Size Outlook by Segments, 2021-2030

By Facing Material

OSB

MgO Board

Others

By Insulation Material

EPS

XPS

Others

By Application

Floor

Wall

Roof

By End-User

Residential

Non-residential

10 Asia Pacific Structural Insulated Panels Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Structural Insulated Panels Markets in 2024

10.2 Asia Pacific Structural Insulated Panels Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Structural Insulated Panels Market size Outlook by Segments, 2021-2030

By Facing Material

OSB

MgO Board

Others

By Insulation Material

EPS

XPS

Others

By Application

Floor

Wall

Roof

By End-User

Residential

Non-residential

11 South America Structural Insulated Panels Market Analysis and Outlook To 2030

11.1 Introduction to South America Structural Insulated Panels Markets in 2024

11.2 South America Structural Insulated Panels Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Structural Insulated Panels Market size Outlook by Segments, 2021-2030

By Facing Material

OSB

MgO Board

Others

By Insulation Material

EPS

XPS

Others

By Application

Floor

Wall

Roof

By End-User

Residential

Non-residential

12 Middle East and Africa Structural Insulated Panels Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Structural Insulated Panels Markets in 2024

12.2 Middle East and Africa Structural Insulated Panels Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Structural Insulated Panels Market size Outlook by Segments, 2021-2030

By Facing Material

OSB

MgO Board

Others

By Insulation Material

EPS

XPS

Others

By Application

Floor

Wall

Roof

By End-User

Residential

Non-residential

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

ACME Panel Company

Alubel SpA

Enercept Inc

Extreme Panel Technologies Inc

Foard Panel Inc

Kingspan Group

Owens Corning

PFB Corp

Premier SIPs

T. Clear Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Facing Material

OSB

MgO Board

Others

By Insulation Material

EPS

XPS

Others

By Application

Floor

Wall

Roof

By End-User

Residential

Non-residential

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Global Structural Insulated Panels is forecast to reach $17.5 Billion in 2030 from $12.5 Billion in 2024, registering a CAGR of 5.8%

Emerging Markets across Asia Pacific, Europe, and Americas present robust growth prospects.

ACME Panel Company, Alubel SpA, Enercept Inc, Extreme Panel Technologies Inc, Foard Panel Inc, Kingspan Group, Owens Corning, PFB Corp, Premier SIPs, T. Clear Corp

Base Year- 2023; Estimated Year- 2024; Historic Period- 2018-2023; Forecast period- 2024 to 2030; Currency: Revenue (USD); Volume