Superalloys Market Overview: High-Temperature Alloys Powering Aerospace and Power Generation Growth

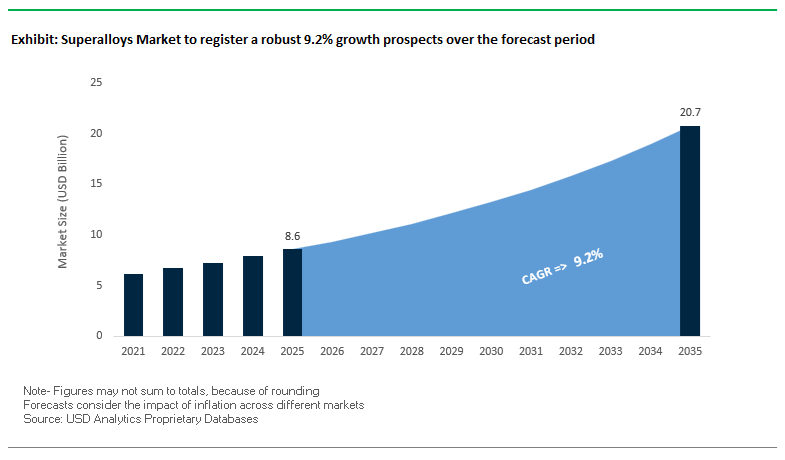

The global Superalloys Market is projected to grow from USD 8.6 billion in 2025 to USD 20.7 billion by 2035, registering a strong CAGR of 9.2% (2025–2035). This expansion is driven by surging demand for nickel-based superalloys in gas turbine engines, aerospace hot-section components, and advanced power generation systems, where extreme temperature and creep resistance are non-negotiable. For manufacturers and vendors, the superalloys industry remains structurally attractive due to high entry barriers, proprietary compositions, and long qualification cycles with OEMs, particularly in aerospace and energy.

Modern nickel-based superalloys used in the hottest sections of advanced gas turbine engines (first-stage blades and vanes) are engineered to retain mechanical integrity and creep resistance at operating temperatures above 1,100°C (2,012°F)—typically 100–200°C higher than many high-strength steels. In the power generation sector, these alloys must deliver extremely low creep rates (≤10⁻⁸ s⁻¹) over service lives exceeding 10,000 hours, with performance closely linked to the density and stability of the γ′ (gamma-prime) strengthening phase. High-performance aerospace superalloys are predominantly nickel-based, typically containing 50–75% nickel by mass, reinforcing the strategic importance of secure nickel supply chains.

Single-crystal (SX) superalloy technology is a major competitive differentiator, eliminating grain boundaries and delivering up to 30% improvement in creep rupture life and ~25°C higher temperature capability versus directionally solidified alloys. In parallel, superalloy producers are investing over USD 50 million annually in additive manufacturing (AM)-grade nickel alloy powders, optimized for laser powder bed fusion and other 3D printing processes, enabling complex, near-net-shape turbine and engine geometries that reduce downstream machining costs and scrap.

Key market insights for superalloy manufacturers and vendors:

- Extreme temperature capability: Nickel-based superalloys reliably operate above 1,100°C, securing their position in jet engines and industrial gas turbines.

- Creep resistance as a design gate: Creep rate targets of ≤10⁻⁸ s⁻¹ over 10,000+ hours are central to alloy design for power generation superalloys.

- Nickel-intensive alloy portfolio: Typical 50–75% nickel content reinforces upstream dependency on critical nickel supply and pricing.

- Single-crystal superalloys advantage: SX turbine blades provide up to 30% longer creep life and higher firing temperatures, directly improving engine efficiency.

- Additive manufacturing growth: AM-grade nickel superalloy powders attract USD 50M+ yearly investments, supporting 3D printed turbine and engine hardware.

Superalloys Market Analysis: Aerospace Backlogs, AM Powders, and Critical Minerals Shape Growth

The global superalloys industry is being reshaped by the convergence of aerospace production ramp-ups, additive manufacturing adoption, and tighter performance requirements in power and space applications. In 2024, Haynes International reported advances in its HAYNES® 282® alloy, demonstrating improved creep and low-cycle fatigue (LCF) resistance for high-temperature structural components in aero and industrial gas turbines. Around the same period in 2024, EOS expanded the superalloys landscape for industrial 3D printing with the launch of EOS NickelAlloy IN738 and EOS K500, giving turbine OEMs and tier suppliers more options to design complex, weight-optimized hot-section parts directly for additive manufacturing. These developments accelerate a broader shift toward AM-optimized nickel-based superalloys that can withstand aggressive thermal cycles while enabling more efficient, integrated component designs.

The commercial aerospace backlog is a structural tailwind for the superalloys market. In 2025, publicly reported data indicated that Boeing’s aircraft backlog approached 6,000 aircraft, signaling a long runway of demand for nickel-based superalloys in jet engine disks, blades, vanes, and structural components. In July 2025, Airbus recorded 501 gross orders year-to-date and delivered 67 aircraft in that month alone, reinforcing the steady pull for advanced superalloys across engine and hot-structure supply chains. In April 2025, QuesTek further highlighted innovation momentum by developing a new nickel superalloy tailored for additive manufacturing and extreme high-pressure, high-temperature conditions for Stoke Space’s reusable rocket engines, demonstrating how space launch markets are becoming an additional growth vector for high-performance superalloys.

Policy, research funding, and raw material security are also playing a central role in market dynamics. In 2025, the National Science Foundation (NSF) awarded a USD 459,000 grant for a two-year research project focused on advanced manufacturing of high-strength metal alloys, directly supporting new processing routes and microstructural control for superalloys. The same year, key alloying elements such as rhenium and tungsten were included on the Critical Minerals List, underscoring the strategic importance and supply risk associated with superalloy chemistries. Industry leaders like VDM Metals are responding by emphasizing ultra-clean melting strategies such as triple-melt routes (VIM/ESR/VAR) for alloys like VDM® Alloy 718, ensuring the high purity and exact chemical analysis required for rotating aerospace components. These combined factors—OEM order backlogs, AM material innovation, critical mineral policy focus, and advanced melting processes—establish a robust, technology-intensive growth environment for the global superalloys market through 2035.

Breakthrough Trends Driving Hydrogen-Turbine Qualification and Additive Manufacturing of Advanced Superalloy Components

Market Trend 1: Qualification of Next-Generation Superalloys for Hydrogen Combustion Turbines and Advanced Nuclear Reactor Systems

The Superalloys Market is experiencing a fundamental shift driven by the urgent need for materials that meet the extreme mechanical and chemical demands of hydrogen-fueled turbines and Generation IV nuclear reactors. Engineering teams are modifying nickel-based alloy chemistries—often reducing iron or altering Cr/Ni ratios—to achieve hydrogen embrittlement resistance, maintaining <5% loss in fracture ductility even under >20 MPa hydrogen pressures at elevated temperatures. This represents a major improvement over legacy alloys such as Inconel 718, which degrade rapidly under hydrogen exposure.

Next-generation superalloys designed for molten salt reactor (MSR) environments must also demonstrate exceptional corrosion resistance. Modified variants of Hastelloy N, for example, are achieving corrosion rates below 10 μm/year in fluoride or chloride molten salts at 700°C, even after thousands of test hours—critical for meeting multi-decade reactor reliability targets.

At the turbine level, cutting-edge single-crystal superalloys now operate at turbine inlet temperatures of 1,550°C, exceeding the first-generation alloys’ service temperature by 150–200°C. These materials must simultaneously meet structural longevity requirements, with nuclear-grade superalloys attaining creep rupture lives >10,000 hours at temperatures above 650°C while sustaining high stress loads. These performance milestones are enabling elevated thermal efficiency, lower emissions, and longer component lifetimes across energy sectors.

Market Trend 2: Additive Manufacturing Adoption for Near-Net-Shape Superalloy Production and Precision Repair

Additive Manufacturing (AM) is redefining superalloy component manufacturing and life-extension strategies. After Hot Isostatic Pressing (HIP), AM versions of high-value alloys such as Inconel 718 exhibit fatigue performance equivalent or superior to wrought material, provided porosity and lack-of-fusion defects are minimized. This has accelerated certification of AM-produced turbine components, combustor hardware, and heat-resistant aerospace structures.

AM also enables precision repair of superalloy turbine blades using Directed Energy Deposition (DED). Qualified repairs of alloys such as GTD-111 must produce a weld zone with hardness variation <5% from the parent material while restoring the critical γ′/γ microstructure, ensuring mechanical compatibility across the repaired region.

Moreover, AM directly improves material efficiency. While conventional forging or subtractive machining often results in a 10:1 to 20:1 buy-to-fly ratio, AM can reduce this to 2:1 or 3:1, drastically reducing waste for ultra-expensive superalloy feedstock. AM also overcomes traditional casting barriers, enabling production of parts with wall thicknesses as low as 0.5 mm—revolutionizing turbine cooling architecture and heat-exchanger designs that were previously unmanufacturable.

Strategic Opportunities in Cobalt-Free Alloy Development and AI-Enabled Digital Alloy Design

Market Opportunity 1: Commercialization of Cobalt-Free and Reduced-Co Superalloys to Strengthen Supply Chain Security

Geopolitical and price volatility in cobalt supply is accelerating the shift toward Co-reduced and Co-free superalloys, particularly for gas turbines, aerospace engines, and industrial heat exchangers. Conventional superalloys like Mar-M247 contain 10–20 wt% cobalt, providing key solid-solution strengthening and stabilizing γ′ precipitation. However, new alloy formulations are achieving near-equivalent performance without cobalt.

Optimized Cr, Al, Ta, and Mo chemistries in Co-free superalloys have demonstrated creep rupture life at 900°C and 100 MPa within 10% of cobalt-containing counterparts. To maintain long-term microstructural stability, alloy designers must adjust compositions to avoid formation of brittle phases such as σ and μ phases during prolonged exposure above 850°C. Beyond performance and supply chain improvements, reduced cobalt content lowers alloy density, providing small but meaningful weight reductions in rotating components—an efficiency multiplier for aerospace and energy systems.

Market Opportunity 2: AI-Driven Digital Alloy Design and ICME Platforms for Predictive Microstructure and Lifetime Engineering

The rise of AI-powered alloy design represents a transformational opportunity for next-generation superalloy development. Integrated Computational Materials Engineering (ICME), combined with high-fidelity Machine Learning (ML) models, can now predict γ′ precipitate size and volume fraction after complex heat treatments with ≥90% accuracy, reducing material iteration cycles that previously required months of experimental work.

Process optimization is also being dramatically accelerated. AI-driven models can determine optimal forging temperatures and strain rates that achieve target grain sizes—compressing development time from dozens of trials to one or two. Property prediction is similarly advancing: ICME platforms estimate key metrics such as UTS, hardness, or oxidation resistance with <5% RMSE, de-risking experimental alloy development and enabling rapid prototyping of previously untested chemistries.

Advanced lifecycle modeling further extends component reliability. ML algorithms trained on high-throughput creep, fatigue, and oxidation datasets can now predict remaining useful life (RUL) of in-service superalloy components with <15% uncertainty at failure, enabling predictive maintenance for turbines, reactors, and industrial furnaces. This digital transformation stands to redefine materials engineering, cutting cost, time-to-market, and operational risk.

Superalloys Market Share Analysis

Market Share by Base Material: Nickel-Based Superalloys Dominate High-Temperature Turbine and Propulsion Applications

Nickel-based superalloys hold the dominant share of the global superalloys market—approximately 65% in 2025—because they deliver unmatched mechanical strength, creep resistance, and oxidation stability in extreme temperature environments where alternative materials fail. Their unique γ′ (gamma prime) strengthening mechanism, formed by Ni₃(Al,Ti) precipitates coherently embedded in the nickel matrix, enables these alloys to maintain structural integrity and mechanical strength at temperatures approaching 1,000°C—conditions typical of modern jet engine hot sections and industrial gas turbine combustion chambers. This microstructural stability directly improves turbine inlet temperatures (TIT), allowing higher thermal efficiency, reduced fuel burn, and lower emissions in next-generation aero-engines and power-generation turbines. Nickel-based alloys also exhibit superior oxidation and corrosion resistance due to the formation of self-healing alumina and chromia layers, enabling reliable long-term performance in corrosive, high-velocity exhaust gas environments. Single-crystal (SC) and directionally solidified (DS) turbine blade alloys, which represent the highest performance tier in the market, are exclusively nickel-based, further reinforcing the segment’s leadership. As global aerospace production ramps back up and industrial gas turbine capacity expands to support grid reliability and hydrogen-ready turbines, nickel-based superalloys remain the backbone of the industry, driving the majority of total market revenue.

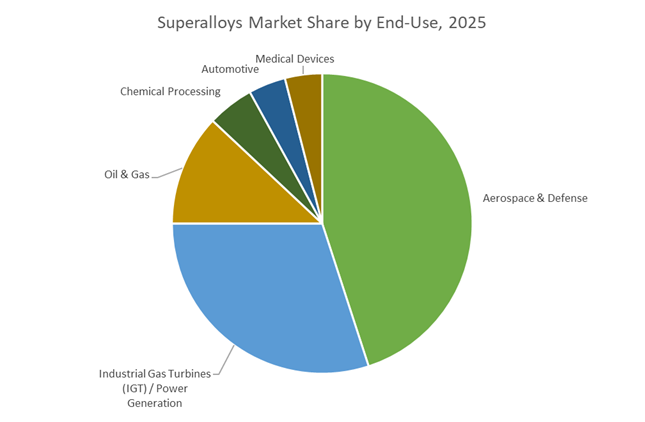

Market Share by End-Use: Aerospace & Defense Leads Superalloy Consumption Through High-Performance Engine Requirements

The Aerospace & Defense sector accounts for roughly 45% of global superalloy demand, reflecting the critical dependence of modern propulsion systems on materials that can withstand extreme thermal and mechanical loading. Jet engines, rocket engines, and advanced military propulsion units rely heavily on nickel-based superalloys for turbine blades, vanes, discs, and combustion liners—components that must endure high-pressure, high-temperature environments while maintaining fatigue resistance and creep stability throughout long service cycles. The industry’s relentless push toward higher bypass ratios, hotter turbine inlet temperatures, and improved fuel efficiency directly correlates with increased consumption of advanced superalloys, including single-crystal variants engineered for maximum creep life and temperature capability. Commercial aircraft programs such as the Boeing 787, Airbus A350, and upcoming next-generation narrow-body platforms, alongside rising global defense procurement, are driving sustained demand for high-performance superalloy components. Modernization of fighter jet fleets, growth in space propulsion, and increasing production of auxiliary power units (APUs) further reinforce aerospace dominance. Given the catastrophic consequences of material failure in propulsion systems, aerospace remains the most material-intensive application for superalloys and continues to shape innovation, alloy development, and high-value manufacturing within the global market.

Country Analysis: Global Drivers in Superalloys Development

United States: Aerospace Engine Demand, High-Temperature Alloy Innovation, and Additive Manufacturing Expansion

The United States continues to solidify its position as the global leader in Superalloys, driven by large-scale aerospace investments, aggressive modernization of defense fleets, and a thriving ecosystem for high-temperature materials R&D. A major milestone was ATI’s five-year, $1 billion supply contract with Airbus (2025), which not only reaffirms U.S. dominance in the aerospace superalloy supply chain but also necessitates further expansion of melting, forging, and precision mill product capacity. This is supported by ATI’s $260–$280 million CapEx program for 2025, with $72 million invested in Q2 alone, channelled toward advanced production lines for nickel-based superalloy mill products used in jet engine discs, cases, and rotating components that operate at extreme temperatures.

Complementing this industrial expansion, Haynes International introduced the HAYNES® 292™ alloy in July 2025, a next-generation gamma-prime–strengthened superalloy engineered for high-temperature structural stability in both aircraft and industrial gas turbine (IGT) engines. The U.S. government further amplifies domestic innovation through DOE-funded research in Additive Manufacturing (AM), targeting the qualification of AM nickel-based superalloys for complex, near-net-shape engine components—an essential step for reducing weight, enhancing thermal efficiency, and minimizing scrap. The U.S. defense sector, led by Lockheed Martin and GE Aviation, remains one of the largest consumers of superalloys globally, driving demand for turbine blades, combustor components, and mission-critical rotating parts across next-generation fighter jets and upgraded propulsion systems.

China: Expanding High-End Superalloy Output and Strengthening Gas Turbine Manufacturing Capabilities

China is rapidly transforming into a major force in the global Superalloys Market, driven by its accelerating aerospace programs and rising energy sector demands. The expansion of indigenous aircraft such as the COMAC C919 and advanced military jets is significantly increasing domestic consumption of nickel-based and cobalt-based superalloys required for turbine blades, discs, and high-temperature engine components. Simultaneously, the ambitious growth of China’s Industrial Gas Turbine (IGT) infrastructure—critical for power generation and pipeline compression—is prompting large-scale investment in creep-resistant, oxidation-resistant superalloys to support long-duration, high-temperature operations.

China is also investing aggressively in Powder Metallurgy (PM) and Additive Manufacturing (AM) for superalloys, aiming to match the performance of Western-certified turbine components. State-backed institutions are pursuing R&D that enhances powder quality, microstructure control, and fatigue performance. These innovations are designed to reduce dependency on imported engine components and support China’s long-term strategic goal of achieving aerospace and energy sector self-sufficiency. As China's heavy industrial base continues to mature, its role in supplying, consuming, and innovating high-performance superalloys is set to expand dramatically.

European Union (Germany/France/UK): Engine Modernization, Circular Recycling Models, and AM Superalloy Commercialization

Europe is advancing as a center for high-performance superalloy engineering, fueled by large-scale engine modernization programs across the region. A major highlight is Rolls-Royce’s £55 million investment (March 2024) in expanding build capacity at facilities in the UK and Germany, supporting a 40%+ increase in engine production starting 2025 for the Trent series and future propulsion platforms. This expansion directly accelerates demand for forged, cast, and additively manufactured superalloy components capable of withstanding extreme thermal and mechanical stresses.

Europe is also emerging as a leader in superalloy recycling and circularity, aligning with EU sustainability legislation. Companies like Aperam Recycling (ELG) are partnering with IperionX to establish a closed-loop, low-carbon titanium and superalloy recycling supply chain, enabling the recovery and reprocessing of high-value scrap from aerospace manufacturing. Meanwhile, EOS’s introduction of IN738 and K500 nickel-based powders (2024) has invigorated the AM ecosystem by commercializing superalloys traditionally limited to casting processes, allowing European companies to adopt PBF-LB for turbine vanes, combustor parts, and hot-section components. With joint ventures such as Rolls-Royce–Safran (2023) targeting ultra-low-emission next-generation engines, Europe remains a critical hub for lightweight, heat-resistant superalloy innovation.

India: Accelerated Defense Localization and Aerospace Manufacturing Through ‘Make in India’ Programs

India is rapidly strengthening its position in the Superalloys Market through targeted government-driven localization programs and strategic partnerships with global aerospace leaders. A key breakthrough occurred in October 2025, when Rolls-Royce expanded its partnership with Bharat Forge to manufacture fan blades for the Pearl 700 and Pearl 10X engines. This move doubles Rolls-Royce’s sourcing from India by 2030 and demands the domestic capability to produce high-integrity superalloy components with tight tolerance and high-temperature performance.

India’s defense manufacturing ecosystem continues to rely heavily on MIDHANI (Mishra Dhatu Nigam Limited), a critical PSU specializing in superalloy development for military aircraft, missile propulsion systems, naval platforms, and strategic programs. MIDHANI’s ongoing efforts to indigenize superalloys reduce dependence on foreign suppliers and accelerate the country’s aerospace self-reliance under “Atmanirbhar Bharat.” With rising domestic aircraft requirements, expanding MRO services, and increasing collaboration with global engine OEMs, India is entering a new phase of strategic capability-building in high-temperature superalloys.

Competitive Landscape of the Global Superalloys Market: Integrated Producers and Specialty Alloy Leaders

The global superalloys competitive landscape is dominated by a mix of integrated specialty metals producers and high-performance alloy specialists that supply critical materials for aerospace, power generation, and emerging applications such as space and advanced AM. Companies like ATI, Haynes International, VDM Metals, Howmet Aerospace, and Carpenter Technology collectively shape the superalloys ecosystem—from nickel-based and cobalt-based alloy design to melting, forging, investment casting, and powder production. Their capabilities in vacuum melting, triple-melt processes, single-crystal casting, and high-purity powder atomization set the benchmark for quality, reliability, and long-term partnerships with jet engine OEMs, turbine manufacturers, and advanced manufacturing users.

ATI drives high-performance nickel and cobalt superalloy solutions for aerospace

Allegheny Technologies Incorporated (ATI) is a major global producer of specialty materials, with strong integration across the aerospace superalloys supply chain. The company is a leading supplier of nickel- and cobalt-based superalloys such as Waspaloy and ATI® 718, delivered in bar, billet, and plate forms for critical jet engine components. ATI operates using an integrated business model, controlling the flow from primary melting through to forgings and precision components, which supports consistent quality and full traceability—core requirements in aerospace and defense. Strategic focus on these markets is evident, with around 66% of Q1 2025 revenue derived from aerospace and defense, emphasizing its heavy exposure to superalloys. To support long-term aircraft production backlogs, ATI continues to invest in advanced specialty metals facilities, expanding capacity to meet sustained demand for high-temperature alloys.

Haynes International strengthens its position with proprietary high-temperature superalloys

Haynes International, Inc. is a specialized producer of high-performance nickel- and cobalt-based superalloys, with a strong emphasis on alloy innovation. Its portfolio includes the HAYNES® and HASTELLOY® families, such as HAYNES® 282® for gas turbine cases and rings and HASTELLOY® X for combustion components, meeting stringent high-temperature and corrosion-resistance needs. Haynes’ core strength lies in creep and oxidation performance—its HAYNES® 230® alloy combines exceptional high-temperature strength with oxidation resistance up to 1,149°C (2,100°F), serving as a benchmark for industrial gas turbines. Strategically, Haynes positions its alloys as enabling technologies for emerging power systems, including advanced ultra-supercritical power plants and supercritical CO₂ power cycles. The company also continues to expand its R&D pipeline with alloys such as HAYNES® 244®, targeted at static parts in advanced gas turbine engines requiring low thermal expansion up to 760°C, further reinforcing its role as an innovation leader.

VDM Metals leverages triple-melt purity for aerospace-grade superalloys

VDM Metals GmbH is a key European supplier of nickel and cobalt alloys, serving both the aerospace and chemical processing industries. The company delivers high-quality semi-finished products such as rods, bars, and plates in alloys like VDM® Alloy 718 and VDM® Alloy 625, widely used in engine manufacturing and turbine components. A defining capability of VDM Metals is its use of triple-melt processes—Vacuum Induction Melting (VIM), Electro-Slag Remelting (ESR), and Vacuum Arc Remelting (VAR)—to achieve the ultra-high purity and microstructural homogeneity required for rotating aerospace parts. VDM’s materials are deployed across both non-rotating casings and rotating parts such as turbine discs, where resistance to creep, fatigue, and crack propagation is essential. Strategically, the company directly links its superalloy portfolio to critical aerospace performance attributes, emphasizing creep strength, low crack growth rates, and high fatigue behavior to maintain its position as a trusted supplier to leading engine OEMs.

Howmet Aerospace leads in single-crystal and directionally solidified superalloy components

Howmet Aerospace Inc. specializes not only in superalloy materials but in complex, finished components for the aerospace and power generation markets. It is a global leader in precision investment castings and forged components made from nickel-based superalloys, including single-crystal (SX) and directionally solidified (DS) turbine blades and vanes. These advanced superalloy components are critical in maximizing the high-temperature efficiency of jet engine hot sections, where thermal margins and durability are tightly constrained. Financial results demonstrate the strength of this positioning—Howmet reported 17% commercial aerospace sales growth in Q3 2024, largely driven by rising demand for its titanium and superalloy structural castings and engine components. The company is a primary supplier to the global single-crystal turbine blade market, a premium niche with a significant global value, underlining Howmet’s focus on high-margin, performance-critical superalloy solutions.

Carpenter Technology expands high-purity superalloy bar and powder for AM and aerospace

Carpenter Technology Corporation focuses on specialty alloys, powders, and advanced manufacturing, playing a vital role in the superalloys market for both traditional and additive processes. It supplies premium nickel- and cobalt-based superalloys in bar, wire, and billet forms—such as Waspaloy and Inconel® 718—serving fasteners, rings, and other non-rotating airframe and engine components where high strength at intermediate temperatures is crucial. A major strategic pillar for Carpenter is additive manufacturing, where it is ramping up production of high-quality spherical superalloy powders to capture growth in the 3D printing nickel alloy powder market, forecast around USD 81 million in 2025. The company leverages deep expertise in Vacuum Induction Melting (VIM) and Electro-Slag Remelting (ESR) to ensure exceptional cleanliness and microstructural integrity. This focus on certified, high-purity material makes Carpenter a preferred supplier for safety-critical aerospace and industrial applications that demand consistent performance and full traceability.

Superalloys Market Report Scope

Superalloys Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.6 Billion

|

|

Market Size (2035)

|

$20.7 Billion

|

|

Market Growth Rate

|

9.2%

|

|

Segments

|

By Base Material (Nickel-Based Superalloys, Cobalt-Based Superalloys, Iron-Based Superalloys), By Alloy Structure/Type (Wrought Superalloys, Cast Superalloys, Directionally Solidified Superalloys, Single-Crystal Superalloys), By Manufacturing Process (Casting, Forging, Powder Metallurgy, Additive Manufacturing), By End-Use Application (Aerospace & Defense, Industrial Gas Turbines & Power Generation, Oil & Gas, Automotive, Chemical Processing, Medical Devices)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Precision Castparts Corp/Special Metals, Allegheny Technologies, Haynes International, Carpenter Technology, VDM Metals, Aperam, Howmet Aerospace, Doncasters Group, Aubert & Duval, VSMPO-AVISMA, IHI Corporation, Proterial, MIDHANI, Nippon Yakin Kogyo, Cannon-Muskegon

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Superalloys Market Segmentation

By Base Material

- Nickel-Based Superalloys

- Cobalt-Based Superalloys

- Iron-Based Superalloys

By Alloy Structure / Type

- Wrought Superalloys

- Cast Superalloys

- Directionally Solidified (DS) Superalloys

- Single-Crystal (SC) Superalloys

By Manufacturing Process

- Casting (Investment Casting)

- Forging

- Powder Metallurgy (PM)

- Additive Manufacturing (3D Printing)

By End-Use Industry

- Aerospace & Defense

- Industrial Gas Turbines / Power Generation

- Oil & Gas

- Automotive

- Chemical Processing

- Medical Devices

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Superalloys Market

- Precision Castparts Corp / Special Metals

- Allegheny Technologies (ATI)

- Haynes International

- Carpenter Technology

- VDM Metals

- Aperam

- Howmet Aerospace

- Doncasters Group

- Aubert & Duval

- VSMPO-AVISMA

- IHI Corporation

- Proterial (Hitachi Metals)

- MIDHANI

- Nippon Yakin Kogyo

- Cannon-Muskegon

*- List not Exhaustive

Research Coverage: Superalloys Market

The latest Superalloys Market study from USDAnalytics delivers a rigorous, decision-ready assessment of how high-temperature alloys are reshaping aerospace, energy, and advanced manufacturing value chains. Drawing on global project pipelines and OEM qualification activity, this report investigates the shifting balance between nickel-based, cobalt-based, and iron-based superalloys as engine firing temperatures rise and duty cycles tighten. It highlights next-generation single-crystal turbine materials, hydrogen-ready gas turbine alloys, and AM-optimized nickel powders, while our analysis reviews OEM order backlogs, raw material exposure to critical minerals, and technology roadmaps across major producers. The study tracks breakthroughs in creep-resistant chemistries, triple-melt purity routes, and additive manufacturing use cases that are redefining performance benchmarks in jet engines, industrial gas turbines, space propulsion, and high-efficiency power systems. By combining quantitative outlooks with qualitative insights on supply risk, qualification cycles, and competitive strategies, this report is an essential resource for aerospace engine makers, turbine OEMs, alloy producers, investors, and policymakers seeking to understand where the superalloys market is heading and which technologies will capture the next decade of value creation.

Scope Highlights

- Segmentation

By Base Material: Nickel-Based Superalloys, Cobalt-Based Superalloys, Iron-Based Superalloys

By Alloy Structure / Type: Wrought Superalloys, Cast Superalloys, Directionally Solidified (DS) Superalloys, Single-Crystal (SC) Superalloys

By Manufacturing Process: Casting (Investment Casting), Forging, Powder Metallurgy (PM), Additive Manufacturing (3D Printing)

By End-Use Industry: Aerospace & Defense, Industrial Gas Turbines / Power Generation, Oil & Gas, Automotive, Chemical Processing, Medical Devices

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Horizon: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies Covered: Analysis / profiles of 15+ companies across the superalloys ecosystem, including integrated producers, casting specialists, and AM powder suppliers.