Sustainable Aerosol Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Sustainable Aerosol Packaging Market Poised to Reach $2.7 Billion by 2034 Driven by Circular Economy and Lightweight Innovations

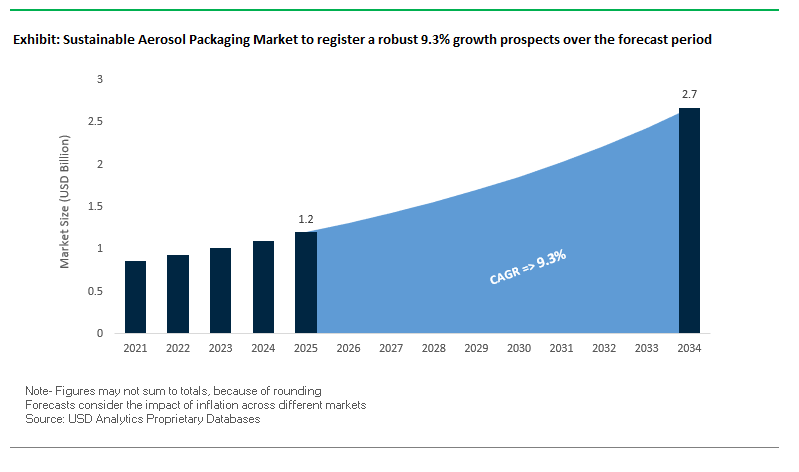

The global sustainable aerosol packaging market is projected to grow from $1.2 billion in 2025 to $2.7 billion by 2034, reflecting a CAGR of 9.3%. This market is undergoing rapid transformation as manufacturers adopt eco-friendly materials, innovative dispensing systems, and greener propellants to meet consumer and regulatory demand. Sustainable aerosol solutions are increasingly critical for brands seeking to demonstrate environmental responsibility while maintaining product performance and safety.

Key Insights for Industry Professionals:

- High recyclability of metal aerosol cans positions aluminum and steel as preferred materials in circular economy strategies.

- Lightweighting and material reduction innovations reduce raw material use and transportation emissions, supporting carbon footprint reduction.

- Greener propellants, such as nitrogen and compressed air, are replacing HFCs to meet stringent VOC and environmental regulations.

- Innovative actuators and dispensing systems improve spray performance, minimize product waste, and introduce refillable or reusable options.

- Increasing focus on sustainable manufacturing and certifications reinforces brand reputation and compliance with evolving global environmental standards.

Sustainable aerosol packaging is emerging as a strategic enabler for companies aiming to balance consumer experience, environmental impact, and regulatory compliance.

Market Analysis: Key Developments Highlight the Integration of Recyclable Materials and Refillable Solutions in Aerosol Packaging

The sustainable aerosol packaging industry is experiencing strong momentum, driven by advancements in materials, propellants, and actuator design. In August 2025, Wild launched a refillable roll-on deodorant, reflecting the broader trend of reusable and eco-friendly personal care packaging. Similarly, Mondi and Krones partnered to produce Hug&Hold, a paper-based alternative to plastic shrink wrap, demonstrating cross-industry innovation in sustainable packaging formats.

Academic and industrial research continues to support market innovation. In July 2025, a review highlighted the use of advanced additives to enhance mechanical strength and antimicrobial properties of sustainable films. The April 2025 launch of LINDAL Group’s FlipStraw dual spray actuator introduced a foldable straw design that improves functionality and reduces product waste, while Cif Infinite Clean leveraged microbiome technology to create advanced formulations requiring protective packaging.

Corporate investments and certifications further underscore sustainability priorities. Ball Corporation’s February 2025 investment in Meadow, a startup focused on aluminum refills, illustrates commitment to a circular economy model, while The Coster Group achieved Zero Waste to Landfill certification in January 2025, reinforcing sustainable manufacturing practices. Other innovations, like Budé’s CO₂ shaking technology (November 2024) and CJ Biomaterials’ BPI-certified PHACT™ masterbatches, highlight the industry’s drive to replace conventional propellants and integrate compostable coatings.

Trends and Opportunities in the Sustainable Aerosol Packaging Market

Transition to Compressed Natural Gas (CNG) and Compressed Air Propellants

The sustainable aerosol packaging market is witnessing a decisive shift from LPG-based hydrocarbon propellants toward safer, lower-impact alternatives such as compressed natural gas (CNG), compressed air, and nitrogen. Traditional LPG propellants are not only flammable but also categorized as volatile organic compounds (VOCs), contributing significantly to air pollution and climate change. In contrast, a report from a leading gas solutions provider indicates that CNG combustion produces substantially lower $CO_2$ emissions and particulates compared to LPG, positioning it as a more environmentally viable option for mass adoption.

Compressed air and nitrogen are gaining traction for their non-flammable and inert properties, eliminating the fire hazards associated with hydrocarbon-based propellants. This innovation is particularly crucial for household, personal care, and healthcare aerosols, where consumer safety is paramount. Industry case studies highlight that these sustainable propellants deliver consistent spray performance while reducing the overall carbon footprint, helping manufacturers align with regulatory mandates and corporate ESG goals.

Incorporation of Post-Consumer Recycled (PCR) Aluminum in Canisters

Another key trend is the integration of PCR aluminum alloys into aerosol canisters, driven by both corporate sustainability commitments and lifecycle emissions reductions. A flagship example comes from Beiersdorf’s Nivea, which successfully launched aerosol cans in Germany made with a DIN EN ISO 14021-certified alloy containing 100% PCR aluminum, ensuring full traceability of material sourcing.

Life Cycle Assessments (LCAs) demonstrate the impact of this innovation: a deodorant can produced entirely from PCR aluminum achieves up to 92% lower carbon emissions compared to virgin aluminum cans. This quantifiable reduction not only strengthens a company’s sustainability narrative but also directly addresses Scope 3 emissions—a growing concern in corporate sustainability reporting. To overcome the technical challenges of ensuring strength and visual quality with recycled inputs, companies are investing in new alloy formulations and purification processes, ensuring PCR aluminum meets the rigorous performance standards of high-pressure aerosol systems.

Development of Bio-Based LDPE Liners for Aluminum Canisters

A significant opportunity lies in addressing the internal liner of aluminum aerosol cans, traditionally made from virgin LDPE to prevent product–metal interactions. These liners have been a blind spot in sustainability strategies, but recent developments in bio-based LDPE resins are changing the landscape. A 2025 product summary from a biopolymer innovator revealed a bio-based LDPE resin that is FDA food contact compliant, offering a drop-in solution compatible with existing aerosol can production lines.

The integration of bio-based liners with PCR aluminum shells and non-flammable propellants enables the creation of an almost fully renewable, circular aerosol system. This innovation not only reduces fossil feedstock dependence but also provides brand owners with a powerful marketing claim—a near-zero-carbon, recyclable, and renewable aerosol package. As consumer demand for plant-based and eco-certified products rises, bio-based liners represent one of the fastest-growing sub-segments in sustainable aerosol packaging.

Engineering Monobloc Aerosol Systems for Easier Recycling

Traditional aerosols are complex, multi-component structures (can body, crimped valve, actuator) that complicate recycling streams. The opportunity lies in the development of monobloc aerosol systems—a single-piece aluminum structure that eliminates the need for crimped joints and improves recyclability. These designs not only reduce leakage risks and enhance structural integrity but also simplify collection, sorting, and remelting processes in aluminum recycling facilities.

Industry initiatives are accelerating this opportunity. The Can Manufacturers Institute (CMI) and the Household & Commercial Products Association (HCPA) have launched a sector-wide campaign to achieve 85% recycling access for aerosol cans by 2030 and ensure that at least 90% of aerosols are clearly labeled as recyclable. By adopting monobloc designs and aligning with these initiatives, manufacturers can significantly increase yield and quality of recycled aluminum while strengthening their compliance with emerging Extended Producer Responsibility (EPR) regulations.

Competitive Landscape: Leading Manufacturers are Driving Sustainable Aerosol Packaging Through Innovation, Recyclability, and Circular Economy Strategies

The global sustainable aerosol packaging market is shaped by key players leveraging metal and plastic manufacturing expertise, advanced dispensing technologies, and sustainability initiatives to provide high-performance solutions.

Ball Corporation: Pioneering Aluminum Refills and Circular Economy Solutions

Ball Corporation is a global leader in aluminum packaging, offering infinitely recyclable aerosol cans with customizable printing. In February 2025, Ball invested in Meadow, a Swedish startup focused on aluminum refills, while its Climate Transition Plan (2023) emphasizes decarbonizing the aluminum value chain. Ball’s core strengths include aluminum manufacturing expertise, brand recognition, and vertically integrated operations, with a strategic focus on innovation and sustainability in product development.

Crown Holdings, Inc.: Advancing Metal Aerosol Packaging with Recycled Content and Global Sustainability Targets

Crown Holdings provides aluminum and steel aerosol cans known for high-quality graphics and infinite recyclability. The company’s “Twentyby30” initiative sets ambitious recycling targets to enhance recycled content and global recycling rates. Crown’s core strengths lie in its global manufacturing network, expertise in metal packaging, and vertically integrated operations, with a strategy centered on supporting the circular economy while meeting customer needs.

Trivium Packaging: Driving Customized, Lightweight, and Sustainable Metal Aerosol Solutions

Trivium Packaging specializes in aluminum and steel aerosol cans for beauty, personal care, food, and home care products. In August 2025, Trivium supported breast cancer care through Panerathon and highlighted its work with Unilever’s Axe Fine Fragrance line, achieving a 5% weight reduction using advanced aluminum alloys. Trivium’s strategy focuses on customized, sustainable metal packaging solutions with strong brand recognition and integrated operations.

Ardagh Group S.A.: Leading Lightweighting and Innovation in Infinitely Recyclable Aerosol Packaging

Ardagh Group produces aluminum and steel aerosol cans with a focus on lightweighting, material reduction, and continuous improvement. The company holds over 50 global patents and 100+ international awards for packaging innovation. Ardagh’s core strengths include metal and glass manufacturing expertise and vertical integration, with a strategy centered on sustainable innovation and enhanced product performance.

Silgan Holdings Inc.: Delivering Advanced Dispensing Systems and Post-Consumer Recycled Solutions

Silgan Holdings is a leader in rigid packaging and specialty closures for aerosols, offering valves and actuators with sustainable design. In 2025, Silgan Dispensing earned an EcoVadis Gold Medal, ranking in the top 3% globally for sustainability. The company’s vertically integrated model enables comprehensive sustainable and functional packaging solutions, with a strategic focus on innovation and developing products that support circular economy goals.

Sustainable Aerosol Packaging Market Share Insights, 2025-2034

Cans Remain the Unchallenged Standard by Product Type in Sustainable Aerosol Packaging Industry

Cans, with an 88% share, overwhelmingly dominate the sustainable aerosol packaging market due to their unique ability to safely contain pressurized propellants while offering infinite recyclability. Aluminum and steel cans deliver critical performance benefits, including strength, product protection, and barrier integrity, making them indispensable across personal care, home care, and automotive segments. Sustainability efforts in this segment focus not on replacing cans but on re-engineering them: lightweighting to reduce material use, incorporating high levels of post-consumer recycled (PCR) content, and innovating mono-material valve systems for easier recycling. While PET bottles with Bag-on-Valve (BoV) systems are gaining traction in premium niches, cans continue to be the universal backbone of sustainable aerosol packaging.

Personal Care & Cosmetics Lead Market Share by Application in Sustainable Aerosol Packaging Industry

Personal care and cosmetics represent 45% of the sustainable aerosol packaging market, reflecting the sector’s role as the primary innovation hub for eco-friendly aerosol solutions. High consumer expectations, strong brand-driven sustainability commitments, and the sheer volume of hairsprays, deodorants, and sunscreens drive this dominance. Brands are aggressively adopting compressed nitrogen and CO₂ as alternative propellants, integrating PCR aluminum, and piloting refillable aerosol systems to reduce plastic and metal waste. This segment also benefits from premium positioning, where sustainability enhances brand equity and consumer loyalty. As global regulatory pressures mount against volatile organic compounds (VOCs) and non-recyclable formats, personal care and cosmetics will remain the testing ground for next-generation aerosol technologies.

United States: Recyclability, Lightweighting, and Low-GWP Propellants Driving Change

The United States sustainable aerosol packaging market is undergoing a significant transformation as EPA’s 2030 recycling goal pushes manufacturers to integrate more recycled aluminum and steel into their can designs. Companies such as Ball Corporation are pioneering this shift, introducing their ReAl® alloy aerosol cans that are 30% lighter and incorporate up to 50% recycled content, cutting the carbon footprint of conventional cans in half. At the same time, Aptar Beauty has advanced dispensing technologies with aerosol actuators and fine mist sprayers containing up to 46% PCR resin, aligning with rising sustainability standards in both cosmetics and personal care packaging.

Recycling initiatives led by the Can Manufacturers Institute, with a goal of 70% aluminum recycling by 2030 and 90% by 2050, provide a structured roadmap for industry sustainability. Alongside this, the U.S. market is seeing a decisive shift toward low-GWP propellants such as compressed air, nitrogen, and CO₂, reducing reliance on hydrocarbon-based systems. The e-commerce boom further drives demand for lightweight, durable, and space-efficient aerosol packaging that minimizes emissions during transport while maintaining product integrity. Together, these initiatives position the U.S. as a leader in circular economy practices for aerosol packaging.

European Union: Regulatory Frameworks and Refillable Aerosol Systems Gaining Momentum

The European Union aerosol packaging market is strongly influenced by comprehensive regulatory frameworks. The Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandates minimum levels of post-consumer recycled content in aerosol packaging by 2030, while the Ecodesign for Sustainable Products Regulation (ESPR) fosters innovation in refillable and repairable aerosol systems. This regulatory environment is accelerating the development of closed-loop packaging models and driving adoption of alternative barrier coatings to replace substances of concern such as PFAS, restricted from 2026.

Propellant sustainability is another major shift, as the EU phases down HFCs under the Montreal Protocol, leading to broader use of compressed gases and other low-GWP solutions. The introduction of the Digital Product Passport will further improve transparency on recyclability and compliance, strengthening consumer trust in sustainable products. Industry leaders like Mondi and Henkel are at the forefront, focusing on innovative laminates, refill systems, and eco-friendly formulations to meet growing consumer and regulatory pressures. These changes make Europe a benchmark for sustainable aerosol packaging innovation.

China: Policy, Premiumization, and High-Tech Packaging Integration

The China sustainable aerosol packaging market is evolving rapidly under the government’s “14th Five-Year Plan”, which mandates tighter plastic pollution control and eco-friendly packaging adoption. New rules effective June 2025 require express delivery companies to prioritize reusable and reduced-waste packaging, a trend directly impacting aerosol shipments across e-commerce and retail supply chains.

A strong focus on premiumization and high-end consumer goods is also driving the adoption of aerosol packaging with enhanced barrier properties, tamper-proof security features, and advanced printing technologies. Reports from the Ellen MacArthur Foundation and Tsinghua University call for significant upgrades in China’s recycling systems, reinforcing the government’s push toward remanufacturing incentives and tax support for green technology adoption. Together, these policies and market shifts are positioning China as a fast-growing hub for advanced and sustainable aerosol packaging.

India: EPR Regulations and E-Commerce Boosting Sustainable Packaging Demand

The India aerosol packaging market is being reshaped by the Plastic Waste Management (Amendment) Rules, 2024, which came into effect on April 1, 2025, making Extended Producer Responsibility (EPR) mandatory for most packaging producers, importers, and brand owners. From July 2025, all plastic packaging must also be traceable via barcodes or QR codes, ensuring transparency and accountability across the value chain. While MSMEs are exempt, responsibility shifts to manufacturers and importers supplying raw materials, creating greater compliance obligations for larger players.

With India’s expanding e-commerce and retail ecosystem, demand for durable, lightweight, and recyclable aerosol packaging is on the rise. Packaging companies are innovating to provide eco-friendly and tamper-resistant solutions that balance sustainability with cost-effectiveness. This regulatory landscape, coupled with consumer demand for safe and sustainable products, is driving significant opportunities for bio-based and recyclable aerosol formats in India.

Japan: Circular Economy Laws and Bio-Based Aerosol Packaging Adoption

The Japan sustainable aerosol packaging market is advancing rapidly under the Plastic Resource Circulation Strategy, which requires all plastic packaging to be reusable or recyclable by 2025. Complementing this, the Plastic Resource Circulation Promotion Law (2025) mandates redesign or reduction of 12 categories of single-use plastic products, pushing companies to innovate in reusable and compostable aerosol alternatives.

The Ministry of Health, Labor and Welfare (MHLW) also enforces a new positive list for synthetic food containers and packaging (June 2025), regulating material safety across sectors. Companies are responding with bio-based aerosol packaging solutions, incorporating plant-derived polymers and recyclable barrier systems. These initiatives make Japan a leading market for sustainable materials innovation in aerosol dispensing and packaging systems, with increasing adoption in cosmetics, household goods, and food sectors.

Sustainable Aerosol Packaging Market Report Scope

Sustainable Aerosol Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.2 Billion

|

|

Market Size (2034)

|

$2.7 Billion

|

|

Market Growth Rate

|

9.3%

|

|

Segments

|

By Material (Aluminum, Steel, Plastics, Glass, Composites, Bio-based Polymers), By Propellant Type (Hydrocarbons, Compressed Gases, Dimethyl Ether, HFOs, Other), By Application (Personal Care & Cosmetics, Home Care, Food & Beverages, Automotive, Medical & Pharmaceutical, Industrial), By Product Type (Cans, Bottles, Other)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ball Corporation, Crown Holdings, Inc., Trivium Packaging, Ardagh Group S.A., CCL Industries Inc., Toyo Seikan Group Holdings Ltd., AptarGroup, Inc., Alucon Public Company, Nampak Ltd., Silgan Holdings Inc., B-Pack GmbH, O. Berk Company, Coster Group, Lindal Group Holding GmbH, Aeropres Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sustainable Aerosol Packaging Market Segmentation

By Material

- Aluminum

- Steel

- Plastics

- Glass

- Composites

- Bio-based Polymers

By Propellant Type

- Hydrocarbons

- Compressed Gases

- Dimethyl Ether

- HFOs

- Others

By Application

- Personal Care & Cosmetics

- Home Care

- Food & Beverages

- Automotive

- Medical & Pharmaceutical

- Industrial

By Product Type

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Sustainable Aerosol Packaging Market

- Ball Corporation

- Crown Holdings, Inc.

- Trivium Packaging

- Ardagh Group S.A.

- CCL Industries Inc.

- Toyo Seikan Group Holdings Ltd.

- AptarGroup, Inc.

- Alucon Public Company

- Nampak Ltd.

- Silgan Holdings Inc.

- B-Pack GmbH

- O. Berk Company

- Coster Group

- Lindal Group Holding GmbH

- Aeropres Corporation

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-layered research methodology to produce accurate, actionable insights for the sustainable aerosol packaging market. Our analysis begins with a comprehensive review of primary sources, including interviews with leading industry executives, corporate filings, sustainability reports, and patent databases from companies such as Ball Corporation, Crown Holdings, and Trivium Packaging. Secondary research encompasses regulatory frameworks, trade publications, technical journals, and academic studies to evaluate trends in eco-friendly materials, propellant innovations, refillable systems, and lifecycle assessments. Market sizing, growth projections, and CAGR calculations are performed using a bottom-up approach, triangulating production volumes, sales data, and adoption rates of sustainable technologies across regions including the U.S., EU, China, India, Japan, and Brazil. USDAnalytics integrates both quantitative and qualitative assessments, factoring in technological innovations, regulatory pressures, corporate ESG initiatives, and consumer adoption patterns. Segmentation analyses by material, propellant type, application, and product type are validated against historical market data and current strategic developments to ensure precise forecasting. This methodology ensures that stakeholders receive a professional, forward-looking, and data-driven view of the global sustainable aerosol packaging market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.