Sustainable Pharmaceutical Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Sustainable Pharmaceutical Packaging Market Poised to Surpass $1.25 Trillion by 2034 Amid Rising Regulatory and Corporate Sustainability Pressures

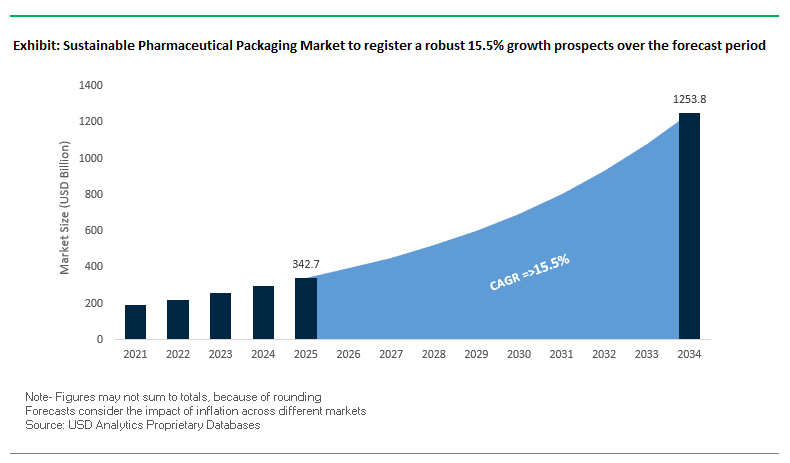

The global sustainable pharmaceutical packaging market is projected to grow from $342.7 billion in 2025 to $1,253.6 billion by 2034, at a CAGR of 15.5%. This high-growth sector is driven by the urgent need to protect sensitive drug formulations, ensure regulatory compliance, and meet ambitious corporate sustainability and circular economy targets. Key pharmaceutical companies, including Johnson & Johnson and Novartis, are committing to 100% reusable, recyclable, or compostable packaging by 2025–2030, accelerating the shift toward eco-friendly solutions.

Key Insights for Industry Professionals:

- Regulatory mandates and corporate sustainability commitments are shaping packaging adoption across pharmaceutical sectors.

- Advancements in high-barrier mono-material films, bio-based polymers, and coated paper-based blister packs enable both product protection and recyclability.

- Digital and smart packaging features, such as QR codes, RFID tags, and printed electronics, enhance traceability, combat counterfeiting, and build patient trust.

- Patient-centric design innovations improve accessibility, ease of use, and adherence while supporting environmental objectives.

- Increasing integration of eco-friendly materials into complex drug delivery systems reflects a broader trend of combining functionality with sustainability.

This market is now a critical intersection of healthcare innovation and environmental responsibility, offering opportunities for companies to differentiate through sustainability, compliance, and enhanced patient experience.

Market Analysis: Recent Strategic Moves Reflect a Focus on Renewable Materials, Circular Economy, and Smart Pharmaceutical Packaging

The sustainable pharmaceutical packaging industry is experiencing rapid innovation and consolidation, driven by eco-friendly material adoption and advanced drug protection technologies. In August 2025, Aptar launched its first nasal pump made with 52% bio-based material, signaling the industry’s shift toward renewable resources in drug delivery. West Pharmaceutical Services opened a new analytical laboratory in Stolberg, Germany (August 2025) to advance testing for injectable containment and delivery solutions, highlighting the importance of R&D infrastructure in sustainable packaging adoption.

Recognition for corporate sustainability is shaping market perception. In July 2025, Huhtamaki earned an EcoVadis Gold Medal for the fifth consecutive year, reinforcing its focus on sustainable packaging solutions for healthcare. Similarly, DuPont highlighted eco-friendly materials through its Tyvek® Sustainable Healthcare Packaging Award (July 2025), showcasing innovations in medical packaging sustainability.

Material innovations and strategic collaborations are further driving growth. Keystone Folding Box Co. launched paper-based blister packs (June 2025) as an alternative to traditional plastic, while Amcor introduced the AmSky™ recycle-ready thermoform blister system (October 2024), PVC- and aluminum-free, to improve recyclability. Collaborative moves like DS Smith and International Paper merging in January 2025 demonstrate a strategic consolidation to enhance global capabilities in sustainable pharmaceutical packaging. Initiatives such as Sanofi joining the Blister Pack Collective (February 2024) underline industry-wide efforts to reduce plastic waste through fiber-based, recyclable alternatives.

Trends and Opportunities in the Sustainable Pharmaceutical Packaging Market

Adoption of Recyclable Mono-Material Blister Packs

The sustainable pharmaceutical packaging market is experiencing a major transition toward mono-material blister packs that address one of the industry’s largest recycling challenges. Conventional blister packs are typically composed of PVC/aluminum laminates, which are difficult—if not impossible—to separate and recycle. To overcome this, leading pharmaceutical companies are collaborating with packaging suppliers to introduce mono-polypropylene (PP) blister packs. These alternatives are fully recyclable in existing PP streams while retaining the moisture and oxygen barriers required to protect sensitive drugs.

This development is being accelerated by regulatory frameworks such as the European Union’s Packaging and Packaging Waste Regulation (PPWR), which mandates that all healthcare packaging placed on the market after 2030 must be designed for recycling. Suppliers like TekniPlex have already commercialized mid-barrier blister films with 30% post-consumer resin, meeting both regulatory expectations and brand sustainability pledges. By integrating these innovations into high-speed thermoforming processes, manufacturers are not only creating circular-ready packaging but also ensuring that these solutions remain scalable and commercially viable for global pharmaceutical markets.

Integration of Post-Consumer Recycled (PCR) Content into Bottles and Containers

Beyond blisters, there is a strong movement toward incorporating PCR plastics into secondary pharmaceutical packaging such as prescription bottles and OTC containers. This approach directly addresses Scope 3 emissions, which make up a significant portion of the pharmaceutical industry’s carbon footprint. Using PCR reduces reliance on virgin fossil-based plastics and supports corporate ESG targets.

The challenge lies in ensuring that PCR resins meet stringent regulatory and safety requirements. The U.S. FDA, for example, evaluates PCR use on a case-by-case basis, necessitating advanced recycling processes that deliver food-grade and pharmaceutical-compliant resins. Industry leaders like Johnson & Johnson have made public commitments to ensuring that all packaging is recyclable by 2025, with a strong emphasis on recycled material integration. These brand-led initiatives signal a decisive shift toward embedding circular economy practices across the global pharmaceutical supply chain.

Development of Bio-Based Polymers for Primary Packaging

A key growth opportunity in the sustainable pharmaceutical packaging market lies in the development of bio-based polymers for direct drug contact. While bio-based materials such as polylactic acid (PLA) and polyhydroxyalkanoates (PHA) are widely used in food packaging, their application in pharmaceuticals remains limited due to the stringent barrier and stability requirements of drug delivery systems.

Academic research is advancing polymers like poly(butylene succinate) (PBS), which shows mechanical and barrier properties comparable to polyolefins while being fully derived from renewable feedstocks. This opens the door to creating primary pharmaceutical packaging that is both renewable and compliant with strict safety standards. The opportunity extends beyond material development, requiring collaboration between material scientists, pharmaceutical companies, and regulators to define pathways for validation and approval. Once achieved, bio-based polymers could become a cornerstone of renewable, circular-ready drug packaging.

Implementation of Reusable Packaging Systems for Closed-Loop Logistics

Another significant opportunity is the adoption of reusable packaging systems in both B2B logistics and consumer-facing markets. In bulk distribution, hospitals, clinics, and pharmacies generate vast amounts of single-use packaging waste. Companies are piloting durable, stackable returnable containers that can be sanitized, tracked with RFID or QR codes, and reintroduced into the supply chain. This creates a closed-loop logistics model that drastically reduces secondary and tertiary packaging waste while lowering costs for large-scale pharmaceutical distributors.

On the consumer side, reusable medicine systems are gaining traction. Companies like Cabinet Health are pioneering reusable glass medicine bottles paired with compostable refill pouches, enabling consumers to reduce their annual plastic waste footprint by up to one pound per person. This innovation not only aligns with the plastic reduction mandates emerging across Europe and North America but also appeals to environmentally conscious consumers, strengthening brand loyalty and market differentiation.

Competitive Landscape: Leading Global Players Are Driving Innovation and Sustainability in Pharmaceutical Packaging

Amcor plc: Pioneering Recycle-Ready Blister Packs and Circular Economy Packaging Solutions

Amcor is a global leader in flexible and rigid pharmaceutical packaging, offering nutraceutical formats including bottles, pouches, and blister packs. In August 2025, the company upgraded its UK recycling facility to increase post-consumer recycled content usage and is developing the AmSky™ thermoform blister system, a PVC- and aluminum-free solution. Amcor’s strength lies in its global manufacturing network, materials expertise, and vertical integration, with strategic focus on R&D-driven circular economy initiatives.

Gerresheimer AG: Expanding Sustainable Plastic and Glass Packaging with Post-Consumer Recycled Content

Gerresheimer provides high-quality glass and plastic containers for pharmaceuticals and nutraceuticals. In August 2025, the company introduced new plastic bottles for nutritional supplements and expanded its “Gx Circular” strategy emphasizing post-consumer recycled content and design-for-less initiatives. Gerresheimer’s core strengths include material expertise, strong brand recognition, and global integration, with a strategic focus on innovative sustainable packaging solutions that support customer and corporate sustainability goals.

AptarGroup, Inc.: Integrating Advanced Dispensing Systems with Circular Economy Packaging

Aptar specializes in dispensing, drug delivery, and active material science solutions. Recognized in June 2025 as one of TIME’s “World’s Most Sustainable Companies”, Aptar focuses on the “Adapt, Integrate, Rethink” strategy to deliver e-commerce-friendly, sustainable dispensing systems. Its core strength lies in active packaging technologies and desiccant-infused closures, critical for protecting sensitive supplements. Strategic focus emphasizes recyclable, reusable, and circular packaging solutions.

West Pharmaceutical Services, Inc.: Ensuring Patient Safety Through Sustainable Injectable Packaging Innovation

West is a leader in injectable drug containment and delivery systems, offering stoppers, plungers, and ready-to-use vial and syringe systems. In August 2025, the company inaugurated a new laboratory in Stolberg, Germany, enhancing R&D capabilities. West’s core strengths are brand recognition, vertical integration, and expertise in complex drug delivery systems, with a strategic focus on innovative, sustainable solutions supporting patient safety and adherence.

Huhtamaki Oyj: Driving Mono-Material and Fiber-Based Solutions in Sustainable Healthcare Packaging

Huhtamaki develops sustainable food and healthcare packaging, including paper, fiber-based containers, and molded fiber solutions. In July 2025, the company earned an EcoVadis Gold Medal and is advancing its Push Tab® blister lid, a mono-material PET solution ready for recycling. Huhtamaki’s core strengths include global manufacturing footprint and diverse material expertise, with strategic focus on achieving 100% recyclable, reusable, or compostable packaging by 2030.

DS Smith Plc: Leading Global Sustainable Packaging Through Paper-Based Alternatives for Pharmaceuticals

DS Smith specializes in corrugated and sustainable packaging, with solutions for the nutraceutical industry, including transit and retail displays. The January 2025 merger with International Paper positioned the company as a global leader in sustainable pharmaceutical packaging. DS Smith focuses on plastic replacement initiatives and “Growing with Purpose” strategy, leveraging extensive R&D capabilities to deliver functional, environmentally responsible packaging solutions.

Sustainable Pharmaceutical Packaging Market Share Insights, 2025-2034

Blister Packs Lead Market Share by Product Type in Sustainable Pharmaceutical Packaging Industry

Blister packs, commanding 30% of the sustainable pharmaceutical packaging market, remain the dominant format due to their critical role in unit-dose pharmaceuticals and supplements. Their leadership position reflects not only compliance with patient safety and dosage accuracy requirements but also the industry’s most concentrated sustainability innovation efforts. The transition from multi-material PVC/aluminum structures to recyclable mono-material designs, such as all-PP or PET blisters, represents a technological breakthrough aimed at tackling one of the industry’s largest waste streams. While bottles and jars are evolving with PCR integration, blister packs are at the center of the sustainability transformation, balancing recyclability with the need for high-barrier protection and tamper evidence.

Vitamins & Minerals Drive the Largest Market Share by Application in Sustainable Pharmaceutical Packaging Industry

Vitamins and minerals, with a 35% share, stand as the largest application segment for sustainable pharmaceutical packaging, driven by both their massive global consumption volume and heightened consumer sensitivity toward eco-friendly branding. The dominance of this segment makes it the primary testing ground for sustainable innovations such as PCR-based bottles, recyclable blister packs, and lightweight container designs. Regulatory compliance ensures packaging integrity, while consumer preference pushes brands to highlight recyclability and reduced plastic usage as key value propositions. As the category with the widest retail penetration—across pharmacies, supermarkets, and online—vitamins and minerals remain the sector where sustainability transitions achieve the greatest market impact.

United States: Smart and Child-Resistant Packaging Driving Growth

The United States sustainable pharmaceutical packaging market is witnessing strong momentum due to regulatory frameworks and technological innovation. The U.S. Food and Drug Administration (FDA) has issued draft guidance on New Dietary Ingredient (NDI) notification procedures and master files for dietary supplements, directly influencing how packaging and labeling are designed for new product approvals. At the same time, safety remains a key priority, with child-resistant packaging (CRP) gaining traction for vitamins and supplements. Companies such as AptarGroup and Berry Global are investing in advanced closure technologies that meet FDA and Consumer Product Safety Commission (CPSC) standards.

The market is also adopting smart packaging technologies, including QR codes and NFC-enabled solutions that allow consumers to verify authenticity, access dosage instructions, and engage with brands through connected devices. The rise of e-commerce in nutraceuticals and pharmaceuticals has accelerated the need for durable, lightweight, and recyclable solutions that can withstand shipping while minimizing environmental impact. To support this shift, the USDA Foreign Agricultural Service (USDA FAS) established the $10 million Sustainable Packaging Innovation Lab (SPIL) to accelerate compostable and recyclable packaging research. Additionally, companies like Amcor are rolling out mono-material, PVC-free, and aluminum-free blister systems, advancing the transition toward recycle-ready pharmaceutical packaging.

European Union: Regulatory Mandates Accelerating Circular Pharma Packaging

The European Union sustainable pharmaceutical packaging market is being transformed by a comprehensive regulatory ecosystem. The Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandates minimum percentages of post-consumer recycled content in pharmaceutical packaging by 2030, pushing companies to redesign existing formats. Complementing this, the EU Medical Device Regulation (MDR) has heightened requirements for sterile packaging of nutraceuticals and medical foods, emphasizing safety, traceability, and compliance.

The Ecodesign for Sustainable Products Regulation (ESPR) is further driving innovation in mono-material and recyclable pharmaceutical packaging solutions, while the Digital Product Passport introduces mandatory transparency on recyclability and material composition. Industry players are responding with innovative collaborations. For example, in February 2024, Sanofi Consumer Healthcare joined the Blister Pack Collective, an initiative by PA Consulting and PulPac, to develop fiber-based recyclable blister packs that replace traditional plastic formats. With the European Food Safety Authority (EFSA) continuously reviewing novel foods and additives, packaging must adapt to ensure compliance, product integrity, and eco-friendly innovation.

China: Premiumization and Smart Features in Pharmaceutical Packaging

The China sustainable pharmaceutical packaging market is influenced by strict regulatory oversight and rising consumer expectations. The State Administration for Market Regulation (SAMR) enforces stringent pre-market registration for health foods and supplements, requiring detailed documentation on ingredients, labeling, and packaging safety. This regulatory framework drives demand for tamper-evident and secure packaging formats.

China’s “14th Five-Year Plan” emphasizes plastic pollution control, with June 2025 regulations mandating eco-friendly, reusable, and reduced packaging across industries, including e-commerce-driven healthcare. A strong trend is the premiumization of nutraceuticals and pharmaceuticals, which has led manufacturers to adopt sophisticated packaging with advanced barrier coatings, anti-counterfeiting technologies, and luxury design aesthetics. Additionally, the government is encouraging sustainable growth by offering tax incentives for remanufacturing industries and collaborating with organizations like the Ellen MacArthur Foundation to strengthen waste plastic recycling. This dual emphasis on eco-friendly compliance and high-end consumer appeal is shaping China’s pharmaceutical packaging innovation.

India: Stringent Labeling Laws and Traceable Packaging Regulations

The India sustainable pharmaceutical packaging market is guided by strong regulatory enforcement from the Food Safety and Standards Authority of India (FSSAI). The Food Safety and Standards (Packaging and Labeling) Regulations, 2020 mandate clear product identification, ingredient listings, nutritional information, and usage instructions on supplement and nutraceutical packaging. New regulations also stipulate that all packaging must be traceable through barcodes or QR codes by July 2025, creating transparency in accountability.

The country’s nutraceutical regulations require that all health claims are backed by credible scientific evidence, which directly impacts packaging design, messaging, and compliance. At the same time, single-serve sachets and stick packs are rapidly gaining popularity due to their portability, affordability, and convenience for on-the-go consumption. Sustainability is also central to market growth, with the Plastic Waste Management (Amendment) Rules, 2024, effective April 2025, placing responsibility on producers and importers under Extended Producer Responsibility (EPR). This is pushing pharmaceutical companies to invest in recyclable, compostable, and lightweight packaging formats to align with India’s circular economy vision.

Japan: Biomass-Based and Circular Solutions Gaining Momentum

The Japan sustainable pharmaceutical packaging market is evolving under the Plastic Resource Circulation Strategy, which requires all plastic packaging to be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law (2025) further mandates the reduction or redesign of single-use plastics, accelerating the transition toward compostable and bio-based alternatives in pharma packaging.

Japan is also witnessing pioneering industry adoption of biomass-based plastics. In a world-first, Astellas Pharma Inc. began using sugarcane-based bio-plastics for blister packages as early as October 2021, setting a benchmark for sustainability in pharmaceutical packaging. Additionally, the Ministry of Health, Labor and Welfare (MHLW) introduced a positive list system for synthetic food containers and packaging, effective June 2025, ensuring that only approved and safe materials are used for food and pharma packaging. These measures, combined with Japan’s focus on bio-based innovation and circular economy policies, are propelling it to the forefront of sustainable pharmaceutical packaging development.

Brazil: Reverse Logistics and Bagasse-Based Packaging Adoption

The Brazil sustainable pharmaceutical packaging market is developing through strong government-backed sustainability frameworks. The National Solid Waste Policy (PNRS) emphasizes reuse, recycling, and waste reduction, while Law No. 15,088, effective January 2025, bans the import of plastic waste, forcing greater reliance on domestic renewable materials.

The government is actively promoting reverse logistics systems, which require producers to manage the recycling and disposal of post-consumer packaging. Local innovation is also contributing, with research institutions like CNPEM (National Center for Research in Energy and Materials) advancing bagasse-based antistatic packaging solutions, originally developed for electronics but adaptable for pharmaceuticals. Together, these developments are pushing pharmaceutical companies in Brazil to adopt compostable, recyclable, and bio-based packaging aligned with circular economy goals.

Sustainable Pharmaceutical Packaging Market Report Scope

Sustainable Pharmaceutical Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$342.7 Billion

|

|

Market Size (2034)

|

$1253.6 Billion

|

|

Market Growth Rate

|

15.5%

|

|

Segments

|

By Product Type (Bags & Pouches, Bottles & Jars, Blister Packs, Strips & Sachets, Stick Packs, Tubes, Cans, Tubs & Canisters), By Material (Plastics, Glass, Paper & Paperboard, Metal, Bioplastics & Compostable Materials, Laminates), By Closure Type (Screw Caps, Child-Resistant Closures, Flip-Top Caps, Dispensing Closures, Tear-Off Seals), By Application (Vitamins & Minerals, Herbal & Botanical Supplements, Protein & Sports Nutrition, Dietary Supplements, Functional Foods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global, Inc., Huhtamaki Oyj, AptarGroup, Inc., Sealed Air Corporation, Gerresheimer AG, Sonoco Products Company, Alpla, Tekni-Plex, Inc., West Pharmaceutical Services, Inc., Körber AG, Hoffmann Neopac AG, Constantia Flexibles Group GmbH, ProAmpac, Comar, LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sustainable Pharmaceutical Packaging Market Segmentation

By Product Type

- Bags & Pouches

- Bottles & Jars

- Blister Packs

- Strips & Sachets

- Stick Packs

- Tubes

- Cans

- Tubs & Canisters

By Material

- Plastics

- Glass

- Paper & Paperboard

- Metal

- Bioplastics & Compostable Materials

- Laminates

By Closure Type

- Screw Caps

- Child-Resistant Closures

- Flip-Top Caps

- Dispensing Closures

- Tear-Off Seals

By Application

- Vitamins & Minerals

- Herbal & Botanical Supplements

- Protein & Sports Nutrition

- Dietary Supplements

- Functional Foods

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Sustainable Pharmaceutical Packaging Market

- Amcor plc

- Berry Global, Inc.

- Huhtamaki Oyj

- AptarGroup, Inc.

- Sealed Air Corporation

- Gerresheimer AG

- Sonoco Products Company

- Alpla

- Tekni-Plex, Inc.

- West Pharmaceutical Services, Inc.

- Körber AG

- Hoffmann Neopac AG

- Constantia Flexibles Group GmbH

- ProAmpac

- Comar, LLC

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-layered research methodology to deliver accurate insights into the global sustainable pharmaceutical packaging market. Our approach integrates extensive primary research through interviews with executives, R&D specialists, and sustainability managers from leading companies such as Amcor, Gerresheimer, and AptarGroup, alongside secondary research comprising regulatory reports, corporate sustainability disclosures, scientific journals, and industry news. Market sizing, forecasts, and CAGR calculations from 2025 to 2034 are derived using a bottom-up approach, factoring adoption rates of bio-based polymers, mono-material blister packs, post-consumer recycled (PCR) content, and reusable packaging systems across key geographies including the U.S., EU, China, India, Japan, and Brazil. USDAnalytics also employs qualitative analysis to evaluate technological innovations like smart packaging (QR codes, RFID tags), patient-centric designs, and high-barrier eco-friendly films, while competitive intelligence examines strategies of market leaders. Segmentation analysis by product type, material, closure type, and application is triangulated with historical market data and regulatory frameworks to ensure accuracy. This methodology provides industry professionals with a holistic, data-driven, and forward-looking understanding of market trends, growth opportunities, and sustainability-driven innovations in pharmaceutical packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.