Syngas Market 2025–2034: $105.3 Billion to $192 Billion at 6.9% CAGR Driven by Coal Gasification, Solar Syngas, and Renewable Hydrogen Integration

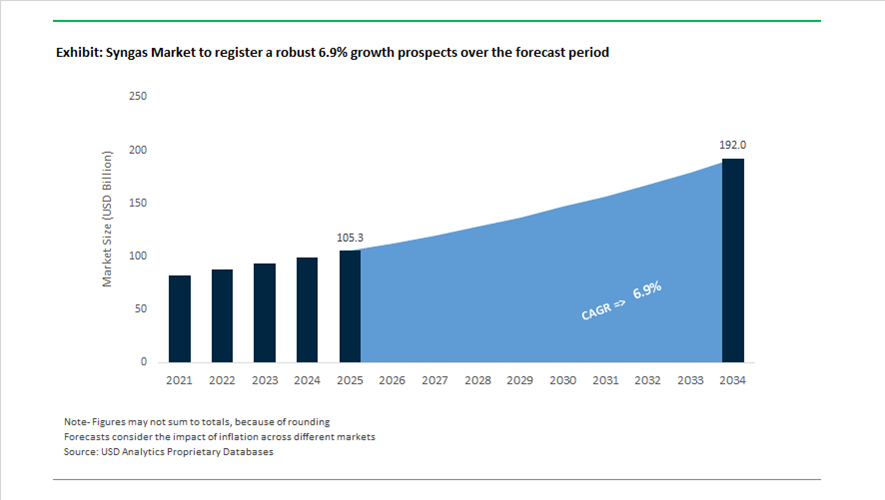

The global syngas market is valued at $105.3 billion in 2025 and is projected to reach $192 billion by 2034, expanding at a CAGR of 6.9%. Growth is supported by rising demand for synthesis gas in ammonia production, methanol synthesis, hydrogen generation, Fischer–Tropsch fuels, and low-carbon chemical intermediates. Industrial decarbonization mandates, renewable hydrogen integration, carbon capture utilization, biomass gasification, and waste-to-syngas technologies are reshaping the traditional coal and steam methane reforming landscape. Advanced syngas catalysts, CO₂ utilization pathways, modular gasification units, and solar thermochemical reactors are accelerating the shift toward lower-carbon and circular carbon feedstocks across fertilizers, sustainable aviation fuel, cement, and specialty chemicals.

Large-scale capacity additions and integrated complexes expanded in 2024 and 2025. In March 2024, Mitsubishi Heavy Industries received final acceptance for the Ghorasal Polash Urea Fertilizer Complex in Bangladesh, the country’s largest fertilizer facility, utilizing advanced reforming and ammonia synthesis technologies anchored in syngas production. In May 2024, Linde operationalized a major syngas processing plant in Geismar, Louisiana, supplying high-purity hydrogen and carbon monoxide through its Gulf Coast pipeline network to chemical and refining customers. In mid-2024, Clariant introduced the ReforMax LDP Plus and ShiftMax 217 Plus catalyst series to enhance steam methane reformer efficiency and reduce carbon intensity in industrial syngas generation. During 2024, LanzaTech and Sekisui Chemical signed a master license agreement to deploy municipal solid waste-to-syngas-to-ethanol facilities across Japan, expanding circular carbon utilization. In summer 2024, Synhelion inaugurated the DAWN solar fuel plant in Germany, and by April 2025 confirmed operation at nameplate capacity, producing solar-derived syngas for sustainable aviation fuel applications. In February 2025, Air Liquide announced a €1 billion investment in two large-scale electrolyzer projects totaling 450 MW, designed to produce renewable hydrogen and renewable syngas for European chemical decarbonization.

Technology diversification and regional mega-projects intensified in 2025 and 2026. In early 2025, WtEnergy launched SynTK technology enabling cement kilns to substitute fossil fuels with waste-derived syngas, lowering industrial CO₂ emissions. In late 2025, OroCarbo partnered with Haffner Energy to deploy a 20 MW SYNOCA module in California for biomass-to-syngas conversion targeting low-carbon biomethanol production. In January 2026, Haffner Energy introduced the C-iC modular syngas units, designed to reduce capital expenditure for decentralized biomass gasification and biofuel facilities. In February 2026, the Adani Group initiated work on a ₹70,000 crore coal gasification complex near Nagpur, India, intended to convert syngas into ammonia and hydrogen to reduce import dependency. By late 2025, BASF’s integrated Verbund syngas plant in Zhanjiang, China, reached full operational status, uniquely utilizing CO₂ off-gas from adjacent operations as feedstock to minimize emissions intensity. These developments in coal gasification, renewable hydrogen-syngas integration, solar thermochemical production, and modular biomass gasification are structurally expanding the global syngas market through 2034.

Structural Trends and Strategic Opportunities Reshaping the Global Syngas Market

Industrial-Scale Transition to Gasification-Based Chemical Recycling

The syngas market is undergoing a structural shift as petrochemical producers increasingly adopt gasification-based advanced recycling to comply with recycled-content mandates embedded in the EU Packaging and Packaging Waste Regulation. Unlike pyrolysis, which struggles with contaminated and multi-layer plastics, gasification converts heterogeneous waste streams into synthesis gas composed of carbon monoxide and hydrogen. This molecular reset allows downstream conversion into virgin-grade polymers, positioning syngas as a compliance-critical intermediate rather than an optional sustainability lever.

Capital expenditure patterns in 2024 and 2025 confirm this pivot. ExxonMobil is executing a major expansion program at its Baytown and Beaumont complexes to scale chemical recycling capacity toward 500,000 tons per year by 2027. The integration of Exxtend technology directly links plastic waste gasification to syngas-fed polymer units, creating a closed-loop production model that satisfies both recycled-content and quality requirements for food-grade applications.

Consortium-led models are further accelerating commercialization. The Cyclyx Circularity Center in Houston, a joint initiative involving ExxonMobil, Agilyx, and LyondellBasell, is designed to process more than 136,000 tonnes of plastic waste annually. Its mid-2025 commissioning underscores that gasification is emerging as the only scalable solution for high-contamination feedstocks, reinforcing syngas demand growth in regions with stringent waste diversion targets.

Strategic Repurposing of GTL Assets for Sustainable Aviation Fuel

A second defining trend is the strategic reuse of existing Gas-to-Liquids infrastructure for low-carbon fuel production. Energy majors are converting underutilized GTL assets into Power-to-Liquids and Bio-to-Liquids hubs by replacing fossil natural gas with green hydrogen and captured carbon dioxide. This transition preserves the capital-intensive Fischer-Tropsch synthesis units while dramatically lowering lifecycle emissions.

The supply-side gap in sustainable aviation fuel remains significant, with SAF expected to represent less than one% of global aviation fuel consumption in 2025. This imbalance is creating strong incentives to accelerate syngas-based SAF pathways. Shell has demonstrated synthetic kerosene produced from green hydrogen and captured CO2 using its GTL expertise, validating that existing FT reactors can be repurposed for certified e-SAF production. These demonstrations have shifted SAF discussions from theoretical feasibility to near-term scalability.

Parallel innovation is occurring at smaller scales. GTI Energy, working with Aether Fuels, has advanced the Cool GTLSM process, proving that modular GTL units can convert diverse waste carbon streams into synthetic fuels. Pilot operations established in late 2024 illustrate that syngas-based SAF production is no longer confined to mega-projects but can be deployed in decentralized configurations, expanding addressable markets for syngas technologies.

Modular Syngas Units Enabling Decentralized Green Hydrogen Hubs

The hydrogen economy is increasingly favoring distributed production models to avoid the high capital cost and permitting complexity of long-distance pipelines. Modular gasification units operating in the 5 to 50 megawatt equivalent range are enabling on-site syngas generation from municipal solid waste, agricultural residues, and waste wood. This approach positions syngas as a flexible intermediate for local hydrogen supply, particularly in regions with abundant biomass or refuse-derived fuels.

By late 2025, Compact Syngas Solutions in the United Kingdom demonstrated a modular system capable of producing hydrogen streams with purity levels approaching 98% from solid recovered fuel. These micro-scale hydrogen hubs are being targeted at waste management companies seeking to decarbonize vehicle fleets and site operations, creating a new class of customers beyond traditional industrial gas buyers.

European policy frameworks are reinforcing this opportunity. Under the Horizon Europe program, the SUPREMAS project is developing transportable syngas units designed to process sewage sludge and municipal waste into energy vectors. These deployments in Southern Europe directly address energy security concerns in regions heavily dependent on imported natural gas, positioning decentralized syngas systems as both an environmental and geopolitical solution.

Green Ammonia Production via Bio-Syngas Pathways

Decarbonization of ammonia and urea production represents one of the largest long-term demand drivers for syngas. While electrolysis-based hydrogen receives significant attention, biomass gasification routes are gaining traction as a lower-cost and more dispatchable alternative in feedstock-rich regions. Bio-syngas provides a stable hydrogen source while enabling negative or near-zero carbon intensity when paired with sustainable biomass sourcing.

India’s National Green Hydrogen Mission has explicitly identified hydrogen from biomass as a priority pathway for 2025 and 2026, supported by dedicated funding for pilot hubs producing green ammonia and methanol. This policy direction is creating early-mover advantages for syngas technologies capable of integrating agricultural residues into large-scale fertilizer value chains.

Technological advances are strengthening the economic case. Studies published in 2025 demonstrate that retrofitting existing large-scale ammonia facilities with advanced dual-reactor systems allows syngas co-production from CO2 while simultaneously generating high-value carbon materials. These configurations deliver substantial reductions in lifecycle emissions and energy demand compared to conventional steam methane reforming, positioning bio-syngas as a commercially viable backbone for the next generation of low-carbon fertilizers and export-oriented green chemicals.

Syngas Market Share Share and Segmentation Insights

Steam Methane Reforming Leads Syngas Production with Cost Efficiency and Hydrogen Scale Advantage

Steam methane reforming accounted for 58.60% of the syngas market in 2025, maintaining leadership due to its high efficiency, cost competitiveness, and scalability in hydrogen and synthesis gas production. SMR remains the preferred technology for producing syngas from natural gas feedstock, supporting large-scale output for ammonia, methanol, and hydrogen applications. Its mature infrastructure and operational reliability enable deployment from small plants to world-scale facilities. The 2025 market shift centers on carbon capture integration in SMR plants, where blue hydrogen production with 90–95% CO₂ capture is gaining traction, allowing producers to decarbonize existing assets while maintaining production efficiency in global syngas markets.

Ammonia Production Drives Syngas Demand Across Fertilizer and Energy Applications

Ammonia accounted for 32.80% of syngas market demand in 2025, making it the largest product segment due to its critical role in nitrogen fertilizer production and global food security. Syngas-derived hydrogen is a key input in the Haber-Bosch process, with ammonia production consuming nearly half of global hydrogen output. The scale of agricultural demand sustains continuous syngas consumption worldwide. The 2025 trend highlights the rise of green ammonia production, where renewable hydrogen is used to reduce carbon intensity, alongside emerging use of ammonia as a hydrogen carrier and marine fuel, while conventional SMR-based ammonia production continues to dominate due to established infrastructure and cost advantages.

Syngas Market Competitive Landscape

The syngas market in 2026 is transitioning toward decarbonization-as-a-service, with leading players integrating carbon capture, green hydrogen, and circular feedstocks. Strategic focus centers on high-purity syngas for sustainable aviation fuel (SAF), green ammonia, and e-methanol production across energy, chemicals, and maritime sectors.

Air Products Leads Mega-Scale Low-Carbon Hydrogen and Syngas Infrastructure Projects

Air Products is reinforcing its leadership through a multi-billion-dollar investment strategy in low-carbon hydrogen and syngas infrastructure. The company reported adjusted EPS of $12.03 in 2025 and projects $12.85–$13.15 for 2026, supported by $4 billion in capital expenditure. Strategic collaboration with Yara integrates syngas into global ammonia value chains. A $140 million NASA contract highlights its role in high-purity hydrogen supply for aerospace applications. Its Kochi Industrial Gas Complex in India supports petrochemical syngas demand, strengthening regional manufacturing ecosystems. The company’s strength lies in executing world-scale hydrogen and syngas mega-projects aligned with decarbonization goals.

Linde Advances AI-Integrated Syngas Plants and e-Methanol Production Systems

Linde is driving innovation through AI-enabled syngas plant automation and integrated low-carbon production systems. The company reported $34 billion in 2025 sales, supported by strong performance across chemicals, energy, and electronics sectors. Its AI-powered ammonia plant solutions optimize renewable energy integration into syngas cycles. Linde is advancing a large-scale integrated syngas facility for BASF’s Zhanjiang Verbund site with reduced emissions. The company is scaling e-methanol (e-MeOH) production using CO2 and green hydrogen for maritime fuel applications. Its diversified portfolio positions it at the forefront of digitalized and sustainable syngas production.

Air Liquide Expands Low-Carbon Syngas Hubs and Industrial Gas Decarbonization Projects

Air Liquide is accelerating industrial decarbonization through large-scale hydrogen and syngas investments. The company reported a €4.9 billion investment backlog in 2026 and achieved over 20% operating margins in 2025. Its €3 billion acquisition of DIG Airgas strengthens its presence in semiconductor and industrial gas markets in Asia. The company has reduced carbon emissions by 13% since 2020 while expanding low-carbon syngas hubs on the U.S. Gulf Coast. Electrification of oxygen production units is enhancing efficiency across syngas value chains. Air Liquide’s integrated industrial gas model enables scalable, low-emission syngas production.

Topsoe Deploys Electrified Syngas Reactors and Power-to-X Catalysis Solutions

Topsoe is redefining syngas production through electrified reactor technologies and Power-to-X systems. Under new leadership in 2026, the company improved EBIT margin guidance to 8.9% driven by energy transition demand. Its eREACT™ technology enables syngas production from CO2, biomass, and waste without fossil-based furnaces. Topsoe is a key technology provider for large SAF projects with Petrobras and Chinese partners. The company inaugurated the world’s first dynamic green ammonia plant in Denmark, integrating renewable energy into syngas synthesis. Its expertise in catalysis and green ammonia positions it as a leader in sustainable fuel technologies.

Johnson Matthey Expands Circular Syngas Technologies for SAF and Methanol Synthesis

Johnson Matthey is advancing circular syngas solutions through methanol synthesis and Fischer-Tropsch technologies. The company is targeting 20 large-scale catalyst projects by FY2025/26, with strong progress in renewable fuel applications. Its FT CANS™ technology converts biomethane-derived syngas into synthetic fuels for SAF production. A major biomethanol project in Louisiana supports maritime decarbonization using biomass-derived syngas. HyCOgen™ technology integrates green hydrogen and captured CO2 to produce drop-in syngas for existing infrastructure. The company’s integrated catalyst and process technologies enable scalable low-carbon fuel production.

Thyssenkrupp Strengthens Green Hydrogen and Syngas Integration Through Electrolysis Technologies

Thyssenkrupp is accelerating its transformation toward green hydrogen and syngas integration under its ACES 2030 strategy. The company reported €7.2 billion in Q1 2025/26 sales, with EBIT growth of 10% driven by performance optimization programs. Its Nucera division secured a major chlor-alkali project in the Middle East, reinforcing its electrolysis leadership. R&D investment increased by 31% to develop next-generation bipolar membrane electrolyzers for efficient syngas-related processes. Strategic restructuring and capital from recent IPO activities are enabling expansion into large-scale decarbonization projects. Thyssenkrupp’s focus on water electrolysis and green hydrogen strengthens its position in the evolving syngas ecosystem.

China Syngas Industry Anchored by Integrated Verbund and Hybrid Feedstock Models

China’s syngas industry is entering a structurally advanced phase characterized by deep integration with downstream petrochemicals and accelerated decarbonization pilots. A pivotal development is the 2025 start-up of BASF’s world-scale syngas facility at the Zhanjiang Verbund site, designed around proprietary process concepts that materially reduce lifecycle carbon intensity compared with conventional gasification units. This investment reinforces China’s strategy of embedding syngas production directly into large chemical ecosystems rather than operating stand-alone plants. Complementing this, Linde Engineering finalized EPC delivery for advanced syngas units integrating membrane separation technologies, enabling high-purity hydrogen and carbon monoxide streams suitable for methanol, oxo-chemicals, and specialty derivatives.

Policy support under the 14th Five-Year Energy Plan has accelerated experimentation with coal-biomass hybrid gasification, particularly in collaboration with Sinopec, to optimize carbon intensity while preserving scale economics. Parallel investments in Inner Mongolia have connected wind-powered electrolysis to legacy coal-to-liquids infrastructure, effectively injecting green hydrogen into syngas loops. Carbon Capture, Utilization, and Storage integration has also reached commercial relevance, with multiple hubs capturing more than one million tonnes of CO2 annually for enhanced oil recovery. At the municipal level, plasma-based waste-to-syngas projects in the Pearl River Delta signal a shift toward localized circular energy systems that convert solid waste into electricity and heat.

United States Syngas Industry Commercialized Through eFuels and Hydrogen Hubs

The United States syngas landscape is increasingly defined by commercial eFuel deployment and federal hydrogen infrastructure. A landmark milestone was the expansion of Mitsui & Co.’s investment in Infinium, whose Corpus Christi facility converts green hydrogen and captured CO2 into syngas using Reverse Water Gas Shift technology. This platform underpins synthetic diesel and aviation fuel production, with tangible downstream adoption demonstrated by Amazon integrating eDiesel into its heavy-duty logistics fleet by early 2026. These deployments validate syngas-derived fuels as operationally viable drop-in alternatives.

On the industrial gas side, Linde expanded syngas processing capacity in Geismar, Louisiana, strengthening pipeline-based delivery of high-purity CO and hydrogen to refiners and chemical producers. Federal momentum under the Bipartisan Infrastructure Law has further accelerated syngas-linked hydrogen hubs, with the U.S. Department of Energy backing autothermal reforming projects with up to 95% carbon capture. Large-scale investments such as Air Products’ $4.5 billion blue hydrogen complex in Louisiana underscore the role of syngas as a transitional bridge between fossil feedstocks and low-carbon ammonia, hydrogen, and sustainable aviation fuel.

India Syngas Industry Driven by Green Hydrogen Mission and Refinery Integration

India’s syngas industry is undergoing rapid transformation as green hydrogen policy converges with domestic technology development. Under the National Green Hydrogen Mission, capacity allocations exceeding 860,000 tonnes per year have been earmarked for syngas-derived outputs such as green ammonia and green methanol. This policy framework has elevated syngas from a refinery utility to a strategic national input. A notable domestic innovation milestone was achieved by Bharat Heavy Electricals Limited, which successfully demonstrated fluidized bed gasification tailored to India’s high-ash coal, enabling higher-purity methanol production without reliance on imported technology.

Downstream integration remains a defining feature. Numaligarh Refinery’s hydrogen generation agreement with Matheson Tri-Gas and Bharat Petroleum’s Kochi refinery syngas complex supplied by Air Products illustrate how syngas is being embedded into petrochemical expansion projects. Complementary initiatives include biomass-to-syngas pilots under Green Hydrogen Valleys and the commissioning of a green methanol facility at V.O. Chidambaranar Port to support coastal shipping. Collectively, these developments position syngas as a cornerstone of India’s industrial decarbonization and import substitution agenda.

Germany Syngas Industry Positioned as a Global Price Setter for eFuels

Germany’s syngas industry is evolving as a policy-driven demand anchor for renewable fuels and low-carbon industrial processes. The Indo-German Green Hydrogen Task Force agreement to develop Mulapeta port into a green ammonia and syngas derivatives hub highlights Germany’s strategy of securing long-term supply through international partnerships. Domestically, research and demonstration have gained momentum through cooperation between Sasol, Topsoe, and the German Aerospace Center, focusing on syngas-to-kerosene pathways critical for sustainable aviation fuel.

Market mechanisms further distinguish Germany’s role. The launch of H2Global physical delivery tenders in 2025 established a transparent benchmark for green ammonia and methanol pricing, directly influencing global syngas-derived fuel economics. In heavy industry, steelmakers such as ThyssenKrupp have scaled Direct Reduced Iron pilots that utilize syngas as a reducing agent, displacing coke and materially lowering emissions. These combined policy, industrial, and market initiatives position Germany not only as a consumer but as a structural price signaler for the global syngas and eFuels ecosystem.

Comparative Snapshot: Syngas Industry by Country

|

Country

|

Strategic Focus

|

Key Enabler

|

Structural Implication

|

|

China

|

Verbund integration and hybrid gasification

|

Five-Year Plans, CCUS pilots

|

Large-scale, lower-carbon syngas embedded in chemicals

|

|

United States

|

eFuels and hydrogen hubs

|

Federal infrastructure funding

|

Commercial validation of syngas-derived fuels

|

|

India

|

Green hydrogen derivatives

|

National Green Hydrogen Mission

|

Import substitution and refinery-linked growth

|

|

Germany

|

eFuels pricing and green steel

|

H2Global tenders, DRI pilots

|

Global benchmark setting for renewable syngas

|

Syngas Market Report Scope

Syngas Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$105.3 Billion

|

|

Market Size (2034)

|

$192 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Production Technology (Steam Methane Reforming, Partial Oxidation, Autothermal Reforming, Biomass Gasification, Plasma Gasification, Power-to-Syngas), By Feedstock (Natural Gas, Coal, Biomass and Waste, Petroleum Byproducts, Captured Carbon), By Gasifier Type (Fixed Bed Gasifiers, Entrained Flow Gasifiers, Fluidized Bed Gasifiers, Plasma Gasifiers), By Product (Ammonia, Methanol, Hydrogen, Liquid Fuels, Direct Reduced Iron)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Air Products and Chemicals, Inc., Linde plc, Air Liquide S.A., BASF SE, Topsoe A/S, Shell plc, Sasol Limited, KBR, Inc., ThyssenKrupp AG, Sinopec Group, Mitsubishi Heavy Industries, Ltd., Johnson Matthey plc, Technip Energies, Casale SA, Infinium Holdings, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Syngas Market Segmentation

By Production Technology

- Steam Methane Reforming

- Partial Oxidation

- Autothermal Reforming

- Biomass Gasification

- Plasma Gasification

- Power-to-Syngas

By Feedstock

- Natural Gas

- Coal

- Biomass and Waste

- Petroleum Byproducts

- Captured Carbon

By Gasifier Type

- Fixed Bed Gasifiers

- Entrained Flow Gasifiers

- Fluidized Bed Gasifiers

- Plasma Gasifiers

By Product

- Ammonia

- Methanol

- Hydrogen

- Liquid Fuels

- Direct Reduced Iron

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Syngas Industry

- Air Products and Chemicals, Inc.

- Linde plc

- Air Liquide S.A.

- BASF SE

- Topsoe A/S

- Shell plc

- Sasol Limited

- KBR, Inc.

- ThyssenKrupp AG

- Sinopec Group

- Mitsubishi Heavy Industries, Ltd.

- Johnson Matthey plc

- Technip Energies

- Casale SA

- Infinium Holdings, Inc.

*- List not Exhaustive