Synthetic Dyes Market 2025–2034: $16.8 Billion to $32.2 Billion at 7.5% CAGR Driven by Sustainable Reactive Dyes, Supply Chain Integration, and Circular Feedstocks

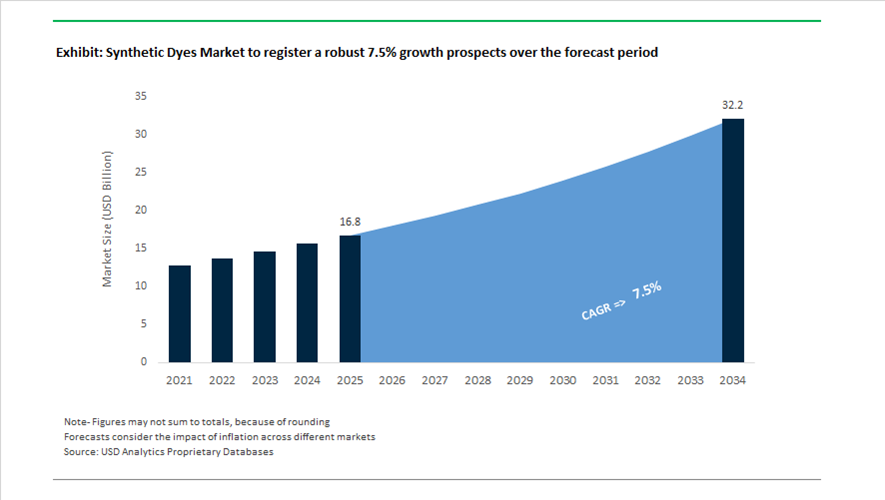

The global synthetic dyes market is valued at $16.8 billion in 2025 and is projected to reach $32.2 billion by 2034, expanding at a CAGR of 7.5%. Growth is driven by rising demand for reactive dyes, disperse dyes, sulfur dyes, vat dyes, acid dyes, and specialty colorants across textiles, leather, paper, plastics, and footwear applications. Increasing regulatory scrutiny on hazardous aromatic amines, wastewater discharge, and chemical traceability is accelerating the shift toward low-impact dye chemistry, ZDHC-compliant formulations, and circular feedstock integration. Manufacturers are prioritizing energy-efficient dyeing processes, water-reduction technologies, digital compliance platforms, and nearshoring supply chains to support fast fashion, sportswear, and performance textile markets.

Strategic consolidation reshaped the competitive landscape beginning in 2024. In January 2024, Archroma introduced the FiberColors range, manufactured using at least 50% waste-based raw materials from upcycled cotton and polyamide fibers, advancing circular synthetic dye production. In September 2024, Archroma launched SAFE EDGE+, a digital compliance and product roadmap platform that includes Foundation+ dyes engineered to reduce hazardous substances by over 95% compared to conventional industry standards. In October 2024, DyStar received the Adidas adiFormulator Champion Award for excellence in sustainable chemical management, reinforcing its leadership in responsible dye formulation. In the same month, Nuevo Mundo expanded its collaboration with Archroma to deploy EarthColors dyes derived from herbal and agricultural waste for nearshore denim production targeting U.S. demand. In early 2025, DyStar consolidated its North American manufacturing footprint by merging Charlotte operations into its Reidsville, North Carolina facility to optimize efficiency. In March 2025, Sudarshan Chemical Industries completed the acquisition of Heubach Group, forming one of the world’s largest integrated colorant portfolios by combining large-scale Indian manufacturing with advanced German synthetic dye and pigment technologies.

Operational optimization and innovation intensified through 2025 and early 2026. In 2025, Archroma introduced AVITERA RASPBERRY SE, a high-performance reactive dye enabling up to 50% reductions in water and energy consumption compared to conventional dyeing processes, targeting sportswear and performance apparel. In August 2025, Lanxess announced plans to shut down its Widnes, UK site by the end of 2026 to streamline its specialty chemical network and reduce operational costs. In January 2026, DyStar formally transitioned to full ownership under Zhejiang Longsheng Group, enabling deeper integration with upstream sulfur and disperse dye intermediate supply chains. In February 2026, UK startup Sparxell secured $5 million in funding to commercialize plant-inspired structural color technology as an alternative to petroleum-based synthetic dyes. In February 2026, Nomagic introduced an AI-driven shoebox picker robot for fashion logistics, facilitating mass customization in footwear and indirectly driving demand for small-batch, high-performance synthetic dye formulations. These consolidations, circular feedstock innovations, digital compliance systems, and sustainable dyeing technologies are structurally reinforcing growth in the synthetic dyes market through 2034.

Strategic Trends and High-Value Opportunities in the Global Synthetic Dyes Market

Digital Printing Transition Driving High-Purity Inkjet Dye Demand

The global synthetic dyes market is undergoing a structural value shift as textile manufacturers accelerate the transition from analog rotary screen printing to Digital Textile Printing. This change is not incremental but transformational, as digital inkjet platforms impose far stricter chemical performance thresholds on dyes. Inkjet systems require ultra-low particulate content, controlled molecular weight distribution, and highly stable rheology to prevent nozzle clogging and jet misfiring. As a result, demand is rapidly migrating away from commodity-grade colorants toward precision-engineered disperse and reactive dyes formulated specifically for high-resolution digital platforms.

Resource efficiency is a central driver of this transition. By 2025, digital printing systems have consistently demonstrated up to 90% reductions in water consumption compared to conventional dyeing routes that typically consume 50 to 60 liters per meter of fabric. This efficiency advantage is directly aligned with tightening wastewater discharge norms across Asia and Europe, making digital dye systems a strategic compliance tool rather than a discretionary upgrade. Adoption data from major textile hubs shows a 34% year-on-year increase in digital textile printing installations, reinforcing the structural nature of this shift.

Within digital dye chemistry, reactive dyes have emerged as the dominant value segment, accounting for nearly 28% of all digital dyeing processes. Their ability to form covalent bonds with cellulose fibers enables superior colorfastness and vibrancy on cotton and viscose substrates. By late 2025, more than 44% of industrial digital printers formally specified high-performance reactive or direct disperse dyes to achieve print resolutions approaching 1200 dpi. This specification-driven procurement is steadily reallocating margin from traditional dye intermediates toward high-purity, application-specific ink formulations.

Non-Discretionary Reformulation Under Global Chemical Regulations

Parallel to technology-driven change, the synthetic dyes market is being reshaped by an unprecedented wave of regulatory mandates. Dye producers and textile processors are now operating under non-negotiable reformulation timelines set by the U.S. EPA and the European Union’s REACH framework. Under the 2024 Rule issued by the U.S. Environmental Protection Agency, fashion articles containing the persistent substance PIP (3:1) will be prohibited from U.S. distribution starting October 31, 2026. This has triggered large-scale inventory audits and reformulation programs throughout 2025, particularly to comply with the stringent 0.1% concentration threshold.

At the same time, voluntary standards have effectively become mandatory market access requirements. From April 1, 2025, the OEKO-TEX STANDARD 100 reduced allowable Bisphenol A levels in skin-contact textiles by 90%, from 100 mg/kg to 10 mg/kg. In parallel, the ZDHC Roadmap to Zero now requires dyehouses supplying major global brands to use MRSL Level 3-certified chemicals exclusively. These combined pressures are accelerating the phase-out of legacy azo dyes capable of cleaving into restricted aromatic amines. For dye manufacturers, regulatory compliance has become a primary driver of R and D investment, reshaping product portfolios toward low-toxicity, high-purity synthetic colorants.

Tailored Dye Systems for Next-Generation Sustainable Fibers

The rapid expansion of Man-Made Cellulosic Fibers and recycled polymers is creating a significant opportunity for specialized synthetic dyes engineered for novel fiber chemistries. Lyocell and related MMCFs are projected to increase their share of global fiber consumption from 6% in 2022 to approximately 8% by 2030. These fibers exhibit dense crystalline structures and unique solvent-spun morphologies, requiring dyes capable of deep penetration and fixation at lower processing temperatures.

Research published in 2025 has validated the commercial viability of dope-dyeing for Lyocell using high-tenacity aqueous pigment dispersions. This approach eliminates conventional aqueous dyeing altogether, reducing water and energy consumption while delivering tensile strengths up to 50 cN per tex. In parallel, the growing dominance of recycled polyester in activewear is driving demand for carrier-free disperse dyes that achieve uniform shade build-up on rPET without amplifying fiber defects. Emerging bio-polymers such as PHA and bio-based polyethylene from platforms like Braskem require dyes that operate below traditional thermal thresholds to avoid polymer degradation, opening a premium niche for low-temperature, high-affinity dye chemistries.

Integrated Functional Dyes for Smart and Protective Textiles

Beyond coloration, the synthetic dyes market is entering a phase of functional convergence where colorants are expected to deliver performance attributes at the molecular level. The rise of smart textiles in healthcare, defense, and outdoor apparel is accelerating demand for dyes that provide UV protection, antimicrobial activity, and durability without additional finishing steps.

Technical disclosures from 2025 highlight the growing adoption of bio-derived and hybrid dyes containing flavonoids, polyphenols, and other bioactive structures. These systems offer dual functionality by delivering stable coloration alongside inherent UV absorption and antimicrobial performance. Such integration is particularly valuable in medical textiles, where durability through repeated laundering is critical.

Advanced synthetic systems are also evolving rapidly. The incorporation of silver nanoparticles and chitosan into dye formulations has demonstrated enhanced pathogen resistance for hospital bedding and surgical textiles. By late 2025, UV-cured functional dye inks gained momentum as a scalable solution, offering rapid curing, low VOC emissions, and the ability to deposit protective layers directly during printing. This convergence of color and function is redefining value creation in the synthetic dyes market, positioning advanced formulations as enablers of next-generation textile performance rather than simple aesthetic inputs.

Synthetic Dyes Market Share and Segmentation Insights

Reactive Dyes Dominate Synthetic Dyes Market with Superior Fiber Bonding and Color Performance

Reactive dyes accounted for 32.80% of the synthetic dyes market in 2025, driven by their strong affinity for cellulosic fibers such as cotton, viscose, and linen, which represent the largest share of global textile consumption. These dyes form covalent bonds with fibers, delivering excellent wash fastness, color vibrancy, and durability required in apparel and home textiles. Their versatility across dyeing processes supports widespread industrial adoption. The 2025 innovation trend focuses on sustainable reactive dye chemistries, including high-fixation dyes that reduce water and salt usage, and cold-branding dyes that lower energy consumption, aligning textile dyeing processes with environmental and regulatory requirements.

Textile and Apparel Sector Drives Bulk Demand for Synthetic Dyes Globally

Textile and apparel accounted for 68.40% of synthetic dyes market demand in 2025, reflecting the massive scale of global fiber, yarn, and fabric coloration processes. The industry’s continuous output, exceeding 100 million tons annually, ensures sustained demand for diverse dye chemistries across fashion, home textiles, and industrial fabrics. Frequent design changes and color trends further accelerate dye consumption cycles. The 2025 market evolution centers on waterless and low-impact dyeing technologies, including supercritical CO₂ dyeing, foam dyeing, and digital textile printing, which improve dye utilization efficiency and reduce environmental footprint while driving the need for advanced dye formulations compatible with next-generation textile processing systems.

Synthetic Dyes Market Competitive Landscape

The synthetic dyes market in 2026 is defined by green synthesis, low-temperature dyeing technologies, and bio-based feedstocks. Leading players are aligning with global decarbonization targets, while India and China dominate over 40% of exports, driving innovation in sustainable textile chemicals and circular dyeing systems.

Archroma Accelerates Circular Dyeing Systems with Low-Temperature AVITERA® Technologies

Archroma leads the sustainable synthetic dyes market through advanced circular chemistry and integrated textile systems. Its partnership with Innovo Fiber (Fibre52®) combines AVITERA® SE reactive dyes with caustic-free, low-temperature bleaching, enabling up to 50% reductions in water and CO2 emissions. The AVITERA® platform delivers ultra-high fixation rates, significantly lowering rinse cycles and energy consumption. At Colombiatex 2026, Archroma introduced SILIGEN® D2W and ERIOFAST® for eco-efficient textile processing. The company’s One Way Impact Calculator provides real-time environmental footprint analytics, ensuring compliance with ZDHC MRSL standards. Its integration of Huntsman Textile Effects strengthens its leadership in sustainable dyeing solutions.

DyStar Strengthens Global Dye Leadership Through Governance Consolidation and Cadira® Sustainability Modules

DyStar is entering a new growth phase following its full acquisition by Zhejiang Longsheng for $702 million, resolving long-standing shareholder disputes. The company is optimizing its global manufacturing footprint by consolidating U.S. operations to enhance supply chain efficiency. A leadership transition in 2026 signals strategic alignment for long-term growth. DyStar’s Cadira® modules enable up to 45% reductions in water, energy, and waste through optimized dyeing processes. Its integrated sustainability framework reinforces its position in eco-efficient textile coloration. The company’s restructuring supports scalable, cost-efficient production across global markets.

Kiri Industries Redirects Capital into Diversified Industrial Expansion While Sustaining Reactive Dye Leadership

Kiri Industries is transitioning into a diversified industrial group following a $689 million capital realization from the DyStar settlement. The company is investing ₹13,300 crore into a large-scale copper smelting and fertilizer complex in Gujarat, targeting a projected IRR of ~25%. Despite diversification, Kiri maintains a strong presence in reactive dyes, serving global textile and fast fashion industries. Its Indian manufacturing base ensures cost competitiveness and export strength. Environmental clearance and land acquisition for its mega-project are largely complete as of 2026. The company’s dual strategy balances specialty dye production with high-growth industrial investments.

Atul Expands Specialty Dye Portfolio with Vat and Sulfur Leadership and Water-Efficient Manufacturing

Atul remains a dominant force in vat and sulfur dyes, supported by strong innovation and sustainability initiatives. Its Colors division received industry recognition for water conservation and indigenous technology development. The Sindica dye range continues to gain traction for superior color fastness across textiles and coatings. The Atul-Buckman joint venture enhances its specialty chemical capabilities and application technologies. The company’s vertically integrated manufacturing supports global supply stability across multiple industries. Its Platinum Green Village certification highlights its commitment to sustainable and eco-efficient dye production.

BASF Drives High-Performance Dye Intermediates and Digital Color Innovation Through Industrial Solutions Strategy

BASF operates as a key upstream supplier of dye intermediates and functional color solutions, focusing on high-value specialty chemicals. The company achieved €1.7 billion in cost reductions by 2025, supporting reinvestment into sustainable chemical innovation. Its divestiture of decorative paints in Brazil sharpens focus on industrial solutions and advanced pigment technologies. BASF’s Automotive Color Trends, including Tesseract Blue, are influencing next-generation synthetic fibers and technical textiles. The company is targeting CO2 emissions between 17.2 and 18.2 million metric tons in 2026 through its green transformation strategy. Its integrated Verbund system ensures cost efficiency and scalable supply of dye intermediates.

China Synthetic Dyes Industry Repositioned Toward High-End and Electronic Applications

China’s synthetic dyes industry is undergoing a decisive structural upgrade under the Ministry of Industry and Information Technology’s 2025–2026 Plan for Stabilizing Chemical Growth. The policy targets sustained growth in chemical industry added value while explicitly prioritizing high-end specialty dyes for electronic chemicals and advanced materials. A critical enforcement mechanism is the mandatory relocation of all remaining dye production into National Chemical Parks by 2026. This shift is forcing producers to adopt automated production lines, closed-loop effluent recycling, and real-time emissions monitoring, effectively raising the technical entry barrier for low-value dye manufacturing.

At the application level, Chinese producers are expanding into structurally complex end markets. In 2025, firms such as Zhejiang Longsheng introduced lightweight, UV-stable synthetic dyes engineered for carbon-fiber composites used in the domestic eVTOL aircraft segment. Parallel progress has been achieved in electronic dyes, where Chinese manufacturers localized ultra-high-purity colorants for OLED and LCD color filters, with a stated objective of reaching 90% domestic self-sufficiency by end-2026. Zhejiang province’s Zero-Waste mandates have further accelerated the adoption of digital ink-jet dyes, delivering up to 60% water savings in textile coloration while aligning compliance with export-oriented sustainability requirements.

India Synthetic Dyes Industry Accelerated by PLI-Driven Import Substitution

India’s synthetic dyes market is expanding through coordinated fiscal support and infrastructure modernization. Under the Production Linked Incentive framework, realized investments in specialty chemicals reached ₹1.76 lakh crore by March 2025, catalyzing domestic capacity for high-performance reactive and disperse dyes that were historically imported. This industrial push is reinforced by higher public spending on textile infrastructure, including targeted funding for modernizing common effluent treatment plants in dyeing clusters such as Tirupur and Surat, improving compliance while enabling higher throughput.

Innovation at the firm level is translating policy support into differentiated products. In mid-2025, Kiri Industries commercialized its Liva-Eco dye range, engineered for higher fixation efficiency on cellulosic fibers. The chemistry reduces salt loading in wastewater streams, addressing both regulatory pressure and operating cost sensitivity for textile processors. India’s broader PCPIR investments in Odisha and Gujarat are now enabling integrated cracker-to-dye value chains, improving feedstock security. By 2025, India had transitioned into a net exporter of chemical intermediates, with specialty dye exports reaching $2.75 billion in the first half of FY26, signaling its emergence as a credible alternative supply base to China.

United States Synthetic Dyes Industry Redirected by Food and Environmental Policy

The U.S. synthetic dyes industry is experiencing a demand-side reconfiguration driven by regulatory intervention and brand-level commitments. In April 2025, the Food and Drug Administration and Department of Health and Human Services announced a plan to phase out six widely used synthetic food dyes by end-2026. This policy signal triggered rapid corporate responses, with major FMCG companies such as Kraft Heinz and Mars Wrigley committing to eliminate certified colors in favor of nature-identical synthetic alternatives.

On the industrial side, process efficiency and emissions compliance are shaping innovation priorities. In October 2025, Huntsman launched ERIOPON® E3-SAVE, enabling simultaneous dyeing and leveling of polyester and reducing processing time by 25%. Concurrently, new Environmental Protection Agency low-VOC mandates are pushing coatings manufacturers toward solvent-free granular dyes. Circular fashion initiatives funded by the U.S. Department of Energy in early 2026 further highlight the industry’s shift toward re-dyeing and fiber life-extension technologies.

European Union Synthetic Dyes Industry Defined by Traceability and PFAS Transition

Across Germany and Switzerland, regulatory architecture rather than volume expansion is defining the synthetic dyes landscape. The anticipated 2026 adoption of the European Chemicals Agency’s PFAS restriction is set to reshape dye formulations by constraining the surfactants and auxiliaries historically used in synthetic colorants. In parallel, the EU’s Digital Product Passport requirement, effective from late 2025 under the New Detergents and Surfactants Regulation, obliges dye manufacturers to provide full precursor traceability, materially increasing data transparency across textile supply chains.

Innovation is increasingly focused on hybrid chemistries and waterless processes. In 2025, Archroma expanded its EarthColors® portfolio to include bio-synthetic hybrid dyes derived from upcycled herbal and food waste streams, reducing petroleum dependency by approximately 40%. Germany’s introduction of Green Tier tax rebates for CO2-based dyeing technology is accelerating the adoption of supercritical carbon dioxide as a solvent for disperse dyes, positioning the region as a process innovation leader rather than a cost-driven producer.

Comparative Snapshot: Synthetic Dyes Industry by Country

Synthetic Dyes Market County Level Snapshot

|

Country / Region

|

Primary Policy Driver

|

Technology Emphasis

|

Structural Outcome

|

|

China

|

MIIT chemical growth plan, park migration

|

Electronic-grade and digital dyes

|

Shift from volume to high-purity self-sufficiency

|

|

India

|

PLI and textile infrastructure funding

|

High-fixation reactive dyes

|

Import substitution and export expansion

|

|

United States

|

FDA phase-out, EPA VOC limits

|

Nature-identical and solvent-free dyes

|

Demand-led portfolio realignment

|

|

European Union

|

REACH, DPP, PFAS restriction

|

Bio-hybrid and CO2 dyeing

|

Traceability-driven premium positioning

|

Synthetic Dyes Market Report Scope

Synthetic Dyes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$16.8 Billion

|

|

Market Size (2034)

|

$32.2 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Product Type (Reactive Dyes, Disperse Dyes, Acid Dyes, Vat Dyes, Direct Dyes, Basic Dyes, Sulfur Dyes), By Chemical Structure (Azo Dyes, Anthraquinone Dyes, Phthalocyanine Dyes, Triphenylmethane Dyes), By Form (Powder Dyes, Liquid Dyes, Granular Dyes), By End-Use Industry (Textile and Apparel, Packaging and Printing, Food and Beverage, Cosmetics and Personal Care, Paints and Coatings, Leather and Paper)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Archroma, Huntsman Corporation, Zhejiang Longsheng Group Co., Ltd., DyStar Group, BASF SE, Atul Ltd., Kiri Industries Ltd., CHT Group, Zhejiang Runtu Co., Ltd., Kyung-In Synthetic Corporation, Everlight Chemical Industrial Corp., Lanxess AG, Bodal Chemicals Ltd., Jay Chemical Industries Private Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Synthetic Dyes Market Segmentation

By Product Type

- Reactive Dyes

- Disperse Dyes

- Acid Dyes

- Vat Dyes

- Direct Dyes

- Basic Dyes

- Sulfur Dyes

By Chemical Structure

- Azo Dyes

- Anthraquinone Dyes

- Phthalocyanine Dyes

- Triphenylmethane Dyes

By Form

- Powder Dyes

- Liquid Dyes

- Granular Dyes

By End-Use Industry

- Textile and Apparel

- Packaging and Printing

- Food and Beverage

- Cosmetics and Personal Care

- Paints and Coatings

- Leather and Paper

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Synthetic Dyes Industry

- Archroma

- Huntsman Corporation

- Zhejiang Longsheng Group Co., Ltd.

- DyStar Group

- BASF SE

- Atul Ltd.

- Kiri Industries Ltd.

- CHT Group

- Zhejiang Runtu Co., Ltd.

- Kyung-In Synthetic Corporation

- Everlight Chemical Industrial Corp.

- Lanxess AG

- Bodal Chemicals Ltd.

- Jay Chemical Industries Private Limited

*- List not Exhaustive