Tannin Market 2025–2034: $3.9 Billion to $6.8 Billion at 6.3% CAGR Driven by Bio-Circular Leather, Functional Nutrition, and Precision Agriculture

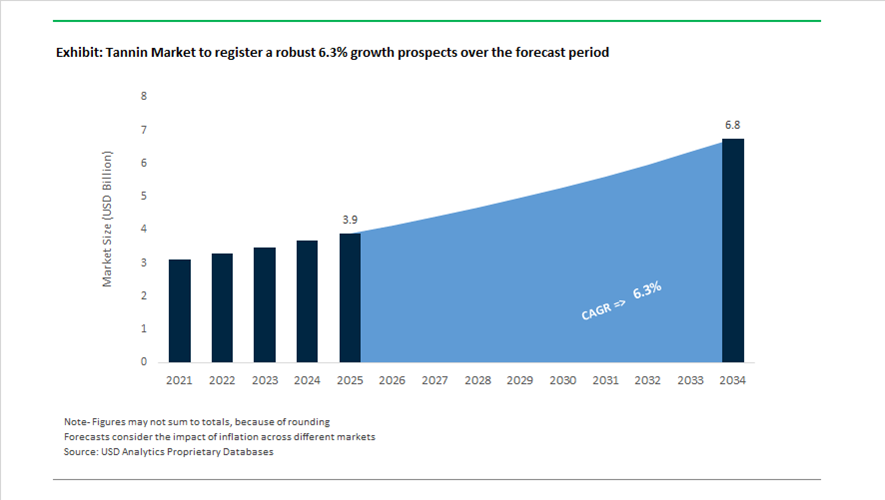

The global tannin market is valued at $3.9 billion in 2025 and is projected to reach $6.8 billion by 2034, expanding at a CAGR of 6.3%. Market growth is being reshaped by three structural transitions: the decarbonization of leather processing, the elevation of tannins into high-value health and nutrition applications, and their integration into sustainable agricultural inputs. Traditionally associated with vegetable tanning, tannins are now positioned as multi-industry bioactive molecules used across leather, animal nutrition, biosimulants, functional foods, and specialty chemicals. The industry is shifting from commodity bark extracts toward highly purified, fractionated, and application-specific tannin chemistries supported by traceable biomass sourcing and circular feedstock strategies.

Consolidation in sustainable leather technologies accelerated in 2024. In February 2024, Silvateam S.p.A. acquired a majority stake in wet-green GmbH, creator of the patented Olivenleder® technology. The transaction combines Silvateam’s global extraction capacity with olive-leaf-based tanning agents derived from agricultural waste streams, strengthening bio-circular leather production across Europe. In July 2024, Tannin Corporation acquired Whittemore-Wright Company, integrating specialized tanning oils to deepen its North American specialty leather footprint. Between 2024 and 2025, luxury automotive OEMs expanded adoption of olive-based tanning systems for premium interiors, validating tannin-derived solutions as substitutes for chromium-based chemistries. In March 2025, Sudarshan Chemical Industries completed the acquisition of the Heubach Group, indirectly influencing the broader leather treatment ecosystem by consolidating colorant and finishing chemistries frequently paired with tannins in high-end coatings and hides.

The diversification of tannins into health, biosimulants, and specialty chemistry intensified through 2025. At the 2025 Polyphenols Applications World Congress, Silvateam presented research from the Stance4health Project demonstrating specific tannin fractions as gut microbiota modulators, positioning tannins within precision nutrition and functional food markets. Throughout 2025, Ajinomoto OmniChem expanded its Health and Well-being strategy, applying tannin extraction expertise to soil health additives and agricultural biosimulants that enhance root growth and carbon sequestration. In early 2024, Tanin Sevnica introduced microencapsulated tannins for ruminant nutrition, improving protein utilization and reducing methane emissions; this was followed in late 2025 by a spray-chilled chestnut-derived encapsulated release system designed to mitigate anti-nutritional effects. Industrial supply chain investments also supported higher-purity processing: in May 2025, BASF SE invested in a semiconductor-grade sulfuric acid plant in Ludwigshafen, enabling advanced modification of hydrolyzable tannins for electronics and medical-grade applications. In early 2026, Tanfac Industries announced a ₹495 crore expansion to reinforce specialty chemical infrastructure tied to tanning intermediates.

Structural Trends and Strategic Opportunities in the Tannin Market

Elimination of Animal-Derived Fining Agents in Vegan and Low-Intervention Winemaking

The tannin market is experiencing a structural uplift from the global shift toward vegan, low-intervention, and transparently labeled wines. As wineries respond to consumer demand for animal-free production, tannins extracted from grape seeds, skins, and pomace are replacing traditional animal-derived fining agents such as gelatin, isinglass, and casein. This transition is no longer niche-driven; it is becoming embedded in procurement standards for premium and export-oriented wineries.

Empirical validation has accelerated adoption. Comparative studies conducted during 2024–2025 demonstrate that grape seed-derived tannins can reduce polymeric proanthocyanidins in red wines by up to 23%, a clarification efficiency previously associated only with high-molecular-weight animal proteins. This performance parity has removed the technical barrier that historically limited plant-based fining agents to artisanal applications. As a result, tannic acid systems are increasingly standardized across commercial wineries seeking consistency, clarity, and oxidative stability.

Labeling and certification dynamics further reinforce this trend. Wine regions actively promoting “natural” and vegan credentials are institutionalizing the use of plant-derived tannins and fermentation byproducts such as cell wall polysaccharides. By integrating pomace-based tannins into clarification protocols, producers maintain varietal integrity while complying with vegan certification requirements, strengthening the role of tannins as both a functional and marketing-critical input.

Transition to Formaldehyde-Free Wood Panels Using Tannin-Based Bio-Resins

A second transformative trend is unfolding in engineered wood and construction materials, where tannin-based adhesives are replacing urea-formaldehyde and phenol-formaldehyde systems. Tightening indoor air quality regulations and global VOC reduction mandates are making formaldehyde-free binders a non-negotiable requirement for plywood, particleboard, and structural timber applications.

Recent technical advances have repositioned condensed tannins as performance-grade resin precursors rather than sustainability compromises. By late 2025, pine bark and quebracho tannin-based adhesives demonstrated flexural strengths of approximately 37 MPa and moduli exceeding 4.5 GPa, outperforming conventional phenol-resorcinol-formaldehyde systems in several engineered wood formats. These metrics are particularly relevant for cross-laminated timber and load-bearing panels used in low-carbon construction.

Regulatory compliance is accelerating commercialization. Newly developed larch tannin–glyoxal adhesive systems have achieved formaldehyde emission levels well below the intrinsic emissions of wood itself, comfortably meeting stringent E0-grade standards in major Asian markets. As a result, tannin-based resins are transitioning from pilot-scale demonstrations to industrial adoption, creating a structurally resilient demand base tied to green building codes and sustainable urbanization.

High-Growth Opportunities Unlocking New End-Use Markets

One of the most commercially significant opportunities for the tannin market lies in chrome-free leather tanning. Regulatory scrutiny over chromium discharge and wastewater toxicity is intensifying across automotive and footwear supply chains, pushing manufacturers to seek scalable vegetable tanning alternatives. Advances in tannin-complexed formulations are overcoming historical limitations related to processing time and thermal stability.

Recent developments have demonstrated that modified mimosa and quebracho tannins can produce leathers with shrinkage temperatures exceeding 83°C and tensile strengths above 280 kg/cm². These properties meet the demanding mechanical and heat-resistance requirements of automotive interiors, including steering wheels, seating, and trim components. Industry leaders such as ECCO Leather are already pioneering water-efficient, chrome-free tanning systems, signaling growing OEM acceptance.

Circular economy models are further expanding this opportunity. In late 2025, standardized processes for converting fish skin waste into high-quality leather using tannin-based systems demonstrated both ethical sourcing and commercial durability. This approach not only valorizes waste streams but also aligns with automotive brand commitments to traceable, low-impact materials.

Bio-Based Corrosion Inhibitors for Industrial Water and Steel Protection

A second high-value opportunity is emerging in industrial water treatment and corrosion protection, where tannins are being deployed as green alternatives to zinc- and chromate-based inhibitors. Tannins form stable metal–tannate films on steel and concrete surfaces, providing rapid and durable protection against electrochemical degradation without introducing persistent toxins into effluent streams.

Performance validation has been a key inflection point. Late-2025 industrial trials showed tannin-based inhibitors achieving corrosion inhibition efficiencies of up to 85% on mild steel under alkaline conditions, with protective layers forming within minutes of application. This rapid adsorption behavior makes tannins particularly attractive for cooling towers, boilers, and closed-loop industrial systems where response time is critical.

Market integration is accelerating as zero-liquid-discharge and water reuse systems become standard across heavy industry. Organic corrosion inhibitors, led by bio-based tannins, now represent a substantial share of the global inhibitor landscape, supported by their compatibility with stringent effluent regulations and sustainability reporting frameworks. As industrial operators prioritize non-toxic chemistries that reduce lifecycle environmental impact, tannins are positioned as a core input in next-generation water and asset protection strategies.

Tannin Market Share and Segmentation Insights

Wood-Based Tannins Lead Market with Scalable Supply and Cost Efficiency

Wood-based tannins accounted for 48.60% of the tannin market in 2025, supported by their abundant availability, cost efficiency, and established extraction infrastructure from sources such as quebracho, chestnut, and wattle. These tannins are widely used in leather tanning, wood adhesives, and industrial applications, where consistent quality and supply are critical. Forestry-based sourcing enables large-scale production across key regions. The 2025 industry shift emphasizes sustainable forestry certification and traceability, with producers adopting FSC and PEFC standards to meet environmental requirements and strengthen positioning in premium leather, food, and beverage applications.

Leather Tanning Segment Dominates Tannin Demand with Premium Sustainable Leather Trends

Leather tanning accounted for 38.60% of tannin market demand in 2025, driven by the use of tannins in vegetable tanning processes that produce high-quality leather for footwear, upholstery, and luxury goods. Tannin-based tanning imparts desirable properties such as durability, natural aesthetics, and aging characteristics. The scale of global leather production supports consistent consumption. The 2025 trend highlights rising demand for sustainable and chrome-free leather, where vegetable tanning is positioned as an environmentally favorable alternative, supported by certification programs and increasing adoption in premium automotive interiors, fashion accessories, and eco-conscious consumer products.

Tannin Market Competitive Landscape

The tannin market in 2026 is driven by botanical extraction innovation, circular economy integration, and demand for ultra-purified polyphenols. Leading producers are scaling chestnut, quebracho, and mimosa extracts for bio-adhesives, leather processing, nutraceuticals, and water treatment, aligning with clean-label and EU Green Deal sustainability mandates.

Silvateam Leads Chromium-Free Leather and Nutraceutical Tannin Innovation Through Integrated Forest-to-Extract Model

Silvateam dominates the tannin market with a fully integrated supply chain and advanced enzymatic extraction technologies. The LIFE I'M TAN initiative is accelerating chromium-free leather adoption in automotive and luxury fashion segments. Its Silvafeed® line improves nutrient absorption by 12% in antibiotic-free livestock systems. Operational optimization at its Italian facility increased production efficiency by 15% through hierarchical extraction upgrades. The company leads in quebracho and chestnut extracts with Ecopel-certified metal-free tanning solutions. Strong positioning in circular bio-based chemicals supports applications in leather, animal nutrition, and sustainable materials.

Saviola Group Expands Circular Wood-Based Tannin Applications in Bio-Adhesives and Agriculture

Saviola Group is leveraging its recycled wood infrastructure to scale tannin-based bio-adhesives and agricultural biostimulants. A €200 million funding package supports expansion of its Sustinente plant, increasing capacity by 140% to 600,000 m³. The company extracts tannins from 100% recycled wood streams, aligning with circular economy mandates. Its chestnut tannins reduce fertilizer dependency by up to 20% in viticulture. New tannin-based water treatment solutions demonstrate 92% heavy metal removal efficiency. Strategic pivot toward life sciences strengthens its position in sustainable agriculture and industrial applications.

Tanac Scales Mimosa-Based Tannin Production with Zero-Waste Biorefinery and Water Treatment Leadership

Tanac leads global mimosa extract production with over 30,000 hectares of FSC-certified plantations. Its Tanfloc range is deployed in over 50 countries for water treatment, leveraging natural flocculation properties. The company introduced high-fixation mimosa extracts that reduce leather processing time by 30% and lower water usage. Facility expansion in Brazil enhances its zero-waste model by converting residual biomass into energy pellets. R&D efforts are focused on phlorotannin applications for food preservation and shelf-life extension. Strong integration of forestry and processing ensures supply stability and sustainability leadership.

Laffort Drives Precision Oenology with High-Purity Tannins for Wine Stability and Color Optimization

Laffort is a global leader in oenological tannins, focusing on high-purity extracts for premium wine production. Its QUERTANIN™ range provides ellagic tannins for advanced redox control in aging processes. OxyProtect technology enhances color stabilization by forming durable tannin-anthocyanin complexes. Research presented in 2026 highlights tannins as protective agents that extend wine longevity up to threefold. The company’s IDP tannins enable instant dissolution, improving process precision during fermentation. Strong specialization in wine chemistry positions Laffort at the high-value end of the tannin market.

Indunorm Expands Chestnut-Based Functional Tannins for Animal Nutrition and Eco-Friendly Coatings

Indunorm, in partnership with Tanin Sevnica, specializes in chestnut-derived tannins with enhanced bioavailability through enzymatic hydrolysis. The company achieved a 15% yield increase in 2025, improving production efficiency. Its Farmatan® range is widely used in animal nutrition as a zinc oxide alternative for gut health. Expansion of compliance infrastructure supports cross-border trade in regulated EU markets. Industrial applications include corrosion-inhibiting tannins for eco-friendly coatings, reducing heavy metal content by 92%. Diversified use across feed and coatings strengthens its market positioning.

Ajinomoto Targets High-Purity Tannins for Pharmaceuticals and Semiconductor Applications Through Advanced Purification

Ajinomoto OmniChem focuses on high-purity tannic acid for pharmaceutical and electronic-grade applications. Expansion of its Belgium facility enhances production of ultra-refined tannins used in semiconductor etching and stabilization. Pharmaceutical demand increased by 12% in 2025, driven by wound care and anti-inflammatory formulations. The company is developing amino acid-tannin blends for nutraceutical applications targeting cognitive and gut health. EcoVadis Gold certification reflects strong sustainability practices in sourcing gallnut raw materials. Advanced purification and specialty applications position Ajinomoto in premium tannin segments.

Italy Tannin Market Anchored in Circular Leather, Enology Innovation, and Agri-Biostimulants

Italy continues to position itself as a global reference point for high-value tannin applications driven by sustainability, craftsmanship, and advanced processing. In 2025, Silvateam S.p.A. expanded its San Michele Mondovì operations, optimizing the extraction of hydrolyzable tannins from chestnut wood. The deployment of a closed-loop water recovery system achieving 98% reuse has set a new environmental benchmark for green chemical manufacturing in Europe, while also lowering operating risk under tightening EU water directives. This investment strengthens Italy’s leadership in chestnut-based tannins used across leather, food, and technical applications.

Downstream, Italian leather clusters in Tuscany and Veneto have accelerated adoption of the Ecotan tanning process through 2024 and 2025. This metal-free, vegetable tannin-based technology enables fully biodegradable leather and supports circularity at end of life, aligning with EU chemical safety and waste reduction policies. Parallel innovation is visible in the wine sector, where Piedmont-based enological firms introduced grape-seed and oak-derived tannins in late 2025 to manage redox potential and color stability in premium organic wines without sulfur dioxide. Beyond industrial uses, tannins are increasingly integrated into agriculture and food preservation. The Italian Ministry of Agriculture reported a 15% increase in domestic use of tannin-based biostimulants in 2025, while research led by the University of Turin demonstrated the potential of ellagitannins as clean-label preservatives in processed meat, signaling future substitution of synthetic nitrites.

Brazil Tannin Market Defined by Certified Forestry, Leather Efficiency, and Feed Applications

Brazil’s tannin market is structurally advantaged by its scale in black wattle forestry and its rapid alignment with international sustainability standards. In 2025, TANAC S.A. achieved full FSC and PEFC certification across its forest assets, securing a long-term, traceable supply of Acacia mearnsii for export-oriented vegetable tannins. This certification milestone reinforces Brazil’s credibility as a reliable supplier to leather, wood, and chemical markets across more than 60 countries.

Technological upgrading has shifted focus from volume to efficiency. TANAC’s Green-Line premium range, launched in mid-2025, improves tannin exhaustion rates in leather processing, enabling higher fiber absorption and materially reducing effluent chemical load. This aligns with stricter wastewater norms in importing regions. Brazil is also broadening tannin utilization beyond leather. Upgraded Silvafeed production lines in 2025 responded to rising demand for tannin-based animal nutrition additives, increasingly positioned as natural alternatives to antibiotic growth promoters in poultry and swine. Looking ahead, early 2026 pilot programs by Brazilian furniture manufacturers are validating condensed tannin-based, formaldehyde-free wood adhesives that meet the highest indoor air quality standards, opening a new technical materials pathway for the sector.

China Tannin Market Strengthened by Vertical Integration and Specialty Chemical Diversification

China remains the dominant global supplier of gallnut-based tannic acid, with 2025 marking a decisive shift toward supply chain stabilization and higher-value end uses. Producers in Hunan and Hubei provinces implemented vertical integration strategies, establishing direct cultivation partnerships with foresters to secure gallnut availability and dampen raw material price volatility. This move has reinforced China’s cost leadership while improving traceability for pharmaceutical and food-grade markets.

At the specialty end, Chinese manufacturers are scaling pharmaceutical-grade tannins. In late 2025, Hunan Gomeet Biotechnology expanded capacity for ultra-high-purity tannic acid exceeding 99% assay, targeting antiviral formulations and advanced drug delivery coatings. Regulatory developments have also influenced application innovation. Restrictions on antimony exports during 2024 and 2025 accelerated domestic R&D into tannin-based flame retardants as bio-based alternatives for textiles and polymers. Concurrently, under the 14th Five-Year Energy Plan, dyeing clusters in the Pearl River Delta have been subsidized to transition toward natural tannin dyes for cotton and silk, supporting China’s push into high-end sustainable fashion exports.

Peru Tannin Market Driven by Tara Pod Expansion and Integrated Extraction Economics

Peru occupies a strategic niche as the world’s primary source of Tara-based tannins, valued for their clarity and consistency in food and pharmaceutical applications. In 2025, the Peruvian government launched a national expansion program to increase Tara plantations by 2,500 hectares in the Andean highlands, directly addressing global demand growth for food-grade and beverage-stabilizing tannins.

Industrial capacity expansion has followed upstream policy support. Ajinomoto OmniChem expanded its Tara-based extraction units in Peru during 2025, focusing on hydrolyzable gallotannins for beverage clarification and pharmaceutical excipients. Process innovation is further enhancing economics. Peruvian processors introduced dual-extraction methods in late 2025 that allow simultaneous recovery of Tara gum and tannins from a single feedstock, materially improving yield per ton and reinforcing Peru’s competitiveness as a low-waste, high-value tannin origin.

Comparative Snapshot: Tannin Market by Country

Tannin Market County Level Snapshot

|

Country

|

Core Feedstock

|

Strategic Focus Area

|

Market Differentiation

|

|

Italy

|

Chestnut wood, grape, oak

|

Circular leather, enology, biostimulants

|

High-value, sustainability-led innovation

|

|

Brazil

|

Black wattle

|

Certified forestry, leather efficiency, feed

|

Scale with environmental credibility

|

|

China

|

Gallnuts

|

Vertical integration, pharma-grade tannins

|

Cost leadership with specialty expansion

|

|

Peru

|

Tara pods

|

Food-grade clarity, dual extraction

|

High yield, low-waste production model

|

Tannin Market Report Scope

Tannin Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.9 Billion

|

|

Market Size (2034)

|

$6.8 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Source Type (Wood-Based, Fruit and Seed-Based, Marine-Based, Leaf-Based), By Product Form (Tannin Extracts, Tannin Powders, Tannin Solutions), By Chemical Classification (Hydrolyzable Tannins, Condensed Tannins, Phlorotannins), By Application (Leather Tanning, Wine and Beverages, Animal Nutrition, Wood Adhesives, Pharmaceuticals and Nutraceuticals, Cosmetics and Personal Care, Water Treatment)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Silvateam S.p.A., TANAC S.A., Ajinomoto OmniChem N.V., Laffort S.A., W. R. Grace & Co., Unitán S.A.I.C.A., Seta S.A., Hunan Gomeet Biotechnology Co., Ltd., Wufeng Chicheng Biotech Co., Ltd., Tanin Sevnica d.d., Polson Ltd., UCL Company (Pty) Ltd., Forestal Mimosa Ltd., Ever S.r.l., Indunor S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Tannin Market Segmentation

By Source Type

- Wood-Based

- Fruit and Seed-Based

- Marine-Based

- Leaf-Based

By Product Form

- Tannin Extracts

- Tannin Powders

- Tannin Solutions

By Chemical Classification

- Hydrolyzable Tannins

- Condensed Tannins

- Phlorotannins

By Application

- Leather Tanning

- Wine and Beverages

- Animal Nutrition

- Wood Adhesives

- Pharmaceuticals and Nutraceuticals

- Cosmetics and Personal Care

- Water Treatment

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Tannin Industry

- Silvateam S.p.A.

- TANAC S.A.

- Ajinomoto OmniChem N.V.

- Laffort S.A.

- W. R. Grace & Co.

- Unitán S.A.I.C.A.

- Seta S.A.

- Hunan Gomeet Biotechnology Co., Ltd.

- Wufeng Chicheng Biotech Co., Ltd.

- Tanin Sevnica d.d.

- Polson Ltd.

- UCL Company (Pty) Ltd.

- Forestal Mimosa Ltd.

- Ever S.r.l.

- Indunor S.A.

*- List not Exhaustive