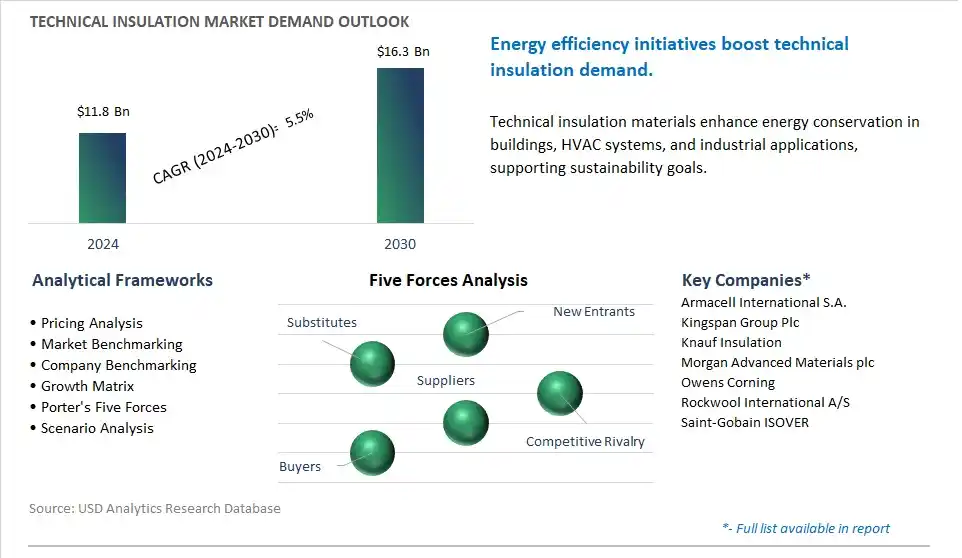

The global Technical Insulation Market is poised to register a 5.5% CAGR from $11.8 Billion in 2024 to $16.3 Billion in 2030.

The global Technical Insulation Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Material (Hot Insulation, Cold-Flexible Insulation, Cold-Rigid Insulation), By Application (Industrial Process, Heating and Plumbing, Acoustic, HVAC, Refrigeration), By End-User (Industrial, Energy, Transportation, Commercial Buildings, Others).

An Introduction to Global Technical Insulation Market in 2024

Technical insulation encompasses a range of materials and systems used to regulate temperature, prevent heat loss or gain, and control noise and vibration in industrial, commercial, and residential buildings, as well as in industrial processes and equipment. The future of technical insulation is shaped by several key trends, including advancements in insulation materials, energy efficiency regulations, and sustainability initiatives. One significant trend is the development of high-performance insulation materials with improved thermal conductivity, fire resistance, and environmental sustainability attributes, meeting the evolving needs of building owners, architects, and engineers for energy-efficient and environmentally friendly building solutions. Manufacturers are investing in research and development to innovate new insulation materials such as aerogels, vacuum insulation panels (VIPs), and phase change materials (PCMs), which offer superior insulation performance in a compact and lightweight form factor, enabling architects and designers to optimize building envelope designs and achieve net-zero energy goals. Additionally, the integration of smart insulation systems with sensors, controls, and automation technologies is driving innovations in building energy management, enabling real-time monitoring, optimization, and predictive maintenance of thermal and acoustic insulation systems, reducing energy consumption and operational costs while improving occupant comfort and productivity. Moreover, the growing emphasis on sustainable construction practices and green building certifications is driving demand for insulation materials with low embodied carbon, recycled content, and recyclability, promoting circular economy principles and reducing environmental impact throughout the lifecycle of buildings. Furthermore, collaborations between insulation manufacturers, building contractors, and energy consultants are driving innovation and market growth by delivering customized solutions that meet the specific performance, regulatory, and sustainability requirements of diverse building projects and environments, ensuring continued adoption and advancement of technical insulation in the construction industry.

Technical Insulation Market Competitive Landscape

The market report analyses the leading companies in the industry including Armacell International S.A., Kingspan Group Plc, Knauf Insulation, Morgan Advanced Materials plc, Owens Corning, Rockwool International A/S, Saint-Gobain ISOVER.

Technical Insulation Market Dynamics

Technical Insulation Market Trend: Growing Demand for Energy-Efficient and Sustainable Building Solutions

A prominent market trend in the technical insulation industry is the increasing demand for energy-efficient and sustainable building solutions. Technical insulation plays a crucial role in enhancing the energy efficiency, thermal comfort, and environmental performance of buildings by reducing heat loss, preventing condensation, and improving indoor air quality. With growing awareness of climate change, energy conservation, and green building practices, there is a rising demand for high-performance insulation materials that help reduce carbon footprint and operating costs in residential, commercial, and industrial buildings. This trend is driven by regulatory requirements, energy efficiency standards, and incentives for green building certification, driving the adoption of innovative insulation solutions that meet stringent performance criteria and sustainability goals.

Technical Insulation Market Driver: Stringent Regulations and Building Energy Codes

A key driver behind the growth of the technical insulation market is stringent regulations and building energy codes aimed at reducing energy consumption and greenhouse gas emissions in the construction sector. Governments worldwide are implementing building codes, standards, and policies that mandate the use of energy-efficient building materials and technologies to achieve sustainability targets and mitigate climate change impacts. Technical insulation materials, such as mineral wool, foam plastics, and aerogels, help buildings comply with thermal performance requirements, moisture management guidelines, and fire safety regulations. The need for compliance with building codes and energy efficiency standards, coupled with incentives for energy-efficient building design and construction, drives the demand for technical insulation products and solutions in both new construction and retrofit projects.

Technical Insulation Market Opportunity: Innovation in Sustainable Insulation Materials and Systems

An opportunity exists for technical insulation manufacturers to innovate sustainable insulation materials and systems that address emerging market needs and industry trends. With advancements in materials science, manufacturing processes, and construction technology, there is potential to develop next-generation insulation products with improved thermal performance, durability, and environmental sustainability. Manufacturers can explore renewable and recycled materials, bio-based insulation options, and low-emission products that minimize environmental impact and promote indoor air quality. Additionally, there is an opportunity to integrate insulation systems with smart building technologies, energy management systems, and renewable energy solutions to create holistic and integrated building envelopes that optimize energy efficiency and occupant comfort. By investing in research and development of innovative insulation solutions and collaborating with industry stakeholders, technical insulation manufacturers can capitalize on the growing demand for sustainable building materials and position themselves as leaders in the green construction market.

Technical Insulation Market Share Analysis: Cold-Rigid Insulation generated the highest revenue in 2024

The largest segment in the Technical Insulation Market is the Cold-Rigid Insulation category. This is primarily because cold-rigid insulation materials are widely used in various industries for their excellent thermal insulation properties, particularly in applications where low temperatures need to be maintained or where thermal efficiency is critical. Cold-rigid insulation materials are made of rigid foam materials such as polyurethane (PUR) or extruded polystyrene (XPS), which provide superior thermal resistance and structural integrity. They are commonly used in refrigeration, HVAC (heating, ventilation, and air conditioning), and cryogenic applications to prevent heat transfer and maintain stable temperatures. Additionally, cold-rigid insulation materials offer advantages such as moisture resistance, durability, and ease of installation, making them preferred choices for a wide range of industrial and commercial applications. Hence, the widespread use and demand for cold-rigid insulation materials contribute to their dominance as the largest segment in the Technical Insulation Market.

Technical Insulation Market Share Analysis: HVAC (Heating, Ventilation, and Air Conditioning) segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest growing segment in the Technical Insulation Market is the HVAC (Heating, Ventilation, and Air Conditioning) category. There is a rising demand for energy-efficient solutions in buildings and industrial facilities to reduce energy consumption and comply with stringent environmental regulations. HVAC systems play a crucial role in maintaining comfortable indoor temperatures and air quality, and effective insulation is essential for optimizing their performance and energy efficiency. Accordingly, there is an increasing emphasis on upgrading and retrofitting existing HVAC systems with high-performance insulation materials to enhance thermal efficiency and reduce heating and cooling costs. Additionally, the growing construction activities, especially in emerging economies, contribute to the rising demand for HVAC systems and insulation materials. Furthermore, advancements in insulation technologies, such as the development of innovative materials with improved thermal resistance and fire-retardant properties, further drive the adoption of technical insulation in HVAC applications. Over the forecast period, the growing awareness of energy conservation and the need for sustainable building practices propel the demand for technical insulation in HVAC systems, making it the fastest growing segment in the Technical Insulation Market.

Technical Insulation Market Share Analysis: Energy segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest growing segment in the Technical Insulation Market is the Energy sector. There is a global shift towards renewable energy sources such as solar, wind, and hydroelectric power to reduce reliance on fossil fuels and mitigate climate change. Technical insulation plays a vital role in energy production and distribution systems by minimizing heat loss and optimizing energy efficiency. As governments worldwide implement policies and incentives to promote renewable energy adoption, there is an increasing demand for technical insulation solutions to improve the performance and reliability of energy infrastructure. Additionally, the ongoing transition towards electric vehicles and the electrification of transportation systems contribute to the growing demand for technical insulation in energy storage and transmission applications. Furthermore, the expansion of energy-efficient building initiatives and green building standards drives the adoption of technical insulation in residential, commercial, and institutional buildings to reduce energy consumption and greenhouse gas emissions. Over the forecast period, the growing emphasis on sustainability, coupled with investments in renewable energy and energy-efficient technologies, fuels the rapid growth of the Energy sector in the Technical Insulation Market.

Technical Insulation Market Report Segmentation

By Material

Hot Insulation

Cold-Flexible Insulation

Cold-Rigid Insulation

By Application

Industrial Process

Heating and Plumbing

Acoustic

HVAC

Refrigeration

By End-User

Industrial

Energy

Transportation

Commercial Buildings

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Technical Insulation Companies Profiled in the Market Study

Armacell International S.A.

Kingspan Group Plc

Knauf Insulation

Morgan Advanced Materials plc

Owens Corning

Rockwool International A/S

Saint-Gobain ISOVER

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Technical Insulation Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Technical Insulation Market Size Outlook, $ Million, 2021 to 2030

3.2 Technical Insulation Market Outlook by Type, $ Million, 2021 to 2030

3.3 Technical Insulation Market Outlook by Product, $ Million, 2021 to 2030

3.4 Technical Insulation Market Outlook by Application, $ Million, 2021 to 2030

3.5 Technical Insulation Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Technical Insulation Industry

4.2 Key Market Trends in Technical Insulation Industry

4.3 Potential Opportunities in Technical Insulation Industry

4.4 Key Challenges in Technical Insulation Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Technical Insulation Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Technical Insulation Market Outlook by Segments

7.1 Technical Insulation Market Outlook by Segments, $ Million, 2021- 2030

By Material

Hot Insulation

Cold-Flexible Insulation

Cold-Rigid Insulation

By Application

Industrial Process

Heating and Plumbing

Acoustic

HVAC

Refrigeration

By End-User

Industrial

Energy

Transportation

Commercial Buildings

Others

8 North America Technical Insulation Market Analysis and Outlook To 2030

8.1 Introduction to North America Technical Insulation Markets in 2024

8.2 North America Technical Insulation Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Technical Insulation Market size Outlook by Segments, 2021-2030

By Material

Hot Insulation

Cold-Flexible Insulation

Cold-Rigid Insulation

By Application

Industrial Process

Heating and Plumbing

Acoustic

HVAC

Refrigeration

By End-User

Industrial

Energy

Transportation

Commercial Buildings

Others

9 Europe Technical Insulation Market Analysis and Outlook To 2030

9.1 Introduction to Europe Technical Insulation Markets in 2024

9.2 Europe Technical Insulation Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Technical Insulation Market Size Outlook by Segments, 2021-2030

By Material

Hot Insulation

Cold-Flexible Insulation

Cold-Rigid Insulation

By Application

Industrial Process

Heating and Plumbing

Acoustic

HVAC

Refrigeration

By End-User

Industrial

Energy

Transportation

Commercial Buildings

Others

10 Asia Pacific Technical Insulation Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Technical Insulation Markets in 2024

10.2 Asia Pacific Technical Insulation Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Technical Insulation Market size Outlook by Segments, 2021-2030

By Material

Hot Insulation

Cold-Flexible Insulation

Cold-Rigid Insulation

By Application

Industrial Process

Heating and Plumbing

Acoustic

HVAC

Refrigeration

By End-User

Industrial

Energy

Transportation

Commercial Buildings

Others

11 South America Technical Insulation Market Analysis and Outlook To 2030

11.1 Introduction to South America Technical Insulation Markets in 2024

11.2 South America Technical Insulation Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Technical Insulation Market size Outlook by Segments, 2021-2030

By Material

Hot Insulation

Cold-Flexible Insulation

Cold-Rigid Insulation

By Application

Industrial Process

Heating and Plumbing

Acoustic

HVAC

Refrigeration

By End-User

Industrial

Energy

Transportation

Commercial Buildings

Others

12 Middle East and Africa Technical Insulation Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Technical Insulation Markets in 2024

12.2 Middle East and Africa Technical Insulation Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Technical Insulation Market size Outlook by Segments, 2021-2030

By Material

Hot Insulation

Cold-Flexible Insulation

Cold-Rigid Insulation

By Application

Industrial Process

Heating and Plumbing

Acoustic

HVAC

Refrigeration

By End-User

Industrial

Energy

Transportation

Commercial Buildings

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Armacell International S.A.

Kingspan Group Plc

Knauf Insulation

Morgan Advanced Materials plc

Owens Corning

Rockwool International A/S

Saint-Gobain ISOVER

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Material

Hot Insulation

Cold-Flexible Insulation

Cold-Rigid Insulation

By Application

Industrial Process

Heating and Plumbing

Acoustic

HVAC

Refrigeration

By End-User

Industrial

Energy

Transportation

Commercial Buildings

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)