AI-Driven Solutions, Strategic Partnerships, and Specialized Platforms Accelerate Growth in the Telemedicine Market

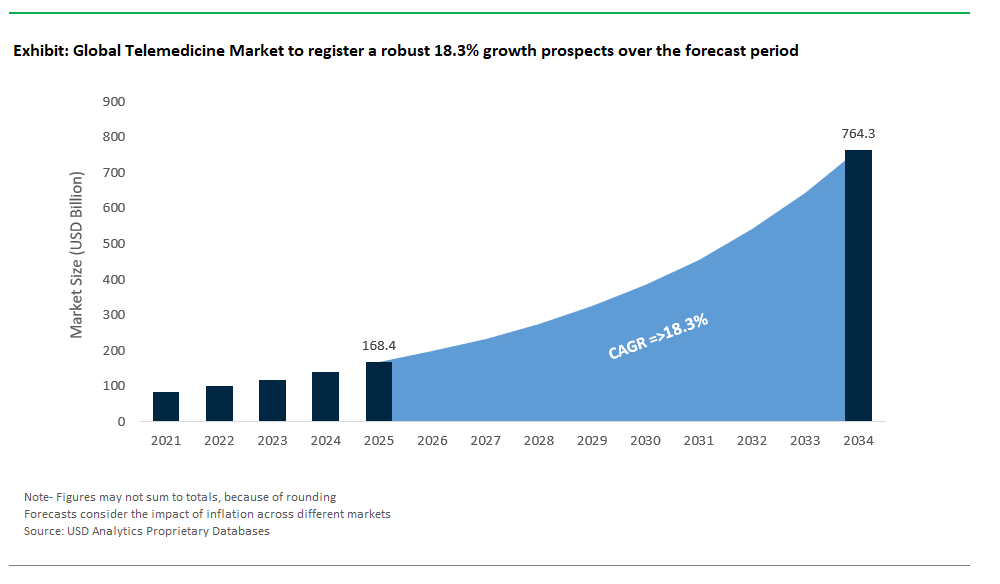

The Global Telemedicine Market Size is estimated at $168.4 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 18.3% to reach $764.2 Billion by 2034.

The telemedicine market is undergoing transformative change as groundbreaking technological advancements and strategic partnerships accelerate its global adoption. In January 2025, SS Innovations International set a new benchmark by successfully performing the world’s first robotic cardiac telesurgeries in India using the SSi Mantra 3 Surgical Robotic System. This historic event showcases how telemedicine is now capable of facilitating even the most complex, life-saving procedures remotely heralding a new era of high-precision, accessible healthcare. Around the same time, industry giant Teladoc Health joined forces with Amazon to expand chronic condition management programs including diabetes and hypertension through Amazon’s Health Benefits Connector, integrating telemedicine into mainstream employee health ecosystems and broadening access to digital care for chronic disease management.

Leading virtual care providers are also leveraging collaboration and acquisitions to enhance diagnostic capabilities and streamline care delivery. In December 2024, DocGo Inc. partnered with SHL Telemedicine to integrate SmartHeart portable ECG devices into mobile healthcare units, enabling comprehensive, real-time cardiac assessments in remote settings. The rise of specialized telemedicine platforms is further illustrated by LTR Pharma’s partnership with the Restorative Sexual Health Clinic to launch a men’s health platform in November 2024, delivering virtual consultations, therapeutic services, and prescription treatments tailored for male patients. Meanwhile, MeMD’s acquisition of TeamHealth VirtualCare in September 2024 aims to boost operational efficiency and clinical capacity, allowing health systems and payers to consolidate and scale their virtual care offerings for urgent and primary care needs.

Innovation continues with a focus on niche services and AI integration, expanding the reach and effectiveness of telemedicine. C3 Med-Tech’s funding for AI-driven portable eye checkup devices in June 2024 reflects the market’s move toward mobile, specialized diagnostic tools that make expert eye care more widely available through telemedicine. The launch of TeleRare Health’s virtual care platform for rare diseases in April 2024 is addressing critical unmet needs by connecting patients with rare conditions to expert clinicians and advanced molecular diagnostics from anywhere in the world. Across the industry, leading players such as Philips, Teladoc, and Amwell are continuously enhancing their platforms with AI and machine learning introducing features like AI-powered diagnostics, predictive analytics for personalized care, and virtual health assistants to streamline operations and improve patient experience. Together, these recent developments are setting new standards in the telemedicine market, driving its rapid growth and reshaping how healthcare is delivered globally.

Transformative Shifts in the Telemedicine Market

Trend: AI-Powered Triage for Low-Acuity Conditions

The telemedicine market is experiencing substantial growth fueled by the rise of AI-powered triage solutions tailored for diagnosing low-acuity medical conditions remotely. Advanced AI diagnostic tools, notably those paired with smartphone-based attachments, have proven exceptionally effective, significantly enhancing diagnostic accuracy and speed compared to traditional methods. For instance, smartphone otoscopes integrated with AI technology have demonstrated superior accuracy in diagnosing ear infections, outperforming conventional examinations by primary care physicians. This development represents a critical milestone, promising increased efficiency and precision in telemedicine assessments, ultimately improving patient outcomes and satisfaction.

The regulatory environment is further accelerating this trend, particularly with expedited FDA approval pathways supporting rapid commercialization of AI-powered diagnostic tools, notably in respiratory illness triage. Such regulatory facilitation has led to a notable surge in available clinical-grade AI diagnostic technologies, streamlining patient assessments and enabling quicker, more informed clinical decisions in virtual healthcare environments. As healthcare providers increasingly embrace these sophisticated AI tools, the telemedicine sector is poised for further growth, driven by heightened diagnostic capabilities and broader adoption among healthcare professionals seeking to enhance remote patient care.

Opportunity: Virtual Care for Incarcerated Populations

The provision of virtual healthcare for incarcerated populations represents a significant and rapidly expanding opportunity within the telemedicine market. Correctional facilities across the United States consistently grapple with challenges in providing adequate specialist medical care due to limited on-site healthcare personnel. Telemedicine directly addresses this critical gap, markedly reducing the reliance on costly and logistically complex transfers of incarcerated individuals for specialist consultations, thus offering considerable financial savings for correctional healthcare systems while simultaneously improving access to essential medical care.

Furthermore, growing awareness regarding the prevalence and impact of mental health conditions within incarcerated populations is driving significant expansion of virtual mental healthcare services, particularly tele-psychiatry. Numerous states are now adopting policies enabling Medicaid reimbursement for tele-psychiatric services delivered in correctional environments, substantially broadening access and incentivizing further deployment of these virtual care solutions. This favorable reimbursement landscape highlights an expansive and largely untapped market opportunity for telemedicine providers specializing in correctional healthcare, positioning virtual mental health solutions as a crucial growth segment within the broader telemedicine industry.

Competitive Landscape: Telemedicine Market

The telemedicine market is rapidly transforming global healthcare delivery by bridging access gaps, reducing costs, and enabling real-time care through virtual platforms. Growth is driven by increasing consumer demand for convenience, rising adoption of remote health solutions post-pandemic, and integration of AI-driven diagnostics, chronic care management, and mental health services. Companies are competing on technological capabilities, service diversity, global reach, and partnerships with healthcare systems and employers. Emerging trends include subscription-based care, integration with wearable health devices, and specialized veterinary telehealth platforms, creating a multi-dimensional competitive ecosystem.

Teladoc Health – Global Leader in Comprehensive Virtual Care

Teladoc Health dominates the telemedicine landscape with its end-to-end digital health ecosystem, offering services that range from general virtual consultations to specialized care for chronic conditions and mental health. Through the integration of Livongo, Teladoc provides advanced chronic disease management programs for diabetes, hypertension, and weight control, incorporating remote monitoring and AI-powered insights for personalized care. Its portfolio extends to mental health therapy via BetterHelp, dermatology, nutrition counseling, and expert medical opinions, supported by AI-driven analytics to enhance care delivery. Recent initiatives include the launch of Primary360, a nationwide primary care service, and the expansion of myStrength Complete for integrated mental health support. Strategic partnerships with Microsoft and Amazon enable Teladoc to embed telehealth in widely used platforms like Teams and Alexa, while collaborations with insurers and health systems solidify its B2B presence. With a footprint in 175 countries and 50 million members, Teladoc leverages subscription and licensing models for revenue diversification. Despite facing challenges such as the Livongo goodwill write-down, Teladoc continues to lead through innovation, scale, and commitment to a connected care ecosystem.

Vetster (Rover Group) – Digital-First Veterinary Telemedicine Pioneer

Vetster is redefining pet telehealth by providing 24/7 on-demand access to licensed veterinarians through a user-friendly platform that supports video consultations, prescriptions, and personalized treatment plans. By addressing a critical pain point veterinary shortages and accessibility gaps Vetster empowers pet parents with quick, affordable care while reducing dependency on in-clinic visits for non-emergency issues. The platform emphasizes seamless digital health history management and tele-triage, ensuring continuity of care. Recognized as Pet App of the Year (2023), Vetster has scaled rapidly, expanding into 100+ countries and growing through B2B partnerships that integrate telehealth into employee benefit programs. Following its acquisition by Rover Group, Vetster benefits from Rover’s extensive pet owner base, reinforcing its competitive edge in brand visibility and user trust. Its direct-to-consumer subscription model combined with global reach positions Vetster as a leading innovator in virtual veterinary care.

Airvet – Employer-Focused Veterinary Telehealth Platform

Airvet has carved out a niche in the telemedicine market by positioning itself as a comprehensive pet care benefit for employers. Its platform delivers 24/7 on-demand access to veterinarians, specialized consultations for behavioral and dietary needs, and prescription services compliant with regulatory standards. Airvet’s partnerships with major corporations like Adobe and Manulife highlight its strength in B2B integration, offering value-driven employee benefits. Recent milestones include regulatory breakthroughs such as becoming the first platform to establish fully VCPR-compliant telemedicine visits in California and expanding into India, signaling a commitment to international growth. Enhanced features like multilingual support and expanded specialist services strengthen accessibility and engagement. By leveraging strategic partnerships with pet product and insurance companies, Airvet builds a holistic ecosystem for pet wellness, making it a preferred platform for enterprises seeking innovative employee benefits and pet health solutions.

Pawp – Subscription Model with Emergency Coverage

Pawp stands out with its affordable, subscription-based telehealth model that combines unlimited virtual consultations with a $3,000 annual emergency fund, providing both convenience and financial security for pet owners. Available 24/7, Pawp offers immediate access to licensed veterinary professionals for health assessments, tele-triage, and behavioral advice, reducing unnecessary emergency visits. By focusing on personalized care plans and affordability, Pawp appeals to cost-conscious consumers while delivering peace of mind through its emergency protection feature. The brand emphasizes continuous improvement of its platform and has built a reputation for responsive, life-saving interventions backed by positive user testimonials. As demand for subscription-based healthcare solutions rises, Pawp’s model offers a scalable approach that combines preventive care with financial safeguards, positioning it as a disruptor in the pet telemedicine segment.

Dutch – AI-Enhanced Virtual Veterinary Care

Dutch, owned by Alleyes, is revolutionizing pet telehealth by integrating AI-driven tools into its virtual care ecosystem, significantly improving veterinary efficiency and reducing administrative burdens. Its platform provides unlimited video and chat consultations, prescription services, and a focus on managing chronic conditions such as allergies and anxiety, now expanding to over 150 treatable conditions. A key differentiator is Dutch’s proprietary AI technology embedded in its EMR system, which automates post-visit summaries and reduces admin time by 50%, addressing the critical issue of veterinary burnout. Dutch has facilitated over 700,000 telehealth visits and doubled revenues annually since its launch in 2021, reflecting robust market adoption. Backed by leading investors and integrated partnerships with pharmacies and pet food companies, Dutch combines subscription-based care, advanced AI, and personalized health programs, positioning itself at the forefront of next-generation veterinary telemedicine.

Market Share and Segmentation Insights: Telemedicine Market

By Type: Tele-hospitals Lead, mHealth Records Fastest Growth

Tele-hospitals dominate the telemedicine market with the largest market share of 44.7% in 2025, driven by strong institutional adoption in hospitals and clinics offering remote consultations and chronic care management. This segment benefits from healthcare systems integrating telemedicine into their existing workflows for specialty care and acute patient monitoring. mHealth is projected to grow at the fastest CAGR of 19.1%, fueled by widespread smartphone adoption, AI-powered health monitoring apps, and wearable device connectivity that supports chronic disease management and fitness tracking. Tele-homes are also witnessing rising demand as aging populations and post-acute care needs increase globally, enhancing home-based virtual care adoption.

.png)

By Mode of Delivery: Cloud-Based Platforms Dominate with Highest Growth Rate

Cloud-based delivery accounts for the largest market share at 49.5% in 2025, owing to its scalability, cost-efficiency, and ability to integrate advanced technologies such as AI for diagnostics and real-time patient analytics. This delivery mode also registers the fastest CAGR of 18.9%, as healthcare providers increasingly shift from legacy on-premise systems to flexible, secure, and interoperable cloud infrastructure to manage rising patient volumes. Web-based delivery continues to hold relevance for electronic health record (EHR) integration and patient portals, while on-premise solutions remain critical for data-sensitive applications but are constrained by high maintenance and infrastructure costs.

United States: Telemedicine Market Accelerates with Policy Innovation and Ecosystem Integration

The United States telemedicine market is undergoing dynamic transformation driven by regulatory enhancements and integration with broader digital health ecosystems. In November 2024, the Centers for Medicare & Medicaid Services (CMS) finalized substantial updates to the Physician Fee Schedule (PFS) and Medicare Part B, effective January 2025, with the goal of making telehealth services more accessible and financially viable. This policy progress is expected to further catalyze adoption among both providers and patients, with chronic care management standing out as a key beneficiary. A major industry milestone was marked in January 2025 when Teladoc Health partnered with Amazon to expand access to chronic care programs, leveraging Amazon Health Benefits Connector to provide telemedicine-based management for conditions such as diabetes and hypertension. This collaboration highlights the market’s movement towards seamless integration of telemedicine into everyday health management and employer benefit platforms.

Additionally, the U.S. market has seen significant innovation in mobile healthcare delivery and virtual care specialization. DocGo Inc.’s partnership with SHL Telemedicine in December 2024 enabled the deployment of portable ECG diagnostics within mobile healthcare units, expanding the clinical utility of telemedicine for home-based care. The acquisition of TeamHealth VirtualCare by MeMD (Fabric Labs) in September 2024 strengthened operational efficiency and expanded virtual care networks for health systems nationwide. Meanwhile, the launch of niche virtual care platforms like TeleRare Health in April 2024, focusing exclusively on rare diseases, illustrates growing market specialization. These developments collectively position the United States as a global leader in telemedicine, marked by strong reimbursement policies, technological advancement, and an expanding ecosystem of specialized providers and partnerships.

Germany: Telemedicine Market Strengthened by Landmark Digital Legislation and e-Prescription Rollout

Germany’s telemedicine market is advancing rapidly, propelled by the passage of the Digital Act (DigiG) in February 2024, which introduced transformative changes such as e-prescriptions, electronic patient records, and robust telemedicine guidelines. This legislative milestone is fundamentally reshaping healthcare delivery by enhancing transparency, accessibility, and interoperability of digital health services throughout the country. As a result, German healthcare providers are seeing increased patient acceptance and uptake of telemedicine platforms, facilitated by leading technology providers like Compugroup Medical SE. Favorable reimbursement frameworks, supported by statutory health insurance guidelines, have made it financially attractive for providers to offer virtual consultations, thereby mainstreaming telemedicine across various medical specialties.

One of the most significant developments in Germany is the widespread adoption of e-prescriptions, streamlining the process from virtual consultation to medication delivery and integrating telemedicine deeply into daily clinical workflows. Patient convenience and access to specialists have been notably improved, particularly in rural and underserved areas. Ongoing digital health initiatives continue to reinforce Germany’s position as a pioneer in digital healthcare, offering a replicable model for telemedicine integration that prioritizes patient outcomes, efficiency, and data security.

United Kingdom: Telemedicine Expands via NHS Digital Integration and Collaborative Infrastructure

The United Kingdom’s telemedicine market is evolving swiftly, driven by the NHS’s commitment to digital integration and cross-industry partnerships. In February 2024, NHS England’s Wireless Trials program allocated £1 million to accelerate the deployment of advanced wireless technologies, directly supporting telehealth solutions and care optimization across multiple trusts. This digital-first approach has expedited the delivery of primary care, clinical trials, and chronic disease management through virtual platforms, reflecting a central objective of the NHS Long Term Plan.

Mental health has emerged as a key telemedicine use case, with platforms like Talkspace playing an increasingly prominent role in expanding online access to therapy and counseling. The infrastructure backbone is supported by major telecommunications providers BT, Virgin Media, and Sky which have partnered with the NHS to build reliable, scalable telehealth systems for practitioners and patients. The UK’s vibrant telemedicine ecosystem is thus characterized by rapid adoption, cross-sector collaboration, and a strategic focus on expanding access to both physical and mental health services.

France: Fast-Track Access and Policy Innovation Drive Telemedicine Market Growth

France has established itself as a European frontrunner in telemedicine through innovative policy and regulatory advancements. In September 2024, the government launched a fast-track market access pathway for digital health applications and telemonitoring, designed to benefit up to 60 million citizens covered by mandatory health insurance. This initiative underscores a strong national commitment to healthcare innovation and democratized care delivery. Additionally, reimbursement for a wide array of teleconsultations including physician, nurse, and speech therapist visits has been broadened, making telemedicine both accessible and financially sustainable for patients and providers.

The French market has also prioritized the use of telemedicine in chronic disease management, leveraging digital solutions to support ongoing care for patients with complex or long-term conditions. French startups such as Doctolib and Qare have reported strong user growth and platform adoption, highlighting the sector’s dynamism and high patient engagement. The combination of robust policy frameworks, accelerated digital application approval, and growing provider-patient uptake solidifies France’s position as a leader in the digital health and telemedicine sector.

India: Telemedicine Market Innovates with Remote Surgery and Digital Health Initiatives

India’s telemedicine market is experiencing unprecedented growth, propelled by technological breakthroughs and government-driven digital health initiatives. In January 2025, SS Innovations International achieved a global first by performing two successful robotic cardiac telesurgeries using its SSi Mantra 3 Surgical Robotic System, underscoring the nation’s capacity for advanced remote healthcare delivery. Simultaneously, the Medanta e-ICU Command Centre, launched in collaboration with GE HealthCare, enables 24/7 advanced critical care monitoring and consultation, revolutionizing access to specialized care across India’s vast geography.

Government policy has been instrumental in supporting the adoption of telemedicine, especially in rural and remote regions where connectivity is critical. Ongoing investment in digital health infrastructure and internet expansion has laid the groundwork for telemedicine services to bridge access gaps, offering primary and specialty care to underserved populations. The government’s sustained focus on digital health, combined with private sector innovation, continues to transform India’s healthcare landscape delivering cost-effective, quality care through virtual means.

Canada: Telemedicine Market Matures with EHR Integration and Mental Health Services

Canada’s telemedicine market has matured significantly, anchored by robust provincial reimbursement policies and growing demand for accessible care. Provincial governments have established comprehensive billing and reimbursement frameworks, incentivizing healthcare providers to expand telemedicine offerings. Telemedicine is now integral to primary care delivery across Canada, especially in remote and Indigenous communities where traditional healthcare access is often limited. The sector’s evolution is further marked by the seamless integration of telemedicine platforms with electronic health records (EHR), enabling providers to maintain holistic, up-to-date patient care records.

Mental health services have emerged as a critical application for telemedicine in Canada, with provinces expanding access to online therapy and counseling to address rising mental health needs. The Canadian telemedicine market stands out for its focus on equity, technology integration, and support for holistic care delivery ensuring that virtual health services are sustainable, accessible, and aligned with broader healthcare goals.

Australia: Telemedicine Market Thrives on Government Investment and Rural Access Initiatives

Australia continues to be a global leader in telemedicine, propelled by strong government investment and a commitment to healthcare access for remote and rural populations. National digital health initiatives, as coordinated by the Australian Digital Health Agency (ADHA), focus on strengthening telehealth capabilities, particularly for populations outside metropolitan centers. Virtual consultations via video and phone have become a standard aspect of primary and specialist care delivery, improving reach and reducing patient travel burdens.

Remote patient monitoring is increasingly being adopted, allowing providers to track chronic conditions from a distance and reduce hospital admissions. These advancements, coupled with ongoing government funding, have ensured that Australia’s telemedicine market remains responsive to patient needs and equipped for future healthcare challenges setting a benchmark for quality, accessibility, and technology-enabled care in the Asia-Pacific region.

Brazil: Telemedicine Market Expands with Regulatory Support and Private Sector Innovation

Brazil’s telemedicine market is rapidly evolving, underpinned by proactive regulatory updates and rising private sector investment. ANVISA and the Federal Council of Medicine continue to refine the legal framework for telemedicine, ensuring patient safety and efficacy while fostering broader adoption of virtual care. The private healthcare sector has invested heavily in telemedicine platforms, especially in urban centers where demand for convenient, on-demand care is rising.

Brazil is also investing in the professional development of its healthcare workforce through tele-education initiatives, training clinicians in best practices for virtual care delivery. Mental health teleconsultations represent a fast-growing segment, with public and private providers expanding access to psychological support via virtual platforms. These trends, supported by a favorable regulatory environment and innovative care models, position Brazil as a leading telemedicine market in Latin America one that is expanding access, improving outcomes, and supporting the digital transformation of healthcare.

Telemedicine Market Report Scope

Telemedicine Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$168.4 Billion

|

|

Market Size (2034)

|

$764.2 Billion

|

|

Market Growth Rate

|

18.3%

|

|

Segments

|

By Type (Tele-hospitals, Tele-homes, mHealth (Mobile Health)), By Component (Products, Services), By Mode of Delivery (On-premise Delivery, Cloud-based Delivery, Web-based Delivery), By Deployment Model (Real-time (Synchronous), Store-and-Forward (Asynchronous), Remote Patient Monitoring), By Application (Primary Care, Specialty Care), By End User (Providers, Payers, Patients, Employer Groups & Government Agencies, Pharmaceutical & Biotechnology Companies, Medtech Companies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Teladoc Health, Inc., Amwell (formerly American Well), Koninklijke Philips N.V. (Philips Healthcare), Doximity, Inc., MDLIVE, Inc. (now part of The Cigna Group), Doctor On Demand (now part of Included Health, Inc.), Practo Technologies, GlobalMed Holdings, LLC, MeMD (Fabric Labs, Inc.), Talkspace, GoodRx, Hims & Hers Health, Cisco Systems Inc., GE HealthCare, Medtronic, Epic Systems Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Telemedicine Market Segmentation

By Type

- Tele-hospitals

- Tele-homes

- mHealth (Mobile Health)

By Component

- Products

- Services

- Tele-consulting

- Tele-monitoring

- Tele-education

- Telepathology

- Telecardiology

- Teleradiology

- Teledermatology

- Other Services

By Mode of Delivery

- On-premise Delivery

- Cloud-based Delivery

- Web-based Delivery

By Deployment Model

- Real-time (Synchronous)

- Store-and-Forward (Asynchronous)

- Remote Patient Monitoring

By Application

- Primary Care

- Specialty Care

By End User

- Providers

- Payers

- Patients

- Employer Groups & Government Agencies

- Pharmaceutical & Biotechnology Companies

- Medtech Companies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Telemedicine Market

- Teladoc Health, Inc.

- Amwell (formerly American Well)

- Koninklijke Philips N.V. (Philips Healthcare)

- Doximity, Inc.

- MDLIVE, Inc. (now part of The Cigna Group)

- Doctor On Demand (now part of Included Health, Inc.)

- Practo Technologies

- GlobalMed Holdings, LLC

- MeMD (Fabric Labs, Inc.)

- Talkspace

- GoodRx

- Hims & Hers Health

- Cisco Systems Inc.

- GE HealthCare

- Medtronic

- Epic Systems Corporation

* List Not Exhaustive

Research Coverage

This USDAnalytics report delivers a comprehensive analysis of the global telemedicine market, featuring historical data from 2021 to 2024 and forecasts from 2025 to 2034. The study provides in-depth market sizing, CAGR, and value projections, placing recent developments such as robotic telesurgery breakthroughs, AI-driven diagnostics, and digital health platform integrations into a broader strategic context.

The report systematically examines:

- Type: Tele-hospitals, tele-homes, mHealth (Mobile Health)

- Component: Products (hardware, software), Services (tele-consulting, tele-monitoring, tele-education, telepathology, telecardiology, teleradiology, teledermatology, other services)

- Mode of Delivery: On-premise delivery, cloud-based delivery, web-based delivery

- Deployment Model: Real-time (synchronous), store-and-forward (asynchronous), remote patient monitoring

- Application: Primary care, specialty care

- End User: Providers, payers, patients, employer groups & government agencies, pharmaceutical & biotechnology companies, medtech companies

Geographical coverage extends across North America, Europe, Asia Pacific, South America, and the Middle East & Africa, with detailed analysis of major markets such as the United States, Germany, United Kingdom, France, India, Canada, Australia, and Brazil. The report captures policy shifts, regulatory milestones, and ecosystem integrations driving adoption in each region.

Competitive landscape analysis profiles industry leaders including Teladoc Health, Amwell, Philips Healthcare, Doximity, MDLIVE, Practo Technologies, and others focusing on their product innovation, AI integration, strategic partnerships, and platform expansion.

The USDAnalytics report is designed to empower healthcare providers, technology developers, investors, and policy makers with actionable insights into global telemedicine trends, challenges, and growth opportunities, leveraging both retrospective and forward-looking intelligence to inform strategic decision-making.

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.