Terephthalic Acid Market 2025–2034: $115.7 Billion to $193.8 Billion at 5.9% CAGR Amid Capacity Surge, Vertical Integration, and Strategic Commodity Exits

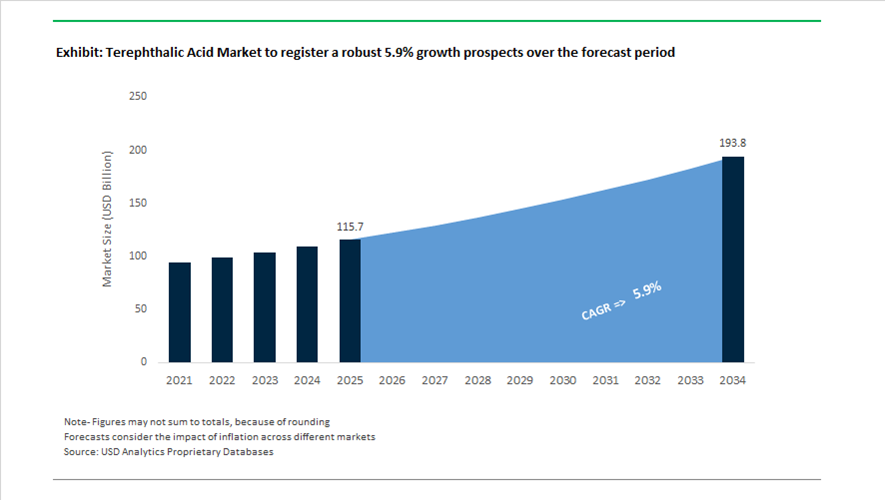

The global terephthalic acid (PTA) market is valued at $115.7 billion in 2025 and is projected to reach $193.8 billion by 2034, expanding at a CAGR of 5.9%. PTA remains the foundational feedstock for polyester fibers, PET resins, and film applications, directly linked to global textile demand, packaging consumption, and beverage bottle production. However, the competitive structure of the market is undergoing rapid transformation. Asia—particularly China and India—is consolidating production dominance through world-scale, integrated complexes, while Western producers are exiting or de-emphasizing commodity PTA exposure in favor of specialty materials, battery minerals, and recycled polymers. The result is a widening divergence between high-efficiency integrated producers and legacy standalone PTA operators facing margin compression.

Capacity expansion in China continues to reshape global supply-demand balances. In April 2024, Sinopec commissioned a 3 million tons per annum (mtpa) PTA facility in Yizheng, incorporating smart manufacturing systems that reportedly reduce energy consumption by approximately 20% versus older generation plants. In 2025, Guangxi Tongkun Petrochemical is scheduled to start a world-scale PTA unit in Qinzhou, part of a broader pipeline expected to add more than 22 million tons of global PTA capacity by 2028. Fujian Fuhaichuang Petrochemical is also preparing to commence operations at its expanded Zhangzhou PTA complex in late 2025, reinforcing China’s position as the epicenter of global polyester feedstock production. These expansions are increasingly integrated with paraxylene and refining assets, allowing producers to optimize feedstock security and cost structures in a market characterized by periodic oversupply cycles.

India and Pakistan are emerging as strategic regional pivots. In January 2025, the Adani Group and Indorama Ventures formed Valor Petrochemicals Ltd. to build a world-scale PTA facility in Maharashtra, marking Adani’s formal entry into the petrochemical value chain. In November 2025, PTA Global Holding Limited completed the acquisition of a 78.74% stake in Lotte Chemical Pakistan Limited, finalizing Lotte Chemical Corporation’s exit from the Pakistani PTA business as it pivots toward high-performance materials. In February 2026, Reliance Industries Limited began implementation of a 2.3 mtpa PTA plant in Dahej, integrated with paraxylene from Jamnagar, reinforcing vertical integration as a competitive necessity. Meanwhile, Western producers are streamlining portfolios: Albemarle is divesting Ketjen to refocus on lithium; Mitsubishi Chemical has launched a workforce transition program tied to its exit from low-margin petrochemicals; and Alpek is pivoting toward specialty PET and recycled rPET solutions. Trade policy is also influencing flows—December 2025 U.S. tariff measures led to a 64% year-on-year drop in PTA imports, accelerating localized sourcing and inventory management strategies.

Structural Cost Rebalancing and Specialty Demand Inflection in the Terephthalic Acid (PTA) Market

Commercial Scaling of Bio-PTA Through Multi-Brand Offtake Structures

The PTA market has entered a decisive commercialization phase for bio-based terephthalic acid, moving beyond demonstration plants into contracted, revenue-visible production. This shift is being pulled by consumer goods and apparel brands that have locked 2030 sustainability targets into procurement contracts, forcing polymer suppliers to secure chemically identical, drop-in PTA alternatives with verified renewable content. Unlike earlier bio-aromatic pilots that struggled with cost parity, current bio-PTA platforms are being designed around scale, feedstock flexibility, and long-term offtake certainty.

A critical inflection occurred in 2024–2025 when Origin Materials transitioned its Origin 1 facility in Ontario from pilot validation to commercial operation. By converting non-food wood residues into chloromethyl furfural (CMF) intermediates, the platform enables the production of fully bio-based para-xylene and downstream PTA without requiring changes to existing polyester polymerization infrastructure. This capability directly supports virgin plastic reduction mandates from global brand owners targeting 30%–33% reductions by 2030, transforming bio-PTA from a sustainability premium into a strategic compliance input.

Supply chain credibility is further reinforced through cross-border partnerships. In early 2024, Idemitsu Kosan, OPTC, and Marubeni formalized a bio-PTA collaboration structured around traceability, mass-balance certification, and apparel-grade polymer requirements. These agreements are not speculative; they are aligned with confirmed downstream demand from performance textile brands integrating bio-polyesters into premium apparel lines, effectively anchoring bio-PTA volumes within long-term procurement frameworks rather than spot sustainability programs.

Crude-to-Chemicals Integration Resets Global PTA Cost Curves

In parallel with renewable scaling, the conventional PTA market is undergoing a fundamental cost-structure realignment driven by crude-to-chemicals integration. Instead of treating PTA as a downstream derivative of refining, energy majors are redesigning complexes to maximize direct chemical yield from crude oil, structurally lowering the cost of para-xylene and insulating PTA margins from traditional fuel demand volatility.

The most consequential example is the Aramco–SABIC Crude-to-Chemicals complex in Saudi Arabia, scheduled for full operational readiness by 2025. Processing approximately 400,000 barrels per day, the facility is engineered to divert a disproportionate share of crude directly into chemical streams, generating an estimated 9 million tons of chemical output annually. For PTA producers, this integration translates into sustained feedstock advantage, particularly for export-oriented supply into Asian polyester hubs where cost leadership determines operating rates.

China is reinforcing this structural shift at scale. In April 2024, Sinopec Yizheng Chemical Fiber announced a multi-billion-yuan investment in a new world-scale PTA plant in Jiangsu Province. This project is emblematic of a broader capacity surge that pushed China’s total PTA capacity to roughly 86 million tons by the end of 2024, with high-single-digit growth expected through 2025. While this expansion intensifies competitive pressure, it also consolidates PTA production into highly integrated, energy-efficient assets, accelerating the exit of sub-scale, cost-exposed producers.

Specialty PTA Grades for Engineering Polyesters and Additive Manufacturing

A structurally attractive opportunity is emerging in specialty PTA grades designed for engineering-grade polyesters such as polycyclohexylenedimethylene terephthalate (PCT). Unlike bottle-grade PTA, these applications demand tighter impurity control, higher molecular consistency, and enhanced thermal stability to support elevated processing temperatures and mechanical loads.

The growth of high-temperature 3D printing is a key demand catalyst. Industry surveys from 2025 indicate that the high-performance additive manufacturing materials market is on track to more than double by 2030, driven by functional prototyping and short-run production in automotive, aerospace, and medical devices. PCT-based filaments and resins, derived from specialty PTA, enable components that retain dimensional stability under heat stress, making PTA suppliers integral to the value chain rather than interchangeable feedstock providers.

Automotive lightweighting further amplifies this opportunity. As OEMs accelerate the substitution of metal components with recycled and bio-based technical plastics, PTA-derived engineering polyesters are being specified for under-the-hood and structural applications. These materials deliver up to 50% weight reduction while meeting mechanical and thermal performance requirements, positioning specialty PTA as a growth lever aligned with electrification and emissions reduction strategies.

Ultra-High-Purity PTA for 5G and 6G Liquid Crystal Polymer Ecosystems

The most technically demanding opportunity for PTA producers lies in ultra-high-purity grades used in Liquid Crystal Polymers for advanced electronics. The deployment of millimeter-wave 5G and early 6G architectures has elevated signal integrity to a critical constraint, making dielectric loss and ionic contamination decisive material selection criteria.

LCPs rely on PTA as a foundational monomer, but electronic-grade applications require near-zero metal ion contamination to preserve stable dielectric constants and ultra-low loss tangents at frequencies exceeding 100 GHz. By late 2025, leading polymer producers were introducing high-flow and soluble LCP grades for ultra-thin antenna modules, effectively transferring purity risk upstream to PTA suppliers.

Strategic capacity expansion underscores the scale of this opportunity. In December 2024, Toray Industries expanded its LCP manufacturing footprint in Malaysia to serve miniaturized electronics and high-frequency communication devices. This move signals sustained demand growth for electronic-grade PTA, where qualification cycles are long, switching costs are high, and margins materially exceed commodity polyester applications.

Terephthalic Acid Market Share and Segmentation Insights

Purified Terephthalic Acid Leads Market with High-Purity Polymer Production Requirements

Purified terephthalic acid accounted for 72.80% of the terephthalic acid market in 2025, reflecting its essential role in producing polyester fibers, PET resins, and polyester films. PTA offers the high purity required for consistent polymerization, product quality, and large-scale manufacturing efficiency across textile and packaging industries. Its integration into global polyester value chains supports sustained demand. The 2025 market trend emphasizes integrated PTA-PET production complexes, where manufacturers co-locate PTA and downstream polymer facilities to reduce logistics costs, improve operational efficiency, and ensure consistent feedstock supply for high-volume polyester production.

Polyester Fiber Segment Dominates Demand with Global Textile Industry Scale

Polyester fiber accounted for 42.80% of terephthalic acid market demand in 2025, driven by its position as the most widely used synthetic fiber globally, representing over half of total fiber production. PTA is a key raw material in polyethylene terephthalate (PET) used for apparel, home textiles, and industrial fabrics. The scale and growth of the global textile industry sustain high-volume PTA consumption. The 2025 trend highlights the rise of recycled polyester, where increasing use of recycled PET (rPET) and advancements in chemical recycling technologies are reshaping demand dynamics, enabling circular production models while maintaining fiber performance and quality standards.

Terephthalic Acid Market Competitive Landscape

The terephthalic acid (PTA) market in 2026 is shaped by Asia’s ~75% capacity dominance, deep PX-to-PET vertical integration, and accelerating transition toward low-carbon PTA production. Energy-efficient crystallization, wastewater management, and circular PET integration are critical differentiators for securing global FMCG supply contracts.

Reliance Industries Strengthens Crude-to-Chemicals Integration with rPET-Linked PTA Expansion

Reliance Industries Limited (RIL) continues to dominate the PTA market through its fully integrated crude-to-chemicals value chain anchored by the Jamnagar refinery complex. Strategic PTA price adjustments in March 2026 reflect alignment with volatile paraxylene feedstock trends and import competition. Capacity expansion initiatives are reinforcing India’s textile manufacturing ecosystem while reducing reliance on imports. RIL’s integration ensures uninterrupted PX supply, delivering operational resilience and cost efficiency. The company is advancing circular polyester solutions by integrating recycled PET (rPET) into PTA production streams. Focus on hybrid polyester materials positions RIL as a key supplier for sustainable apparel value chains.

Indorama Ventures Optimizes Global PTA Footprint with Decarbonization and Asset Rationalization Strategy

Indorama Ventures (IVL) is strengthening its global PTA leadership under the IVL 2.0 strategy, emphasizing operational efficiency and sustainability. The shutdown of a high-cost Thailand facility in March 2026 reflects consolidation toward large-scale, energy-efficient plants. A $200 million IFC-backed loan is accelerating decarbonization across PTA and PET operations. IVL is aligning with EU CSRD requirements, targeting reduced GHG intensity across European assets. Its global manufacturing footprint ensures stable PTA supply for packaging, fibers, and medical applications. Strategic focus remains on eco-efficient PTA production and long-term financial resilience.

Sinopec Expands Global Dominance with 3 Million Ton PTA Mega-Plant and High Localization Efficiency

Sinopec leads global PTA production with the commissioning of a 3 million ton per year mega-facility at Yizheng in 2025. The project achieved 97.5% equipment localization, showcasing China’s technological independence in large-scale PTA manufacturing. With over Yuan 5 billion invested, Sinopec is reinforcing the polyester value chain, particularly for PSF applications. China’s ~55% share of global PTA demand underpins Sinopec’s market influence. Advanced automation and intelligent production systems enhance efficiency and output reliability. The company remains central to Asia-Pacific’s dominance in PTA supply and downstream polyester markets.

INEOS Aromatics Drives European PTA Competitiveness Through Asset Modernization and Carbon Reduction Initiatives

INEOS Aromatics is focusing on modernization and rationalization to sustain competitiveness in Western PTA markets. Investments at the Lavera site in France are enhancing operational efficiency and long-term asset viability. Proposed mothballing of the Geel PTA unit reflects strategic consolidation toward lower-carbon, high-efficiency production lines. INEOS is advancing CO2 storage projects and green hydrogen feasibility studies to reduce emissions by over 100,000 tonnes annually. The company also maintains leadership in PTA and PX process technology licensing globally. Emphasis on low-carbon PTA aligns with stringent European sustainability regulations.

Alpek Strengthens PTA-PET Integration with Recycling Expansion and Corporate Consolidation Strategy

Alpek is enhancing its PTA market position through corporate consolidation and circular PET integration. The 2025 merger streamlined operations, improving financial agility and capital allocation efficiency. The company targets strong free cash flow generation in 2026 amid PET margin pressures of around $270 per ton. Expansion toward 300,000 metric tons of PET recycling capacity enables direct integration of recycled feedstock into PTA production. Leadership restructuring, including the appointment of a new CFO, supports strategic execution across the Americas. Alpek’s integrated PTA-PET model reinforces its competitiveness in sustainable packaging markets.

Mitsubishi Chemical Accelerates Transition to Bio-Based PTA Through Green Chemicals Strategy and Strategic Alliances

Mitsubishi Chemical Group Corporation (MCGC) is pivoting toward bio-based terephthalic acid under its Green Chemicals transformation strategy. The establishment of a dedicated business unit in March 2026 accelerates commercialization of renewable PTA intermediates. Strategic alliances with Asahi Kasei and Mitsui Chemicals support decarbonization of aromatic production in Japan. Divestment from carbon-intensive businesses reflects capital reallocation toward high-value sustainable materials. Recognition in the CDP Climate Change A List underscores its ESG leadership. Focus remains on low-carbon PTA and specialty materials for advanced applications in EVs and electronics.

China Terephthalic Acid Market Defined by Mega-Scale Integration and Green Manufacturing Mandates

China’s terephthalic acid market continues to be shaped by unprecedented single-unit scale, regional integration, and mandated efficiency upgrades. In mid-2025, Sinopec achieved full-scale operations at its Yizheng Chemical Fiber complex, commissioning the world’s largest single PTA unit with 3 million tonnes per annum capacity. The plant deploys short-process and smart-manufacturing technologies that reduce energy intensity by an estimated 15%, reinforcing China’s cost leadership in paraxylene-to-PTA conversion. This commissioning marks a structural shift toward fewer, larger, and more energy-efficient PTA assets.

Regional integration has accelerated in parallel. In August 2025, the Jiangxi Jiujiang petrochemical cluster finalized contracts for a 33.2 billion yuan integrated project combining 3 million tons of PTA with 3.76 million tons of PET, establishing central China’s first refining-to-polyester industrial chain. Southern capacity followed suit, as the Guangxi Tongkun Petrochemical project in Qinzhou brought its first 3 mtpa PTA line online in late 2025, with a second identical unit planned to serve Southeast Asian export corridors. Collectively, these investments support China’s trajectory toward projected cumulative new PTA capacity of 17.2 mtpa by 2030, materially reducing import dependence on South Korea and Taiwan. Regulatory overlays further shape asset design. Under the MIIT 2025 roadmap, new PTA plants must integrate wastewater heat recovery and low-temperature oxidation systems to comply with “Green Intelligent Petroleum Refining” standards, embedding decarbonization directly into capacity expansion.

India Terephthalic Acid Market Accelerated by Import Substitution and Polyester Backward Integration

India’s terephthalic acid market is transitioning from import reliance to integrated domestic production, anchored by large-scale investments and policy support. In 2025, Reliance Industries Limited accelerated its ₹75,000 crore Oil-to-Chemicals expansion, advancing a flagship 3 million tonne PTA facility at Dahej. The project, targeted for phased completion by late 2026, represents a strategic move to secure feedstock for India’s fast-growing polyester and packaging industries.

Vertical integration is central to this strategy. Reliance’s PTA assets are being co-located with paraxylene production at Jamnagar and downstream 1 MMTPA PET units at Dahej, creating a tightly coupled PX–PTA–PET chain that reduces exposure to global price volatility. On the policy front, India’s Make in India initiative introduced stricter Quality Control Orders on PTA imports in 2025, effectively raising compliance thresholds and incentivizing domestic sourcing for textile manufacturers. Sustainability considerations are increasingly embedded in new capacity planning. Chemical parks in Gujarat began piloting circular polyester recycling units in 2025 that depolymerize post-consumer PET back into PTA and MEG, aligning the terephthalic acid value chain with India’s long-term 2070 net-zero commitment.

United States Terephthalic Acid Market Characterized by Price Premiums and Low-Carbon Differentiation

The U.S. terephthalic acid market remains structurally smaller than Asia but commands a premium position driven by logistics, quality requirements, and ESG differentiation. In September 2025, domestic PTA prices reached approximately $960 per metric ton, reflecting higher logistics costs and resilient demand from food-grade and specialty packaging applications. This pricing environment supports continued operation of U.S. Gulf Coast assets despite global oversupply pressures.

Process innovation has emerged as a key competitive lever. Following its acquisition of BP’s petrochemical assets, INEOS Aromatics launched the PTAir technology suite in 2025. The platform employs high-activity catalysts operating at lower temperatures, reducing the carbon footprint of PTA production while maintaining product purity. Trade policy remains a swing factor. In late 2025, U.S. authorities initiated reviews of anti-dumping duties on PTA imports to shield domestic producers from the influx of low-cost Asian capacity. Concurrently, several Houston Ship Channel PTA units began installing carbon capture and sequestration pilots, positioning “Blue PTA” as a differentiated product for beverage bottlers and brand owners with stringent ESG targets.

Russia Terephthalic Acid Market Focused on Catalyst Sovereignty and Feedstock Security

Russia’s terephthalic acid market strategy in 2025 centered on reducing technological dependence and securing the upstream catalyst supply chain. In July 2025, SIBUR commenced construction of the country’s largest catalyst production facility, aimed at producing indigenous chromium-based and metallocene catalysts for PTA and polyester processes. This move addresses vulnerabilities created by restricted access to Western technologies.

Downstream integration is reinforced by the Amur Gas Chemical Complex. By August 2025, the project reached 82% completion, positioning it as a major feedstock and polymer hub for Northern Asia. Once fully operational by late 2026, the Amur GCC is expected to influence regional PTA and PET balances by anchoring Russia’s participation in the Asian polyester value chain.

Mexico Terephthalic Acid Market Anchored in Geographic Advantage and Regional Supply Stability

Mexico’s terephthalic acid market plays a stabilizing role within the Americas, leveraging proximity to North American demand centers. In its 2025 guidance, Alpek S.A.B. de C.V. emphasized geographic optimization, maintaining stable polyester production of 3.7 million tons despite margin pressures. Alpek’s strategy prioritizes operational continuity and regional supply reliability over aggressive capacity expansion, reinforcing Mexico’s position as a key PTA and PET supplier to the U.S. and Latin American markets.

Comparative Summary: Terephthalic Acid Market by Country

Terephthalic Acid Market County Level Snapshot

|

Country

|

Strategic Priority

|

Structural Driver

|

Competitive Implication

|

|

China

|

Mega-scale PTA and PX–PET integration

|

Smart manufacturing and green mandates

|

Lowest-cost global supply base

|

|

India

|

Import substitution and backward integration

|

Policy support and polyester demand

|

Rapid domestic capacity build-up

|

|

United States

|

Low-carbon differentiation

|

ESG-driven packaging demand

|

Price premiums and CCS adoption

|

|

Russia

|

Catalyst self-sufficiency

|

Feedstock security and localization

|

Reduced technology dependence

|

|

Mexico

|

Regional supply optimization

|

Geographic proximity to end users

|

Stable Americas-focused production

|

Terephthalic Acid Market Report Scope

Terephthalic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$115.7 Billion

|

|

Market Size (2034)

|

$193.8 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Grade (Purified Terephthalic Acid, Medium Quality Terephthalic Acid, Qualified Terephthalic Acid), By Application (Polyester Fiber, PET Resin, Polyester Films, Industrial Resins, Specialty Chemicals), By End-Use Industry (Textile and Apparel, Food and Beverage Packaging, Automotive and Transportation, Electrical and Electronics, Construction and Paints)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sinopec Group, Reliance Industries Limited, INEOS Aromatics, Indorama Ventures Public Company Limited, Alpek S.A.B. de C.V., Hengli Petrochemical Co., Ltd., Zhejiang Rongsheng Holding Group, Sibur Holding, Lotte Chemical Corporation, Mitsubishi Chemical Group, Hanwha Impact, Formosa Plastics Group, Mitsubishi Gas Chemical Company, JBF Industries Ltd., BP p.l.c.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Terephthalic Acid Market Segmentation

By Grade

- Purified Terephthalic Acid

- Medium Quality Terephthalic Acid

- Qualified Terephthalic Acid

By Application

- Polyester Fiber

- PET Resin

- Polyester Films

- Industrial Resins

- Specialty Chemicals

By End-Use Industry

- Textile and Apparel

- Food and Beverage Packaging

- Automotive and Transportation

- Electrical and Electronics

- Construction and Paints

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Terephthalic Acid Market

- Sinopec Group

- Reliance Industries Limited

- INEOS Aromatics

- Indorama Ventures Public Company Limited

- Alpek S.A.B. de C.V.

- Hengli Petrochemical Co., Ltd.

- Zhejiang Rongsheng Holding Group

- Sibur Holding

- Lotte Chemical Corporation

- Mitsubishi Chemical Group

- Hanwha Impact

- Formosa Plastics Group

- Mitsubishi Gas Chemical Company

- JBF Industries Ltd.

- BP p.l.c.

*- List not Exhaustive