Tetrahydrofuran Market 2025–2034: $9.6 Billion to $17.5 Billion at 6.9% CAGR Fueled by Bio-Based PTMEG, Textile Decarbonization, and BDO Integration

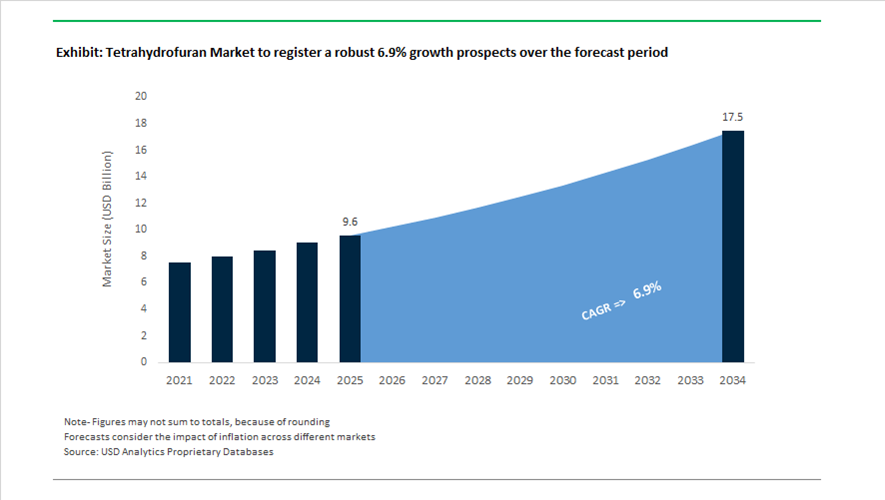

The global tetrahydrofuran (THF) market is valued at $9.6 billion in 2025 and is projected to reach $17.5 billion by 2034, expanding at a CAGR of 6.9%. THF is a critical intermediate in the production of polytetramethylene ether glycol (PTMEG), which accounts for the majority of spandex fiber composition, as well as in solvents for coatings, adhesives, pharmaceuticals, and electronics. Market growth is closely tied to the expansion of sustainable textiles, bio-based polymer platforms, and the integration of the 1,4-butanediol (BDO)–THF value chain. Increasing regulatory scrutiny around VOC emissions and carbon intensity is accelerating the commercialization of biomass-balanced and renewable THF pathways, particularly in Europe and Asia.

Sustainability-driven innovation intensified in 2024. In May 2024, BASF SE expanded its biomass-balanced (BMB) portfolio to include THF, partnering with Asahi Kasei Corporation to supply BMB THF for ROICA™ premium stretch fibers. The drop-in solution reduces product carbon footprint by approximately 25% through renewable feedstock substitution. In January 2024, The LYCRA Company initiated large-scale commercial production of bio-based spandex, significantly increasing demand for renewable PTMEG and upstream THF. In February 2024, Ashland Global Holdings partnered with Bio-on to explore renewable THF production routes derived from bio-butanol. Simultaneously, Dow Inc. collaborated with a technology startup to develop solvent recycling systems capable of recovering and purifying THF from industrial polymer and pharmaceutical waste streams, reinforcing circular solvent management trends.

Capacity expansion and feedstock security remain central competitive factors. In 2024, Hunan Yuxin Energy operationalized a 120,000-ton-per-year BDO plant, strengthening regional THF/PTMEG supply in China. In April 2024, Hyosung announced a $1 billion investment in a Vietnamese bio-textile complex focused on sustainable spandex and associated THF intermediates. In late 2025, Sinopec advanced its Kuqa green hydrogen project, enabling lower-carbon intermediates within the BDO–THF chain while outlining its 2026–2030 strategy to expand high-end THF derivatives for electronics and semiconductor applications. In February 2026, BASF reinforced European supply security by upgrading its Ludwigshafen BDO and THF units to stabilize output amid global volatility. Meanwhile, November 2025 regulatory audits across North America targeting VOC emissions prompted producers to introduce high-purity, low-emission THF grades for coatings and adhesive systems.

Structural Shifts and Value-Creation Pathways in the Tetrahydrofuran (THF) Market

Upstream Vertical Integration of Spandex Producers into THF–PTMEG Value Chains

The tetrahydrofuran market is increasingly being shaped upstream by spandex and elastane manufacturers that are internalizing THF and PTMEG production to protect margins and stabilize feedstock exposure. This shift is not incremental but structural. As global spandex capacity expands at double-digit rates, fiber producers are no longer willing to remain exposed to merchant THF price volatility or purity variability, both of which directly affect PTMEG molecular weight distribution and, ultimately, yarn elasticity and fatigue resistance.

By late 2025, China’s spandex sector reported a planned capacity growth rate of 13.1%, driven by aggressive commissioning cycles in the second half of the year. Integrated chemical majors such as Huafon Chemical added approximately 75,000 tons of new spandex capacity in 2025, supported by in-house THF and PTMEG units. This integration allows tighter control over >99.95% purity THF, a threshold increasingly specified by premium activewear brands to ensure consistent stretch recovery and low hysteresis losses.

A similar strategy is visible in global brand-aligned production hubs. The LYCRA Company commissioned a 30,000-ton project in Yinchuan in 2025, positioning the site as a global PTMEG-spandex anchor. Such investments signal a decisive move away from spot-market THF sourcing toward captive supply, effectively reducing addressable merchant volumes while increasing demand for high-spec, contract-based THF production. For the broader THF market, this trend tightens supply flexibility and raises the strategic value of backward integration into BDO and downstream PTMEG.

Escalating Demand for Ultra-High-Purity THF in CDMO-Led Pharmaceutical Synthesis

Beyond fibers, pharmaceutical manufacturing has emerged as a structurally different growth vector for THF, defined by extreme purity requirements, regulatory scrutiny, and supply-chain resilience. Contract Development and Manufacturing Organizations are specifying ultra-high-purity THF for complex organometallic and peptide synthesis, particularly for next-generation therapeutics such as GLP-1 receptor agonists. In these applications, trace peroxide levels, moisture content, and metal ion contamination directly impact reaction yield and regulatory compliance.

In December 2025, global pharmaceutical player Lupin entered a major licensing and supply agreement for Bofanglutide, a novel GLP-1 agonist. The multi-step synthesis routes for such molecules rely heavily on THF as a solvent for Grignard and controlled lithiation reactions, elevating THF from a commodity solvent to a cGMP-qualified critical raw material.

Supply security has become equally important. Following volatility in the 1,4-butanediol precursor market, CDMOs are prioritizing long-term solvent contracts with validated suppliers. This is evident in the strategic expansion of Samsung Biologics, which strengthened its U.S. footprint in late 2025 through a $280 million Rockville acquisition. Such expansions are accompanied by solvent qualification programs that favor suppliers capable of delivering consistent UHP THF at scale, reshaping demand away from volume-driven chemical distribution toward compliance-driven specialty supply.

THF as a Lower-Energy Co-Solvent in Lithium-Ion Battery Electrode Manufacturing

A significant opportunity is emerging for THF in battery materials processing as global regulators tighten restrictions on N-methyl-2-pyrrolidone. With NMP classified as a reproductive toxin and limited to sub-0.3% usage under EU REACH and U.S. EPA frameworks, battery manufacturers are actively qualifying alternative solvent systems. THF is gaining attention as a co-solvent due to its low boiling point, strong solvency for polymer binders, and favorable evaporation kinetics.

Validated technical studies from 2024–2025 demonstrate that blending or partially substituting NMP with THF or similar low-boiling solvents can reduce electrode drying energy consumption by up to four times. This is economically material for gigafactories, where solvent drying and recovery can account for roughly 40% of total process energy consumption. As EV manufacturers push for lower cost-per-kWh and reduced Scope 1 emissions, solvent system optimization is becoming a board-level efficiency lever.

THF’s role is particularly relevant for silicon-rich anode slurries, where dispersion stability is critical. Silicon expansion during cycling places severe demands on binder-solvent interactions, and THF’s solvency profile enables more uniform slurry rheology. As battery producers accelerate the transition toward high-silicon and next-generation cathode chemistries, THF is shifting from a laboratory solvent into a strategic processing input.

Commercialization of Bio-Based THF via the Furfural Route

The second major opportunity lies in the rapid commercialization of bio-based THF derived from agricultural waste streams. Sustainability mandates from textile and automotive brands are pushing beyond recycled content toward renewable chemical inputs, creating a premium market for Bio-THF as a drop-in alternative to fossil-derived material. Produced via the furfural route using sugarcane bagasse, corn cobs, or other lignocellulosic residues, Bio-THF directly supports low-carbon PTMEG and spandex production.

In March 2025, Hyosung TNC partnered with premium apparel brands such as Van Harvey to launch garments incorporating bio-based spandex. These products rely on bio-PTMEG synthesized from renewable THF, enabling measurable reductions in cradle-to-gate carbon intensity across the synthetic fiber value chain.

Industrial data from late 2025 confirms that THF has become the leading furfural derivative by volume, overtaking traditional solvent applications. Producers in China and India, already dominant in global furfural exports, are upgrading from raw biomass processing to integrated Bio-THF production. This transition aligns with the EU’s 2050 toxic-free environment objective and is positioning Bio-THF as a cornerstone molecule for green polymers in Europe and North America.

Tetrahydrofuran Market Share and Segmentation Insights

Production Technology Market Share: BDO Dehydration Leads with Integrated Cost Efficiency

The tetrahydrofuran (THF) market by production technology is strongly dominated by BDO dehydration, accounting for 58.60% market share in 2025, driven by its superior process efficiency and direct conversion economics. This route benefits from integrated BDO-THF production facilities, enabling manufacturers to optimize feedstock utilization and dynamically balance BDO and THF output based on pricing trends. Alternative technologies such as the maleic anhydride process, Reppe process, bio-based production, and butadiene process hold comparatively smaller shares due to higher capital intensity or feedstock constraints. The integrated BDO-THF value chain remains a critical competitive advantage, particularly for PTMEG production, reinforcing its leadership in industrial-scale THF manufacturing.

End-Use Industry Market Share: Textile and Apparel Segment Anchored by Spandex Demand

By end-use industry, textile and apparel dominates the THF market with a 48.60% share in 2025, supported by robust demand for PTMEG used in spandex fiber production. The widespread adoption of stretchable fabrics across activewear, denim, and intimate apparel continues to drive THF consumption at scale. Automotive, pharmaceuticals, electronics, and packaging and construction sectors contribute smaller shares, reflecting more specialized applications. A key market driver is the sustained growth of the athleisure trend, where demand for comfort-oriented and performance textiles remains elevated. Continuous innovation in elastane fiber blends and finishing technologies further strengthens THF demand across global textile manufacturing hubs.

Tetrahydrofuran Market Competitive Landscape

The tetrahydrofuran (THF) market in 2026 is defined by strategic portfolio rebalancing, with producers shifting toward bio-based feedstocks and electronic-grade purity. Investments in Southeast Asia and North America, combined with ESG-driven divestments, are accelerating demand for low-PCF THF across spandex, medical, and pharmaceutical applications.

BASF Advances Bio-Based THF Integration with Low-Carbon BDO and Verbund Efficiency

BASF remains the global benchmark in the THF market, leveraging its integrated C4 value chain and Verbund production model. The 2025 divestment of coal-based Korla assets aligns with its strategy to reduce exposure to high-carbon footprint products. In 2026, BASF is accelerating bio-based THF production via renewable BDO, targeting 40% to 60% CO2 reduction for PTMEG applications. Price adjustments across Europe reflect strong demand for elastic fibers and sustainable solvents. Its catalytic hydrogenation and dehydration processes ensure consistent high-purity THF supply for APIs and specialty polymers. Strong ESG alignment reinforces BASF’s leadership in low-PCF solvent innovation.

Dairen Chemical Strengthens Global THF Supply with PTMEG Integration and AI-Driven Quality Control

Dairen Chemical Corporation (DCC) is a dominant merchant supplier of THF, driven by large-scale integrated production in Taiwan and China. Its proprietary allyl alcohol hydroformylation process ensures high selectivity in BDO-to-THF conversion. Strong integration into PTMEG production supports the global spandex and athleisure markets. In 2026, DCC is implementing AI-based monitoring systems to enhance purity standards for pharmaceutical and electronic-grade applications. Its THF is widely recognized for low moisture content and superior solvency for PVC and specialty polymers. Continuous quality optimization strengthens its position in high-performance textile and industrial markets.

Mitsubishi Chemical Accelerates Green THF Transition with Bioengineering and Automotive Integration

Mitsubishi Chemical Group Corporation (MCGC) is transitioning toward green THF and specialty derivatives under its sustainability-driven portfolio transformation. Recognition in the CDP Climate Change A List in 2026 highlights its decarbonization progress. THF derivatives are being utilized in DURABIO bioengineering plastics for automotive and electronics applications, including EV interiors and AI-enabled devices. Strategic alliances with Asahi Kasei and Mitsui Chemicals are lowering feedstock carbon intensity. Divestment from carbon-heavy segments supports capital reallocation toward high-purity materials. The company is strengthening its presence in semiconductor-grade and advanced polymer markets.

LyondellBasell Enhances THF Production Efficiency with Feedstock Optimization and Safety-Driven Formulations

LyondellBasell (LYB) is optimizing THF production through feedstock integration and circularity initiatives. The company’s ethane utilization strategy improves cost efficiency across its BDO and THF value chains. Its THF products, stabilized with BHT, ensure safe storage and transport for industrial users. Investments in propylene expansion projects enhance upstream self-sufficiency and stabilize raw material supply. LYB’s THF is widely used in PVC welding and infrastructure-grade adhesives meeting NSF standards. Strong positioning in construction and piping sectors supports steady demand for industrial-grade THF solvents.

Sinopec Expands THF Market Dominance with Coal-to-Chemical Integration and Green Hydrogen Adoption

Sinopec, through Great Wall Energy Chemical, leads in large-scale THF production with integrated coal-to-chemical complexes. In 2026, the company is focusing on yield optimization and increasing petrochemical contributions to refining margins. Integration of green hydrogen projects, including a 30,000 t/y facility in Ordos, is reducing the carbon footprint of coal-derived THF. High utilization rates strengthen its dominance in the Asia-Pacific spandex supply chain. Significant capital expenditure in CCUS and petrochemical upgrades ensures regulatory compliance and long-term sustainability. Sinopec remains a key stabilizer of global THF pricing dynamics.

Ashland Targets High-Purity THF Demand with Specialty Solvent Positioning for Pharmaceuticals and Coatings

Ashland Inc. is focusing on high-margin specialty THF applications, particularly in pharmaceuticals and advanced coatings. Its acid-catalyzed BDO dehydration process is optimized for ultra-high purity solvent production. In 2026, rising drug manufacturing demand in North America and Europe is driving increased consumption of THF as a reaction medium. Ashland positions its THF as a premium solvent for API synthesis, emphasizing volatility and residue-free removal. The company is aligning its portfolio with low-VOC regulatory standards under the EU Green Deal. Strong focus on specialty additives supports growth in high-performance industrial and life sciences markets.

China Tetrahydrofuran Market Anchored in Mega-Scale Integration and Spandex-Led Demand

China continues to dominate the global tetrahydrofuran market through unmatched scale, deep feedstock integration, and downstream spandex pull. In early 2025, Sinopec achieved mechanical completion of the second-phase expansion at its Zhenhai Refinery, part of a 41.6 billion yuan investment. The project integrates advanced 1,4-butanediol units directly into high-capacity THF production lines, structurally supporting an annual downstream petrochemical value chain exceeding 8 million tons. This short-process integration materially lowers conversion losses and positions China as the lowest-cost THF producer globally.

Downstream consolidation further reinforces China’s strategic role. In November 2025, BASF SE announced the centralization of its Asian PolyTHF operations at Caojing, China, with the planned closure of its Ulsan, South Korea facility by 2026. The decision reflects China’s superior logistics, feedstock availability, and proximity to spandex clusters. Supporting this, Huaheng Energy Technology’s 46 kTA PTMEG plant in Inner Mongolia has addressed domestic elastane supply gaps, while MIIT-led smart manufacturing programs are delivering double-digit energy-efficiency gains. With Yangtze River Delta spandex clusters accounting for an estimated 78% of global PTMEG pull in 2025, China’s THF demand base remains structurally entrenched.

United States Tetrahydrofuran Market Driven by Pharma Purity and Bio-Based Transition

The United States tetrahydrofuran market is increasingly differentiated by high-purity applications and early adoption of renewable feedstocks. In 2025, BASF SE completed capacity debottlenecking at its Geismar, Louisiana facility, reinforcing its role as a primary supplier of pharmaceutical-grade THF and specialty adhesive solvents for the North American construction sector. The U.S. remains the world’s largest consumer of analytical-grade THF, driven by its indispensable role as a reaction medium in hormone synthesis and antiviral drug manufacturing.

A parallel structural shift is occurring toward bio-based THF precursors. A strategic collaboration between The LYCRA Company and Dairen Chemical Corporation reached commercial scale in 2025, enabling the mass production of PTMEG derived from QIRA® bio-based BDO. This marks the first large-scale renewable pathway for THF-derived polymers in the U.S. apparel market. Trade policy has reinforced domestic positioning, as 2025 tariffs reduced chemical imports from China by roughly 30%, encouraging reshoring and technology licensing. BASF’s November 2025 decision to offer PolyTHF 1800 technology licenses further supports decentralized, high-performance polymer manufacturing across North America.

India Tetrahydrofuran Market Accelerated by API Manufacturing and Import Substitution

India’s tetrahydrofuran market is expanding rapidly as part of a broader pharmaceutical and technical textiles manufacturing push. Under Make in India 2.0 and the National Manufacturing Mission, bulk drug parks have been prioritized, directly lifting THF demand as a solvent for API intermediates in the domestic generics industry. This structural demand is reinforced by the Ministry of Textiles’ ambition to scale India’s technical textiles market to $40–50 billion, prompting investments in THF-to-PTMEG conversion units to support localized spandex and elastane production.

Policy support has strengthened the cost position of domestic producers. The 2025 Union Budget introduced RoDTEP remission schemes that materially reduce the export and production burden for THF manufacturers, positioning India as a credible China+1 sourcing alternative. Environmental compliance is also shaping production economics. By early 2026, Zero Liquid Discharge mandates across Gujarat chemical clusters forced THF plants to deploy advanced wastewater heat recovery and solvent management systems, raising entry barriers while favoring organized, technology-driven producers.

Germany Tetrahydrofuran Market Focused on Specialty Grades and Green Hydrogen Integration

Germany’s tetrahydrofuran market is characterized by consolidation, energy-risk mitigation, and sustainability-driven differentiation. In 2025, BASF SE consolidated its European THF production at Ludwigshafen, leveraging the Verbund model to offset structurally high energy costs. The site now prioritizes specialty THF grades for automotive elastomers and medical devices, segments where performance consistency and regulatory compliance outweigh cost considerations.

Energy transition initiatives are reshaping production pathways. In 2025, green hydrogen supplied by RCT Hydrogen began feeding regional chemical parks, enabling pilot-scale production of low-carbon or “Green THF” for EU textile and medical customers with strict sustainability mandates. At the strategic level, German producers are also de-risking supply chains. Under the 2026 Germany–China trade outlook, firms are diversifying sourcing toward Southeast Asia while retaining technology leadership through licensing and process IP, ensuring resilience without sacrificing margin control.

Comparative Snapshot: Tetrahydrofuran Market by Country

Tetrahydrofuran Market County Level Snapshot

|

Country

|

Strategic Focus

|

Core Demand Driver

|

Market Implication

|

|

China

|

Mega-scale BDO–THF integration

|

Spandex and PTMEG

|

Global cost leadership and volume dominance

|

|

United States

|

High-purity and bio-based THF

|

Pharmaceuticals and apparel polymers

|

Premium positioning and reshoring gains

|

|

India

|

Import substitution and APIs

|

Generics and technical textiles

|

Rapid demand growth with policy tailwinds

|

|

Germany

|

Specialty grades and green hydrogen

|

Automotive and medical devices

|

Sustainability-led differentiation

|

Tetrahydrofuran Market Report Scope

Tetrahydrofuran Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.6 Billion

|

|

Market Size (2034)

|

$17.5 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Production Technology (Reppe Process, Maleic Anhydride Process, Butadiene Process, Bio-Based Production, BDO Dehydration), By Grade (Technical Grade, Analytical Grade, Electronic Grade), By Application (PTMEG Production, Solvents, Chemical Intermediates, Pharmaceutical Intermediates, Reaction Medium), By End-Use Industry (Textile and Apparel, Automotive, Pharmaceuticals, Packaging and Construction, Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Sinopec Group, Dairen Chemical Corporation, LyondellBasell Industries N.V., INVISTA, Mitsubishi Chemical Group, Ashland Global Holdings Inc., Hengli Petrochemical Co., Ltd., Xinjiang Tianye Co., Ltd., Sipchem, Nan Ya Plastics Corporation, Shanxi Sanwei Group Co., Ltd., Markor Chemical Manufacturing, Gantrade Corporation, Balaji Amines Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Tetrahydrofuran Market Segmentation

By Production Technology

- Reppe Process

- Maleic Anhydride Process

- Butadiene Process

- Bio-Based Production

- BDO Dehydration

By Grade

- Technical Grade

- Analytical Grade

- Electronic Grade

By Application

- PTMEG Production

- Solvents

- Chemical Intermediates

- Pharmaceutical Intermediates

- Reaction Medium

By End-Use Industry

- Textile and Apparel

- Automotive

- Pharmaceuticals

- Packaging and Construction

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Tetrahydrofuran Industry

- BASF SE

- Sinopec Group

- Dairen Chemical Corporation

- LyondellBasell Industries N.V.

- INVISTA

- Mitsubishi Chemical Group

- Ashland Global Holdings Inc.

- Hengli Petrochemical Co., Ltd.

- Xinjiang Tianye Co., Ltd.

- Sipchem

- Nan Ya Plastics Corporation

- Shanxi Sanwei Group Co., Ltd.

- Markor Chemical Manufacturing

- Gantrade Corporation

- Balaji Amines Ltd.

*- List not Exhaustive