Titanates Market Overview 2025–2034: $2.2 Billion to $3.6 Billion at 5.7% CAGR Fueled by LTO Batteries, MLCC Expansion, and Silicon Photonics Breakthroughs

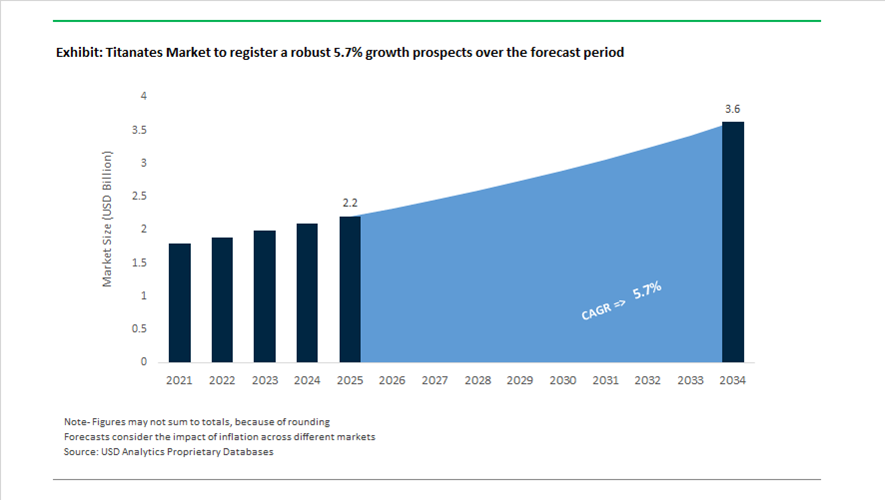

The global Titanates market is valued at $2.2 billion in 2025 and is projected to reach $3.6 billion by 2034, expanding at a CAGR of 5.7%. Titanates, including barium titanate, lithium titanate (Li₄Ti₅O₁₂ or LTO), and specialty organo-titanates, are critical functional materials in multilayer ceramic capacitors (MLCCs), lithium titanate oxide batteries, electronic ceramics, catalysts, and advanced photonic systems. Market growth is increasingly driven by semiconductor recovery cycles, electric vehicle battery innovation, grid-scale energy storage deployment, and the push toward ultra-fast optical communication platforms. The value chain is shifting from commodity-grade titanate intermediates toward high-purity, electronics-grade and battery-grade titanate materials with stringent particle size control, dielectric stability, and electrochemical performance optimization.

Between 2024 and 2025, capacity expansion in electronic ceramics materially strengthened demand for barium titanate. Under its 2024 Medium-Term Business Plan, Nippon Chemical Industrial allocated approximately 6.5 billion yen, nearly 30% of total capital expenditure, toward growth segments including electronic ceramic materials. In 2024, the company fully operationalized a new production building dedicated to high-purity barium titanate, expanding supply to the global MLCC market amid recovering semiconductor demand. In November 2025, Nippon Chemical Industrial and TDK Corporation signed an agreement to initiate joint venture discussions focused on next-generation electronic ceramic components, reinforcing strategic alignment across dielectric material and device integration layers. In January 2026, imec and Veeco announced a major breakthrough enabling integration of barium titanate thin films on silicon photonics platforms. This development supports ultra-fast optical modulators essential for quantum computing architectures and hyperscale data centers, positioning titanates at the intersection of advanced semiconductor packaging and photonic integration.

Lithium titanate oxide chemistry is simultaneously redefining the energy storage segment. In March 2024, ZAPBATT, in collaboration with Toshiba, launched a Battery Operating System optimized for Toshiba’s SCiB lithium titanium oxide batteries, facilitating broader industrial integration of LTO technology. In September 2024, Microvast debuted high-performance LTO battery systems at IAA Transportation, targeting commercial vehicles that require extreme fast-charging capability and long cycle life. Investment momentum accelerated in 2025. In April 2025, South Korea’s Grinergy secured $1.5 million from TitanVolt to expand into Europe. In August 2025, Grinergy and TitanVolt announced plans to establish a lithium titanate production gigafactory in Dundee, Scotland, creating a strategic European hub for EV and grid storage battery manufacturing. These developments underscore rising demand for LTO batteries characterized by rapid charge-discharge rates, superior thermal stability, and extended cycle durability compared to conventional lithium-ion chemistries.

Strategic consolidation and low-carbon feedstock integration are reshaping supply dynamics. In January 2025, Germany-based TIB Chemicals acquired REAXIS Inc., strengthening its global presence in specialty metal salts and titanate-based catalysts. By December 2025, REAXIS was formally rebranded as TIB Chemical Corporation, consolidating its titanate catalyst portfolio under a unified global platform. In late 2025, Sinopec integrated green hydrogen from its Xinjiang project into the synthesis of high-purity inorganic intermediates, providing a lower-carbon pathway for titanate feedstock production in China. In February 2026, Sakai Chemical revised its earnings forecast while signaling a strategic pivot toward R&D-driven growth in electronic materials, including core titanate technologies.

High-Voltage Electrification, Functional Materials Innovation, and Non-Traditional End-Market Expansion in the Titanates Market

Automotive-Grade Barium Titanate Becomes Mission-Critical for 1,000V+ EV Power Electronics

The Titanates market is entering a qualification-driven growth phase, led by barium titanate (BaTiO₃) as a non-substitutable dielectric material for next-generation electric vehicle architectures. The global transition from 400V platforms to 800V and now 1,000V–1,200V systems is fundamentally altering MLCC design constraints, pushing capacitor manufacturers toward ultra-high-purity titanate powders with tightly controlled grain size, defect density, and dielectric constant stability. In high-voltage onboard chargers, DC–DC converters, and CLLC resonant circuits, dielectric failure is no longer a reliability issue but a safety-critical risk, elevating titanate qualification to an OEM-level gate rather than a Tier-2 procurement decision.

This shift is already visible in commercial launches. In December 2025, Samsung Electro-Mechanics introduced the industry’s first 1,000V-rated automotive MLCC in a 1210 package, enabled by proprietary barium titanate stacking and sintering control. Parallel developments from Murata Manufacturing and TDK Corporation in early 2025 demonstrated that next-generation BaTiO₃ powders can support 1,250V ratings in compact 3225 formats, reducing the need for series capacitor arrays. For automakers, this translates directly into a roughly 15% reduction in onboard charger mass and improved thermal packaging density. For titanate producers, it shifts competitive advantage toward crystal engineering, powder morphology consistency, and contamination control rather than bulk tonnage, favoring suppliers capable of meeting automotive PPAP and AEC-Q200 standards at scale.

Lithium Titanate Scales as a Zero-Strain Anode for Extreme Duty and High-Frequency Charging

Alongside BaTiO₃, lithium titanate (Li₄Ti₅O₁₂) is emerging as a structurally distinct growth vector within the titanates market, driven by applications where cycle life, thermal stability, and fast charging outweigh energy density considerations. Heavy-duty electric buses, port vehicles, ferries, mining trucks, and automated guided vehicles are increasingly specifying LTO-based battery systems because the material’s zero-strain lattice eliminates volumetric expansion during lithium insertion. This characteristic enables 20,000+ charge cycles and ultra-fast charging without the degradation mechanisms typical of graphite-based anodes.

Commercial innovation accelerated in April 2025, when Toshiba launched an upgraded SCiB™ lithium titanate module featuring an aluminum heat-dissipating baseplate designed for high C-rate operation. These systems can reach 80% state-of-charge in approximately six minutes while maintaining stable performance across extreme temperature ranges. Policy alignment is reinforcing this trend. Under the EU Green Deal, pilot deployments of LTO-powered public buses in Germany and Scandinavia are validating performance in sub-zero climates where conventional lithium-ion chemistries experience severe capacity loss. As a result, lithium titanate is transitioning from a niche chemistry into a strategic material for mission-critical electrification, expanding the titanates market beyond consumer electronics into infrastructure-grade mobility platforms.

Photocatalytic Titanate Coatings Emerge as Active Urban Air Remediation Materials

A high-impact opportunity for titanates is unfolding in smart city infrastructure through the development of visible-light-active photocatalytic coatings. While titanium dioxide has long been used for self-cleaning surfaces, modified titanates capable of operating under ambient or LED lighting conditions significantly expand addressable applications. These materials actively decompose nitrogen oxides, volatile organic compounds, and hydrocarbons, converting passive building surfaces into functional air-purifying assets.

Government-backed validation is accelerating adoption. In September 2025, the Delhi Environment Department initiated field trials of titanate-based “smog-eating” coatings along high-traffic urban corridors to assess real-world NO₂ abatement. Early-stage research published in 2025 confirms that functionalized titanate composites can sustain high photocatalytic efficiency under ultra-low light intensities as low as 0.1 mW/cm², enabling deployment not only on outdoor facades but also in indoor public spaces. For titanate manufacturers, this opportunity shifts demand toward surface-modified powders and composite formulations rather than bulk pigments, opening premium pricing pathways linked to environmental performance metrics rather than volume consumption.

Biomedical-Grade Titanate Coatings Redefine Long-Term Implant Performance

The medical implant sector represents a structurally attractive, high-margin opportunity for titanates as aging populations drive demand for durable orthopedic and dental solutions. Calcium and strontium titanate coatings are increasingly specified to enhance osseointegration, reduce bacterial adhesion, and mitigate implant loosening over long service lifetimes. Unlike conventional hydroxyapatite coatings, titanate-based surfaces can be engineered for controlled porosity, antimicrobial functionality, and stimuli responsiveness.

Manufacturing innovation is enabling this shift. In 2025, Japanese medical device manufacturers reported increased use of Atomic Layer Deposition to apply nano-scale titanate films onto complex, 3D-printed titanium implants. These coatings are designed to respond to local pH changes associated with inflammation, enabling localized antibiotic release or diagnostic signaling. Biomaterials research published in 2025 shows that titanate-coated porous implants achieve elastic modulus values between 16.37 and 22.56 GPa, closely matching human cortical bone and significantly reducing stress shielding, a leading cause of implant failure. For the titanates market, biomedical applications elevate regulatory compliance, traceability, and surface chemistry control as core value drivers, positioning qualified suppliers for sustained, defensible growth.

Titanates Market Share and Segmentation Insights

Type Market Share: Barium Titanate Leads with MLCC Miniaturization and High Dielectric Performance

Barium titanate dominates the titanates market with a 42.80% share in 2025, supported by its critical role as a ferroelectric ceramic material in multilayer ceramic capacitors (MLCCs). Its high dielectric constant, thermal stability, and reliability make it indispensable in high-performance electronic components. Other types such as organometallic titanates, lithium titanate, strontium titanate, calcium titanate, and other titanates serve niche applications across energy storage, coatings, and specialty ceramics. A key growth driver is MLCC miniaturization, where advancements in nano-sized barium titanate powders and controlled grain structures enable ultra-thin dielectric layers, supporting higher capacitance and compact electronic device architectures.

End-Use Industry Market Share: Electronics and Telecommunications Drives Volume Consumption of Titanates

Electronics and telecommunications accounts for 52.80% of the titanates market in 2025, driven by the extensive use of ceramic capacitors in smartphones, computing devices, and telecom infrastructure. The rapid expansion of 5G networks, IoT ecosystems, and connected devices continues to accelerate demand for high-performance titanate materials. Automotive and transportation, chemicals and plastics, renewable energy, and aerospace and defense contribute additional demand across specialized applications. A major growth trend is the rise of automotive electronics, particularly in electric vehicles and advanced driver assistance systems, where increasing MLCC content per vehicle is significantly boosting titanate consumption across power electronics and control systems.

Titanates Market Competitive Landscape

The titanates market in 2026 is shaped by electronic miniaturization and energy storage density requirements. Industry leaders are advancing hydrothermal synthesis for sub-micron titanates and prioritizing non-toxic titanium-based catalysts to replace heavy metals, aligning with ESPR regulations and next-generation semiconductor, MLCC, and polymer applications.

Chemours Optimizes Titanium Value Chain with Strategic Divestment and High-Purity Titanate Expansion

Chemours maintains leadership across the titanium value chain, leveraging integration from mining to specialty titanates within its Titanium Technologies and Advanced Performance Materials segments. The $360 million divestment of its Taiwan facility in 2026 reflects a shift toward high-margin titanate and thermal management solutions. Its Ti-Pure™ portfolio offers over 20 customized grades for coatings, plastics, and packaging applications. Pricing adjustments in late 2025 stabilized margins amid global volatility and supported innovation investments. The company projects $800–$900 million EBITDA in 2026, reinforcing financial strength. Chemours continues to scale semiconductor-grade titanates for high-performance industrial and electronic applications.

Sakai Chemical Scales Ultra-Fine Barium Titanate for MLCC and 6G Electronics Miniaturization

Sakai Chemical is a global benchmark in electronic-grade titanates, focusing on high-purity barium titanate for MLCC and semiconductor applications. The 2026 commissioning of a ¥300 million multipurpose plant enhances its capacity to support miniaturized electronic components. A 14.7% operating profit increase highlights strong demand in its electronic materials segment. Its ultra-fine particle control technology ensures dielectric consistency required for 5G/6G infrastructure and EV electronics. Adoption by Tier-1 automotive and electronics manufacturers strengthens its global footprint. Dividend expansion to ¥145 per share reflects confidence in sustained demand for advanced titanate materials.

ISK Advances Functional Titanates for Automotive Electrification and ICT Applications

Ishihara Sangyo Kaisha is accelerating its transition toward high-value functional materials under its Vision 2030 roadmap. The company is diversifying titanate properties to enhance dielectric and optical performance in automotive electrification and ICT systems. Revised 2026 earnings guidance of ¥13 billion reflects growth driven by organic chemicals and structural optimization. ISK is implementing low-cost, low-emission manufacturing systems aligned with global carbon neutrality goals. Its titanate technologies are expanding into agrochemical and animal health applications. This diversification strengthens its positioning in adjacent high-growth markets.

Evonik Expands Titanate Catalyst Applications for High-Performance Polymers and Coatings

Evonik is strengthening its role in titanate-based additives and catalysts through its Advanced Technologies segment. A streamlined 2026 distribution network across North America enhances customer access to specialty crosslinkers and coating additives. The company achieved €1.9 billion EBITDA in 2025, with continued growth driven by tailor-made catalyst solutions. Its VISIOMER® platform leverages titanate catalysts to produce high-clarity resins for automotive lighting and optical applications. Evonik is focusing on circular polymer systems, enabling recycling of production waste through advanced catalyst design. Its titanate additives are critical for high-performance coatings, inks, and engineered materials.

Kobo Products Innovates Surface-Treated Titanates for High-Performance Cosmetics and Functional Coatings

Kobo Products leads in surface-treated titanates, particularly for cosmetics and specialty coatings. Its Isopropyl Titanium Triisostearate (ITT) technology enables high pigment loading with ultra-low viscosity, supporting next-generation clean beauty formulations. The Hybrid Treatment (TTB) platform combines titanate chemistry with silicones to deliver dual hydrophobic and lipophilic properties for long-lasting cosmetic performance. Titanate-treated pigments such as BTD-401 provide superior skin affinity and dry-touch characteristics. Expansion of Asia-Pacific technical centers supports regional demand for SPF and mineral-based cosmetic formulations. Kobo’s innovation focus positions it strongly in high-value personal care and coating applications.

Japan Titanates Market Driven by Electronic Materials Leadership and Process Innovation

Japan’s titanates market is structurally anchored in electronic materials, precision ceramics, and environmentally optimized production routes. In November 2025, TDK Corporation and Nippon Chemical Industrial signed a joint venture agreement to accelerate the development of barium titanate and related dielectric materials. The strategic objective is to shorten lead times for 5G and emerging 6G ceramic components, where multilayer ceramic capacitors and RF modules require consistent nano-scale titanate performance. Capacity reinforcement is already visible. Ishihara Sangyo Kaisha, through its MF MATERIAL joint venture with Murata Manufacturing, is expanding high-purity barium titanate output at the Nobeoka No. 2 Plant, with full-scale operations targeted for 2027 to support AI server and data center electronics.

Process leadership remains a differentiator. As of July 2025, Ishihara Sangyo Kaisha is the only Japanese producer operating the chlorine process for titanium-based functional materials, materially lowering waste generation compared with sulfuric acid routes. Product innovation continues across adjacent applications. Fuji Titanium Industry launched metatitanic acid grades in 2025 with particle sizes down to 50 nanometers, enabling precision copier toners and optical filters. Financial signals reinforce the trend. Tosoh Corporation reported a 5.7% net sales increase for FY2025, with specialty inorganic chemicals, including titanate precursors, cited as a key growth engine. Upstream security is also strengthening, as Osaka Titanium and Toho Titanium finalized long-term aerospace supply agreements in 2025, embedding titanate-based catalysts into high-performance alloy manufacturing.

China Titanates Market Anchored in Battery Scale and Alkoxide Export Dominance

China represents the volume center of the global titanates market, underpinned by energy storage and integrated alkoxide production. By December 2025, China accounted for roughly 80% of global lithium titanate battery deployment, driven by expansions from BTR and Microvast, alongside localized operations of Toshiba. Lithium titanate’s fast-charging profile and thermal stability continue to position it as a preferred anode material for buses, grid buffering, and high-duty-cycle transport fleets across Asia.

Policy alignment is reinforcing specialization. Under the MIIT 2026 modernization blueprint, China is prioritizing electronic-grade titanates and associated cleaning chemistries for semiconductor fabrication, aligning purity thresholds above 99.5% with domestic chip self-sufficiency goals. In parallel, Chinese producers dominate organotitanate intermediates. Manufacturers such as Jinan Haohua Industry now control close to 60% of global tetrabutyl titanate supply, leveraging integrated titanium tetrachloride procurement and scale economics. Beyond electronics and batteries, architectural applications are expanding. In April 2025, Nippon Steel selected titanate-treated TranTixxii material for a landmark temple roofing project in Taiwan, underscoring regional demand for titanates in durable, corrosion-resistant cladding systems.

United States Titanates Market Defined by Advanced Research and Regulatory Oversight

The United States titanates market is increasingly shaped by frontier research and structured regulatory compliance. In October 2025, researchers at Stanford University, supported by Samsung and Google, identified strontium titanate as a breakthrough electro-optic material for quantum computing. Its demonstrated electro-optic response, measured at multiples above incumbent materials under cryogenic conditions, has positioned strontium titanate as a strategic material for next-generation photonics and qubit control architectures.

Commercial deployment is advancing in parallel. The U.S. Department of Energy reported in 2025 that over 15 million lithium titanate battery units were deployed across mobile medical devices and remote monitoring stations, reflecting safety-driven adoption over graphite-based systems. At the same time, regulatory rigor is tightening. Under TSCA Section 8(a), U.S. producers of organometallic titanates are now subject to expanded reporting obligations covering usage in consumer coatings and adhesives. This compliance layer is reshaping formulation transparency and favoring suppliers with robust toxicological documentation and traceable production systems.

India Titanates Market Accelerated by Policy-Backed Battery Localization

India’s titanates market is transitioning from import reliance toward strategic domestic processing. The National Critical Minerals Mission, launched in January 2025 with a ₹16,300 crore allocation, explicitly targets the conversion of titanium-bearing ores into value-added titanates for the electric vehicle and stationary storage supply chain. This initiative is materially lowering entry barriers for domestic producers seeking to move upstream into lithium titanate and related functional materials.

Fiscal measures are amplifying momentum. The Union Budget 2025–26 eliminated basic customs duty on several lithium-ion battery inputs, directly improving the economics of lithium titanate cell manufacturing. Under the ₹18,100 crore Production Linked Incentive scheme for Advanced Chemistry Cells, at least ten manufacturers have announced cumulative capacities of 178 GWh by late 2025, with lithium titanate chemistry prioritized for fast-charging electric buses and public transport fleets. Collectively, these measures are positioning India as a secondary but rapidly scaling hub for titanate-based energy storage.

Germany Titanates Market Focused on Separation Media and PFAS-Free Catalysis

Germany’s titanates market is concentrated in high-value separation technologies and sustainable coatings chemistry. Tosoh Bioscience expanded its Griesheim facility in October 2024 to strengthen its chromatography portfolio, which relies on titanate-based media for pharmaceutical and bioprocess separations. This investment reinforces Germany’s role in precision, low-volume titanate applications where consistency and surface chemistry are critical.

Simultaneously, regulatory pressure is driving substitution. In 2025, major German chemical clusters transitioned toward organic titanates as catalysts in esterification and cross-linking reactions, replacing PFAS-based additives in automotive paints and industrial coatings. This shift aligns with tightening European chemical regulations and positions titanates as functional enablers of compliant, high-performance coating systems.

Comparative Snapshot: Titanates Market by Country

Titanates Market County Level Snapshot

|

Country

|

Core Demand Engine

|

Policy or Technology Driver

|

Strategic Position

|

|

Japan

|

Electronic ceramics and capacitors

|

Chlorine process, JV-led R&D

|

High-purity, precision titanates

|

|

China

|

Lithium titanate batteries, alkoxides

|

MIIT modernization, scale integration

|

Volume leadership and export control

|

|

United States

|

Quantum materials, grid storage

|

DOE deployment, TSCA reporting

|

Advanced R&D with compliance focus

|

|

India

|

EV batteries and critical minerals

|

NCMM, PLI ACC incentives

|

Rapid localization and scale-up

|

|

Germany

|

Separation media, coatings catalysis

|

PFAS substitution, EU regulation

|

Premium sustainable applications

|

Titanates Market Report Scope

Titanates Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.2 Billion

|

|

Market Size (2034)

|

$3.6 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Type (Barium Titanate, Lithium Titanate, Strontium Titanate, Calcium Titanate, Organometallic Titanates, Other Titanates), By Application (Energy Storage, Electronic Components, Catalysts and Additives, Optical and Photonics, Mining and Metallurgy), By End-Use Industry (Electronics and Telecommunications, Automotive and Transportation, Renewable Energy, Aerospace and Defense, Chemicals and Plastics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Tosoh Corporation, Ishihara Sangyo Kaisha Ltd., Nippon Chemical Industrial Co. Ltd., Fuji Titanium Industry Co. Ltd., Sakai Chemical Industry Co. Ltd., TDK Corporation, Toho Titanium Co. Ltd., BTR New Material Group Co. Ltd., Microvast Holdings Inc., Dorf Ketal Chemicals, Goulston Technologies Inc., Kronos Worldwide Inc., Evonik Industries AG, BaoTi Group, Ferro Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Titanates Market Segmentation

By Type

- Barium Titanate

- Lithium Titanate

- Strontium Titanate

- Calcium Titanate

- Organometallic Titanates

- Other Titanates

By Application

- Energy Storage

- Electronic Components

- Catalysts and Additives

- Optical and Photonics

- Mining and Metallurgy

By End-Use Industry

- Electronics and Telecommunications

- Automotive and Transportation

- Renewable Energy

- Aerospace and Defense

- Chemicals and Plastics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Titanates Market

- Tosoh Corporation

- Ishihara Sangyo Kaisha Ltd.

- Nippon Chemical Industrial Co. Ltd.

- Fuji Titanium Industry Co. Ltd.

- Sakai Chemical Industry Co. Ltd.

- TDK Corporation

- Toho Titanium Co. Ltd.

- BTR New Material Group Co. Ltd.

- Microvast Holdings Inc.

- Dorf Ketal Chemicals

- Goulston Technologies Inc.

- Kronos Worldwide Inc.

- Evonik Industries AG

- BaoTi Group

- Ferro Corporation

*- List not Exhaustive