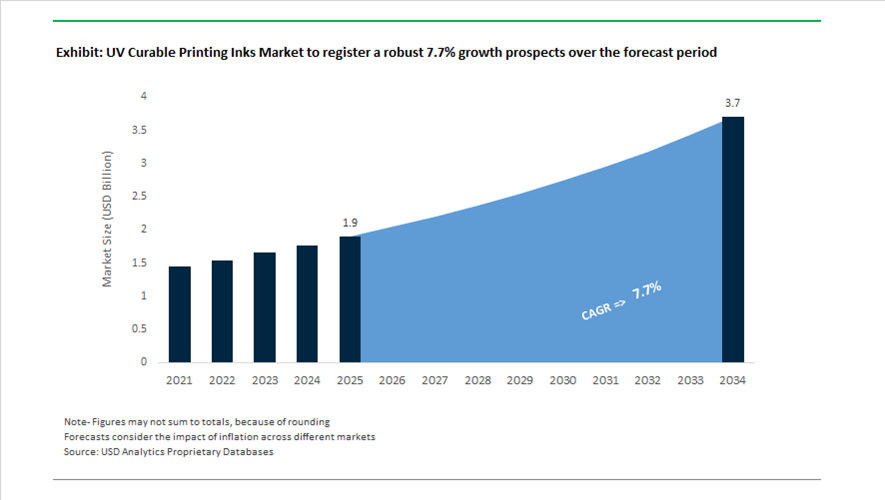

UV Curable Printing Inks Market Overview 2025–2034: $1.9 Billion to $3.7 Billion at 7.7% CAGR Accelerated by Recyclability, Low-VOC Formulations, and High-Speed Digital Packaging

The global UV Curable Printing Inks market is valued at $1.9 billion in 2025 and is projected to reach $3.7 billion by 2034, expanding at a robust CAGR of 7.7%. Growth is being driven by rapid adoption of UV-LED curing technology, low-VOC ink systems, digital inkjet packaging, food contact compliant UV inks, BPA-NI beverage inks, and recyclable flexible packaging solutions. Demand is strongest in folding cartons, shrink sleeves, beverage cans, flexible films, and high-speed commercial printing, where instant curing, superior rub resistance, and reduced energy consumption are critical performance metrics. Regulatory alignment in Europe and North America, combined with sustainability targets across FMCG and beverage brands, is reshaping ink formulation chemistry toward bio-renewable content, solvent-free systems, and deinkable substrates.

Between 2024 and 2026, sustainability and recycling compatibility became central innovation pillars. In June 2024, Toyo Ink announced collaboration with J-Film to develop deinking technology for UV-curable inks used on clear cosmetic packaging, targeting commercialization of a recycling system by 2026 for near-total material recovery. In February 2025, Fujifilm and Mutoh launched AQUAFUZE™, a hybrid water-based UV-LED ink platform commercialized in the Acuity Triton printer. The technology delivers low-VOC, odorless performance with high durability and received the EDP Award 2025 for Best Water-Based Ink. In May 2025, INX International expanded its footprint in Oceania through the acquisition of Galaxy Inks & Coatings Australia and Servicom New Zealand, strengthening regional manufacturing of sustainable UV-curable packaging inks. In July 2025, Sun Chemical introduced SunCure Advance ECO, a bio-renewable UV sheetfed ink line containing 25–30% renewable content and certified by the American Soybean Association, capable of supporting 20,000+ impressions per hour in folding carton production. In late 2025, leading suppliers confirmed readiness for compliance with the German Printing Ink Ordinance ahead of 2026–2027 enforcement, ensuring their food contact material UV ink series meet strict compositional and migration standards. In February 2026, Siegwerk achieved a milestone by securing the first RecyClass approval for UV/LED-curable inks on PE films, confirming compatibility of its SICURA Nutriflex and SICURA Flex series with Europe’s colored PE recycling streams.

Advanced performance and functional specialization are expanding application depth. In July 2025, INX International launched INXJet MDLM, a BPA-NI, No-VOC UV-curable inkjet solution engineered for high-speed digital beverage can decoration, aligning with Nestlé and EuPIA safety standards. In January 2026, Flint Group expanded its EkoCure® XS dual-cure shrink-sleeve ink portfolio, introducing high-performance whites designed to maintain structural integrity during aggressive shrink processes. In February 2026, hubergroup introduced the ELARA additive brand, featuring dispersing and wetting agents tailored for UV-curable and solvent-free systems to enhance pigment stability and surface finish. Regional supply chain scaling also intensified. In April 2024, Toyo Ink India announced a 3.5x capacity expansion at its Gujarat facility, scheduled for completion by April 2026, to support adhesive intermediates and UV ink component production. In February 2026, DIC Corporation unveiled Vision 2030 Phase 2, prioritizing carbon-neutral chemistries and digital transformation of its global ink portfolio.

Trends and Opportunities in the UV Curable Printing Inks Market

75–90% Energy Savings Accelerating UV LED Curing Adoption

Energy efficiency has shifted from a cost advantage to a strategic necessity in the UV curable printing inks market, particularly across Europe and North America where converters face tightening carbon reduction mandates. UV LED curing is emerging as the dominant technology as it fundamentally reshapes pressroom energy economics. According to the 2025 CAS Coatings and Inks Sustainability assessment, UV and electron beam curing systems reduce energy consumption by 75% to 90% compared to solvent-based thermal drying tunnels, directly lowering Scope 2 emissions for printers operating under ESG-linked procurement contracts.

In 2025, leading ink manufacturers such as INX International and Zeller+Gmelin reported that UV LED installations are outpacing mercury-arc UV retrofits across new press deployments. LED curing reduces total press power consumption by approximately 60% to 65%, while eliminating ozone extraction systems and high-voltage standby power requirements. With lamp surface temperatures capped near 40°C, UV LED systems also enable printing on heat-sensitive substrates such as thin films and metallized foils, expanding addressable applications while improving uptime and lamp longevity.

German Printing Ink Ordinance Driving Low-Migration UV Ink Reformulation

Regulatory compliance has become a decisive market filter in UV curable printing inks, particularly for food-contact materials. The German Printing Ink Ordinance, taking full effect on January 1, 2026, is already reshaping ink qualification decisions across European packaging supply chains. In November 2025, Flint Group confirmed that its UV-curable flexographic ink portfolio for food packaging achieved full compliance with the ordinance, which enforces a 0.01 mg/kg detection limit for non-listed substances.

This regulation has intensified scrutiny of photoinitiator chemistry, forcing ink manufacturers to redesign formulations around stabilized, low-migration systems. In response, suppliers such as Siegwerk and Sun Chemical introduced dual-cure UV LED platforms specifically engineered for primary food packaging. These systems incorporate 25% to 30% bio-renewable content and are optimized for high-speed presses exceeding 20,000 impressions per hour, enabling converters to meet food safety compliance without sacrificing productivity or ink laydown performance.

High-Speed Digital UV Inkjet Unlocking Corrugated E-Commerce Growth

The rapid expansion of e-commerce is transforming corrugated packaging into a premium, short-run branding medium, creating a structural growth opportunity for UV curable digital inkjet inks. In 2025, technical performance data from Domino Printing Sciences demonstrated that UV LED curing for corrugated applications consumes up to three times less energy than IR drying required for aqueous inks at high coverage levels. UV inks also eliminate substrate warping and edge curl by avoiding high-temperature moisture evaporation, preserving board integrity during downstream converting.

From an economic standpoint, digital packaging printing represented approximately 4.1% of total printed packaging value by mid-2025, with corrugated formats posting the fastest growth rate. UV curable inks enable variable data printing, QR-based traceability, and Fit-to-Product box customization on demand. This capability supports e-commerce fulfillment models that minimize pre-printed inventory while enhancing brand differentiation, positioning UV inkjet as a core enabler of agile, short-run packaging production.

Distributed Manufacturing and Direct-to-Shape Printing Expanding UV Ink Scope

UV curable inks are increasingly central to distributed manufacturing strategies, where printing and customization occur at regional or point-of-use facilities. In July 2025, INX International launched INXJet MDLM, a UV-curable ink platform designed for direct-to-shape printing on aluminum beverage cans and metal packaging. This allows bottlers to change designs instantly without printing plates or long lead times, aligning with local-for-local production models and reducing logistics-related emissions.

Beyond graphics, UV curable chemistries are gaining traction in industrial and additive manufacturing environments. Research published in August 2025 showed that UV-curable bio-composite inks used in Drop-on-Demand systems can improve the mechanical strength of printed components by up to 20% through optimized layer height control. This opens a high-value pathway for UV inks in customized medical devices, lightweight automotive components, and functional industrial parts, extending the market well beyond traditional printing into advanced manufacturing ecosystems.

UV Curable Printing Inks Market Share and Segmentation Insights

Curing Technology Market Share: UV LED Curing Leads with Energy Efficiency and Advanced Photoinitiator Systems

UV LED curing holds a dominant 52.80% share in the UV curable printing inks market in 2025, driven by its superior energy efficiency, reduced operational costs, and elimination of mercury-based systems. The technology enables instant on and off functionality, longer equipment life, and compatibility with heat-sensitive substrates, making it the preferred choice for modern printing operations. Mercury vapor curing, dual-cure systems, and electron beam curing serve niche or legacy applications. A key trend is LED wavelength optimization, where ink formulations are engineered for 365–405 nm emission ranges, improving cure speed, through-cure performance, and substrate adhesion across packaging and label printing applications.

Application Market Share: Packaging Segment Leads with High-Speed Printing and Sustainable Ink Formulations

Packaging accounts for 48.60% of the UV curable printing inks market in 2025, supported by the need for high-speed, instant-dry printing on non-porous substrates such as films, foils, and metallized papers. UV inks enable superior print quality, durability, and production efficiency in flexible packaging and folding cartons. Labels, commercial printing, and industrial printing contribute additional demand. A major market driver is the shift toward sustainable packaging, where UV ink formulations are designed for recyclability, low migration, and compliance with food contact regulations, enabling converters to meet environmental standards while maintaining high-performance printing outcomes.

UV Curable Printing Inks Market Competitive Landscape

The UV Curable Printing Inks market in 2026 is defined by circular formulation, de-inkable ink systems, ultra-low monomer (ULM) profiles for food-contact materials, and LED-optimized curing technologies, with Product Carbon Footprint transparency emerging as a key differentiator across sustainable packaging and digital printing applications.

DIC Corporation (Sun Chemical) Advances Food-Contact Safe UV Inks with Integrated Supply Chain Control

DIC Corporation, through Sun Chemical, is strengthening its leadership in the UV Curable Printing Inks market with food-safe, low-migration UV ink innovations and vertically integrated pigment supply chains. The launch of SunCure® Advance ECO and EcoPlast solutions targets folding cartons and plastic packaging with enhanced adhesion and compliance with food-contact regulations. Strategic price adjustments in March 2026 reflect cost pass-through amid global supply chain volatility while sustaining R&D investments. The company’s regulatory leadership, including guidance on GIO and PFAS-free transitions, positions it as a key technical advisor to converters. Investment in Quinacridone pigment capacity in Delaware secures upstream raw material availability for high-performance UV inks. This integrated approach enhances supply security and performance consistency.

Flint Group Delivers GIO-Compliant UV Ink Systems with Reduced Photoinitiator Migration

Flint Group is positioning itself as a compliance-first innovator in the UV Curable Printing Inks market, focusing on low-migration solutions for flexible packaging and narrow-web printing. Its Flexocure® LEAP technology introduces a new resin system that significantly reduces photoinitiator migration, addressing critical food-contact safety requirements. Full compliance with the German Printing Ink Ordinance across its European portfolio strengthens its regulatory credibility. Expansion into Eastern Europe through INX Poland enhances regional manufacturing and distribution capabilities. The launch of INXJet™ MDLM UV inkjet inks bridges conventional printing and digital metal decoration applications. This combination of compliance, innovation, and geographic expansion strengthens Flint Group’s competitive positioning.

Siegwerk Leads Circular Packaging with Recyclable UV Ink Technologies

Siegwerk Druckfarben is at the forefront of circularity in the UV Curable Printing Inks market, enabling compatibility between UV inks and mechanical recycling systems. Its SICURA series received RecyClass Technology Approval, confirming suitability for polyethylene flexible packaging recycling streams. The SustainUP initiative integrates ethical sourcing and sustainability into procurement strategies, earning global recognition. Siegwerk is scaling dual-cure UV/LED ink systems to support converters transitioning to energy-efficient LED curing technologies. Its focus on “Circular Packaging Freedom” allows brand owners to achieve recyclability without compromising performance or safety. This leadership in recycling-compatible inks positions Siegwerk as a pioneer in sustainable packaging solutions.

Artience (Toyo Ink Group) Expands Low-Migration UV Ink R&D with Global Innovation Centers

Artience Co., Ltd. is accelerating innovation in the UV Curable Printing Inks market through global R&D expansion and low-migration ink technologies. The establishment of the aTIC innovation center in Bengaluru marks its first overseas research hub, focusing on molecular-level advancements in sustainable materials. Its GIO-compliant UV inks introduced in 2026 combine low-energy LED curing with strong adhesion for food-safe flexible substrates. Price revisions reflect rising production costs while maintaining investment in high-purity formulations. The company is advancing vegetable oil-based and petroleum-free chemistries across its UV ink portfolio. This integration of sustainability and advanced R&D enhances its global competitiveness.

Sakata INX Strengthens De-Inkable UV Ink Solutions for PET Recycling and Digital Printing

Sakata INX is reinforcing its position in the UV Curable Printing Inks market through environmentally oriented chemistries and recyclable ink systems. Its Genesis® washable inks, designed for CPET shrink films, enable efficient de-inking during PET recycling, supporting circular packaging initiatives. Recognition with the EcoVadis Platinum Medal highlights its leadership in sustainability and low-carbon ink development. The company is integrating these de-inkable technologies into UV-curable formats to meet evolving regulatory and recycling requirements. Expansion into digital printing and metal decorating segments strengthens its application diversity. Its focus on botanical and nitrocellulose-free inks aligns with global demand for safe, compliant packaging materials.

Germany: Food-Safe Compliance, LED Curing Uptake, and Functional Packaging Redesign

Germany continues to set the technical and regulatory benchmark for UV curable printing inks, with market evolution shaped by food safety compliance, circular economy targets, and energy-efficient curing systems. In mid-2025, Siegwerk Druckfarben presented its re-engineered SICURA Nutriflex 10 UV flexo series, developed to comply with the updated German Ink Ordinance. The ordinance introduces tighter migration limits for food packaging, pushing ink formulators toward low-migration photoinitiators and optimized oligomer systems suitable for sensitive applications such as flexible food contact materials.

Beyond inks, German producers are expanding into UV-curable functional coatings. Following the April 2024 creation of dedicated business units, suppliers are enabling the replacement of complex multi-material laminates with mono-material, recyclable paper-based packaging. This shift improves recyclability while maintaining barrier and surface performance through UV-curable layers. Manufacturing efficiency is also advancing. By late 2025, more than half of newly installed curing capacity in German print shops had transitioned from mercury vapor lamps to UV LED systems, supported by federal energy reduction subsidies. On the supply side, the October 2024 acquisition of the Heubach Group by Sudarshan Chemical consolidated access to high-performance pigments for UV inks across Europe, strengthening security of supply and formulation depth.

India: Capacity Expansion, Low-Migration Formulations, and Export Positioning

India’s UV curable printing inks market is scaling rapidly on the back of packaging growth, food safety alignment, and policy-backed export ambitions. In November 2025, Toyo Ink India, part of the Artience Group, announced a 1.5x expansion of liquid ink capacity at its Gujarat facility. The expansion specifically targets UV-curable and LED-UV systems to meet accelerating demand from labels, flexible packaging, and folding cartons.

Product innovation is responding to global compliance needs. At PrintPack India 2025, Toyo Ink introduced the Toyo Steraplast UV series, a non-CMR ink platform engineered for high-speed curing and compliance with the Swiss Ordinance for food packaging safety. From a trade perspective, the Ministry of Commerce and Industry is positioning the Gujarat chemical cluster as a regional export hub for UV inks serving Middle Eastern and African markets. This strategy is supported by the Production Linked Incentive scheme, which is improving cost competitiveness and encouraging scale-up of advanced ink technologies.

United States: PFAS Elimination, Specialty Adhesion, and Tighter Food Contact Oversight

The United States UV curable printing inks market is being reshaped by environmental regulation, application-specific performance demands, and stricter documentation for food contact materials. In late 2025, leading suppliers completed the transition to PFAS-free additive portfolios, substituting legacy fluorinated components with alternatives such as rice-bran-derived waxes. This shift reflects intensifying state-level action on persistent chemicals and is influencing ink selection across packaging and commercial print segments.

Performance innovation is targeting complex substrates. INX International launched the INXFlex Contour™ dual-cure UV ink series in 2025, designed for shrink sleeve applications where adhesion challenges traditionally required primers. The new system delivers strong adhesion and durability without additional coating steps. Regulatory expectations are also increasing. As of July 3, 2025, updated guidance from the Food and Drug Administration requires more rigorous migration study data for UV inks used in multi-layer flexible packaging, elevating testing standards and favoring suppliers with robust compliance infrastructure.

Japan: Dual-Cure Flexibility, Precision Pigments, and Bio-Based Resins

Japan’s UV curable printing inks market is characterized by process flexibility, high-precision color control, and early adoption of renewable raw materials. In 2025, DIC Corporation and its subsidiary Sun Chemical introduced a new SolarFlex® LED ink range based on dual-cure chemistry. This allows converters to operate with either LED or conventional UV lamps during transition periods, reducing capital constraints while improving energy efficiency.

Inkjet performance is also advancing through materials science. Japanese R&D programs reported in early 2025 highlighted nano-milled pigment technologies that reduce inter-color bleeding and improve gloss uniformity in high-speed industrial UV inkjet printing. Sustainability is gaining traction as well. By January 2026, several Japanese manufacturers reported UV resin formulations exceeding 30% bio-based content, supporting lower carbon footprints without compromising cure speed or mechanical performance.

United Kingdom and Global Platforms: Water-Based UV and Low-Temperature Processing

The United Kingdom is emerging as a global innovation platform for next-generation UV curable ink technologies. In November 2025, Fujifilm Speciality Ink Systems received the RadTech Europe Innovation Award for its AQUAFUZE technology. This water-based UV LED curing emulsion combines the safety profile of water-based inks with the durability and chemical resistance of UV-curable systems.

AQUAFUZE’s low-temperature curing capability is a critical differentiator. With reported cure temperatures of 40 to 45 degrees Celsius, the system enables UV curable inks to be used on ultra-heat-sensitive substrates such as thin polymer films and delicate textiles. This expands addressable applications while reducing energy consumption and substrate distortion, positioning water-based UV as a credible alternative to solvent and conventional UV systems.

Comparative Snapshot: Country-Level Dynamics in the UV Curable Printing Inks Market

UV Curable Printing Inks Market County Level Snapshot

|

Country or Region

|

Primary Driver

|

Key Application Focus

|

Structural Direction

|

|

Germany

|

Food safety regulation and energy efficiency

|

Food packaging, recyclable papers

|

Low-migration inks and LED UV adoption

|

|

India

|

Capacity scale-up and export policy

|

Packaging and labels

|

Compliance-led growth and regional exports

|

|

United States

|

PFAS bans and FDA oversight

|

Shrink sleeves, flexible packaging

|

Safer additives and specialty adhesion

|

|

Japan

|

Dual-cure flexibility and precision printing

|

Industrial inkjet, electronics

|

Process flexibility and bio-based resins

|

|

United Kingdom

|

Platform innovation

|

Heat-sensitive substrates

|

Water-based UV and low-temperature curing

|

UV Curable Printing Inks Market Report Scope

UV Curable Printing Inks Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.9 Billion

|

|

Market Size (2034)

|

$3.7 Billion

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By Curing Technology (UV LED Curing, Mercury Vapor Curing, Dual-Cure Systems, Electron Beam Curing), By Printing Process (Flexographic UV Inks, Digital Inkjet UV Inks, Offset UV Inks, Screen UV Inks, Gravure UV Inks), By Ink Type (Free Radical Inks, Cationic Inks, Water-Based UV Emulsions, Bio-Based UV Inks), By Application (Packaging, Labels, Commercial Printing, Industrial and Specialty Printing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Siegwerk Druckfarben AG & Co. KGaA, DIC Corporation, Fujifilm Corporation, Flint Group, Toyo Ink SC Holdings, INX International Ink Co., Hubergroup Holding SE, Hewlett-Packard Company, Agfa-Gevaert Group, Sakata Inx Corporation, Marabu GmbH & Co. KG, Nazdar Ink Technologies, T&K Toka Co., Ltd., Wikoff Color Corporation, Epple Druckfarben AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

UV Curable Printing Inks Market Segmentation

By Curing Technology

- UV LED Curing

- Mercury Vapor Curing

- Dual-Cure Systems

- Electron Beam Curing

By Printing Process

- Flexographic UV Inks

- Digital Inkjet UV Inks

- Offset UV Inks

- Screen UV Inks

- Gravure UV Inks

By Ink Type

- Free Radical Inks

- Cationic Inks

- Water-Based UV Emulsions

- Bio-Based UV Inks

By Application

- Packaging

- Labels

- Commercial Printing

- Industrial and Specialty Printing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the UV Curable Printing Inks Market

- Siegwerk Druckfarben AG & Co. KGaA

- DIC Corporation

- Fujifilm Corporation

- Flint Group

- Toyo Ink SC Holdings

- INX International Ink Co.

- Hubergroup Holding SE

- Hewlett-Packard Company

- Agfa-Gevaert Group

- Sakata Inx Corporation

- Marabu GmbH & Co. KG

- Nazdar Ink Technologies

- T&K Toka Co., Ltd.

- Wikoff Color Corporation

- Epple Druckfarben AG

*- List not Exhaustive