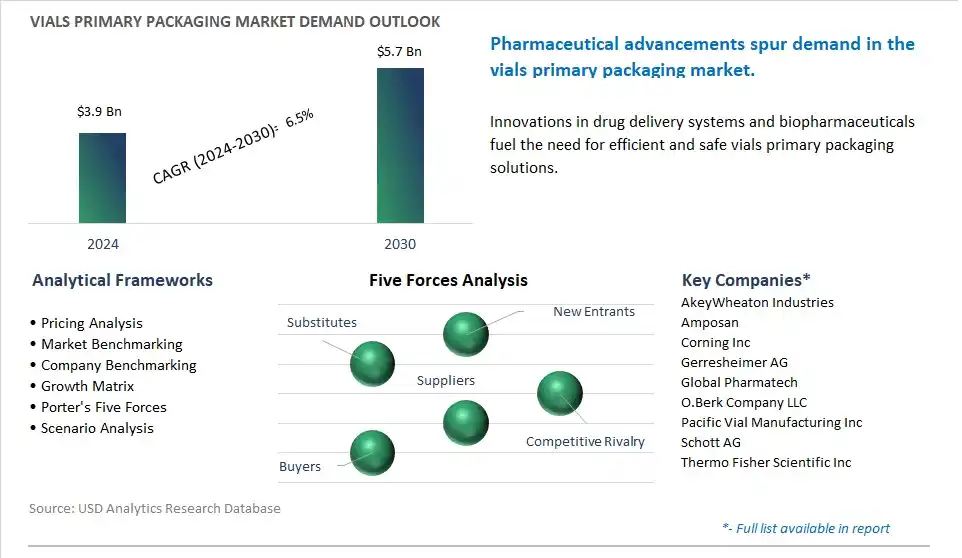

The global Vials Primary Packaging Market is poised to register a 6.5% CAGR from $3.9 Billion in 2024 to $5.7 Billion in 2030.

The global Vials Primary Packaging Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Glass, Plastic), By Application (Hospitals, Research Institutes, Pharmaceutical Industries, Others).

An Introduction to Global Vials Primary Packaging Market in 2024

The vials primary packaging market is experiencing notable growth driven by increasing demand in pharmaceuticals, biotechnology, and healthcare sectors for drug storage, transportation, and administration. Key trends shaping the future of the industry include the growing adoption of vials as primary packaging solutions for injectable drugs, parenteral nutrition, and biologics due to their compatibility with sterilization methods, barrier properties, and ease of handling. Moreover, there's a rising emphasis on quality assurance and regulatory compliance, leading to innovations in vial materials, closure systems, and packaging designs to ensure product integrity, tamper resistance, and patient safety. Additionally, advancements in vial manufacturing processes, automation, and serialization technologies are driving innovation and market differentiation, enabling manufacturers to offer customizable and cost-effective solutions for diverse pharmaceutical packaging needs and market requirements in the global vials primary packaging market.

Vials Primary Packaging Market Competitive Landscape

The market report analyses the leading companies in the industry including AkeyWheaton Industries, Amposan, Corning Inc, Gerresheimer AG, Global Pharmatech, O.Berk Company LLC, Pacific Vial Manufacturing Inc, Schott AG, Thermo Fisher Scientific Inc.

Vials Primary Packaging Market Dynamics

Vials Primary Packaging Market Trend: Increasing Demand for Biologics and Specialty Pharmaceuticals

The most prominent market trend for vials primary packaging is the increasing demand for biologics and specialty pharmaceuticals. Biologics, including vaccines, monoclonal antibodies, and cell therapies, as well as specialty pharmaceuticals such as personalized medicines and orphan drugs, require specialized packaging solutions to maintain product stability, integrity, and sterility. Vials are preferred primary packaging containers for these high-value, sensitive pharmaceutical products due to their compatibility with a wide range of drug formulations, their ability to withstand rigorous sterilization processes, and their inertness to drug interactions. This trend is driven by advancements in biotechnology, personalized medicine, and targeted therapies, as well as the growing prevalence of chronic diseases and the aging population, which necessitate innovative pharmaceutical formulations and packaging solutions to meet patient needs.

Vials Primary Packaging Market Driver: Stringent Regulatory Requirements and Quality Standards

A key market driver for vials primary packaging is stringent regulatory requirements and quality standards in the pharmaceutical industry. Regulatory agencies such as the FDA (Food and Drug Administration) and EMA (European Medicines Agency) have strict guidelines governing the manufacturing, packaging, and labeling of pharmaceutical products to ensure patient safety, product efficacy, and compliance with Good Manufacturing Practices (GMP). Vials primary packaging must adhere to these regulations, which mandate factors such as container integrity, sterility assurance, and compatibility with drug formulations. The need for high-quality, reliable vials packaging solutions is further driven by the increasing complexity of drug formulations, the rise of biologics and personalized medicines, and the globalization of pharmaceutical supply chains, which require robust packaging systems to ensure product quality and regulatory compliance throughout the product lifecycle.

Vials Primary Packaging Market Opportunity: Adoption of Advanced Materials and Manufacturing Technologies

An exciting opportunity in the vials primary packaging market lies in the adoption of advanced materials and manufacturing technologies. Innovations in materials science, such as the development of high-quality glass compositions, polymer coatings, and barrier materials, offer opportunities to enhance vial performance, reduce extractables and leachables, and improve drug stability and compatibility. Additionally, advancements in manufacturing processes, including automated vial production, precision molding, and assembly technologies, enable the production of vials with consistent quality, dimensional accuracy, and customization options. By investing in research and development, collaboration with technology partners, and strategic investments in manufacturing capabilities, vial primary packaging manufacturers can capitalize on the demand for innovative packaging solutions, differentiate their offerings in the market, and address evolving customer needs for safe, reliable, and high-performance pharmaceutical packaging. This opportunity allows vial primary packaging suppliers to strengthen their market position, expand their product portfolio, and drive growth in the dynamic pharmaceutical packaging industry.

Vials Primary Packaging Market Share Analysis: Glass Segment generated the highest revenue in the industry

The largest segment in the Vials Primary Packaging Market is Glass. This dominance can be attributed to diverse factors. The glass vials have a long-standing reputation for being the preferred choice for pharmaceutical packaging due to their inherent properties such as chemical inertness, impermeability to gases and moisture, and non-reactivity with drug formulations. These properties ensure the stability and integrity of pharmaceutical products, protecting them from contamination and degradation over time. Additionally, glass vials offer excellent transparency, allowing for visual inspection of the contents and facilitating accurate dosing and administration of medications. In addition, glass is a recyclable and environmentally friendly material, aligning with the sustainability goals of pharmaceutical companies and regulatory agencies. While plastic vials offer certain advantages such as lighter weight and lower risk of breakage, glass vials continue to dominate the primary packaging market for vials in the pharmaceutical industry due to their superior performance, compatibility with a wide range of drug formulations, and established track record of safety and reliability.

Vials Primary Packaging Market Share Analysis: Pharmaceutical Industries Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Vials Primary Packaging Market is the Pharmaceutical Industries segment. The rapid growth is driven by the pharmaceutical industry is experiencing rapid expansion globally, driven by factors such as population growth, increasing prevalence of chronic diseases, and rising healthcare expenditure. As pharmaceutical companies continue to innovate and develop new drug formulations and biologics, there is a growing demand for high-quality primary packaging solutions, including vials, to ensure the integrity, stability, and safety of medications throughout their lifecycle. Additionally, stringent regulatory requirements for pharmaceutical packaging, including compliance with Good Manufacturing Practices (GMP) and quality standards, contribute to the demand for advanced primary packaging solutions that meet regulatory specifications. In addition, advancements in pharmaceutical manufacturing technologies and processes, such as lyophilization and aseptic filling, require specialized vials capable of withstanding extreme conditions and maintaining product sterility. As a result of these factors, the pharmaceutical industries segment is witnessing significant growth in the vials primary packaging market, driven by the increasing demand for pharmaceutical products and the need for high-quality packaging solutions to meet regulatory requirements and ensure product safety and efficacy.

Vials Primary Packaging Market Report Segmentation

By Type

Glass

Plastic

By Application

Hospitals

Research Institutes

Pharmaceutical Industries

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Vials Primary Packaging Companies Profiled in the Market Study

AkeyWheaton Industries

Amposan

Corning Inc

Gerresheimer AG

Global Pharmatech

O.Berk Company LLC

Pacific Vial Manufacturing Inc

Schott AG

Thermo Fisher Scientific Inc

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Vials Primary Packaging Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Vials Primary Packaging Market Size Outlook, $ Million, 2021 to 2030

3.2 Vials Primary Packaging Market Outlook by Type, $ Million, 2021 to 2030

3.3 Vials Primary Packaging Market Outlook by Product, $ Million, 2021 to 2030

3.4 Vials Primary Packaging Market Outlook by Application, $ Million, 2021 to 2030

3.5 Vials Primary Packaging Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Vials Primary Packaging Industry

4.2 Key Market Trends in Vials Primary Packaging Industry

4.3 Potential Opportunities in Vials Primary Packaging Industry

4.4 Key Challenges in Vials Primary Packaging Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Vials Primary Packaging Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Vials Primary Packaging Market Outlook by Segments

7.1 Vials Primary Packaging Market Outlook by Segments, $ Million, 2021- 2030

By Type

Glass

Plastic

By Application

Hospitals

Research Institutes

Pharmaceutical Industries

Others

8 North America Vials Primary Packaging Market Analysis and Outlook To 2030

8.1 Introduction to North America Vials Primary Packaging Markets in 2024

8.2 North America Vials Primary Packaging Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Vials Primary Packaging Market size Outlook by Segments, 2021-2030

By Type

Glass

Plastic

By Application

Hospitals

Research Institutes

Pharmaceutical Industries

Others

9 Europe Vials Primary Packaging Market Analysis and Outlook To 2030

9.1 Introduction to Europe Vials Primary Packaging Markets in 2024

9.2 Europe Vials Primary Packaging Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Vials Primary Packaging Market Size Outlook by Segments, 2021-2030

By Type

Glass

Plastic

By Application

Hospitals

Research Institutes

Pharmaceutical Industries

Others

10 Asia Pacific Vials Primary Packaging Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Vials Primary Packaging Markets in 2024

10.2 Asia Pacific Vials Primary Packaging Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Vials Primary Packaging Market size Outlook by Segments, 2021-2030

By Type

Glass

Plastic

By Application

Hospitals

Research Institutes

Pharmaceutical Industries

Others

11 South America Vials Primary Packaging Market Analysis and Outlook To 2030

11.1 Introduction to South America Vials Primary Packaging Markets in 2024

11.2 South America Vials Primary Packaging Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Vials Primary Packaging Market size Outlook by Segments, 2021-2030

By Type

Glass

Plastic

By Application

Hospitals

Research Institutes

Pharmaceutical Industries

Others

12 Middle East and Africa Vials Primary Packaging Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Vials Primary Packaging Markets in 2024

12.2 Middle East and Africa Vials Primary Packaging Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Vials Primary Packaging Market size Outlook by Segments, 2021-2030

By Type

Glass

Plastic

By Application

Hospitals

Research Institutes

Pharmaceutical Industries

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

AkeyWheaton Industries

Amposan

Corning Inc

Gerresheimer AG

Global Pharmatech

O.Berk Company LLC

Pacific Vial Manufacturing Inc

Schott AG

Thermo Fisher Scientific Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Glass

Plastic

By Application

Hospitals

Research Institutes

Pharmaceutical Industries

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)