Voluntary Carbon Market (VCM) Overview 2025–2034: $4.8 Billion to $57.6 Billion at 31.8% CAGR Driven by CCP Labeling, Article 6.4 Clarity, and High-Durability Carbon Removal

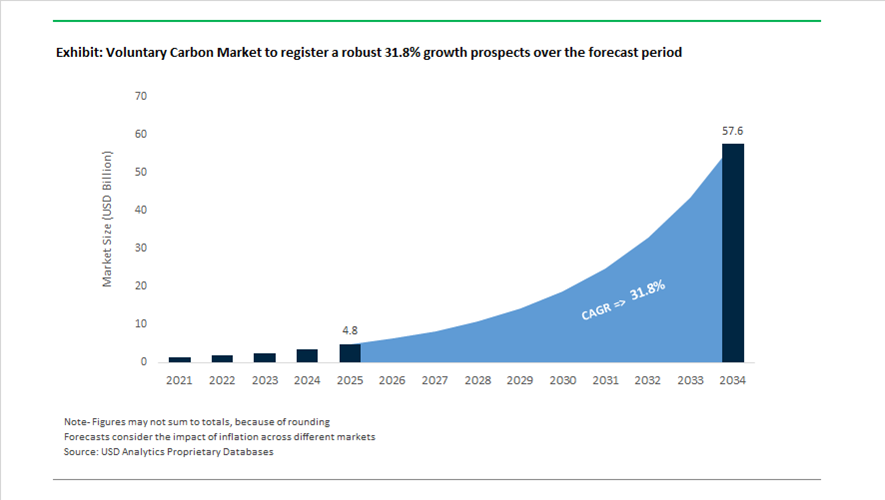

The global Voluntary Carbon Market (VCM) is valued at $4.8 billion in 2025 and is projected to reach $57.6 billion by 2034, expanding at an exceptional CAGR of 31.8%. Growth is being propelled by tightening corporate net-zero commitments, expansion of carbon dioxide removal (CDR) credits, integration with compliance mechanisms under Article 6.4 of the Paris Agreement, and increasing price differentiation between high-integrity and legacy credits. Market structure is shifting from volume-driven avoidance credits toward high-durability removal credits, biodiversity-linked nature credits, superpollutant mitigation offsets, and digitally verified MRV systems. Institutional buyers are prioritizing permanence, additionality, and third-party integrity labeling, resulting in premium pricing for credits aligned with new global standards.

Integrity reforms between 2024 and 2026 materially reshaped pricing dynamics. Throughout 2024 and 2025, the Integrity Council for the Voluntary Carbon Market began issuing Core Carbon Principle (CCP) labels, approving more than 51 million unretired credits under eligible methodologies. By late 2025, CCP-labeled credits were commanding an average 25% price premium relative to non-labeled units. In 2025, Verra launched Version 5 of its Verified Carbon Standard (VCS) program, introducing enhanced additionality screening tools and digitized monitoring, reporting, and verification systems to address legacy concerns around REDD+ methodologies. In November 2025, COP30 negotiators finalized key operational details for Article 6.4, clarifying how voluntary credits may be correspondingly adjusted to avoid double counting, accelerating convergence between the VCM and compliance frameworks such as CORSIA. In January 2026, Verra opened its Nature Framework certification process to all projects, enabling quantification of biodiversity outcomes and issuance of Nature Credits alongside carbon units. Parallel digitalization efforts advanced registry transparency. During 2025–2026, Verra partnered with S&P Global to migrate its registry infrastructure, reducing project review timelines by up to 70% and strengthening traceability across issuance and retirement cycles.

Demand-side acceleration is being led by large technology and energy buyers scaling durable removals. In 2025, Microsoft contracted 45 million metric tonnes of CDR across Direct Air Capture, BECCS, and mineralization projects, more than doubling its 2024 commitments. In January 2026, Microsoft signed a 12-year agreement with Indigo Ag for 2.85 million metric tonnes of soil carbon removals, aligning with CCP integrity standards. In 2025–2026, Drax repositioned itself as a carbon removal provider, offering BECCS credits priced at $350 per ton, reflecting high permanence value. In February 2026, Amazon expanded procurement toward superpollutant reduction projects such as methane and HFC abatement, which represented roughly 20% of total VCM issuances in 2025. Market infrastructure expansion also intensified. In 2025, Xpansiv partnered with the Korea Exchange to launch a standardized carbon trading platform in South Korea, reinforcing Asia-Pacific liquidity channels. Legal and contractual scrutiny increased in early 2026 when Olin Corporation recorded a charge related to a dispute in its Vinyl Chloride Monomer supply chain, underscoring growing compliance oversight across carbon-intensive sectors interacting with offset markets.

Strategic Trends and Opportunities in the Voluntary Carbon Market (VCM)

Strategic Pivot Toward CCP-Labeled High-Integrity Carbon Credits

Market credibility has become the single most decisive factor shaping liquidity, pricing power, and buyer participation in the Voluntary Carbon Market. The introduction of the Core Carbon Principles (CCPs) by the Integrity Council for the Voluntary Carbon Market has effectively split the VCM into two structurally distinct tiers. High-integrity CCP-labeled credits are increasingly treated as investable climate instruments, while legacy credits without robust additionality, permanence, and MRV assurances are facing declining demand and widening discounts. By October 2025, more than 51 million unretired credits had been approved for CCP labeling, representing only about 4% of total credits issued in 2024, underscoring the structural scarcity embedded in the premium segment. This scarcity has translated directly into pricing power, with CCP-aligned credits trading at roughly a 25% premium on average, and in some cases reaching multiples when benchmarked against low-integrity indices.

Regulatory signaling has reinforced this bifurcation. In May 2024, the U.S. Department of the Treasury, working alongside the U.S. Department of Energy and the U.S. Department of Agriculture, issued a joint policy statement explicitly endorsing high-integrity voluntary carbon markets. This was followed by final guidance from the Commodity Futures Trading Commission, which standardized voluntary carbon credit derivatives. Collectively, these actions are reframing high-quality voluntary credits as a legitimate, compliance-adjacent financial asset class, accelerating institutional participation.

Rise of Direct Equity Stakes and Advance Purchase Agreements

As competition intensifies for a limited pool of high-integrity carbon removals, leading buyers are moving decisively away from spot market procurement toward long-term capital deployment models. Advance Purchase Agreements and direct equity investments are now central to corporate carbon strategies, particularly for engineered removals such as Direct Air Capture. These structures allow buyers to secure future supply at predictable prices while providing developers with the bankability required to finance capital-intensive infrastructure. In March 2024, CarbonCapture Inc. closed an $80 million Series A round anchored by strategic industrial investors, highlighting the shift toward balance-sheet backed climate procurement.

Public sector participation is amplifying this trend. The U.S. Department of Energy has moved beyond policy support into direct demand creation, announcing $35 million in semi-finalist awards for the first federal purchase of carbon removal credits. At the project level, long-term offtake commitments are proving decisive. In October 2025, Canada’s Tamarack DAC project achieved its first capture milestone, a development made viable largely through multi-year corporate purchase agreements. This evolution signals a structural re-rating of the VCM from transactional offsetting toward infrastructure-style climate investment.

Monetizing Regenerative Agriculture Through Advanced Soil Carbon MRV

A major growth opportunity in the Voluntary Carbon Market is emerging from regenerative agriculture, enabled by rapid advances in Measurement, Reporting, and Verification technologies. Soil carbon, long considered too fragmented and uncertain for scalable markets, is now becoming investable due to digital MRV platforms, satellite monitoring, and model-based verification. According to the World Development Report 2025 published by the World Bank, agricultural carbon credits reached a market value of $5.83 billion in 2024, supported by regulatory streamlining under the U.S. Growing Climate Solutions Act. This framework has lowered entry barriers for farmers by certifying technical assistance providers and verifiers under USDA oversight.

Large corporates are accelerating demand by embedding soil carbon credits directly into their value chains. Agribusiness leaders such as Cargill and Bayer are using satellite-verified soil carbon projects to generate inset credits that support Scope 3 decarbonization. This model simultaneously enhances supply chain resilience and creates recurring income streams for producers, aligning climate finance with agricultural productivity across thousands of science-based target adopters worldwide.

Article 6 as a Compliance-Adjacent Growth Engine for the VCM

The operational rollout of Article 6 of the Paris Agreement is creating a powerful new revenue channel that links voluntary markets with national compliance systems. Under Article 6.2, Internationally Transferred Mitigation Outcomes allow countries to trade emission reductions while applying corresponding adjustments to prevent double counting. By mid-December 2025, 106 bilateral agreements had been signed among 62 countries, establishing a sovereign-backed framework that significantly enhances credit credibility. Countries such as Singapore and Switzerland have emerged as anchor buyers, executing agreements with nations including Ethiopia, Malawi, Zambia, and Mongolia to secure high-integrity mitigation outcomes aligned with national climate strategies.

This architecture is also enabling the transition of legacy mechanisms. Under Article 6.4, also referred to as the Paris Agreement Crediting Mechanism, more than 1,000 projects have submitted notifications of prior consideration. If approved, this transition from the Clean Development Mechanism could mobilize over 900 million tonnes of high-integrity CO₂e reductions. For project developers and investors, Article 6 represents a convergence point where voluntary credits gain quasi-compliance status, unlocking deeper liquidity, longer contract tenors, and a structurally larger addressable market for premium carbon assets.

Voluntary Carbon Market (VCM) Share and Segmentation Insights

Category Market Share: Nature-Based Solutions Lead with High-Quality Carbon Credit Demand

Nature-based solutions account for 58.60% of the voluntary carbon market in 2025, driven by projects such as reforestation, afforestation, blue carbon, and soil carbon initiatives. These solutions offer additional environmental and social co-benefits, including biodiversity conservation and community development, making them highly attractive to corporate buyers. Technology-based removals and avoidance or reduction credits contribute to a diversified credit portfolio. A key market trend is the growing premium for high-quality carbon credits, where buyers prioritize verified projects with strong additionality, permanence, and transparent monitoring, supporting higher pricing for nature-based credits with measurable impact.

End-User Industry Market Share: Technology Sector Leads with Net-Zero Commitments and Scope 3 Focus

Technology companies hold a 34.80% share in the voluntary carbon market in 2025, reflecting their leadership in corporate sustainability and net-zero commitments. These organizations actively invest in carbon credits to offset residual emissions and enhance environmental credentials. Energy and utilities, consumer goods, aviation, and shipping sectors also contribute to demand across compliance and voluntary frameworks. A key trend is the increasing focus on scope 3 emissions, where technology firms are adopting portfolio approaches that combine carbon removals and reductions across supply chains, driving demand for innovative, high-quality carbon credit solutions aligned with long-term decarbonization strategies.

Voluntary Carbon VCM Market Competitive Landscape

The Voluntary Carbon Market (VCM) in 2026 is defined by structural professionalization, multi-year offtake agreements, and digital MRV systems, with high-durability carbon removal solutions such as biochar and BECCS commanding premium pricing amid rising scrutiny over credit integrity and net-zero compliance.

South Pole Accelerates High-Durability Carbon Removal with TechGen Buyers’ Club

South Pole is reinforcing its leadership in the Voluntary Carbon Market through high-integrity project development and innovative procurement platforms. The launch of TechGen in 2026 enables pooled risk-sharing and long-term offtake agreements for emerging carbon dioxide removal technologies. The company has supported over 850 climate projects across 50+ countries, delivering more than 200 million tonnes of CO2e reductions. Its 2026 buyer guide highlights that 77% of financial institutions favor companies with structured carbon credit strategies. South Pole is actively guiding corporates through regulatory frameworks such as the EU CRCF and CBAM. This combination of project scale and regulatory foresight strengthens its position as a leading climate solutions provider.

Carbon Direct Sets Benchmark for High-Quality CDR Procurement and Scientific Validation

Carbon Direct is a leading science-based advisory firm in the Voluntary Carbon Market, specializing in high-durability carbon removal procurement. Its 2026 market report highlights over 90 million tonnes of forward-contracted demand for durable CDR solutions despite nature-based credits dominating current supply. The firm applies stringent quality criteria, approving fewer than 10% of evaluated projects for investment. As a strategic partner to major corporations, it manages large-scale removal portfolios with a focus on Biomass Carbon Removal and Storage (BiCRS). Carbon Direct is actively promoting forward offtake agreements to secure future supply amid tightening market conditions. This rigorous scientific validation framework positions it as a trusted advisor in high-integrity carbon markets.

Climate Impact X Drives Standardized Carbon Trading with Institutional-Grade Market Infrastructure

Climate Impact X (CIX) is transforming the Voluntary Carbon Market through standardized contracts and enhanced price transparency. The launch of CORSIA Phase 1 standardized contracts enables airlines to access compliant carbon credits across ICAO-approved registries. Integration with the S&P Global Meta Registry provides access to 12 registries, simplifying credit retirement for corporate buyers. Collaboration with MSCI enhances market intelligence through real-time pricing and project-level analytics. Recognition as the “Best Carbon Exchange 2025” underscores its credibility in institutional markets. This infrastructure-driven approach is standardizing carbon trading and improving liquidity across global markets.

Verra Advances Digital Carbon Registry and Scope 3 Decarbonization Standards

Verra is leading the Voluntary Carbon Market through registry innovation and integrity-focused standards development. The launch of its Scope 3 Standard enables corporations to generate Intervention Units for value-chain decarbonization across sectors such as agriculture and construction. Its digital-native project hub incorporates automated attribution tools to prevent double counting and ensure compliance with GHGP and SBTi frameworks. Alignment with ICVCM standards through VCS Version 5.0 enhances credibility of issued credits. Verra is actively developing advanced reporting frameworks for complex global supply chains. This focus on digitalization and standardization strengthens its role as the backbone of global carbon credit infrastructure.

Sylvera Establishes Credit-Level Ratings and Data Transparency in Carbon Markets

Sylvera is shaping the Voluntary Carbon Market through independent ratings and data-driven verification of carbon credits. Its analysis shows high-quality ARR projects achieving premiums above $35 per tonne, while lower-rated credits face pricing pressure below $20. The company has expanded into carbon-differentiated commodity markets, providing emissions data for cement, ammonia, and hydrogen. Rapid adoption by major corporations reflects growing demand for transparent, credit-level performance insights. Its proprietary geospatial analytics and machine learning tools enable real-time monitoring of carbon assets. This emphasis on independent verification and data transparency positions Sylvera as a key enabler of market integrity.

United States Voluntary Carbon Market Defined by Regulatory Flexibility and Corporate-Led Removals

The United States voluntary carbon market entered a recalibration phase in 2025, marked by a deliberate shift away from prescriptive federal templates toward principles-based oversight. In September 2025, the Commodity Futures Trading Commission withdrew its 2024 guidance on listing voluntary carbon credit derivatives. This move redirected exchanges toward reliance on the Commodity Exchange Act uniform framework, encouraging innovation in contract design rather than rigid standardization. As a result, U.S. exchanges and intermediaries are experimenting with bespoke contract structures linked to durability, delivery risk, and credit vintage differentiation, reinforcing the sophistication of the domestic VCM ecosystem.

Corporate procurement behavior remains the dominant demand driver. Throughout 2025, U.S. technology companies significantly expanded carbon removal purchasing, with Microsoft accounting for a majority share of global durable carbon dioxide removal contracts. Procurement focused heavily on biochar and direct air capture with carbon storage to align with Microsoft’s 2030 carbon-negative commitment. Parallel regulatory pressure is reinforcing quality thresholds. Following the implementation of enhanced climate-related disclosures, overseen by the U.S. Securities and Exchange Commission, listed companies accelerated voluntary credit retirements to substantiate Scope 3 claims. This has driven a pronounced flight toward credits aligned with the ICVCM Core Carbon Principles, elevating verification rigor and permanence as primary purchasing criteria.

India Voluntary Carbon Market Anchored in Hybrid Compliance-Voluntary Architecture

India’s voluntary carbon market is transitioning into a hybrid structure that tightly links offsets with compliance obligations. The Indian Carbon Credit Trading Scheme is scheduled for operational launch in mid-2026, integrating a voluntary offset mechanism with a national compliance framework covering nine energy-intensive sectors and more than 740 regulated entities. This architecture positions voluntary credits not as peripheral instruments, but as a liquidity bridge between uncovered sectors and the future compliance market.

Institutional reforms in 2025 laid the groundwork for this transition. The government initiated the phased migration of the Perform, Achieve and Trade scheme into the CCTS, with mandatory emission intensity reductions deliberately back-loaded. Approximately 60% of required reductions are scheduled for the 2026–2027 cycle, creating near-term demand for voluntary offsets. In March 2025, the Bureau of Energy Efficiency released Version 1 of the Offset Mechanism, approving eight domestic methodologies for voluntary projects. This regulatory clarity has materially improved credit bankability and is expected to boost liquidity from industrial efficiency, renewable energy, and waste-to-energy projects.

European Union Voluntary Carbon Market Structured Around Certification and Buyer Aggregation

The European Union voluntary carbon market is evolving into a highly institutionalized framework centered on removals certification and demand aggregation. The Carbon Removal Certification Framework enters its operational phase in early 2026, with the European Commission beginning to accept applications for certification schemes that meet the transparency and monitoring requirements set out in Implementing Regulation (EU) 2025/2358. This framework establishes a unified credibility baseline for removals, differentiating European credits from fragmented global standards.

To stimulate early demand, the Commission launched an EU Buyers’ Club in late 2025, pooling private-sector demand for permanent removal pathways such as bioenergy with carbon capture and storage and direct air capture. These aggregated offtake commitments provide up to 15 years of revenue visibility, directly addressing investor risk in capital-intensive removal technologies. At the project level, new delegated acts effective from 2026 introduce tailored methodologies for soil carbon and forestry, including peatland rewetting and afforestation. These rules enable European farmers and land managers to generate certified voluntary credits for corporate buyers, embedding carbon farming into the EU’s broader agricultural and climate strategy.

Indonesia Voluntary Carbon Market Positioned on Blue Carbon and Regional Competitiveness

Indonesia’s voluntary carbon market is gaining international visibility through institutional transparency and strong alignment with national fiscal policy. The Indonesia Carbon Exchange, inaugurated for international trading in January 2025, was recognized with the Carbon Positive Award for its auction-based pricing and disclosure mechanisms. This platform has improved price discovery and buyer confidence, particularly for nature-based credits originating from peatland and mangrove ecosystems.

Policy synchronization is a critical differentiator. The Indonesian government has confirmed that its national carbon tax will take effect in 2026, deliberately timed alongside the European Union’s Carbon Border Adjustment Mechanism. This sequencing is designed to preserve the competitiveness of domestic credits in export-oriented sectors. Government estimates place Indonesia’s carbon trading economic potential at IDR 3,000 trillion, with strategic emphasis on peatland restoration and blue carbon projects that offer high mitigation potential alongside biodiversity and coastal resilience co-benefits.

Brazil Voluntary Carbon Market Entering Formal Institutionalization Phase

Brazil’s voluntary carbon market is moving from policy signaling to formal institutionalization. In October 2025, President Lula signed Decree 12,677, establishing the Extraordinary Secretariat for the Carbon Market. This body is mandated to finalize the regulatory architecture of the Sistema Brasileiro de Comércio de Emissões, including rules for credit issuance, registry alignment, and integration with voluntary mechanisms.

At the international level, Brazil used COP30 in 2025 to propose the Open Coalition for Carbon Market Integration. The initiative aims to harmonize standards across jurisdictions and facilitate interoperability between existing voluntary systems. By positioning itself as a convening power for cross-border liquidity, Brazil is seeking to leverage its vast forestry and land-use mitigation potential into a globally connected VCM framework rather than a purely domestic market.

Singapore Voluntary Carbon Market Functioning as Asia-Pacific Innovation Hub

Singapore continues to consolidate its role as the Asia-Pacific hub for high-integrity voluntary carbon markets. In 2025, the country launched the Equatic-1 ocean carbon removal pilot, the largest of its kind globally, with a targeted capacity of ten tonnes per day by the first quarter of 2026. This project underscores Singapore’s focus on engineered and ocean-based removals with high durability.

Policy instruments reinforce demand. Singapore expanded its Article 6.2 bilateral framework in 2025 by signing carbon credit transfer agreements with Thailand and Vietnam. These agreements allow tax-liable companies to offset up to five% of their carbon tax obligations using approved international credits. This mechanism has created predictable demand for high-quality credits while maintaining environmental integrity thresholds, strengthening Singapore’s role as a regional clearinghouse for voluntary transactions.

Kenya Voluntary Carbon Market Strengthened by Registry Transparency and Global Coalitions

Kenya’s voluntary carbon market is being formalized through governance and international collaboration. In July 2025, the government unveiled the Climate Change Carbon Registry Regulations, establishing a mandatory electronic registry for all projects generating credits under bilateral or international agreements. This system enhances state oversight, prevents double counting, and improves traceability for buyers seeking high-integrity African credits.

Kenya is also shaping the global agenda. In partnership with Singapore and the United Kingdom, the country co-launched the Coalition to Grow Carbon Markets during the 2025 London Climate Action Week. The coalition’s objective is to unlock up to $250 billion in climate finance by 2050 by scaling high-integrity voluntary markets. This positioning reinforces Kenya’s role not just as a project host country, but as an active architect of the future VCM governance landscape.

Summary of Country-Level Voluntary Carbon Market Dynamics

Voluntary Carbon Market County Level Snapshot

|

Country / Region

|

Primary Policy Lever

|

Core Credit Focus

|

Strategic Positioning

|

|

United States

|

Derivatives flexibility and disclosure rules

|

Durable removals, CCP-aligned credits

|

Corporate-led quality benchmark

|

|

India

|

Hybrid compliance-voluntary integration

|

Industrial efficiency, energy projects

|

Liquidity bridge to compliance market

|

|

European Union

|

CRCF and buyers’ aggregation

|

Certified removals, carbon farming

|

Institutional credibility leader

|

|

Indonesia

|

Carbon exchange and tax alignment

|

Peatland and blue carbon

|

Nature-based scale with transparency

|

|

Brazil

|

SBCE institutionalization

|

Forestry and land-use mitigation

|

Global integration convenor

|

|

Singapore

|

Article 6.2 bilateralism

|

Engineered and ocean removals

|

Asia-Pacific VCM hub

|

|

Kenya

|

National registry and coalitions

|

Nature-based projects

|

Governance-focused emerging leader

|

Voluntary Carbon Market Report Scope

Voluntary Carbon Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.8 Billion

|

|

Market Size (2034)

|

$57.6 Billion

|

|

Market Growth Rate

|

31.8%

|

|

Segments

|

By Category (Nature-Based Solutions, Technology-Based Removals, Avoidance and Reduction), By Credit Quality (Core Carbon Principle Credits, CORSIA-Eligible Credits, Article 6-Aligned Credits), By Project Structure (Host Country Projects, Jurisdictional and Nested Projects), By End-User Industry (Technology, Energy and Utilities, Aviation and Shipping, Consumer Goods and Retail)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

South Pole, EcoSecurities, ClimatePartner, FirstClimate, Vertree, Respira International, Genzero, 3Degrees, TerraPass, Aera Group, Puro.earth, Verra, Gold Standard, Climeworks, Indigo Ag

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Voluntary Carbon Market Segmentation

By Category

REDD+

Afforestation and Reforestation

Blue Carbon

Soil Carbon

- Technology-Based Removals

Direct Air Capture

Bioenergy with Carbon Capture and Storage

Biochar

Enhanced Rock Weathering

Renewable Energy

Energy Efficiency

Methane Capture

Clean Cookstoves

By Credit Quality

- Core Carbon Principle Credits

- CORSIA-Eligible Credits

- Article 6-Aligned Credits

By Project Structure

- Host Country Projects

- Jurisdictional and Nested Projects

By End-User Industry

- Technology

- Energy and Utilities

- Aviation and Shipping

- Consumer Goods and Retail

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Voluntary Carbon Market

- South Pole

- EcoSecurities

- ClimatePartner

- FirstClimate

- Vertree

- Respira International

- Genzero

- 3Degrees

- TerraPass

- Aera Group

- Puro.earth

- Verra

- Gold Standard

- Climeworks

- Indigo Ag

*- List not Exhaustive