Water and Wastewater Treatment Technologies Market Overview 2025–2034: $40.8 Billion to $67.8 Billion at 5.8% CAGR Driven by PFAS Mitigation, ZLD Systems, and Advanced Membrane Infrastructure

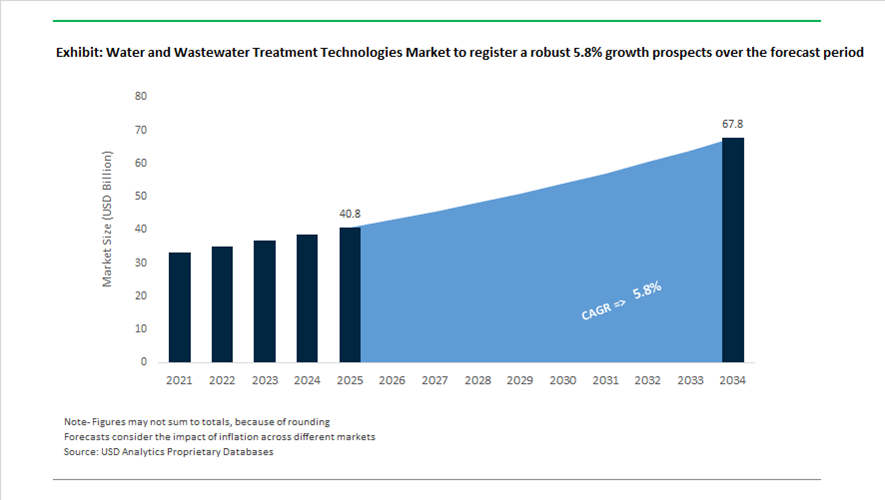

The Water and Wastewater Treatment Technologies market is valued at $40.8 billion in 2025 and is projected to reach $67.8 billion by 2034, expanding at a CAGR of 5.8%. Growth is anchored in tightening environmental discharge standards, industrial water reuse mandates, PFAS remediation requirements, desalination investments, and semiconductor-driven ultrapure water demand. The market encompasses reverse osmosis (RO) membranes, ultrafiltration (UF), nanofiltration (NF), UV disinfection systems, zero liquid discharge (ZLD) technologies, sludge dewatering solutions, advanced oxidation processes (AOP), and high-efficiency evaporators. Capital deployment is accelerating across North America and Asia-Pacific, with water infrastructure positioned as a national resilience priority amid climate stress, groundwater depletion, and transboundary contamination challenges.

In 2024, major technology providers sharpened their high-value portfolios. Veolia introduced its “GreenUp 24–27” PFAS and micropollutant treatment platform, combining foam fractionation with high-recovery RO membranes to address emerging “forever chemical” regulations. DuPont Water Solutions expanded its FilmTec™ dairy-focused RO range with the MXP RO-8038-FF element, engineered for high-solids concentration processes to improve recovery rates and reduce fouling in food and beverage operations. These product-level innovations coincide with a broader pivot toward advanced membrane technologies capable of delivering higher flux, lower energy consumption, and superior contaminant rejection.

Strategic consolidation intensified in 2025 as companies pursued vertical integration and regional specialization. In February 2025, Veralto acquired Aquafides for $20 million, strengthening its chemical-free UV disinfection portfolio. In March 2025, Veolia reported record financial results following the integration of Suez assets, highlighting a 15% reduction in CO2 emissions and 1.45 billion cubic meters of freshwater savings through operational efficiencies. In June 2025, Aquatech acquired Singapore-based Century Water, establishing a global Center of Excellence focused on ultrapure water and ZLD solutions for semiconductor and pharmaceutical manufacturing. In September 2025, Kemira acquired Water Engineering, Inc. for $150 million, expanding its North American footprint in industrial water treatment services targeting healthcare and food processing clients. These transactions reflect a clear industry strategy: combine chemicals, membranes, digital monitoring, and service contracts into full-stack water treatment platforms.

Public-sector infrastructure deployment accelerated during 2025–2026. In August 2025, the US EPA and IBWC completed a 10 MGD expansion of the South Bay International Wastewater Treatment Plant addressing the Tijuana River transboundary crisis, delivered within a 100-day fast-track schedule. In December 2025, California finalized eight major water projects totaling $2.9 billion, including the Antioch Brackish Water Desalination Plant and the Monterey Advanced Water Purification Facility, collectively adding nearly 3 billion gallons annually to the state’s drinking water supply. The City of Brandon initiated a major facility expansion in late 2025 featuring dual-membrane UF and NF systems, with outfall infrastructure targeted for completion in February 2026. In January 2026, Suez secured Hong Kong’s Sha Tin cavern sewage treatment contract, setting a benchmark for subterranean wastewater infrastructure to optimize urban land use. By October 2026, Suez and PYREG introduced an integrated pyrocarbonisation solution converting sewage sludge into biochar, linking wastewater management with carbon sequestration and circular economy objectives.

Water and Wastewater Treatment Technologies Market Trends and Opportunities: PFAS Regulation, ESG-Driven Reuse, and Smart Infrastructure

PFAS Regulation Driving Advanced Treatment Technologies and Destruction-Based Solutions

The Water and Wastewater Treatment Technologies market is being fundamentally reshaped by stringent regulatory mandates targeting PFAS (“forever chemicals”), transforming treatment from containment-based approaches to advanced destruction and mineralization technologies. The enforcement of ultra-low thresholds is compelling utilities and industries to deploy high-performance treatment systems such as granular activated carbon (GAC), ion exchange resins, and high-pressure membrane filtration.

A major regulatory milestone was the U.S. EPA’s National Primary Drinking Water Regulation (NPDWR) finalized in April 2024, setting Maximum Contaminant Levels (MCLs) for PFOA and PFOS at 4.0 ppt. Public water systems are required to complete monitoring by 2027 and implement treatment solutions by 2029, triggering large-scale infrastructure upgrades. Backed by the $9 billion allocation under the Infrastructure Investment and Jobs Act, annual implementation costs are projected to reach $1.5 billion by 2026, underscoring the scale of compliance-driven capital expenditure.

In parallel, Europe is advancing a group-wide PFAS restriction under REACH, with a final evaluation expected by 2026. This regulatory push is estimated to generate up to €18 billion in annual treatment costs, reinforcing global demand for next-generation PFAS removal technologies. Importantly, the market is shifting toward permanent destruction solutions, including electrochemical oxidation and advanced oxidation processes, with the PFAS destruction segment projected to reach $3.0 billion by 2026, reflecting a transition toward carbon-fluorine bond mineralization and zero-waste treatment systems.

Industrial Water Reuse and ESG Compliance Accelerating Closed-Loop Treatment Adoption

Rising water scarcity and the operationalization of corporate ESG mandates are accelerating the adoption of industrial water reuse technologies, positioning wastewater as a strategic resource rather than a disposal challenge. Companies are increasingly implementing “Net Water Positive” strategies, leveraging advanced treatment systems such as membrane bioreactors (MBRs) and closed-loop recycling infrastructure to reduce freshwater dependency.

Corporate case studies highlight rapid progress. By March 2024, PepsiCo achieved a 25% improvement in water-use efficiency in high-risk regions, driven by the deployment of MBR systems across 21 sites, enabling up to 70% reduction in freshwater intake. This reflects a broader industry shift toward high-efficiency wastewater recycling technologies that support both sustainability targets and cost optimization.

The emergence of quantitative ESG benchmarking tools, such as the Water Sustainability Index, is further accelerating adoption. Facilities integrating advanced reuse systems can improve scores from 1.17 to 3.0, directly influencing investor perception and regulatory compliance. Additionally, with only 6.4% of wastewater currently reused in the U.S., policy initiatives such as the EPA Water Reuse Action Plan are driving industrial users toward alternative water sourcing strategies, including recycled effluent and brackish water utilization, reinforcing long-term demand for water reuse and recycling technologies.

Decentralized Water Treatment Systems Enabling Resource Recovery and Circular Water Economies

A significant growth opportunity lies in the rise of decentralized water and wastewater treatment systems, which enable on-site water purification, resource recovery, and infrastructure resilience. These modular and containerized solutions are gaining traction as cost-effective alternatives to centralized treatment plants, particularly in urban developments, industrial clusters, and remote locations.

The decentralized water treatment market reached $23.08 billion in 2024, with strong growth driven by the adoption of point-of-use and cluster-based systems capable of recovering up to 97% of wastewater for reuse. These systems are increasingly integrated into green buildings and smart cities, supported by certification frameworks such as LEED and WELL, which incentivize on-site water recycling to improve sustainability metrics.

Beyond water recovery, advanced decentralized systems are evolving into resource valorization platforms, capable of generating energy, fertilizers, and reusable by-products from wastewater streams. Technologies developed by companies such as Organica Water and BioKube are enabling biological nutrient recovery and energy generation, transforming wastewater from a cost center into a revenue-generating asset. This aligns with the broader shift toward circular water economies and distributed infrastructure models, particularly in regions facing water stress and aging utility networks.

AI and Digital Twin Technologies Transforming Smart Water Treatment Plant Operations

The integration of Artificial Intelligence (AI) and Digital Twin technology is revolutionizing water treatment operations, enabling real-time optimization, predictive maintenance, and enhanced system resilience. These technologies are central to the transition toward smart water infrastructure, where operational decisions are driven by data analytics and simulation-based insights.

AI-powered systems are delivering measurable efficiency gains. By 2025, solutions such as Xylem Vue’s dynamic optimization platforms demonstrated the ability to reduce energy consumption by up to 25%, through real-time adjustment of chemical dosing and process parameters based on fluctuating water quality conditions. This is particularly critical in large-scale treatment plants where energy and chemical costs represent a significant portion of operating expenditure.

The Digital Twin water treatment market, valued at $1.42 billion in 2024, is expanding rapidly as utilities adopt virtual replicas of physical assets to simulate operational scenarios, including extreme weather events and system failures. These platforms enhance asset lifecycle management, enabling early fault detection and reducing maintenance costs through predictive analytics.

Additionally, the convergence of cybersecurity and operational technology (OT/ICS) within digital twin ecosystems is becoming a strategic priority. By 2026, utilities are deploying integrated platforms that provide a unified, real-time view of physical and digital infrastructure, minimizing engineering risks and improving decision-making in complex, sensor-driven environments. This positions AI and digital twins as core enablers of next-generation, autonomous water treatment systems.

Water and Wastewater Treatment Technologies Market Share and Segmentation Insights

Technology Market Share: Biological Treatment Leads with Cost-Effective and Sustainable Wastewater Processing

Biological treatment holds a 32.80% share in the water and wastewater treatment technologies market in 2025, driven by its efficiency in removing organic pollutants, nutrients, and pathogens through processes such as activated sludge, MBBR, MBR, and anaerobic digestion. Its cost-effectiveness and sustainability make it the preferred choice for large-scale municipal and industrial wastewater treatment. Membrane technology, chemical treatment, physical and mechanical treatment, and advanced oxidation processes complement treatment systems for specific requirements. A key trend is the transition toward resource recovery, where biological systems are optimized for biogas generation, nutrient recovery, and water reuse, supporting circular water management strategies.

Application Market Share: Municipal Water Treatment Leads with Infrastructure Expansion and Water Reuse Initiatives

Municipal water treatment accounts for 48.60% of the market in 2025, reflecting the large-scale demand for drinking water supply and wastewater management in urban populations. Industrial water treatment and desalination contribute to additional demand across sectors facing water stress and regulatory compliance requirements. A key growth driver is the expansion of water reuse initiatives, where municipalities invest in advanced treatment technologies such as membrane bioreactors, reverse osmosis, and UV-based systems to produce high-quality reclaimed water. Increasing urbanization, aging infrastructure, and stringent environmental regulations continue to drive investment in municipal water treatment systems globally.

Water and Wastewater Treatment Technologies Market Competitive Landscape

The Water and Wastewater Treatment Technologies market in 2026 is defined by digital twin integration, energy-neutral wastewater treatment, and direct potable reuse systems, with advanced membrane chemistry and AI-driven optimization enabling operational resilience, leakage control, and high-efficiency water recovery across municipal and industrial sectors.

Veolia Leads Digital-Integrated Desalination and Industrial Water Reuse Systems

Veolia is strengthening its leadership in the Water and Wastewater Treatment Technologies market through full ownership of its Water Technologies and Solutions unit and large-scale desalination and reuse projects. Its Barrel™ modular desalination systems deployed in Mumbai and Chile reduce energy consumption and infrastructure footprint. The SATORP industrial recycling project highlights its capability in treating high-complexity effluents for reuse. A €2.5 billion bond issuance supports its GreenUp strategy focused on high-growth sectors such as semiconductor-grade water. The Hubgrade™ platform manages over 8,500 sites globally, delivering up to 15% operational savings through AI-driven optimization. This integration of digital platforms and physical infrastructure enhances Veolia’s position in resource recovery.

Xylem Expands AI-Driven Water Management for Data Centers and Smart Infrastructure

Xylem Inc. is advancing its position in the Water and Wastewater Treatment Technologies market through AI-enabled digital platforms and large-scale infrastructure solutions. The company reported $8.5 billion in revenue with strong growth in smart metering systems. Its strategy targets the rapidly growing water demand from data centers, focusing on closed-loop cooling and high-purity water systems. Expansion of manufacturing hubs in Gujarat improves supply chain efficiency for South Asian projects. The Xylem Vue platform enables AI-based wastewater optimization, reducing energy consumption by up to 25%. This focus on digitalization and high-growth verticals strengthens its leadership in smart water management.

SUEZ Strengthens Municipal Water Infrastructure with Digital Concessions and Circular Solutions

SUEZ is reinforcing its role in the Water and Wastewater Treatment Technologies market through concession-based infrastructure management and circular resource recovery solutions. The €456 million Salem project involves large-scale pipeline rehabilitation and digitization to reduce non-revenue water by 20%. Its deployment of Dehydris™ Twist units in Hong Kong supports compact wastewater treatment in space-constrained environments. Investment in solvent recovery facilities in China highlights its transition toward waste-to-resource models. SUEZ’s ability to manage the entire water lifecycle provides municipalities with integrated ESG and carbon compliance solutions. This concession-driven model enhances long-term operational resilience.

DuPont Water Solutions Drives Advanced Membrane Technologies for Energy Transition Applications

DuPont is a global leader in the Water and Wastewater Treatment Technologies market through its advanced membrane and ion exchange solutions. The WAVE PRO platform integrates multiple treatment technologies into a unified digital design environment, improving system optimization. Its AmberLite™ P2X110 resin supports green hydrogen production by withstanding extreme operating conditions in PEM electrolyzers. FilmTec™ LiNE-XD membranes enable lithium extraction from brines, supporting EV battery supply chains. The Sustainability Navigator tool provides carbon footprint analysis for water treatment processes. This focus on materials science and digital modeling positions DuPont at the forefront of energy transition water solutions.

Kurita Water Industries Expands Recurring Ultrapure Water Services for Semiconductor Manufacturing

Kurita Water Industries is strengthening its competitive position in the Water and Wastewater Treatment Technologies market through recurring service models and ultrapure water solutions. Growth in maintenance and service contracts has driven a 10.1% increase in business profit, reflecting demand for outsourced water management. Its CSV business emphasizes water conservation and waste reduction, aligning with strict environmental regulations. Kurita is expanding precision tool cleaning services for semiconductor manufacturing, integrating water recycling into critical processes. Its “Chemistry-as-a-Service” model combines treatment chemicals with engineering expertise for continuous water quality control. This service-oriented approach enhances its role in mission-critical industrial applications.

Saudi Arabia Water and Wastewater Treatment Technologies Market Anchored in Industrial Reuse and Non-Conventional Water Systems

Saudi Arabia’s water and wastewater treatment technologies market is undergoing a structural transformation driven by industrial circularity, desalination resilience, and national sustainability programs. In September 2025, a consortium led by Veolia, Marafiq, and Lamar signed a landmark agreement with SATORP to deliver the Middle East’s largest industrial wastewater reuse facility in Jubail. Valued at approximately $500 million, the project will recycle 8.8 million cubic meters of complex petrochemical effluents annually, positioning advanced tertiary and quaternary treatment as core industrial infrastructure rather than environmental compliance add-ons. This development reflects Saudi Arabia’s strategic pivot toward closed-loop water systems within energy and chemicals clusters.

Non-conventional water resources are gaining parallel momentum. In early 2026, the Saudi Water Authority awarded a contract for a 50 MLD brackish water reverse osmosis plant in Aljouf, integrating ceramic membrane pre-treatment to manage raw water containing rare elements and fouling-prone compounds. Under the Saudi Green Initiative, treated wastewater is also being scaled for productive reuse, including irrigation of four million lemon trees to enhance food self-sufficiency by 2030. Institutional cooperation is reinforcing digital adoption. A December 2025 memorandum of understanding between the Saudi Water Authority and the Singapore Water Association aims to accelerate deployment of digital twins and smart water systems across arid urban centers, strengthening operational resilience.

India Water and Wastewater Treatment Technologies Market Driven by Digitalization and Green Hydrogen Demand

India’s water and wastewater treatment technologies market is expanding rapidly, supported by multilateral financing, industrial decarbonization, and large-scale public–private investment pipelines. In October 2025, European Investment Bank issued its first water-dedicated loan to India, totaling $191 million, to modernize infrastructure in Uttarakhand. The program emphasizes continuous leak detection, automated meter reading, and treatment plant automation, directly supporting digital twins and real-time system optimization for utilities serving nearly 900,000 residents.

Industrial demand is intensifying due to energy transition policies. Under the National Green Hydrogen Mission, India is commissioning over 1,500 MW of electrolyzer manufacturing capacity by August 2026 through the SIGHT program. This has sharply increased requirements for ultra-pure water systems, where advanced reverse osmosis, electrodeionization, and polishing technologies are mission critical for electrolyzer performance. Investment visibility remains strong. The India Investment Grid reported more than 550 active water treatment projects valued at over $60 billion in late 2025, largely structured as public–private partnerships. Additionally, the extension of the Fortified Rice Scheme is indirectly increasing demand for high-purity process water in agro-processing, linking nutrition policy with industrial water treatment upgrades.

European Union Water and Wastewater Treatment Technologies Market Reshaped by Quaternary Treatment and Energy Neutrality

The European Union water and wastewater treatment technologies market is entering a compliance-driven innovation cycle, with Germany and France at the forefront of advanced treatment deployment. The Recast Urban Wastewater Treatment Directive (EU 2024/3019) entered into force in 2025, with first compliance milestones in 2026 mandating quaternary treatment capable of removing at least 80% of micropollutants such as pharmaceuticals and cosmetics in large agglomerations. This requirement is accelerating adoption of advanced oxidation processes, activated carbon adsorption, and membrane polishing across municipal systems.

Cost allocation mechanisms are reshaping procurement behavior. By 2028, the directive introduces extended producer responsibility, requiring pharmaceutical and cosmetic manufacturers to cover at least 80% of the costs associated with quaternary treatment upgrades. This policy is incentivizing utilities to select scalable, modular technologies with predictable operating costs. Energy performance is another strategic axis. Facilities serving more than 10,000 population equivalents must achieve energy neutrality by 2045 through biogas recovery and integrated renewables. In France, modernization initiatives are already underway. In March 2025, Veolia and SIAAP inaugurated a new primary settling unit at the Seine Aval facility, combining high-performance clarification with carbon capture and valorization, signaling the convergence of wastewater treatment and climate mitigation infrastructure.

United States Water and Wastewater Treatment Technologies Market Focused on Semiconductors and PFAS Mitigation

The United States water and wastewater treatment technologies market is being shaped by semiconductor manufacturing expansion and tightening drinking water regulations. Driven by the CHIPS Act, advanced fabrication facilities are deploying treat, recover, and reuse models that prioritize water circularity and upstream contaminant recovery. Technology providers such as ElectraMet are scaling electrochemical systems capable of neutralizing high-strength peroxide streams and recovering valuable metals before conventional membrane treatment, reducing both water footprint and waste loads.

Regulatory pressure is reinforcing municipal investment. Following the Environmental Protection Agency final rule on PFAS in drinking water, utilities in 2025 have accelerated deployment of specialty ion-exchange resins and granular activated carbon systems to meet stringent limits. Resource recovery is also gaining prominence. In May 2025, Veolia installed MemGas membrane technology at San Francisco’s largest wastewater facility, upgrading biogas to pipeline-quality renewable natural gas. This project exemplifies the shift toward energy-positive wastewater plants that integrate treatment, recovery, and decarbonization.

Brazil Water and Wastewater Treatment Technologies Market Advancing Industrial Water Neutrality

Brazil’s water and wastewater treatment technologies market is increasingly aligned with industrial water neutrality and offshore energy requirements. In 2025, PetStar and Rhodia partnered with international technology providers to achieve 94% water reuse at textile and PET recycling operations in São Paulo. These projects utilize advanced effluent-to-process-water conversion systems, positioning water reuse as a competitiveness lever rather than a regulatory obligation.

Energy-sector applications add another demand layer. In June 2025, Petrobras secured contracts for advanced seawater desalination units on floating production storage and offloading platforms in the Santos Basin. These systems are designed to protect reservoirs and maintain injection water quality under harsh offshore conditions. Collectively, Brazil’s market is characterized by targeted, high-impact deployments that link water stewardship with industrial efficiency and energy security.

Summary of Country-Level Water and Wastewater Treatment Technologies Market Dynamics

Water and Wastewater Treatment Technologies Market County Level Snapshot

|

Country / Region

|

Primary Strategic Driver

|

Key Technology Focus

|

Market Positioning

|

|

Saudi Arabia

|

Industrial circularity and non-conventional water

|

Reuse plants, BWRO, digital twins

|

Flagship large-scale reuse hub

|

|

India

|

Digital utilities and green hydrogen

|

UPW systems, automation, PPP plants

|

Rapidly scaling infrastructure market

|

|

European Union

|

Quaternary treatment mandates

|

AOP, activated carbon, energy recovery

|

Compliance-led innovation benchmark

|

|

United States

|

Semiconductor fabs and PFAS rules

|

Reuse systems, ion exchange, GAC

|

Technology-intensive upgrade market

|

|

Brazil

|

Industrial water neutrality and offshore needs

|

Reuse, desalination

|

Selective high-impact deployment market

|

Water and Wastewater Treatment Technologies Market Report Scope

Water and Wastewater Treatment Technologies Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$40.8 Billion

|

|

Market Size (2034)

|

$67.8 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Technology (Membrane Technology, Biological Treatment, Chemical Treatment, Advanced Oxidation Processes, Physical and Mechanical Treatment), By Application (Municipal Water Treatment, Industrial Water Treatment, Desalination), By Service and Integration (Digital Water Solutions, Resource Recovery Systems, Mobile Water Services)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia Group, Suez SA, Xylem Inc., DuPont Water Solutions, Ecolab Inc., Pentair plc, Aquatech International LLC, VA Tech WABAG Ltd., Kurita Water Industries Ltd., Evoqua Water Technologies, Saur Group, Acciona Agua, IDE Technologies, Toshiba Water Solutions, Koch Separation Solutions

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water and Wastewater Treatment Technologies Market Segmentation

By Technology

Reverse Osmosis

Ultrafiltration

Microfiltration

Nanofiltration

- Biological Treatment

- Chemical Treatment

- Advanced Oxidation Processes

- Physical and Mechanical Treatment

By Application

- Municipal Water Treatment

- Industrial Water Treatment

- Desalination

By Service and Integration

- Digital Water Solutions

- Resource Recovery Systems

- Mobile Water Services

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Water and Wastewater Treatment Technologies Market

- Veolia Group

- Suez SA

- Xylem Inc.

- DuPont Water Solutions

- Ecolab Inc.

- Pentair plc

- Aquatech International LLC

- VA Tech WABAG Ltd.

- Kurita Water Industries Ltd.

- Evoqua Water Technologies

- Saur Group

- Acciona Agua

- IDE Technologies

- Toshiba Water Solutions

- Koch Separation Solutions

*- List not Exhaustive