Water Based Pigments Market Overview 2025–2034: $11 Billion to $19.9 Billion at 6.8% CAGR Fueled by Sustainable Automotive Coatings and High-Stability Dispersions

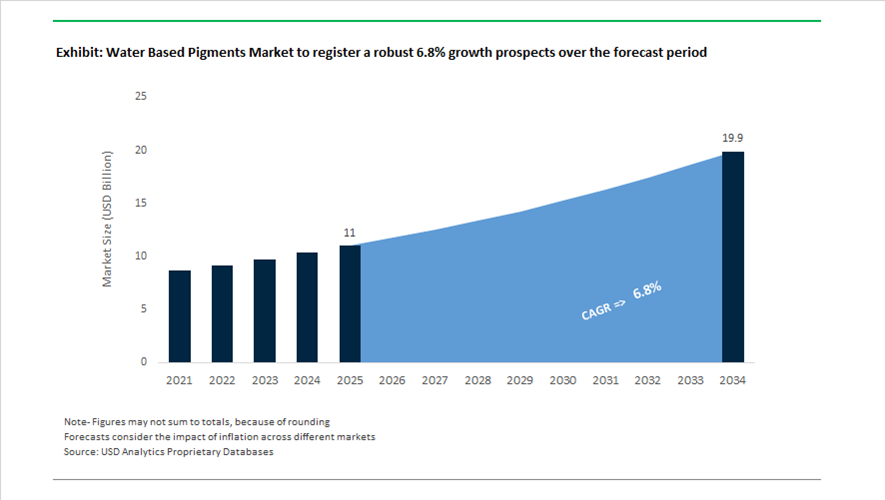

The Water Based Pigments market is valued at $11 billion in 2025 and is projected to reach $19.9 billion by 2034, registering a CAGR of 6.8%. Growth is driven by accelerating adoption of waterborne coatings, low-VOC pigment dispersions, eco-friendly architectural paints, water-based automotive finishes, and sustainable printing inks. Regulatory pressure on solvent emissions across Europe, North America, and Asia-Pacific is reshaping pigment formulation strategies, pushing manufacturers toward high-performance water-compatible organic and inorganic pigments with improved dispersion stability, color strength, and weather resistance. Innovation is centered on enhanced pigment wetting agents, mineral-oil-free systems, bio-attributed raw materials, and metallic/interference pigments engineered specifically for water-based systems.

In 2024, product-level innovation focused on dispersion stability and regulatory compliance. In March 2024, BYK, part of Altana Group, initiated construction of a €25 million innovation and laboratory complex in Wesel dedicated to next-generation additives for stabilizing complex pigments in fully water-based and UV-curable systems. In early 2024, Heubach expanded its Colanyl® 500 pigment preparations with Orange H5GD 500, designed to resolve stability challenges associated with Pigment Orange 62 in waterborne architectural coatings. In December 2024, ECKART, an ALTANA company, launched the TOPSTAR SuperEco 16 series, mineral-oil-free metallic pigments compatible with water-based printing inks and aligned with stringent 2025 French packaging regulations. These developments reflect a market transition toward waterborne dispersion robustness, regulatory-safe formulations, and high-performance metallic effects without solvent dependency.

Strategic consolidation reshaped global competitive dynamics in 2025. In March 2025, Sudarshan Chemical Industries Limited completed the acquisition of the Heubach Group, creating a global pigment platform with 19 production sites and integrating legacy Clariant and Heubach portfolios. This transaction significantly expands Sudarshan’s footprint in water-based pigment dispersions, effect pigments, and architectural colorants. In October 2025, BASF Coatings introduced its 2025–2026 Automotive Color Trends collection, including Tesseract Blue, a water-based interference pigment formulation engineered for multidimensional surface effects across EMEA automotive OEM coatings. In November 2025, Sun Chemical expanded Perylene pigment capacity at its Ludwigshafen site to meet rising demand for high-performance reds and blacks in waterborne automotive and industrial coatings. At CHINACOAT 2025, Sun Chemical also debuted Paliocrom® Premium Orange L 2900, a high-chroma aluminum effect pigment optimized for both solventborne and waterborne systems, targeting premium automotive finishes.

Sustainability positioning intensified in 2025–2026. At the European Coatings Show 2025, LANXESS introduced Scopeblue variants of its Bayferrox yellow iron oxide pigments for waterborne facade paints, reporting a 35% lower carbon footprint through eco-efficient sourcing. In January 2026, DIC Corporation implemented a global organizational reform to streamline its Color & Comfort division and accelerate deployment of sustainable waterborne pigment dispersions following integration of the BASF Colors & Effects business. In February 2026, Sun Chemical launched Glacier™ Exterior Ceramic White S1303M at PaintIndia, a waterborne-compatible transparent synthetic mica pigment delivering high-purity white shades with satin effects for architectural and automotive coatings. Earlier portfolio integration efforts, including the May 2024 acquisition of LUBCON by FUCHS Group, introduced advanced additive technologies that enhance dispersion stability in high-performance water-based industrial coatings.

The water based pigments market is evolving toward high-chroma effect pigments, mineral-oil-free metallics, low-carbon iron oxides, advanced perylenes, and robust dispersion chemistries designed for 100% waterborne and hybrid UV systems. Automotive OEM coatings, architectural facade paints, industrial protective finishes, and sustainable packaging inks remain the primary growth engines supporting expansion through 2034.

Trends and Opportunities in the Water-Based Pigments Market

Trends and Opportunities Reshaping the Global Water-Based Pigments Market

The water-based pigments market is undergoing a structural transformation driven by OEM-level decarbonization mandates, circular packaging regulations, and tightening safety standards across consumer-facing applications. In 2025, growth is no longer anchored in basic environmental compliance alone; instead, it is defined by high-performance reformulation, verified recyclability, and purity-driven differentiation. Water-based pigments are increasingly specified at the formulation design stage by automotive OEMs, global CPG brands, and institutional buyers, making performance parity with solvent-based systems a non-negotiable requirement rather than a future aspiration.

Trend 1: High-Performance Reformulation for Automotive and Industrial OEM Coatings

Global automotive and industrial OEMs are accelerating the transition toward fully waterborne basecoat and primer systems, directly increasing demand for advanced water-based pigments that can deliver metallic brilliance, corrosion resistance, and long-term durability under extreme operating conditions. This shift is tightly linked to lifecycle emissions reduction targets, as solvent-borne coatings are being phased out to meet plant-level VOC and Product Carbon Footprint thresholds.

In November 2025, BASF commissioned a dedicated high-performance dispersant production line in Nanjing, China, utilizing Controlled Free Radical Polymerization (CFRP) technology. This investment is strategically aligned with the automotive and industrial coatings sectors, enabling pigment dispersions that achieve narrower particle size distribution, enhanced stability, and lower resin demand in water-based formulations. These dispersants allow OEMs to expand color gamut and effect pigments while simultaneously reducing energy consumption during application and curing.

On the pigment side, DIC Corporation and Sun Chemical introduced Paliocrom® Brilliant Ruby L 3558 in late 2025, a waterborne-compatible effect pigment engineered for premium automotive finishes. The pigment delivers exceptional hiding power and chromatic depth while maintaining stability in aqueous systems. Importantly, its adoption enables automotive manufacturers to reduce hazardous air pollutant emissions by up to 90% compared to solvent-based metallic pigments, without sacrificing the “liquid metal” aesthetic increasingly favored in EV and premium vehicle segments.

Trend 2: Mainstreaming Water-Based Pigment Inks for Circular Packaging Systems

Circular economy mandates from global CPG companies are accelerating the replacement of solvent-based inks with water-based pigment inks across flexible and rigid packaging formats. In 2025, recyclability and de-inkability have become contractual requirements rather than sustainability add-ons, particularly for brands operating under heightened scrutiny from “Green Claims” regulations in the EU and comparable frameworks in North America.

A major inflection point occurred in January 2025 when Siegwerk launched an NC-free, water-based surface ink system for polyolefin packaging. These inks are engineered to be fully de-inkable during mechanical recycling, enabling higher-quality plastic recyclates suitable for closed-loop, bottle-to-bottle applications. This addresses one of the primary historical limitations of pigment-based inks, where contamination previously downgraded recyclate value.

Simultaneously, BASF’s Joncryl® BRC series, highlighted in October 2025, integrates biomass-balanced content into water-based resins used for pigment inks. Independent lifecycle assessments show that these formulations reduce CO2 emissions by approximately 25 to 30% compared to conventional petrochemical systems. This innovation directly supports the 2030 Net Zero packaging commitments of multinational brand owners such as Nestlé and Unilever, positioning water-based pigments as a strategic enabler of compliant packaging transformation rather than a cost center.

Opportunity 1: Scaling Eco-Friendly Digital Textile Pigment Printing

Digital textile pigment printing represents one of the most disruptive growth opportunities for water-based pigments, particularly as fashion brands confront water scarcity, inventory risk, and supply chain volatility. Unlike reactive or disperse dyeing, digital pigment printing relies on water-based pigment inks that are fixed through heat curing, eliminating the need for water-intensive steaming and washing processes.

Sustainability briefings released in February 2025 indicate that digital pigment printing reduces water consumption in textile production by nearly 95% compared to conventional dyeing methods. This dramatic reduction is driving rapid adoption among apparel manufacturers seeking compliance with regional water-use restrictions and ESG reporting requirements, especially in water-stressed production hubs across South Asia.

Technological progress is addressing earlier performance limitations. Kao Corporation’s LUNAJET® pigment nano-dispersion technology enables high jet stability and color consistency at industrial print speeds, even on non-absorbent or blended fabrics. This capability supports on-demand, near-market manufacturing models that reduce overproduction and markdown losses, making water-based pigment inks a cornerstone technology for next-generation, low-waste fashion supply chains.

Opportunity 2: High-Purity Water-Based Pigments for Safety-Critical Art and Therapeutic Applications

Stricter safety standards in educational, pediatric, and therapeutic art materials are creating a premium niche for ultra-pure water-based pigments with validated toxicological profiles. Regulatory frameworks such as ASTM D4236 and EN 71-3 are increasingly enforced through procurement audits, particularly by institutional buyers including schools, hospitals, and care facilities.

The 2025 update to the EU Toy Safety Directive introduced tighter limits on isothiazolinone preservatives in water-based paints, compelling manufacturers to adopt high-purity aqueous pigment dispersions stabilized with green chemistry alternatives. Compliance with these requirements enables products to carry the ACMI “AP” Non-Toxic seal, which has become a baseline qualification for institutional purchasing.

According to Toxic-Free Future reports published in 2025, institutional buyers are actively auditing pigment formulations for heavy metal content, driving demand for inorganic-free organic pigments that eliminate exposure risks associated with lead and cadmium. This trend is particularly pronounced in therapeutic art programs and special education settings, supporting a high-margin opportunity within the $3.8 billion global educational and institutional art supplies market.

Water Based Pigments Market Share and Segmentation Insights

Product Type Market Share: Inorganic Pigments Lead with Opacity, Durability, and TiO₂ Optimization

Inorganic pigments account for 48.60% of the water based pigments market in 2025, driven by their superior opacity, weather resistance, and thermal stability in architectural paints and industrial coatings. Titanium dioxide, iron oxides, and carbon black remain essential for high-performance, cost-effective color formulations. Organic pigments and specialty effect pigments serve premium and niche applications requiring enhanced color vibrancy or visual effects. A key trend is TiO₂ dispersion optimization, where advanced surface treatments and grinding technologies enable stable, high-loading aqueous dispersions with improved color development and rheology, simplifying formulation for water-based coatings and enhancing performance consistency.

End-Use Industry Market Share: Building and Construction Leads with Architectural Coatings and Green Building Standards

Building and construction hold a 42.80% share in the water based pigments market in 2025, supported by the large-scale use of water-based architectural paints in residential and commercial infrastructure. Packaging and labeling, automotive and transportation, and consumer goods sectors contribute additional demand across coatings and printing applications. A key growth driver is the adoption of green building standards such as LEED and BREEAM, where low-VOC materials are required, accelerating the shift toward water-based pigment systems. Manufacturers are developing pigment solutions that meet durability, color stability, and environmental compliance requirements for high-performance sustainable coatings.

Water Based Pigments Market Competitive Landscape

The Water Based Pigments market in 2026 is defined by formula cleanliness, functional pigment integration, and precision aesthetics, with innovations in NIR-detectability, solar heat management, and low-VOC dispersions enabling sustainable coatings for automotive, packaging, and architectural applications.

DIC Corporation Accelerates Digital Sustainability with High-Performance Effect Pigments

DIC Corporation, through Sun Chemical, is strengthening its leadership in the Water Based Pigments market with advanced effect pigments and digital sustainability tools. The Glacier™ Exterior Ceramic White S1303M introduces synthetic mica-based dispersion optimized for high-luster, pure white waterborne coatings. Its 3AH3809W water-based coating system targets extreme environments such as photovoltaic frames and EV battery enclosures with high chemical resistance. Integration of Product Carbon Footprint data into the Pigment Finder platform enables real-time sustainability tracking for formulators. Continued investment in perylene pigment capacity ensures supply stability amid regulatory pressure on phthalocyanines. This combination of performance chemistry and digital transparency enhances its competitive positioning.

Sudarshan Chemical Scales Global Pigment Leadership with Circular and Compostable Solutions

Sudarshan Chemical Industries has emerged as a global powerhouse in the Water Based Pigments market following the integration of Heubach’s international assets. The addition of 19 manufacturing sites strengthens its capabilities in high-performance pigments and complex inorganic colored pigments. Its OK Compost-certified Sudaperm and Sudafast ranges support biodegradable packaging applications. The company’s NIR-detectable black pigments improve automated plastic sorting, addressing recycling inefficiencies in water-based coatings. Structural optimization initiatives streamline operations toward high-growth APAC and European markets. This focus on responsible color chemistry and circularity reinforces its global competitiveness.

BASF Advances Automotive Aesthetic Innovation with Water-Compatible Interference Pigments

BASF SE is leading the Water Based Pigments market through advanced interference pigments and sustainable coating technologies. Its “Driving the Proxy” collection introduces TESSERACT BLUE, delivering multi-angle color shifts for high-end automotive finishes. The PHYGITAL MAGNETAR system utilizes water-based two-coat technology to create liquid-metal visual effects with reduced environmental impact. BASF is integrating renewable and recycled feedstocks into pigment dispersions to support green transformation goals. The Zhanjiang Verbund site enhances cost efficiency and supply chain integration for pigment precursors. This focus on emotional design and sustainable chemistry strengthens BASF’s leadership in premium coatings.

Clariant Enhances High-Purity Water-Based Pigments with Digital Traceability and Bio-Based Inputs

Clariant is reinforcing its position in the Water Based Pigments market through high-purity formulations and digital supply chain transparency. The CHF 80 million expansion at Daya Bay increases capacity for ethylene oxide derivatives used in pigment stabilization. Operational efficiency programs have generated significant cost savings, enabling reinvestment into bio-based surfactant R&D. Its top-tier CDP rating strengthens its appeal among ESG-focused multinational customers. The CLARITY™ platform provides real-time footprint tracking, enabling clients to reduce emissions through optimized pigment systems. This integration of sustainability, digitalization, and performance chemistry enhances Clariant’s competitive advantage.

Heubach Strengthens Functional Waterborne Pigment Systems with Anti-Corrosive and POS Innovations

Heubach, now part of Sudarshan, continues to define technical standards in the Water Based Pigments market through advanced waterborne systems. The HEUCOTINT™ W range offers VOC- and APEO-free colorants for architectural coatings, supporting regulatory compliance. Its HEUCOFLASH™ line provides waterborne anti-corrosive pigments that prevent flash rust during drying in acrylic and epoxy systems. Automotive styling innovations include LIDAR-reflective pigments for autonomous vehicle detection. The brand’s local-for-local manufacturing strategy reduces logistics emissions while ensuring supply reliability. This focus on functional performance and localized production strengthens its position in industrial coatings.

India Water Based Pigments Market Repositioned as a Global Manufacturing and Consolidation Engine

India has emerged as the structural center of gravity for the global water based pigments market following a wave of consolidation, policy alignment, and cost-driven manufacturing realignment. The defining inflection point was the October 2024 acquisition of the global operations of Heubach Group by Sudarshan Chemical Industries Limited for approximately ₹1,180 crore. By early 2025, this transaction had triggered a deliberate shift of commodity pigment and intermediate production from Germany to India, leveraging lower operating costs, scale efficiencies, and proximity to fast-growing end markets. Post-acquisition, Indian facilities are being positioned as the global backbone for water-borne pigment dispersions, while European assets are converted into specialty and customer-facing centers.

Regulatory and policy drivers are reinforcing this manufacturing pivot. The rollout of the Indian Carbon Credit Trading Scheme during 2025 is incentivizing pigment producers to accelerate adoption of aqueous pigment systems to reduce Scope 1 emissions, particularly in textiles and architectural coatings. Parallel demand-side support is emerging from food security programs. The government’s fortified rice mandate, backed by a ₹17,082 crore allocation, has increased demand for food-grade water based pigments used in labeling and grain-marking, where low toxicity and regulatory compliance are non-negotiable. Under the NITI Aayog Chemicals 2030 roadmap, operating subsidies are being extended for domestic synthesis of water-based azo pigments, targeting a 15% reduction in imported precursors by 2026. Product innovation is keeping pace, with Indian manufacturers securing 2025 approvals for high-performance pigments such as Yellow H4G and Red F5RK-IN for the two-wheeler automotive refinish segment, strengthening India’s position across both value and performance tiers.

China Water Based Pigments Market Accelerated by VOC Controls and NEV Coatings Demand

China’s water based pigments market is being reshaped by stricter environmental standards and rapid innovation in automotive and electronics coatings. Under the 14th Five-Year Plan, 2025 directives imposed a mandatory 20% reduction in volatile organic compound emissions in clusters such as Zhejiang, accelerating the transition from solvent-based inks to water-borne dispersions across packaging and stationery applications. This regulatory push is translating directly into higher adoption of aqueous pigment concentrates with improved dispersion stability and color strength.

Industrial innovation remains a core differentiator. At ChinaCoat 2025, global leaders including DIC and Sun Chemical highlighted localized production of advanced water-based binders and pigment systems such as WATERSOL UD-5002 for in-mold decoration films, enabling flawless metallic pigment orientation. Automotive and energy transition applications are expanding rapidly. New water-based acrylic systems tailored for New Energy Vehicle battery packs and photovoltaic panel frames were unveiled, reflecting rising demand for corrosion-resistant, low-VOC coatings in electrified mobility. Effect pigments are also gaining traction. In November 2025, Sun Chemical premiered Glacier Exterior Ceramic White S1303M in Shanghai, a synthetic mica pearl pigment optimized for cool sparkle effects in waterborne industrial coatings. Collectively, China’s market is evolving from volume-driven output toward application-specific, regulation-compliant water based pigment solutions.

Germany Water Based Pigments Market Defined by Sensor Compatibility and Sustainability Reset

Germany’s water based pigments market is undergoing a strategic reset driven by automotive technology shifts and corporate restructuring. At the European Coatings Show 2025, ECKART, part of the Altana Group, introduced SILVERSHINE Hydro Platinum, a radar-transparent water-based pigment paste designed specifically for autonomous driving sensors. These pigments allow metallic-look coatings to coexist with advanced driver-assistance systems, highlighting Germany’s leadership in functional pigment innovation rather than commodity volumes.

Corrosion protection remains another focus area. In early 2025, ECKART launched ProFLAKE Zn HYDRO PM 3090, the first zinc flake pigment engineered exclusively for water-based systems, targeting heavy-duty industrial coatings with enhanced rust resistance. Structural change has also redefined the competitive landscape. The 2024 insolvency of Heubach Colorants Germany and its subsequent acquisition by Sudarshan Chemical marked the end of a two-century independent German pigment lineage. German producers are now emphasizing sustainability upgrades, including a shift toward AL-II metallic pigments made from secondary aluminum, cutting carbon intensity per ton by an estimated 25%. Germany’s role is thus transitioning toward high-value, technology-led water based pigment development aligned with automotive safety and sustainability mandates.

United States Water Based Pigments Market Shaped by PFAS Regulation and Digital Printing Growth

The United States water based pigments market is being reshaped by chemical regulation and demand from digital printing and consumer packaging. In 2025, final rules issued by the Environmental Protection Agency targeting persistent chemicals accelerated the withdrawal of fluorinated surfactants from aqueous pigment dispersions. This regulatory shift is forcing pigment formulators to adopt polymeric dispersants and bio-based alternatives, particularly in applications requiring high washability and durability.

Innovation in carbon black and specialty pigments is supporting this transition. Orion Engineered Carbons introduced circular carbon black grades derived from pyrolysis oils for water-based systems, targeting high-jetness digital ink applications while aligning with long-term net-zero emissions goals. Demand from direct-to-consumer ecommerce has further strengthened the market. Rising shipment volumes have increased requirements for high-purity, water-based inks used in food packaging and toy labeling, where compliance with EU Article 3 standards is critical for U.S. exporters. The U.S. market is therefore characterized by regulation-driven reformulation coupled with premiumization in digital and safety-sensitive applications.

Switzerland Water Based Pigments Market Focused on Bio-Innovation and Specialty Positioning

Switzerland’s water based pigments market is narrowing its focus toward specialty innovation following strategic restructuring within its chemical sector. After Clariant’s divestment and restructuring phase during 2024–2025, Swiss stakeholders retained a minority stake in the Heubach–Sudarshan entity, positioning themselves to benefit from global pigment growth without direct exposure to capital-intensive manufacturing. This strategic retreat has allowed Swiss players to concentrate on higher-margin segments within care chemicals and natural resources.

Bio-based pigment innovation is emerging as a distinctive theme. Swiss biotechnology startups are collaborating with established industry partners to develop indigo and quinacridone pigments via bacterial fermentation. These precision-fermentation pigments are targeted at luxury water-based textile inks, where traceability, sustainability, and color consistency command pricing power. Switzerland’s contribution to the global water based pigments market is therefore increasingly defined by upstream innovation and specialty chemistry rather than production scale.

Summary of Country-Level Water Based Pigments Market Dynamics

Water Based Pigments Market County Level Snapshot

Country

Strategic Driver

Key Application Focus

Market Positioning

India

Global consolidation and cost-efficient manufacturing

Textiles, coatings, food labeling

Global production and dispersion hub

China

VOC mandates and NEV growth

Automotive, packaging, effect pigments

Regulation-led innovation scale

Germany

Autonomous mobility and sustainability

Radar-compatible and anticorrosive coatings

High-performance technology leader

United States

PFAS regulation and digital inks

Packaging, digital printing, toys

Premium reformulation-driven market

Switzerland

Specialty restructuring and bio-pigments

Luxury textiles, sustainable inks

Innovation and fermentation pioneer

Water Based Pigments Market Report Scope

Water Based Pigments Market

Parameter

Details

Market Size (2025)

$11 Billion

Market Size (2034)

$19.9 Billion

Market Growth Rate

6.8%

Segments

By Product Type (Inorganic Pigments, Organic Pigments, Specialty and Effect Pigments), By Dispersion Type (Resin-Free Dispersions, Resin-Based Dispersions, Micro-Encapsulated Pigments), By Application (Paints and Coatings, Printing Inks, Textiles, Plastics and Rubber, Personal Care), By End-Use Industry (Building and Construction, Automotive and Transportation, Packaging and Labeling, Consumer Goods and Electronics)

Study Period

2019- 2025 and 2026-2034

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Water Based Pigments Market Segmentation

By Product Type

Inorganic Pigments

Organic Pigments

Specialty and Effect Pigments

By Dispersion Type

Resin-Free Dispersions

Resin-Based Dispersions

Micro-Encapsulated Pigments

By Application

Paints and Coatings

Printing Inks

Textiles

Plastics and Rubber

Personal Care

By End-Use Industry

Building and Construction

Automotive and Transportation

Packaging and Labeling

Consumer Goods and Electronics

By Region

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

2. Water Based Pigments Market Landscape & Outlook (2025–2034)

2.1. Introduction to Water Based Pigments Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Low-VOC Regulations and Waterborne Coatings Adoption

2.4. Dispersion Stability, High-Performance Pigments, and Metallic Effects

2.5. Sustainable Raw Materials and Mineral-Oil-Free Formulations

3. Innovations Reshaping the Water Based Pigments Market

3.1. Trend: High-Performance Reformulation for Automotive and Industrial Coatings

3.2. Trend: Water-Based Pigment Inks for Circular Packaging Systems

3.3. Opportunity: Digital Textile Pigment Printing and Water Reduction

3.4. Opportunity: High-Purity Pigments for Safety-Critical Applications

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Water Based Pigments Market

5.1. By Product Type

5.1.1. Inorganic Pigments

5.1.2. Organic Pigments

5.1.3. Specialty and Effect Pigments

5.2. By Dispersion Type

5.2.1. Resin-Free Dispersions

5.2.2. Resin-Based Dispersions

5.2.3. Micro-Encapsulated Pigments

5.3. By Application

5.3.1. Paints and Coatings

5.3.2. Printing Inks

5.3.3. Textiles

5.3.4. Plastics and Rubber

5.3.5. Personal Care

5.4. By End-Use Industry

5.4.1. Building and Construction

5.4.2. Automotive and Transportation

5.4.3. Packaging and Labeling

5.4.4. Consumer Goods and Electronics

5.5. By Region

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. South and Central America

5.5.5. Middle East and Africa

6. Country Analysis and Outlook of Water Based Pigments Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Water Based Pigments Market Size Outlook by Region (2025-2034)

7.1. North America Water Based Pigments Market Size Outlook to 2034

7.1.1. By Product Type

7.1.2. By Dispersion Type

7.1.3. By Application

7.1.4. By End-Use Industry

7.1.5. By Region

7.2. Europe Water Based Pigments Market Size Outlook to 2034

7.2.1. By Product Type

7.2.2. By Dispersion Type

7.2.3. By Application

7.2.4. By End-Use Industry

7.2.5. By Region

7.3. Asia Pacific Water Based Pigments Market Size Outlook to 2034

7.3.1. By Product Type

7.3.2. By Dispersion Type

7.3.3. By Application

7.3.4. By End-Use Industry

7.3.5. By Region

7.4. South America Water Based Pigments Market Size Outlook to 2034

7.4.1. By Product Type

7.4.2. By Dispersion Type

7.4.3. By Application

7.4.4. By End-Use Industry

7.4.5. By Region

7.5. Middle East and Africa Water Based Pigments Market Size Outlook to 2034

7.5.1. By Product Type

7.5.2. By Dispersion Type

7.5.3. By Application

7.5.4. By End-Use Industry

7.5.5. By Region

8. Company Profiles: Leading Players in the Water Based Pigments Market

8.1. Sudarshan Chemical Industries Limited

8.2. DIC Corporation

8.3. BASF SE

8.4. Altana AG

8.5. Lanxess AG

8.6. Clariant AG

8.7. Dow Inc.

8.8. Archroma

8.9. Toyo Ink SC Holdings Co. Ltd.

8.10. Sensient Technologies Corporation

8.11. Orion Engineered Carbons

8.12. Pidilite Industries Ltd.

8.13. Zhejiang NHU Co. Ltd.

8.14. Cabot Corporation

8.15. Atul Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Water Based Pigments Market Segmentation

By Product Type

Inorganic Pigments

Organic Pigments

Specialty and Effect Pigments

By Dispersion Type

Resin-Free Dispersions

Resin-Based Dispersions

Micro-Encapsulated Pigments

By Application

Paints and Coatings

Printing Inks

Textiles

Plastics and Rubber

Personal Care

By End-Use Industry

Building and Construction

Automotive and Transportation

Packaging and Labeling

Consumer Goods and Electronics

By Region

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

The market is valued at $11 billion in 2025 and is expected to reach $19.9 billion by 2034, growing at a CAGR of 6.8%. Expansion is driven by regulatory pressure on VOC emissions and rapid adoption of waterborne coatings. Automotive and packaging sectors are key growth engines.

Innovation is centered on high-stability dispersions, mineral-oil-free metallic pigments, and bio-attributed raw materials. Advanced wetting agents and controlled particle size distribution are improving performance parity with solvent-based systems. UV-curable hybrid systems are also gaining traction.

Automotive OEM coatings and architectural paints dominate demand due to sustainability mandates and durability requirements. Packaging inks are rapidly shifting toward water-based systems for recyclability compliance. Textile digital pigment printing is emerging as a high-growth niche.

India is emerging as a global manufacturing hub due to consolidation and cost advantages. China is driving demand through VOC regulations and EV coatings. Europe leads in sustainability-driven innovation, while the U.S. market is shaped by PFAS regulations and digital printing growth.

Key players include Sudarshan Chemical Industries, DIC Corporation, BASF, Altana, Clariant, and Lanxess. Competition is shifting toward sustainable chemistry, dispersion performance, and digital traceability. Strategic acquisitions and capacity expansions are strengthening global positioning.