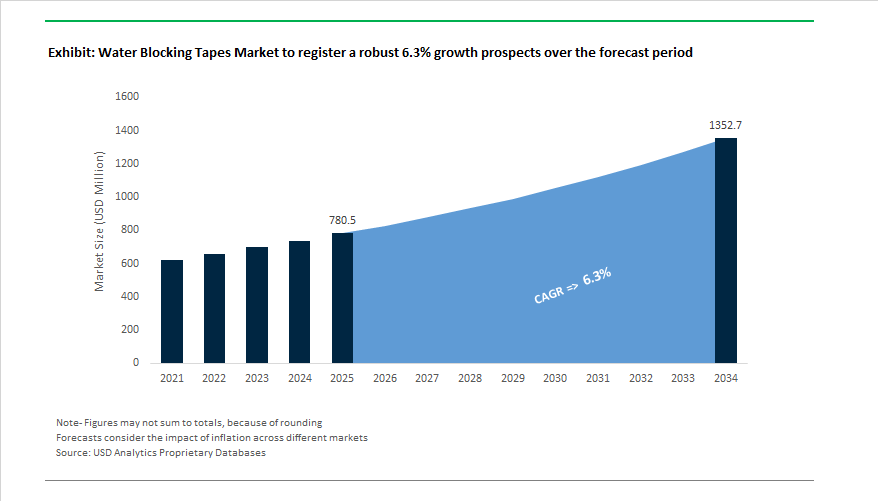

The Global Water Blocking Tapes Market is projected to grow from USD 780.5 million in 2025 to USD 1,352.6 million by 2034, registering a CAGR of 6.3%. This growth is primarily driven by the accelerated expansion of global fiber broadband networks, 5G deployments, and the modernization of electrical transmission and submarine cable infrastructure. Industry professionals are prioritizing lightweight, flexible, and high-swell tapes built on superabsorbent polymer (SAP) technology, which ensure superior cable protection against moisture ingress while maintaining structural integrity during installation and operation.

The market’s evolution is defined by the shift from conventional polyethylene tapes toward non-conductive and semi-conductive SAP-based materials, designed for optical fiber, energy transmission, and EV infrastructure applications. Rapid industrial digitization, coupled with government-funded broadband programs—such as India’s BharatNet and China’s EHV power network expansion—continues to elevate the demand for high-performance moisture barrier tapes across Asia Pacific.

Furthermore, sustainability imperatives and technological convergence are reshaping the product landscape. Manufacturers are pursuing recyclable polymers, bio-based coatings, and low-weight composite structures, aligning with the industry’s movement toward energy-efficient and eco-friendly cable materials. This trajectory positions water blocking tapes not merely as consumables but as strategic enablers of telecom reliability and power grid resilience.

Key Industry Insights

- Non-Conductive Segment Leadership: led by applications in optical fiber and submarine cables.

- 5G & Fiber Infrastructure Expansion: More than 8.3 billion global mobile subscriptions and ongoing 5G rollouts are fueling advanced cable protection needs.

- SAP Integration Revolution: Superabsorbent polymer (SAP) technology enhances flexibility, reduces cable weight, and improves water-blocking efficiency.

- Asia Pacific at the Forefront: massive telecom and power infrastructure investments.

- Rise of Semi-Conductive Tapes: Growing use between metal core screens and sheaths in high-voltage cables for combined electrical continuity and moisture resistance.

The Global Water Blocking Tapes Industry is witnessing a series of strategic developments since early 2025, marking a period of intense innovation in high-performance materials, manufacturing sustainability, and application-specific product engineering. These developments highlight the synergy between chemical science, polymer innovation, and infrastructure modernization across multiple sectors.

In September 2025, Arkema expanded its Kynar® PVDF production capacity in the United States, reinforcing its leadership in fluoropolymer-based moisture barrier coatings. This move directly supports the rising demand for high-purity water transport systems and wire & cable applications, offering enhanced resistance to water ingress and chemical degradation. Around the same period, Nitto Denko Corporation entered a Joint Development Agreement with Aqualung Carbon Capture, signaling a major step toward integrating sustainability-linked material science into membrane and water-blocking technologies. This partnership underscores Nitto’s pivot to ESG-aligned product portfolios, including next-generation hydrogel and polymer tape systems for environmental and industrial sealing.

In May 2025, an industry player launched a low-temperature butyl rubber tape optimized for cold-weather installations—an essential development for wind energy, telecommunication towers, and northern industrial projects. This innovation demonstrated the market’s increasing responsiveness to regional climate conditions and application adaptability. Earlier, 3M’s “eXcellence” model, highlighted in its 2025 Global Impact Report, redefined operational priorities by integrating sustainability and performance as dual pillars of growth for its adhesives, sealants, and semi-conductive water-blocking tape divisions.

At the JEC World event (February 2025), Arkema presented UDX® carbon fiber tapes impregnated with bio-based PA11 & PPA polymers, reinforcing the global trend toward lightweight, recyclable cable and composite materials. In January 2025, reports confirmed a surge in semi-conductive tape demand for EV charging infrastructure, as global electric mobility investments intensified. Concurrently, raw material cost inflation and tariff hikes in North America prompted manufacturers to pursue localized sourcing and polymer reformulation strategies to sustain profitability and reduce supply chain risks.

Companies like Sika AG continued emphasizing industrial sealing durability, aligning their waterproofing product innovations with the same design principles guiding their cable protection business. The integration of UV resistance, flexibility, and long-term performance mirrors the direction the water blocking tape sector is heading—toward greater reliability, sustainability, and operational efficiency across energy, construction, and telecom domains.

Market Trend 1: Integration of Superabsorbent Polymer (SAP) Technology for Enhanced Flood Protection in Submarine and Fiber Optic Cables

The growing deployment of submarine communication cables and offshore renewable energy networks has created a strong need for high-swelling, fast-reacting Superabsorbent Polymer (SAP)-based water blocking tapes that offer superior flood resistance even under deep-water pressure. These tapes, crucial for longitudinal water blocking, prevent catastrophic insulation failure and ensure long-term cable reliability.

Recent performance evaluations show that modern SAP-integrated tapes can achieve swelling heights exceeding 9.5 mm within the first minute of contact, setting a new benchmark for absorption efficiency. Some advanced formulations target ≥10 mm swell height in 60 seconds, ensuring immediate protection against water ingress during installation or accidental sheath breaches.

A major milestone in material innovation comes from Nippon Shokubai, whose AQUALIC™ CS salt-tolerant SAP technology can absorb 20–30 times its weight in seawater, making it indispensable for subsea fiber optic and power cables. The high osmotic performance enables optimal protection in saline and high-pressure marine environments.

In addition, new semi-conductive SAP-based tapes are replacing traditional water-blocking pastes in longitudinally sealed submarine cable designs. Patent-protected innovations demonstrate that integrating semi-conductive water-blocking layers around stranded conductors substantially enhances vertical water-blocking performance, ensuring superior integrity compared to conventional filling compounds.

Market Trend 2: Development of Non-Yellowing, Low-Migration Tapes for Indoor and Aerial Fiber Optic Cables

The global expansion of Fiber-to-the-Home (FTTH), 5G backhaul networks, and data center interconnections is reshaping material design for aerial and indoor fiber optic cables. Modern applications demand non-yellowing, low-migration, thermally stable water-blocking tapes that maintain optical clarity and long-term reliability under high temperature and UV exposure.

Water ingress remains a major concern for optical signal attenuation. When moisture interacts with glass fibers, hydrogen and OH− ion formation significantly increases transmission loss, necessitating the adoption of dry, non-migrating water-blocking materials that prevent moisture diffusion without introducing volatile chemical residues.

Modern manufacturing practices are optimizing SAP particle size distributions—with less than 7% of particles exceeding 300 microns in diameter—to minimize microbending losses and preserve optical transmission performance. The fine-tuning of the coating process enhances fiber geometry uniformity and overall signal integrity.

Additionally, advanced fiber optic tapes are being engineered for thermal stability up to 230°C (instantaneous) and long-term operation at 90°C–160°C, ensuring mechanical durability in high-temperature or fluctuating climates. These innovations align with the rapid growth of high-bandwidth, low-latency networks, where thermal stability and chemical inertness are essential to extending cable life and minimizing maintenance costs.

Market Opportunity 1: Development of Halogen-Free, Flame-Retardant Tapes for Plenum and EV Battery Cables

The push for fire-safe, environmentally sustainable materials across the automotive and construction sectors is fueling rapid growth in halogen-free, flame-retardant water blocking tapes. These tapes are crucial for plenum-rated communication cables, electric vehicle (EV) battery harnesses, and high-voltage distribution assemblies, where non-toxic smoke generation and flame containment are regulatory imperatives.

Modern halogen-free water blocking systems utilize Halogen-Free Flame Retardant (HFFR) polyolefin compounds, offering low-smoke, zero-halogen (LSZH) properties that meet stringent flammability and toxicity standards. These formulations not only ensure compliance with UL 94 VTM-0 ratings but also maintain superior insulation and thermal endurance, critical for confined environments such as EV battery enclosures and building plenums.

Market data indicates a growing preference for UL 94 V-0 certified silicone foams and rubbers for EV cable penetrations and charging assemblies, recognized for their low smoke density and high self-extinguishing behavior. These innovations align with global initiatives for electrical fire safety, as manufacturers pivot toward non-halogenated flame-retardant adhesives compatible with eco-compliant insulation systems.

By integrating HFFR-based water-blocking layers, cable manufacturers achieve multi-functional protection—ensuring both fire safety and moisture resistance—while maintaining recyclability and compliance with environmental directives like RoHS and REACH.

Market Opportunity 2: Engineering Thermally Conductive Water Blocking Tapes for Underground and HVDC Power Transmission

The evolution of smart grids and renewable energy networks is generating strong demand for thermally conductive water blocking tapes that mitigate heat accumulation in underground and high-voltage power transmission cables. As current densities and operating voltages increase, thermal management has become a decisive performance factor.

Thermal modeling data reports that in high-voltage cable assemblies, buffer layers containing conventional water-blocking strips exhibit thermal conductivities as low as 0.09 W/(m·K)—far below that of XLPE insulation (0.286 W/(m·K)) and metal conductors (402 W/(m·K)). The imbalance forms a thermal bottleneck that limits current-carrying capacity and shortens cable lifespan.

To address the, R&D efforts are focused on hybrid SAP-filled thermally conductive composites, designed to preserve water-blocking functionality while enhancing heat dissipation through the cable core. These materials ensure that moisture control does not compromise thermal performance, an essential requirement for underground transmission and HVDC subsea power cable systems.

The HVDC design guidelines emphasize that the choice of materials within the conductor interstices directly affects both resistance and heat transport efficiency. Thermally optimized water blocking tapes can thus significantly improve the ampacity and reliability of cables used in offshore wind farm grid connections, underground networks, and intercontinental power links.

Water Blocking Tapes Market Share Insights, 2025-2034

Market Share by Conductive Type

The non-conductive water blocking tapes segment dominates the global market, accounting for an estimated 63.6% share in 2025. This dominance is attributed to their widespread use as the standard moisture protection solution in fiber optic and low- to medium-voltage power cables, which constitute the largest portion of the global cable manufacturing industry. These tapes are designed to swell and form a gel barrier upon contact with water, preventing its longitudinal movement within the cable and ensuring long-term cable integrity and operational reliability. Their chemical stability, low cost, and easy integration into existing cable production lines make them the preferred option for manufacturers focusing on high-volume, performance-driven cable designs. The continuous expansion of telecommunications infrastructure, 5G rollouts, and data center connectivity projects further strengthens the dominance of non-conductive water blocking tapes, especially in fiber optic cables where maintaining signal integrity is critical.

The semi-conductive and conductive water blocking tapes segments, while smaller, play crucial roles in specialized and high-performance cable systems. Semi-conductive water blocking tapes are indispensable in medium- and high-voltage power cable constructions, where they serve a dual purpose—providing both controlled electrical stress management and moisture resistance. Their conductive properties help ground electric fields around the conductor shield, ensuring safety and reliability under high-voltage conditions. This makes them essential in energy transmission and grid modernization projects, where long-distance and high-capacity cables are exposed to moisture and electrical stress simultaneously. Conductive water blocking tapes, on the other hand, occupy a niche but technologically demanding space, used primarily in telecommunication and specialty cables requiring electromagnetic interference (EMI) shielding in addition to water resistance. As the demand for hybrid, multifunctional cable components grows—especially in smart grid and advanced communication systems—these specialized conductive tapes are expected to gain incremental adoption despite their smaller share.

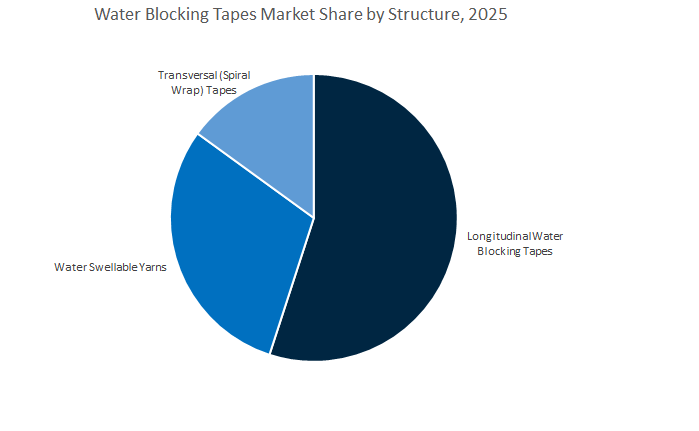

Market Share by Structure

The longitudinal water blocking tapes segment holds the largest market share, projected at 52.6% in 2025, and remains the industry standard for most fiber optic and power cable designs. Their simple yet highly effective application method—laying tapes parallel along the cable’s length—makes them ideal for providing continuous moisture resistance and mechanical reinforcement without adding significant weight or complexity. Longitudinal tapes are widely used in telecommunication, data transmission, and energy distribution cables, offering a cost-effective solution for manufacturers seeking consistent swelling performance and minimal production time. The dominance of this segment is closely tied to the ongoing expansion of global broadband infrastructure and renewable energy networks, both of which demand durable, moisture-protected cables capable of long service life in outdoor and underground installations. Their compatibility with both non-conductive and semi-conductive formulations also enhances their versatility, making them the most utilized structural configuration across diverse cable types and applications.

Meanwhile, water-swellable yarns represent a critical complementary technology and the second-largest structural segment, widely adopted for their three-dimensional blocking efficiency. These yarns are strategically placed within cable interstices to prevent water migration through even the smallest voids, ensuring enhanced protection in direct-burial and submarine cable installations. Their ability to absorb and retain water without losing structural integrity makes them indispensable in environments where longitudinal tapes alone cannot offer complete sealing. The combination of tapes and swellable yarns has become standard practice in high-performance cables, reflecting the industry’s move toward redundant, fail-safe moisture protection systems. On the other hand, transversal (spiral-wrap) tapes cater to large-diameter or specialized cable designs where longitudinal application is less effective. These tapes are wrapped helically around the cable core, creating a continuous physical barrier against water ingress. While their application is more material-intensive and slower, they are favored in premium cable designs requiring superior mechanical strength, enhanced water resistance, and flexibility, such as subsea cables, offshore wind farm connectors, and high-capacity energy transmission lines.

The Water Blocking Tapes Market is moderately consolidated, with a handful of major players commanding significant technological and regional influence. These leaders—H.B. Fuller, Nitto Denko Corporation, 3M, Chase Corporation, Sika AG, and Arkema S.A.—have adopted strategies centered around sustainability, polymer innovation, and diversified industrial integration. Their ongoing R&D, acquisitions, and production expansions are defining the next chapter in cable protection material evolution.

H.B. Fuller is at the forefront of high-performance sealant and water-blocking tape innovation with its proprietary MicroSealant® technology. Its portfolio of butyl and modified rubber tapes offers superior adhesion to EPDM, TPO, and metal substrates, making it ideal for transportation, wind energy, and industrial assembly. The company’s emphasis on low-temperature flexibility, UV durability, and water-based adhesive systems positions it as a sustainability-aligned leader in exterior cable protection and sealing applications.

Nitto Denko leverages its mastery of membrane and adhesive film technologies to produce ultra-thin, clean-peeling, and high-swell materials for infrastructure and mobility applications. Its global R&D efforts integrate film coating and thin-film science, forming the backbone of its high-performance water-swellable tapes. The company’s “Nitto-Style ESG Strategy” reflects a long-term commitment to green innovation, while its worldwide production network ensures supply chain resilience across over 20 manufacturing and technical service centers.

3M maintains a diversified adhesive and sealing technology portfolio with deep roots in industrial safety, energy, and telecommunications. Its semi-conductive water-blocking tapes are recognized for moisture resistance, dielectric stability, and reliability in extreme conditions. Under the “3M eXcellence” initiative, the company has renewed its focus on sustainable innovation, driving R&D investments into environmentally responsible polymers for next-generation telecom and power transmission applications.

Chase Corporation specializes in protective materials and chemical compounds engineered for wire & cable reliability. Its flagship product, Chase BlH₂Ock®, exemplifies the firm’s leadership in pumpable semi-conductive strand filling compounds that protect conductors against moisture. Chase’s suite of superabsorbent powders, strand seal compounds, and shielding materials extends into both telecom and energy cables, showcasing its strength in material science and applied chemistry for cable integrity.

Sika AG applies its extensive industrial sealing expertise to semi-conductive water-blocking tapes such as WSC244, known for fast-swell behavior and low electrical resistance. Designed for power cable sheathing and core screen applications, Sika’s products leverage its proven strengths in UV-resistant, durable, and flexible sealing systems. The company’s strong industrial base across Asia, Europe, and North America allows it to address the evolving needs of global power infrastructure and renewable energy projects.

Arkema stands out for its high-performance polymer solutions that merge lightweight design, moisture resistance, and sustainability. Its Kynar® PVDF fluoropolymer is a cornerstone for internal cable coatings and barrier systems, while the Rilsan® Polyamide 11 series, made from 100% bio-based materials, demonstrates Arkema’s dedication to green chemistry. The company’s innovations in wire & cable, 5G infrastructure, and EV components align perfectly with the growing industry emphasis on durable, eco-efficient materials.

Country Analysis: Regional Developments Defining the Global Water Blocking Tapes Industry

China – Expansion Driven by Ultra-High-Voltage Projects and 5G Infrastructure Growth

China remains the epicenter of global demand for water blocking tapes, propelled by its massive power transmission, fiber optics, and telecommunication infrastructure expansion. The State Grid Corporation of China (SGCC) continues its multibillion-dollar Ultra-High-Voltage (UHV) transmission line investments, which require high-reliability, water-resistant cable components to ensure performance and longevity in underground and long-distance energy networks. Major domestic manufacturers such as Jiangsu Zhongtian Technology (ZTT) and Far East Cable have unveiled new lines of water swellable tapes and yarns engineered for both power cable insulation and optical fiber protection.

China’s 5G and broadband expansion initiatives remain a defining growth driver. Companies like China Telecom and China Unicom are investing heavily in next-generation submarine cable systems, necessitating non-conductive, saltwater-resistant water blocking tapes to ensure performance integrity under high-pressure marine environments. Additionally, local investments in Super Absorbent Polymer (SAP) and non-woven fabric production are creating a vertically integrated supply chain that reduces import dependency. The developments position China as the largest global manufacturing hub for water blocking materials, aligned with its Made in China 2025 strategy.

United States – Strengthening Submarine Cable Security and Offshore Wind Infrastructure

The United States water blocking tapes market is experiencing strong momentum, driven by the intersection of national security concerns, renewable energy expansion, and smart grid modernization. The Federal Communications Commission (FCC) and U.S. lawmakers have intensified scrutiny of submarine communication cable security, leading to new investments in water-blocking and self-healing protective tape technologies. Utility operators such as Dominion Energy are spearheading offshore wind projects, including HVDC cable installations, which rely heavily on semi-conductive and non-conductive water blocking tapes to safeguard against corrosion and moisture ingress.

Industry leaders like 3M Company and Chase Corporation are expanding their non-conductive and hybrid tape portfolios, supporting the nationwide deployment of fiber optic broadband and high-speed communication networks. Furthermore, U.S. manufacturers are focusing on smart grid-enabled hybrid tapes capable of dual power and data transmission protection. Innovation in self-healing and thermally stable water blocking tapes is a growing trend, ensuring reduced downtime and lower lifecycle maintenance costs in buried and subsea power networks.

Germany – Automotive Electrification and Sustainable Water Blocking Solutions

Germany continues to lead the European water blocking tapes market, combining technological innovation, renewable energy integration, and stringent EU environmental compliance. The automotive sector’s rapid shift to Electric Vehicle (EV) platforms is driving the use of lightweight, small-format hydrophilic water blocking tapes in battery cables, wiring harnesses, and charging systems. The country’s robust offshore wind installations in the North Sea are simultaneously creating high-volume demand for hydrophilic and high-tensile water blocking materials designed to withstand marine exposure.

Compliance with the EU’s RoHS and REACH regulations is prompting industry giants like tesa SE and Freudenberg Performance Materials to pioneer halogen-free, eco-friendly, and recyclable water blocking tapes. German utilities are also modernizing underground power networks, requiring high-voltage semi-conductive water blocking solutions for reliability and insulation integrity. Supported by EU funding for sustainable infrastructure, Germany is at the forefront of green innovation in cable protection, integrating bio-based polymer composites and next-generation SAP formulations for performance and sustainability.

India – Smart City Connectivity and High-Speed Fiber Expansion

India’s water blocking tapes market is expanding rapidly, supported by nationwide digitalization and infrastructure initiatives. The Smart Cities Mission and National Broadband Mission are driving massive deployment of Optical Fiber Cables (OFCs), creating unprecedented demand for non-conductive, SAP-based water blocking tapes. The tapes are essential for moisture ingress protection and long-term durability in underground and high-humidity environments.

Manufacturers such as Indore Composites and Sneham International are scaling up domestic production capacities to serve the growing domestic and export markets, aligning with the ‘Make in India’ initiative. Parallel growth in solar parks, renewable energy grids, and metro rail systems is further increasing consumption of semi-conductive water blocking tapes for high-voltage power cables. With India's focus on local manufacturing, cost optimization, and sustainability, the country is emerging as a strategic manufacturing base for water blocking materials in South Asia.

Saudi Arabia – Giga-Projects and Renewable Energy Grid Expansion

Saudi Arabia’s giga-project ecosystem, including NEOM City, the Red Sea Project, and Qiddiya, is propelling the regional water blocking tapes industry to new heights. The mega-infrastructure initiatives require high-performance, fire-retardant, and water-resistant tape systems for extensive underground utilities and high-voltage cable installations. The nation’s strong pivot toward renewable energy infrastructure, particularly solar and wind, necessitates high-strength, semi-conductive water blocking materials to ensure long-term cable insulation integrity in extreme temperature conditions.

The government’s Vision 2030 diversification plan emphasizes local content development and infrastructure resilience, leading to collaborations between global and domestic manufacturers for localized tape production and cable component integration. Simultaneously, large-scale fiber optic network expansions to support smart city connectivity across new urban centers are driving high-value demand for non-conductive water blocking tapes in telecommunications.

United Kingdom – Offshore Wind Grid Modernization and Subsea Cable Protection

The United Kingdom water blocking tapes market is rapidly evolving in response to the country’s offshore wind energy expansion and subsea infrastructure upgrades. The government’s net-zero emissions target for 2050 underpins significant investments in offshore wind farms that depend on robust submarine power cable systems protected by premium-grade water blocking tapes. Recent subsea cable faults in the Baltic Sea have heightened the focus on cable durability and fault prevention, pushing demand for next-generation hydrophilic tapes with improved tensile and swelling performance.

Scapa Industrial (now part of SWM International) remains a global leader, producing fire-retardant, non-conductive, and high-performance water blocking tapes for the power and telecommunication sectors. The UK’s renewable grid projects, combined with advancements in marine cable resilience technologies, are reinforcing the country’s status as a key European market for advanced water-blocking and cable protection systems.

Water Blocking Tapes Market Report Scope

Water Blocking Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$780.5 Million

|

|

Market Size (2034)

|

$1352.6 Million

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Conductive Type (Non-Conductive, Semi-Conductive, Conductive), By Material Composition (SAP-based, Butyl Rubber-based, Hydrophilic Polymer-based, XLPE-based), By Cable Application (Submarine, High-Voltage, Fiber Optic, Communication, Industrial), By Structure (Longitudinal, Transversal, Water Swellable Yarns), By Manufacturing Process (Non-Woven, Laminated Film

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SWM International, Chase Corporation, tesa SE, 3M, Freudenberg Performance Materials, Nitto Denko Corporation, Berry Global Group, Inc., LS Cable & System Ltd., Nexans S.A., Prysmian Group, Geca Tapes S.r.l., Fori Group S.p.A., Gurfil Ltd., Sumitomo Electric Industries, Ltd., Hanyu Cable Materials Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Conductive Type

- Non-Conductive

- Semi-Conductive

- Conductive

By Material Composition

- SAP-based

- Butyl Rubber-based

- Hydrophilic Polymer-based

- XLPE-based

By Cable Application

- Submarine

- High-Voltage

- Fiber Optic

- Communication

- Industrial

By Structure

- Longitudinal

- Transversal

- Water Swellable Yarns

By Manufacturing Process

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Water Blocking Tapes Market-

- SWM International

- Chase Corporation

- tesa SE

- 3M

- Freudenberg Performance Materials

- Nitto Denko Corporation

- Berry Global Group, Inc.

- LS Cable & System Ltd.

- Nexans S.A.

- Prysmian Group

- Geca Tapes S.r.l.

- Fori Group S.p.A.

- Gurfil Ltd.

- Sumitomo Electric Industries, Ltd.

- Hanyu Cable Materials Co., Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the rapidly evolving Water Blocking Tapes Market, connecting infrastructure rollouts in 5G, fiber broadband, submarine links, and power transmission with the shift to superabsorbent polymer (SAP) architectures; our analysis reviews conductivity classes, swelling kinetics, mechanical/thermal stability, and manufacturing routes to map performance-to-cost across telecom and energy cables; it also highlights recyclable polymers, halogen-free fire safety, and thermally enhanced designs as near-term differentiators, distills breakthroughs in salt-tolerant SAPs and low-migration builds for indoor/aerial fiber, and explains why sourcing localization and qualification discipline are becoming board-level topics—making this report an essential resource for product leaders, sourcing heads, and specification engineers who need market clarity, risk visibility, and actionable growth pathways, etc……

Scope Highlights

Segmentation:

- By Conductive Type: Non-Conductive; Semi-Conductive; Conductive

- By Material Composition: SAP-based; Butyl Rubber-based; Hydrophilic Polymer-based; XLPE-based

- By Cable Application: Submarine; High-Voltage; Fiber Optic; Communication; Industrial

- By Structure: Longitudinal; Transversal; Water Swellable Yarns

- By Manufacturing Process: Non-Woven; Laminated Film

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies Covered (analysis/profiles of 15+): SWM International; Chase Corporation; tesa SE; 3M; Freudenberg Performance Materials; Nitto Denko Corporation; Berry Global Group, Inc.; LS Cable & System Ltd.; Nexans S.A.; Prysmian Group; Geca Tapes S.r.l.; Fori Group S.p.A.; Gurfil Ltd.; Sumitomo Electric Industries, Ltd.; Hanyu Cable Materials Co., Ltd. (non-exhaustive)

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.