Water Recycle and Reuse Market Overview: Growth Outlook and Key Insights

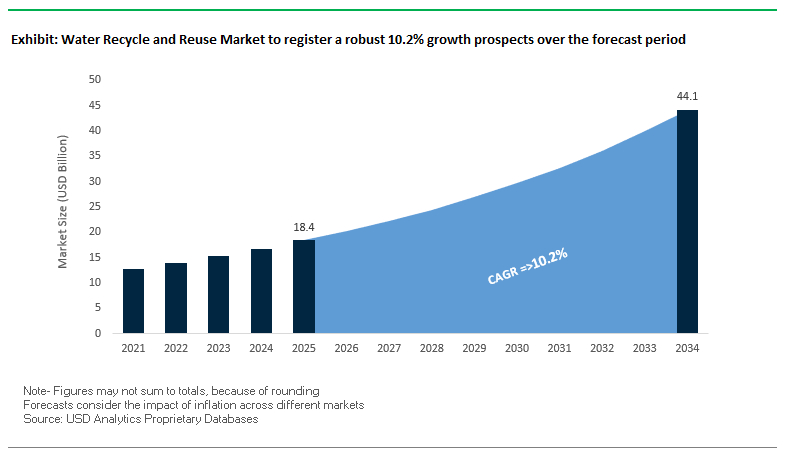

The global water recycle and reuse market is set to grow from $18.4 billion in 2025 to $44.1 billion by 2034, registering a strong CAGR of 10.2%. This expansion is being driven by escalating water scarcity concerns, stricter environmental regulations, and the rising need for sustainable industrial water management solutions.

Key Insights:

- Asia Pacific dominance: In 2024, China and India held a significant share due to industrial growth and mandatory water reuse regulations.

- Industrial uptake: Power generation, semiconductors, and food & beverage sectors are investing heavily in zero liquid discharge (ZLD) systems.

- Technology preference: Reverse osmosis (RO) and ultrafiltration (UF) remain the most widely used for high-quality recycled water production.

- Middle East focus: Countries such as Saudi Arabia are investing aggressively in desalination and water recycling projects to counter water stress.

Market Analysis: Strategic Developments Driving Growth

The water recycle and reuse market is undergoing significant transformation, marked by technological breakthroughs, policy shifts, and large-scale infrastructure projects. In August 2025, VA Tech Wabag won a ₹46.5 crore contract to provide ultrapure water and ZLD systems for a solar cell facility in Hyderabad, showcasing how advanced recycling solutions are being integrated into high-tech industries. Similarly, in July 2025, Brunswick County (USA) advanced its $167.3 million low-pressure RO system to eliminate PFAS from drinking water one of the largest such initiatives nationwide.

That same month, VA Tech Wabag also secured a ₹380 crore contract in Bengaluru for an energy-efficient water reuse facility, further cementing the company’s role in municipal wastewater recycling. Meanwhile, policy support is accelerating adoption Texas, in June 2025, passed new laws promoting produced-water reuse in oil and gas, streamlining permitting and providing liability protections, which is expected to spur wider use of industrial recycling systems.

Other strategic moves underscore the globalization of water reuse solutions. Veolia Water Technologies, in May 2025, acquired full ownership of its Water Technologies and Solutions subsidiary, reinforcing its end-to-end water recycling portfolio. European government funding in March 2025 for anti-fouling membrane R&D highlights innovation trends focused on reducing operational costs. Looking back to late 2024, Nitto Denko’s COP29 showcase of carbon-negative membranes and Ramky Infrastructure’s ₹215.08 crore STP project in Hyderabad underline how both technological and infrastructure-driven approaches are propelling this market forward.

Key Trends Shaping the Water Reuse Industry

Government Policy and Financial Support for Water Reuse Infrastructure

Regulatory initiatives are driving large-scale adoption of water recycling solutions globally. The European Union's Water Reuse Regulation, effective June 2023, sets harmonized minimum quality standards for treated urban wastewater used in agricultural irrigation. According to the European Commission's Joint Research Centre (JRC), while roughly 1 billion cubic meters of treated wastewater are currently reused annually in Europe, the continent has the potential to expand this sixfold. In the United States, the Infrastructure Investment and Jobs Act of 2021 allocated over $1 billion toward water recycling projects over five years. Notable examples include the Pure Water Monterey Groundwater Replenishment Project, which secured a $76 million loan to treat municipal wastewater for aquifer recharge, addressing saltwater intrusion and enhancing regional water security.

Corporate Investment in On-Site Industrial Water Recycling

Corporate sustainability strategies are increasingly steering investments in on-site water recycling. Microsoft’s Quincy Water Reuse Utility in Washington is a leading example, where recycled cooling water from the company’s data center reduces dependence on potable groundwater. In Latin America, the Aquapolo project in São Paulo, Brazil, highlights the benefits of industrial water reuse on a regional scale. Through a partnership between Sabesp and GS Inima, the facility produces up to 1,000 liters per second of recycled water for petrochemical industries, ensuring continuity during droughts and demonstrating the resilience that water reuse offers to water-intensive sectors.

Hybrid Treatment Systems for Diverse Water Sources

Technological innovation is enabling more efficient and adaptable water recycling solutions. Research from the Indian Institute of Technology, Bombay, emphasizes hybrid systems that combine mechanized and natural treatment processes, achieving Biological Oxygen Demand (BOD) levels below 10 mg/L cost-effectively. Advanced multi-stage systems integrating moving bed biofilm reactors (MBBR), membrane bioreactors (MBR), and direct contact membrane distillation (DCMD) are demonstrating exceptional performance in industrial wastewater treatment, enabling high-quality water output suitable for a broad range of reuse applications.

Water Recycle and Reuse Market Share Insights

Market Share by Technology

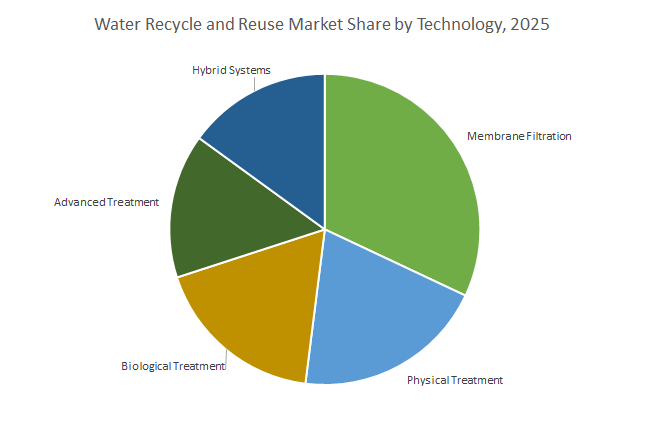

Membrane Filtration is projected to dominate the market in 2025 with a share of approximately 32%, largely driven by its ability to produce high-purity water suitable for industrial and potable reuse. Advanced Hybrid Systems, combining biological and membrane technologies, are the fastest-growing segment with a projected share of 15%, offering customized solutions for complex water quality requirements. Physical and Biological treatments, accounting for 20% and 18% respectively, remain essential as cost-effective primary and secondary treatment processes, while Advanced Treatment (15%) ensures final polishing and pathogen removal, crucial for public acceptance of indirect potable reuse initiatives.

Market Share by Application

Industrial Reuse leads the market with a projected 45% share in 2025, driven by clear economic returns and operational necessity. Municipal Reuse (30%) is expanding, particularly in arid regions, supported by non-potable and indirect potable reuse initiatives. Agricultural Reuse (20%) holds a significant but challenging position due to public perception, infrastructure costs, and salinity management. The Commercial & Residential segment (5%) represents a niche market, gaining traction through greywater systems in green buildings and local water conservation mandates.

Market Share by End-Use Industry

Power Generation is the largest end-user segment (18%), utilizing recycled water primarily for cooling purposes. Food & Beverage (15%) and Chemicals & Petrochemicals (14%) are key industrial adopters requiring reliable and high-quality recycled water. Municipal Utilities (12%) play a strategic role in public water supply augmentation. The Oil & Gas sector (11%) benefits from reusing fracturing and produced water, while Electronics & Semiconductors and Pharmaceuticals & Biotechnology require ultra-pure water for manufacturing processes. Textiles, Dyeing, and Pulp & Paper industries face challenges in treating high-strength wastewater. Mining & Metals (4%) and Commercial & Residential Buildings represent smaller segments but are increasingly investing in tailored water reuse solutions.

Country Analysis of Water Recycle and Reuse Market

United States: Federal Funding and Innovative Reuse Projects Driving Market Growth

The United States is a key market for water recycle and reuse, supported by substantial federal funding and advanced technology deployment. Through the Bipartisan Infrastructure Law, the Environmental Protection Agency (EPA) receives over $50 billion to upgrade national water infrastructure, including specific allocations to address emerging contaminants such as PFAS. The new PFAS Maximum Contaminant Levels have prompted immediate retrofitting of water treatment facilities with advanced membrane filtration technologies. Initiatives under the National Water Reuse Action Plan (WRAP) and the Bureau of Reclamation’s Large-Scale Water Recycling Program, backed by $180 million in funding, are promoting innovative applications to transform unusable water into drought-resistant supplies. Corporate actions by Veolia Water Technologies and Evoqua Water Technologies, alongside the Pure Water Center in El Paso America’s first direct-to-distribution potable reuse facility highlight growing adoption. Additionally, Micron Technology’s pilot program using Aqua Membranes’ 3D-printed spacers in RO systems underscores industrial commitment to water reuse and conservation.

China: Stringent Regulations and Membrane Innovations Boost Recycling Infrastructure

China’s recycling water reuse market is strongly influenced by stringent regulatory oversight and technological advancement. The Ministry of Ecology and Environment (MEE) enforces tough standards on industrial wastewater discharge, aligning with the 14th Five-Year Plan which targets 95% wastewater treatment across all county-level cities. This has accelerated adoption of membrane filtration and recycling water infrastructure. In 2024, researchers at the Chinese Academy of Sciences introduced a dual-functional RO membrane with enhanced antibacterial and anti-adhesion properties, improving efficiency in recycling applications. Government investments of $50 billion by 2025 focus on wastewater treatment in heavy-polluting industries, including textiles, steel, and pharmaceuticals. Membrane bioreactors (MBRs) are increasingly integrated into municipal wastewater expansion and renovation projects, ensuring compliance with stricter discharge standards while minimizing the physical footprint.

India: Policy Support and Infrastructure Expansion Driving Water Reuse Initiatives

India’s water recycle and reuse sector is propelled by comprehensive government initiatives and substantial infrastructure investment. Programs such as the Jal Jeevan Mission, National Mission for Clean Ganga (NMCG), and Smart Cities Mission accelerate deployment and modernization of wastewater treatment facilities. The Atal Mission for Rejuvenation and Urban Transformation (AMRUT) has allocated approximately USD 10 billion for enhancing water supply and treatment infrastructure, leveraging public-private partnership (PPP) models for large-scale projects. Progressive state-level regulations, such as Gujarat’s 50% capital subsidy for treated wastewater reuse projects, further incentivize adoption. Industrial applications, especially in power, chemicals, and textiles, are increasingly implementing wastewater reuse to mitigate water scarcity and comply with stringent environmental regulations.

Singapore: NEWater Project Setting Global Standards in Water Recycling

Singapore remains a global pioneer in water recycling through its NEWater initiative, which treats and recycles wastewater to meet a significant portion of the nation’s water demand. The system integrates microfiltration, reverse osmosis, and UV disinfection to produce high-quality water for industrial and potable applications. The Public Utilities Board (PUB) continuously invests in R&D to improve recycling capabilities, focusing on advanced membrane technologies and intelligent monitoring systems. Recycled water is utilized across industrial cooling, potable blending, and other applications, demonstrating Singapore’s leadership in reliable and sustainable water reuse solutions.

Germany: Regulatory Enforcement and Industrial Recirculation Driving Advanced Filtration

Germany leads the European water recycle and reuse market with stringent regulatory frameworks and advanced treatment technologies. The Federal Water Act and Waste Water Ordinance enforce strict standards for wastewater discharge, compelling companies to adopt recycling solutions. Over 96% of wastewater from households and public facilities is processed in sewage treatment plants, with a strong emphasis on removing contaminants such as pharmaceuticals and antibiotics. Companies like CERAFILTEC are supplying ceramic flat membranes for MBR projects worldwide, while PPU Umwelttechnik develops containerized membrane systems suitable for retrofitting existing infrastructure. Industrial sectors, including paper production, extensively practice water recirculation to reduce freshwater consumption.

Saudi Arabia: Strategic Investments and Membrane Technologies Supporting Reuse

Saudi Arabia is aggressively investing in water recycle and reuse to address its arid climate. The Kingdom plans approximately $4 billion across 96 projects aimed at reusing 1.8 billion cubic meters of treated water by 2030, covering agriculture, industrial, and urban applications. The Saudi Water Partnership Company (SWPC) leads Public-Private Partnership (PPP) initiatives that utilize advanced reverse osmosis and membrane filtration technologies. Treated wastewater is prioritized for non-potable municipal use, industrial processes, and irrigation, reflecting a strategic focus on sustainable water management and resource optimization.

Competitive Landscape: Key Industry Players

The competitive landscape of the global water recycle and reuse market is shaped by leading multinational corporations combining advanced membrane technologies, sustainability-driven solutions, and digital optimization platforms. These players are differentiating themselves through strategic contracts, acquisitions, and innovations that address industrial, municipal, and environmental water challenges.

SUEZ – Strengthening Global Footprint in Wastewater Recycling

SUEZ is a leader in membrane-based recycling technologies and digital water solutions. The company has secured major contracts in Asia, including a seawater RO project in the Philippines and an industrial wastewater facility in China, both designed for 100% recycling efficiency. Its portfolio spans RO, UF, and MBR technologies, and it integrates predictive analytics to optimize performance, reduce fouling, and cut operational costs for clients worldwide.

Veolia Water Technologies – Expanding Global Reuse Projects

Veolia is recognized for its desalination leadership and operates treatment facilities with a capacity exceeding 13 million m³ per day across 44 countries. In July 2025, it secured a major municipal wastewater reuse contract in Brazil, leveraging advanced biological and membrane technologies. Beyond water, Veolia’s MemGas™ technology demonstrates its innovation in converting wastewater biogas into renewable natural gas, underscoring its sustainability focus.

DuPont Water Solutions – Driving Membrane Innovation

DuPont leverages polymer science and materials expertise to deliver world-class RO and NF membranes. Its FilmTec™ Fortilife™ series has earned recognition for enabling industrial wastewater reuse with greater efficiency. Alongside RO, UF, and ion exchange technologies, DuPont’s strategy emphasizes water circularity and carbon reduction, making it a preferred partner for industries aiming to cut operational costs while achieving sustainability goals.

Xylem Inc. – Integrated Water Solutions Provider

Xylem has established itself as a full-cycle water technology leader, offering solutions ranging from biological treatment systems and MBRs to advanced oxidation processes. Its 2023 acquisition of Evoqua has significantly expanded its capabilities in wastewater recycling. Recent collaborations include a partnership with Gross-Wen Technologies on algal biofilm wastewater treatment and participation in the PureWater Colorado DPR project, advancing potable reuse initiatives.

Aquatech International LLC – Specialist in ZLD and Industrial Reuse

Aquatech is known for its comprehensive industrial water reuse systems, particularly in ZLD applications. The company has partnered with AECOM to deploy PFAS destruction technologies, combining electrochemical treatment with end-to-end solutions. Its offerings span RO, NF, MBRs, crystallizers, and evaporators, enabling treatment of complex streams. A major highlight is its contract for Kuwait Oil Company’s Lower Fars Heavy Oil Project, underscoring its expertise in managing challenging industrial wastewater.

Water Recycle and Reuse Market Report Scope

Water Recycle and Reuse Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.4 Billion

|

|

Market Size (2034)

|

$44.1 Billion

|

|

Market Growth Rate

|

10.2%

|

|

Segments

|

By Technology (Physical Treatment, Membrane Filtration, Biological Treatment, Advanced Treatment, Hybrid Systems), By Application (Municipal Reuse, Industrial Reuse, Agricultural Reuse, Commercial & Residential Reuse), By End-Use Industry (Power Generation, Oil & Gas, Food & Beverage, Pulp & Paper, Textiles & Dyeing, Electronics & Semiconductors, Pharmaceuticals & Biotechnology, Chemicals & Petrochemicals, Mining & Metals, Municipal Utilities, Commercial & Residential Buildings), By System Configuration (Centralized Systems, Decentralized / On-Site Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, Pentair plc, DuPont de Nemours, Inc., Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, V.A. TECH WABAG Ltd., Mitsubishi Chemical Corporation, Kuraray Co., Ltd., Nalco Water (An Ecolab Company), MANN+HUMMEL

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Recycle and Reuse Market Segmentation

By Technology

- Physical Treatment

- Sedimentation & Clarification

- Sand & Multimedia Filtration

- Activated Carbon Filtration

- Membrane Filtration

- Microfiltration (MF)

- Ultrafiltration (UF)

- Nanofiltration (NF)

- Reverse Osmosis (RO)

- Biological Treatment

- Conventional Activated Sludge (CAS)

- Sequencing Batch Reactors (SBR)

- Membrane Bioreactors (MBR)

- Moving Bed Biofilm Reactors (MBBR)

- Advanced Treatment

- Advanced Oxidation Processes (AOPs)

- UV & Ozone Disinfection

- Electrocoagulation & Electro-oxidation

- Hybrid Systems

- Integrated Membrane + Biological Treatment

- Zero Liquid Discharge (ZLD) Solutions

By Application

- Municipal Reuse

- Potable Water Reuse

- Non-Potable Uses

- Wastewater Reclamation

- Industrial Reuse

- Cooling Tower Blowdown Recycling

- Boiler Feedwater Reuse

- Process Water Recycling

- Zero Liquid Discharge (ZLD) Systems

- Agricultural Reuse

- Irrigation Water Recycling

- Aquaculture Water Reuse

- Commercial & Residential Reuse

- Greywater Reuse

- Decentralized Water Recycling in Buildings & Housing Complexes

By End-Use Industry

- Power Generation

- Oil & Gas

- Food & Beverage

- Pulp & Paper

- Textiles & Dyeing

- Electronics & Semiconductors

- Pharmaceuticals & Biotechnology

- Chemicals & Petrochemicals

- Mining & Metals

- Municipal Utilities

- Commercial & Residential Buildings

By System Configuration

- Centralized Systems

- Decentralized / On-Site Systems

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Water Recycle and Reuse Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- Pentair plc

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- V.A. TECH WABAG Ltd.

- Mitsubishi Chemical Corporation

- Kuraray Co., Ltd.

- Nalco Water (An Ecolab Company)

- MANN+HUMMEL

*- List not Exhaustive

Research Coverage

This report investigates the global Water Recycle and Reuse Market, delivering analysis reviews on growth drivers, technology breakthroughs, project pipelines, and regulatory inflection points that shape bankable reuse outcomes through 2034. Produced by USDAnalytics, this report is an essential resource for utilities, industrial operators, EPCs, and policymakers. It highlights how hybrid biological-membrane trains, advanced polishing, and decentralized modular systems elevate recovery rates, stabilize quality for indirect/direct potable reuse, and compress lifecycle costs. With strategic highlights on financing models, policy catalysts, and sector-specific adoption (power, semiconductors, F&B, oil & gas), the study maps practical upgrade pathways and payback levers for stakeholders planning ZLD, retrofit programs, and new builds. Scope Includes-

- Segmentation:

- By Technology: Physical Treatment (Sedimentation & Clarification; Sand & Multimedia Filtration; Activated Carbon Filtration); Membrane Filtration (MF, UF, NF, RO); Biological Treatment (CAS, SBR, MBR, MBBR); Advanced Treatment (AOPs, UV & Ozone, Electrocoagulation & Electro-oxidation); Hybrid Systems (Integrated Membrane + Biological, ZLD).

- By Application: Municipal Reuse (Potable, Non-Potable, Wastewater Reclamation); Industrial Reuse (Cooling Tower Blowdown, Boiler Feedwater, Process Water, ZLD); Agricultural Reuse (Irrigation, Aquaculture); Commercial & Residential Reuse (Greywater, Decentralized Building Systems).

- By End-Use Industry: Power Generation; Oil & Gas; Food & Beverage; Pulp & Paper; Textiles & Dyeing; Electronics & Semiconductors; Pharmaceuticals & Biotechnology; Chemicals & Petrochemicals; Mining & Metals; Municipal Utilities; Commercial & Residential Buildings.

- By System Configuration: Centralized Systems; Decentralized / On-Site Systems.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; Pentair plc; DuPont de Nemours, Inc.; Toray Industries, Inc.; Aquatech International; Kubota Corporation; The Dow Chemical Company; V.A. TECH WABAG Ltd.; Mitsubishi Chemical Corporation; Kuraray Co., Ltd.; Nalco Water (An Ecolab Company); MANN+HUMMEL.

Methodology

USDAnalytics applies a mixed top-down/bottom-up approach, sizing each country by technology, application, end-use, and system configuration, then triangulating with utility capex, industrial water intensity, reuse mandates, PPP/tender pipelines, and tariff structures. Primary research covers interviews with utility managers, plant engineers, OEMs, integrators, and O&M providers to validate kWh/m³, chemical dose, SDI/permeate specs, recovery rates, and payback for centralized and modular deployments. Secondary inputs include regulatory databases (WRAP/EU Water Reuse), project trackers, corporate filings, and peer-reviewed studies to benchmark CAS/BNR, MBR, RO/NF, AOPs, DPR/IPR trains. Scenario modeling stress-tests sensitivities to energy prices, PFAS and nutrient standards, brine salinity, and automation maturity, producing robust 2025–2034 forecasts and decision-grade guidance.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Water Recycle and Reuse Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights: Market Drivers and Technology Trends

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): $18.4 Billion

1.3.2. Projected Market Valuation (2034): $44.1 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 10.2%

2. Market Outlook (2025–2034)

2.1. Introduction: Growth Outlook and Key Insights

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Trends Shaping the Water Reuse Industry

2.3.1. Government Policy and Financial Support for Water Reuse Infrastructure

2.3.2. Corporate Investment in On-Site Industrial Water Recycling

2.3.3. Hybrid Treatment Systems for Diverse Water Sources

3. Innovations and Strategic Developments Driving Market Growth

3.1. Market Analysis: Recent Strategic Developments

3.1.1. VA Tech Wabag Secures Major ZLD and Water Reuse Contracts in India (July-August 2025)

3.1.2. Brunswick County Advances Landmark PFAS Removal Project in the U.S. (July 2025)

3.1.3. Texas Promotes Produced-Water Reuse with New Legislation (June 2025)

3.1.4. Veolia Acquires Full Ownership of Water Technologies and Solutions Subsidiary (May 2025)

3.1.5. European Funding Drives R&D in Anti-Fouling Membranes (March 2025)

3.1.6. Nitto Denko Unveils Carbon-Negative Membrane Technology (October 2024)

4. Competitive Landscape: Key Industry Players

4.1. Competitive Overview: Leaders in Technology and Global Projects

4.2. Strategic Profiles of Key Companies

4.2.1. SUEZ: Strengthening Global Footprint in Wastewater Recycling

4.2.2. Veolia Water Technologies: Expanding Global Reuse Projects

4.2.3. DuPont Water Solutions: Driving Membrane Innovation

4.2.4. Xylem Inc.: Integrated Water Solutions Provider

4.2.5. Aquatech International LLC: Specialist in ZLD and Industrial Reuse

5. Water Recycle and Reuse Market – Segmentation Insights (2025)

5.1. By Technology

5.1.1. Membrane Filtration (32% Market Share)

5.1.2. Physical Treatment (20% Market Share)

5.1.3. Biological Treatment (18% Market Share)

5.1.4. Advanced Hybrid Systems (15% Market Share)

5.1.5. Advanced Treatment (15% Market Share)

5.2. By Application

5.2.1. Industrial Reuse (45% Market Share)

5.2.2. Municipal Reuse (30% Market Share)

5.2.3. Agricultural Reuse (20% Market Share)

5.2.4. Commercial & Residential Reuse (5% Market Share)

5.3. By End-Use Industry

5.3.1. Power Generation (18% Market Share)

5.3.2. Food & Beverage (15% Market Share)

5.3.3. Chemicals & Petrochemicals (14% Market Share)

5.3.4. Municipal Utilities (12% Market Share)

5.3.5. Oil & Gas (11% Market Share)

5.3.6. Other Industries (30% Market Share)

5.4. By System Configuration

5.4.1. Centralized Systems

5.4.2. Decentralized / On-Site Systems

6. Country Analysis: Water Recycle and Reuse Market

6.1. United States: Federal Funding and Innovative Reuse Projects Driving Growth

6.2. China: Stringent Regulations and Membrane Innovations Boost Infrastructure

6.3. India: Policy Support and Infrastructure Expansion Fueling Initiatives

6.4. Singapore: NEWater Project Setting Global Standards in Water Recycling

6.5. Germany: Regulatory Enforcement and Industrial Recirculation

6.6. Saudi Arabia: Strategic Investments and Membrane Technologies

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Market Outlook

7.1.1. By Technology

7.1.2. By Application

7.1.3. By End-Use Industry

7.2. Europe Market Outlook

7.2.1. By Technology

7.2.2. By Application

7.2.3. By End-Use Industry

7.3. Asia Pacific Market Outlook

7.3.1. By Technology

7.3.2. By Application

7.3.3. By End-Use Industry

7.4. South America Market Outlook

7.4.1. By Technology

7.4.2. By Application

7.4.3. By End-Use Industry

7.5. Middle East & Africa Market Outlook

7.5.1. By Technology

7.5.2. By Application

7.5.3. By End-Use Industry

8. Company Profiles: Leading Players

8.1. Veolia

8.2. SUEZ

8.3. Xylem Inc.

8.4. Evoqua Water Technologies

8.5. Pentair plc

8.6. DuPont de Nemours, Inc.

8.7. Toray Industries, Inc.

8.8. Aquatech International

8.9. Kubota Corporation

8.10. The Dow Chemical Company

8.11. V.A. TECH WABAG Ltd.

8.12. Mitsubishi Chemical Corporation

8.13. Kuraray Co., Ltd.

8.14. Nalco Water (An Ecolab Company)

8.15. MANN+HUMMEL

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures