Water Treatment Chemicals Market Overview 2025–2034: $34.7 Billion to $56.7 Billion at 5.6% CAGR Powered by PFAS Remediation, Ultra-Pure Water Systems, and Bio-Based Inhibitors

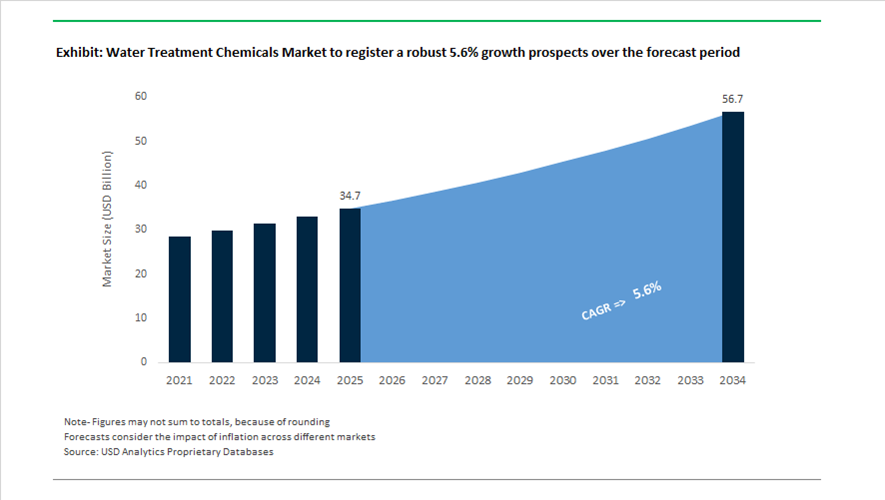

The Water Treatment Chemicals market is valued at $34.7 billion in 2025 and is projected to reach $56.7 billion by 2034, registering a CAGR of 5.6%. Growth is supported by tightening global drinking water standards, PFAS removal mandates, semiconductor-driven ultra-pure water (UPW) demand, and large-scale desalination investments. The market includes coagulants, flocculants, corrosion inhibitors, scale inhibitors, biocides, pH adjusters, membrane cleaning chemicals, and specialty polymers used across municipal water treatment, industrial wastewater management, cooling towers, boiler systems, and desalination plants. Chemical dosing optimization, digital monitoring integration, and sustainable bio-based formulations are reshaping procurement strategies among utilities and industrial end users.

Innovation momentum accelerated in 2024. In April 2024, Gradiant launched CURE Chemicals, a dedicated platform focused on integrating specialty treatment chemistries with IoT-enabled water treatment systems to enhance recovery rates in heavy industrial facilities. In September 2024, a breakthrough PFAS-removal filtration material was introduced, engineered to sequester PFOA and PFOS at sub-nanogram concentrations, aligning with newly established U.S. EPA federal drinking water standards. In March 2025, DuPont Water Solutions launched WAVE PRO, an advanced digital modeling platform for ultrafiltration and reverse osmosis systems that enables operators to optimize chemical dosing and predict membrane performance in municipal and desalination applications. These developments highlight the convergence of chemical treatment programs with real-time analytics and regulatory-driven contaminant removal technologies.

Strategic consolidation intensified through late 2025 and early 2026. In September 2025, Kemira acquired Water Engineering, Inc. for $150 million, marking a significant expansion into North American boiler and cooling tower treatment services. In November 2025, Solenis completed the acquisition of NCH Corporation’s water treatment portfolio, combining specialty chemistries with digital monitoring tools targeting food & beverage and institutional markets. In December 2025, Ecolab finalized its $1.8 billion acquisition of Ovivo’s Electronics UPW division, strengthening its footprint in semiconductor and high-tech manufacturing water systems. In February 2026, Kemira acquired SIDRA Wasserchemie to reinforce its European municipal and industrial wastewater presence, particularly in Germany. In January 2026, Windjammer Capital acquired MFG Chemical to scale polymer manufacturing for clarification applications. The same month, Kurita America partnered with Solugen to introduce Kurita TowerNG, a line of bio-based corrosion and scale inhibitors produced using chemienzymatic processes, with manufacturing scheduled to expand in Minnesota in late 2026.

Infrastructure expansion further underpins chemical demand. Construction progressed through 2025–2026 on the Perur Desalination Plant in India, projected to become Southeast Asia’s largest facility upon completion in late 2026, utilizing large volumes of reverse osmosis treatment chemicals and lamella clarification systems supplied by a consortium including VA TECH WABAG. In February 2026, India’s Union Budget allocated ₹600 crore to establish three dedicated chemical parks equipped with shared water treatment and environmental compliance infrastructure to accelerate domestic specialty chemical production.

Trends and Opportunities in the Water Treatment Chemicals Market

Regulatory, Digital, and Performance-Led Shifts Reshaping Water Treatment Chemicals Demand

The water treatment chemicals market is undergoing a structural transformation in 2024–2026, driven by enforceable PFAS regulations, digitization of chemical management, and outcome-linked commercial models. Demand is no longer defined by volume growth alone but by regulatory resilience, audit-readiness, and the ability of chemical programs to deliver measurable reductions in water use, energy consumption, and operational risk. These forces are reshaping supplier portfolios across municipal, food and beverage, healthcare, and semiconductor manufacturing end users.

Trend 1: Strategic Portfolio Restructuring to Eliminate PFAS and Meet Global Mandates

The elimination of PFAS from water treatment chemistries has moved decisively from voluntary stewardship to mandatory compliance. In September 2025, U.S. Environmental Protection Agency reaffirmed the designation of PFOA and PFOS as hazardous substances under CERCLA, legally assigning cleanup liability to manufacturers and users. This regulatory shift has materially altered supplier risk exposure, triggering accelerated reformulation of surfactants, dispersants, and defoamers historically reliant on fluorinated chemistry.

Simultaneously, the U.S. Food and Drug Administration rendered 35 PFAS-related Food Contact Notifications inactive as of January 1, 2025. This action has had immediate downstream effects on water treatment chemical programs in the food and beverage sector, where process water compliance is now subject to stricter federal scrutiny. Suppliers servicing breweries, dairy processors, and beverage bottlers have been forced to deploy silicone-free, non-fluorinated alternatives that can pass third-party audits without disrupting cleaning-in-place or reuse systems. As a result, PFAS-free water treatment formulations are no longer premium offerings but baseline requirements for supplier qualification.

Trend 2: Shift to Outcome-Based Models via IoT and AI Chemical Optimization

The commercialization model for water treatment chemicals is shifting toward Chemicals-as-a-Service, where pricing and renewals are linked to outcomes such as reduced corrosion rates, minimized scaling, or lower water withdrawal intensity. This transition is enabled by real-time monitoring and AI-driven analytics.

Global providers such as Ecolab are scaling platforms like 3D TRASAR™ and ECOLAB3D™, which integrate smart sensors with predictive algorithms to monitor corrosion, biofouling, and scaling in real time. Field data from 2024–2025 deployments show that AI-guided optimization can reduce chemical overfeed and associated energy use by up to 25%, directly aligning supplier revenue with customer ESG and cost targets.

In parallel, Suez expanded its Digital Twin solutions in early 2025, enabling industrial operators to simulate dosing scenarios under fluctuating raw water quality and load conditions. These virtual models are delivering documented chemical OPEX reductions of 15–20% by eliminating conservative overdosing practices, a critical advantage as raw material prices remain volatile and procurement teams demand tighter cost control.

Opportunity 1: Legionella Risk Mitigation in Large-Scale Building Systems

Public health enforcement and updated building codes are creating a durable, compliance-driven opportunity for specialized water treatment chemicals in complex building plumbing systems. The 2025 update to ASHRAE Standard 188 now requires most human-occupied buildings to implement a formal Water Management Program, including documented disinfectant residual control and risk assessments for Legionella.

This mandate has converted what was previously an episodic service into a recurring chemical and monitoring requirement for hospitals, hotels, senior living facilities, and large commercial buildings. Demand is accelerating for stabilized oxidizing biocides, secondary disinfectants, and automated dosing systems capable of maintaining residuals across low-flow and stagnant zones. Post-pandemic guidance from public health agencies has further intensified institutional demand for real-time microbial monitoring and audit-ready chemical programs, particularly in healthcare environments where tolerance for failure is effectively zero.

Opportunity 2: High-Purity Chemical Trains for Semiconductor Water Circularity

The rapid expansion of semiconductor fabrication capacity is creating one of the most technically demanding growth segments for water treatment chemicals. Advanced fabs now target near-total water reuse, requiring chemical programs that function at extreme purity thresholds without introducing ionic or organic contamination.

In November 2025, Gradiant reported achieving 99% water recycling at a USD 300 million semiconductor facility, enabled by advanced coagulants, metal-specific chelants, and next-generation antiscalants capable of removing trace copper and heavy metals. These chemical trains are foundational to enabling circular reuse of cooling tower blowdown and scrubber wastewater.

This opportunity is structurally reinforced by CHIPS Act-driven fab investments. Intel and TSMC have publicly committed to Net Positive Water targets by 2030, with Intel’s June 2025 water policy stating that reclaimed water will support 60% of global operations. Meeting these commitments requires ultra-pure, non-interfering water treatment chemistries that can operate within Ultrapure Water systems without compromising yield. Suppliers capable of delivering semiconductor-grade, PFAS-free, and digitally optimized chemical programs are positioned to capture long-term, high-margin contracts in this expansion cycle.

Water Treatment Chemicals Market Share and Segmentation Insights

Product Type Market Share: Coagulants and Flocculants Lead with High-Volume Water Clarification Demand

Coagulants and flocculants account for 32.80% of the water treatment chemicals market in 2025, driven by their essential role in removing suspended solids, turbidity, and organic matter across municipal and industrial water treatment systems. Their continuous use in large-scale water processing ensures consistent demand across drinking water and wastewater applications. Corrosion and scale inhibitors, biocides and disinfectants, pH adjusters, chelating agents, and antifoaming agents support complementary treatment functions. A key trend is the optimization of coagulant chemistry for emerging contaminant removal, including microplastics, PFAS, and pharmaceutical residues, with advanced polymer formulations improving treatment efficiency and regulatory compliance.

Application Market Share: Wastewater Treatment Leads with Rising Reuse and Regulatory Compliance Demand

Wastewater treatment holds a 38.60% share in the water treatment chemicals market in 2025, reflecting the increasing need to treat municipal and industrial effluents before discharge or reuse. Chemical processes such as coagulation, disinfection, and pH control are critical for meeting stringent environmental standards. Cooling water, boiler water, raw water treatment, desalination, and effluent treatment plants contribute to broader market demand. A key growth driver is the expansion of water reuse initiatives, where advanced treatment systems require additional chemical inputs for membrane protection, nutrient removal, and pathogen control, supporting the transition toward sustainable water management practices.

Water Treatment Chemicals Market Competitive Landscape

The Water Treatment Chemicals market in 2026 is defined by outcome-based service models, IIoT-enabled monitoring, and digital twin simulations, with strong demand for PFAS remediation chemicals, ZLD enhancers, and energy-efficient formulations transforming industrial water treatment into performance-driven, OPEX-focused solutions.

Ecolab Strengthens Digital Water Stewardship with AI-Driven Chemical Optimization Platforms

Ecolab, through Nalco Water, leads the Water Treatment Chemicals market with advanced IIoT-enabled monitoring and predictive analytics platforms. The acquisition of Ovivo’s Electronics UPW business expands its footprint in semiconductor-grade water treatment for sub-10 nm fabrication. Its 3D TRASAR™ technology supports direct-to-chip cooling in AI-driven data centers, optimizing chemical dosing while reducing water consumption. The ECOLAB3D™ platform manages over 40,000 systems globally, preventing scaling, corrosion, and biofouling through real-time analytics. Strong financial performance with projected EPS growth of 12–15% reflects the success of its value-based pricing strategy. This integration of digital intelligence and chemical expertise strengthens its leadership in Water-as-a-Service models.

Solenis Expands 360-Degree Water Treatment Services with Sustainability-Driven Innovation

Solenis is rapidly advancing in the Water Treatment Chemicals market through strategic acquisitions and a unified global service model. The acquisition of NCH Corporation expands its reach into mid-market industrial and institutional water treatment segments. The company derives 74% of its revenue from sustainability-linked solutions, with 91% of its R&D pipeline focused on green chemistry and circularity. Its Delaware Global Research Center accelerates development of next-generation water treatment chemicals and renewable polymers. The ValueAdvantageSM program delivered $349 million in customer value through chemical optimization in 2025. This integrated digital and service-oriented approach positions Solenis as a key player in outcome-based water management.

SNF Group Drives Polymer-Based Water Treatment with Vertical Integration and Green Chemistry

SNF Group dominates the Water Treatment Chemicals market through its leadership in water-soluble polymers and vertically integrated production capabilities. The acquisition of Syensqo’s Oil & Gas division expands its portfolio with over 700 specialized products for high-performance applications. Its EcoVadis Platinum rating strengthens its position in sustainability-driven municipal contracts. SNF’s €540 million annual investment supports capacity expansion for bio-based acrylamides across global facilities. Vertical integration in acrylamide production enables cost stability and strong EBITDA margins despite feedstock volatility. This scale and integration reinforce its leadership in polymer-based coagulants and flocculants.

Kemira Advances Nutrient Removal and Bio-Based Chemical Solutions for Regulatory Compliance

Kemira is strengthening its position in the Water Treatment Chemicals market through advanced coagulants and regulatory-driven innovation. Expansion of ferric sulphate capacity in the UK aligns with tightening phosphorus discharge limits under AMP8 regulations. Collaboration with Solugen enables the development of bio-based scale inhibitors using chemienzymatic processes. The Kemira Water Index highlights growing concern over water scarcity, reinforcing demand for cost-efficient treatment solutions. The company is piloting phosphorus recovery systems to convert waste streams into reusable raw materials. This focus on nutrient removal and circular chemistry supports its leadership in municipal water treatment.

Kurita Expands High-Purity Chemical Solutions with AI-Optimized Membrane and Semiconductor Applications

Kurita Water Industries is advancing in the Water Treatment Chemicals market through high-purity formulations and AI-driven process optimization. Increased R&D investment supports the development of advanced chemicals for semiconductor manufacturing, focusing on Total Organic Carbon control and ultra-clean water systems. The integration of Avista Technologies enhances its membrane treatment portfolio for desalination and industrial reuse applications. Expansion in North America strengthens its regional supply capabilities for high-performance chemicals. The Meta-Aqua platform utilizes AI to optimize facility design and extend membrane lifespan, improving operational efficiency by up to 15%. This focus on advanced materials and digital optimization strengthens Kurita’s competitive positioning in high-growth industrial sectors.

United States Water Treatment Chemicals Market Shaped by PFAS Timelines, Federal Funding, and Digital Dosing

The United States water treatment chemicals market is navigating a regulatory recalibration phase that is extending procurement runways while accelerating near-term upgrades. In May 2025, the Environmental Protection Agency announced a strategic extension of compliance timelines for the National Primary Drinking Water Regulation covering PFOA and PFOS, pushing final enforcement to 2031. This decision effectively creates a 24-month planning window for utilities to scale adoption of high-selectivity ion-exchange resins and granular activated carbon, prioritizing systems that protect downstream assets and deliver predictable breakthrough performance. Utilities are using this window to phase investments, standardize resin regeneration strategies, and align chemical supply contracts with long-term compliance trajectories.

Capital availability is reinforcing demand momentum. As of early 2026, more than $30 billion under the Infrastructure Investment and Jobs Act has been released for water infrastructure, triggering a measurable increase in municipal retrofits that rely on coagulants and flocculants for enhanced primary and secondary treatment. Technology is further optimizing chemical use. In late 2025, Ecolab through its Nalco Water platform deployed AI-driven dosing across dozens of U.S. data centers, achieving double-digit reductions in chemical consumption via real-time monitoring and control. Competitive dynamics are consolidating as well. Solenis completed the integration of NCH’s industrial business in 2025, broadening its mid-market footprint in biocides and corrosion inhibitors. At the state level, new restrictions in Maine and California on PFAS-containing biosolids are catalyzing development of chemical locking agents used during sludge dewatering to immobilize contaminants and ensure compliant disposal pathways.

China Water Treatment Chemicals Market Accelerated by Green Standards, ZLD Mandates, and Metals Partnerships

China’s water treatment chemicals market is expanding on the back of large-scale industrial investment and a tightening regulatory environment. The late-2025 commissioning of the Zhanjiang Verbund site by BASF marks a pivotal capacity addition, integrating advanced water treatment additives and controlled free-radical polymerization dispersants within a highly efficient production ecosystem. This localized supply is aligning with China’s industrial decarbonization and water reuse priorities.

Regulatory pressure is intensifying. Mandatory standards issued by the State Administration for Market Regulation under GB 30981.1-2025 will take effect in June 2026, strictly limiting harmful substances in water-based industrial additives and accelerating the phase-out of nonylphenol ethoxylates. Concurrently, a 2025 directive from the Ministry of Water Resources requires industrial parks in the Yangtze River basin to implement Zero Liquid Discharge, driving strong domestic demand for high-performance antiscalants and specialty dispersants. Sustainability credentials are becoming differentiators. The BASF Nanjing Verbund site received Carbon Trust validation for low-carbon formic acid used as a pH adjuster in eco-sensitive applications. In metals, Nalco Water’s 2025 partnership with Danieli is scaling tailored chemical programs for Chinese steelmakers to cut water footprint per ton, embedding chemical optimization into core production KPIs.

Saudi Arabia Water Treatment Chemicals Market Anchored in Desalination Conversion and Circular Reuse

Saudi Arabia’s water treatment chemicals market is being reshaped by desalination modernization and circular water mandates under Vision 2030. In September 2025, the Saudi Water Authority secured a substantial financing package to convert aging multi-stage flash assets to reverse osmosis. This transition is shifting demand profiles toward specialized membrane cleaners, antiscalants, and biofouling control chemistries that protect RO performance under high salinity and variable feed conditions.

Mega-projects are adding differentiated demand. NEOM’s 2025 commitment to 100% renewable desalination is advancing selective brine mining chemistries that recover magnesium and lithium from reject streams, linking water treatment chemicals with resource valorization. In hydrocarbons, Saudi Aramco increased investment in water-injection chemicals for enhanced oil recovery in late 2025, prioritizing oxygen scavengers and biocides to maintain integrity across high-salinity systems. Urban reuse targets are also catalytic. The mandate to recycle all treated wastewater in cities has expanded markets for quaternary ammonium compounds and advanced disinfectants, positioning chemical suppliers as enablers of large-scale reuse.

European Union Water Treatment Chemicals Market Defined by Quaternary Treatment and Producer Responsibility

Across the European Union, water treatment chemicals demand is being reoriented toward micropollutant removal and energy performance, with Germany and Spain at the forefront. The recast Urban Wastewater Treatment Directive requires Member States to submit national implementation programs by 2026, mandating quaternary treatment at large facilities. This is accelerating adoption of advanced oxidation process chemistries, ozone-based systems, and specialty activated carbon dispersions designed for pharmaceuticals and cosmetics removal.

Supply investments are responding. In July 2025, Kemira announced a €20 million expansion in Tarragona, Spain, adding Aluminium Chloro Hydrate capacity to meet rising demand for high-performance coagulants. Policy design is shaping procurement incentives. From 2026, the Extended Producer Responsibility framework obliges pharmaceutical and cosmetic companies to fund the majority of micropollutant removal costs, favoring solutions with predictable operating profiles and verifiable removal efficiencies. In Germany, updated requirements under the Water Act are pushing wastewater plants toward energy neutrality, increasing the use of additives that enhance anaerobic digestion stability and biogas yield.

India Water Treatment Chemicals Market Supported by PLI Manufacturing and Rural Scale-Up

India’s water treatment chemicals market is expanding through a combination of domestic manufacturing incentives and nationwide service delivery programs. The Production Linked Incentive scheme for advanced chemicals achieved realized investments of ₹1.76 lakh crore by March 2025, supporting local production of polyacrylamides and synthetic flocculants and reducing reliance on imports. This capacity build-out is aligning with rising municipal and industrial demand for reliable, cost-effective treatment inputs.

Public programs are sustaining volume demand. Continued allocations under the Jal Jeevan Mission in the 2025–26 budget are supporting bulk procurement of disinfectants such as bleaching powder and liquid chlorine across hundreds of thousands of villages. Industrial compliance is adding a premium layer. Mandatory Zero Liquid Discharge for new chemical units implemented by the Gujarat Industrial Development Corporation in 2025 is boosting demand for specialty defoamers and chelating agents capable of handling complex effluents before membrane systems. Together, these drivers are positioning India as both a high-volume consumption market and an increasingly self-reliant manufacturing base for water treatment chemicals.

Summary of Country-Level Water Treatment Chemicals Market Dynamics

Water Treatment Chemicals Market County Level Snapshot

|

Country / Region

|

Primary Policy or Investment Driver

|

Key Chemical Classes in Demand

|

Strategic Market Role

|

|

United States

|

PFAS timelines and IIJA funding

|

Ion exchange, GAC, coagulants

|

Compliance-led modernization

|

|

China

|

Green standards and ZLD mandates

|

Antiscalants, dispersants, pH control

|

Industrial reuse scale-up

|

|

Saudi Arabia

|

Desalination conversion and reuse

|

RO cleaners, disinfectants

|

Circular water transformation

|

|

European Union

|

Quaternary treatment and EPR

|

AOP chemicals, ACH, activated carbon

|

Micropollutant removal leader

|

|

India

|

PLI manufacturing and rural rollout

|

Flocculants, disinfectants

|

Volume growth with localization

|

Water Treatment Chemicals Market Report Scope

Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$34.7 Billion

|

|

Market Size (2034)

|

$56.7 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Product Type (Coagulants and Flocculants, Biocides and Disinfectants, Corrosion and Scale Inhibitors, pH Adjusters and Softeners, Chelating Agents, Antifoaming Agents), By Application (Raw Water Treatment, Boiler Water Treatment, Cooling Water Treatment, Wastewater Treatment, Desalination, Effluent Treatment Plants), By End-Use Industry (Municipal, Oil and Gas, Power Generation, Chemical Manufacturing, Food and Beverage, Semiconductors and Data Centers)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc., Solenis, BASF SE, Kemira Oyj, Kurita Water Industries Ltd., Veolia Group, SNF Group, DuPont Water Solutions, Suez SA, VA Tech WABAG, Aramco Chemicals Company, Lonza Group, Buckman Laboratories International, Dow Chemical Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Treatment Chemicals Market Segmentation

By Product Type

- Coagulants and Flocculants

- Biocides and Disinfectants

- Corrosion and Scale Inhibitors

- pH Adjusters and Softeners

- Chelating Agents

- Antifoaming Agents

By Application

- Raw Water Treatment

- Boiler Water Treatment

- Cooling Water Treatment

- Wastewater Treatment

- Desalination

- Effluent Treatment Plants

By End-Use Industry

- Municipal

- Oil and Gas

- Power Generation

- Chemical Manufacturing

- Food and Beverage

- Semiconductors and Data Centers

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Water Treatment Chemicals Market

- Ecolab Inc.

- Solenis

- BASF SE

- Kemira Oyj

- Kurita Water Industries Ltd.

- Veolia Group

- SNF Group

- DuPont Water Solutions

- Suez SA

- VA Tech WABAG

- Aramco Chemicals Company

- Lonza Group

- Buckman Laboratories International

- Dow Chemical Company

*- List not Exhaustive