Waterborne Coatings Market Size Expansion Fueled by Low-VOC Transition and Advanced Resin Technologies

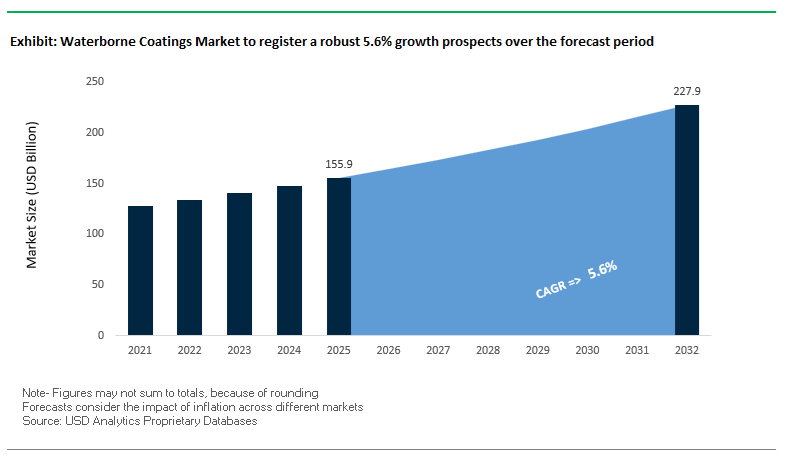

The global Waterborne Coatings Market was valued at $155.9 billion in 2025 and is projected to grow at a CAGR of 5.6% from 2025 to 2032, reaching $228.3 billion by 2032. This growth reflects a decisive global shift toward low-VOC, environmentally compliant coating technologies, as industries across construction, automotive, packaging, and industrial manufacturing transition away from solvent-based systems. Waterborne coatings have become the preferred solution due to their reduced emissions, enhanced workplace safety, regulatory compliance, and improved lifecycle sustainability performance.

A central growth driver is the rapid advancement of waterborne resin chemistries, including acrylics, polyurethanes, alkyd hybrids, and UV-curable dispersions, which now deliver performance parity—or superiority—compared to solvent-based coatings. These innovations are enabling enhanced adhesion, corrosion resistance, weatherability, and gloss retention, while also improving process efficiency through faster drying times and lower curing energy requirements. Additionally, the increasing adoption of electric vehicles (EVs), lightweight materials, and smart infrastructure systems is accelerating demand for specialized waterborne coatings tailored to high-performance and multi-substrate applications.

Sustainability continues to be a defining pillar of market expansion. Manufacturers are prioritizing bio-based raw materials, circular economy principles, and carbon footprint reduction strategies, aligning with global decarbonization targets and environmental regulations. The growing emphasis on green building certifications, eco-labeling standards, and sustainable packaging solutions is further reinforcing demand for waterborne coatings across architectural and industrial segments. Furthermore, the rise of functional coatings—including antimicrobial, anti-corrosion, heat-reflective, and UV-resistant systems—is expanding the application scope of waterborne technologies.

Market Analysis: Sustainability Certification, Digital Platforms, and Advanced Material Innovation Reshaping Competitive Landscape

The Waterborne Coatings Market is undergoing a structural transformation driven by sustainability certifications, digitalization, and advanced material innovation, as leading players intensify efforts to differentiate through performance and environmental compliance. A major milestone is Arkema’s ISCC PLUS certification achievement (January 2026), with over 70% of its global coating facilities now certified, enabling the supply of bio-attributed resins and additives with at least 20% lower product carbon footprint (PCF). This development underscores the growing importance of traceability, renewable feedstocks, and low-carbon manufacturing processes in the coatings value chain.

Digital transformation is emerging as a key competitive lever. In February 2026, Arkema launched its centralized Coating Materials digital platform, designed to provide integrated access to technical data, regulatory compliance tools, and formulation guidance for waterborne and energy-curable systems. This platform specifically targets high-growth sectors such as e-mobility, data centers, and sustainable urban infrastructure, streamlining product selection and accelerating innovation cycles.

Material innovation continues to redefine performance benchmarks. Covestro’s expansion of its waterborne UV resin portfolio (2025–2026) introduces advanced formulations capable of delivering instant hardness, ultra-low VOC emissions, and compatibility with high-speed industrial coating processes, particularly in wood and flooring applications. Similarly, AkzoNobel’s RUBBOL WF 3350 bio-based coating, featuring 20% renewable content verified through ASTM standards, highlights the increasing integration of plant-derived materials in high-performance coatings.

Capacity expansion and regional manufacturing strategies are also shaping market dynamics. PPG’s commissioning of its Thailand-based waterborne coatings plant (March 2025)—with a capacity of 2,000 tons annually—positions Southeast Asia as a strategic hub for automotive OEM coatings, particularly supporting the rapid growth of EV production by Chinese manufacturers. Meanwhile, Axalta’s record 2025 performance and “2026 A Plan” execution emphasize the growing adoption of eco-friendly waterborne systems in mobility coatings, particularly in North America and China.

Innovation in specialty coatings is expanding application boundaries. CRX Coatings’ graphene-enhanced waterborne marine paint (November 2024) demonstrates the ability of waterborne systems to deliver high-performance corrosion resistance and biofouling protection, traditionally dominated by solvent-based alternatives. Additionally, Siegwerk’s acquisition of Allinova (August 2025) strengthens its capabilities in PFAS-free waterborne barrier coatings, aligning with increasing regulatory pressure in the packaging sector.

Further reinforcing this trajectory, PPG’s 2026 “Parallels” design theme and BASF’s “Driving the Proxy” collection highlight the role of waterborne basecoat systems in enabling advanced color technologies, adaptive finishes, and sustainable automotive coatings. Collectively, these developments signal a market transitioning toward digitally enabled, sustainability-driven, and high-performance coating solutions, supported by certification frameworks, advanced resin technologies, and evolving end-user requirements.

Market Trend: CARB SCM 2025–2026 Enforcement Accelerating Ultra-Low VOC Waterborne Coatings Adoption

The expansion of the California Air Resources Board Suggested Control Measure across major urban districts is significantly reshaping the global waterborne coatings market, establishing the 50 g/L VOC cap as a dominant regulatory benchmark. The alignment of multiple states under the Ozone Transport Commission model is accelerating the transition toward ultra-low VOC waterborne coatings, particularly in architectural and decorative coatings segments.

Under 2026 enforcement, even high-gloss and non-flat coatings are being reformulated to comply with the 50 g/L VOC threshold, driving a shift away from conventional coalescing agents such as Texanol. Manufacturers are increasingly adopting reactive diluents that chemically integrate into the resin matrix, preserving film formation while eliminating VOC contribution. This transformation is reinforcing the demand for advanced low-VOC coating technologies and environmentally compliant formulations.

To ensure performance parity, next-generation waterborne acrylic coatings are incorporating self-crosslinking technologies that enhance durability and adhesion. These coatings achieve Class 1 scrub resistance as per ISO 11998, with less than 5 microns of film loss after 200 cycles. This demonstrates that ultra-low VOC coatings can deliver high durability and long service life, strengthening their adoption in residential, commercial, and institutional construction markets.

Market Trend: China GB/T 41660-2025 Standard Driving Hygrothermal Stability in High-Humidity Applications

China’s GB/T 41660-2025 standard is elevating performance expectations in the waterborne coatings industry, particularly by prioritizing hygrothermal stability in high-humidity environments. This regulatory shift is critical for regions affected by monsoon climates, where moisture-induced coating failure has historically been a major challenge.

The 2026 standard mandates a wet-state bond strength of at least 0.4 MPa after 168 hours of continuous water immersion. This requirement is effectively eliminating low-quality emulsions from the commercial construction market, driving demand for polymer-modified and high-performance waterborne coatings with superior moisture resistance.

Additionally, coatings must demonstrate zero chalking performance, achieving a Rating of 0 under ASTM D4214 after 500 hours of accelerated weathering. This benchmark has become a prerequisite for government-led infrastructure projects, reinforcing the importance of long-term durability and weather resistance in modern coating formulations. These standards are accelerating innovation in high-durability waterborne coatings and strengthening their role in large-scale infrastructure development across Asia-Pacific markets.

Market Opportunity: Bio-Based Waterborne Coatings Driving Growth in Sustainable Coatings Market

The shift toward sustainable materials is creating strong opportunities for bio-based waterborne coatings, particularly those incorporating renewable raw materials such as soybean oil, cardanol, and lignin. In 2026, formulations achieving bio-based carbon content of 25% or higher, validated through ASTM D6866, are gaining significant traction in green building and eco-friendly coatings markets.

These bio-based coatings enable a reduction of 20% to 30% in cradle-to-gate carbon emissions, making them highly attractive for developers targeting LEED Platinum and WELL v2 certifications. The integration of renewable materials is also aligning the waterborne coatings industry with global decarbonization goals and circular economy initiatives.

Importantly, performance parity has been achieved, with advanced bio-based polyurethane dispersions matching the mechanical properties of conventional coatings. These formulations deliver König hardness values between 150 and 180 seconds and tensile strength of 30 MPa or higher, making them suitable for demanding applications such as furniture coatings, industrial finishes, and sustainable packaging solutions. This convergence of sustainability and performance is driving rapid adoption of bio-based coatings across multiple end-use industries.

Market Opportunity: Anti-Viral and Formaldehyde-Eliminating Coatings Advancing Functional Coatings Market Growth

The emergence of functional coatings is creating significant opportunities in the waterborne coatings market, particularly through anti-viral and formaldehyde-eliminating technologies designed to improve indoor air quality and hygiene. These coatings are increasingly specified in healthcare, education, and public infrastructure projects where environmental safety and occupant health are critical considerations.

Advanced waterborne coatings incorporate functionalized amine groups within the binder system to chemically capture and neutralize formaldehyde emissions. Laboratory testing based on ISO 16000-23 standards indicates that these coatings can reduce ambient formaldehyde levels by 80% or more within 24 hours of application. This capability is particularly valuable in mitigating indoor air pollution caused by off-gassing materials.

In addition to air purification, anti-viral coatings utilizing nano-silver and copper-ion encapsulation technologies are demonstrating more than 99.9% reduction in viral load according to ISO 21702 standards. These coatings provide a durable protective layer that remains effective throughout a typical five-year maintenance cycle, making them ideal for high-risk environments such as hospitals and public facilities.

Field applications in 2026 school retrofit projects have shown that the use of formaldehyde-scavenging coatings contributes to approximately 12% improvement in indoor environmental quality scores. This measurable impact is facilitating faster regulatory approvals and strengthening the adoption of functional waterborne coatings as a key component of healthy building design.

Waterborne Coatings Market Share and Segmentation Insights

Waterborne Dispersions (Latex) Dominate with 61.8% Share as Backbone of Architectural Coatings

The waterborne dispersions (latex) segment leads the global waterborne coatings market with a dominant 61.8% market share in 2025, driven by its widespread use in architectural paints and decorative coatings applications. In the water-based paints and sustainable coatings market, latex dispersions such as acrylic, vinyl-acrylic, and styrene-acrylic systems form the foundation of interior and exterior wall paints, accounting for the largest volume consumption globally. These coatings offer excellent film formation, adhesion, flexibility, and durability, making them ideal for residential and commercial construction. A key innovation driving growth is the ability to formulate modern latex coatings without coalescing solvents, enabling ultra-low VOC and zero-VOC paints that comply with green building standards such as LEED, BREEAM, and WELL certifications. As sustainability regulations tighten and demand for eco-friendly, high-performance coatings rises, latex dispersions continue to dominate the global waterborne coatings market.

Retail and DIY Centers Lead with 43.5% Share Driven by Convenience and Color Customization

The retail and DIY centers segment dominates the waterborne coatings market with a 43.5% market share in 2025, fueled by strong demand from homeowners and small-scale painting contractors. Within the architectural coatings distribution and home improvement retail market, major chains such as Home Depot, Lowe’s, and B&Q serve as primary purchasing hubs for waterborne paints sold in quart and gallon packaging. A key growth driver is the increasing popularity of DIY home renovation and repainting projects, where consumers prioritize ease of access, product variety, and immediate availability. Retail outlets enhance the buying experience by offering advanced color matching and tinting services, paint samples, and extended weekend hours, making them highly attractive for both DIY users and professionals. This combination of convenience, competitive pricing, and customization options reinforces the dominance of retail channels in the global waterborne coatings market.

Competitive Landscape Analysis of the Waterborne Coatings Market

AkzoNobel Reinforces Market Leadership Through Axalta Merger and Smart Coating Technologies

AkzoNobel N.V. is consolidating its leadership in the waterborne coatings market through a landmark all-stock merger with Axalta Coating Systems, creating a global powerhouse with a combined revenue base of USD 17 billion and enterprise value of USD 25 billion. The company introduced a drone-based aircraft paint inspection tool in April 2026, reducing maintenance downtime by 25% while ensuring coating integrity. Its “Rhythm of Blues” 2026 color collection enhances aesthetic performance in waterborne architectural coatings. Additionally, AkzoNobel streamlined operations by divesting its Pakistan business, allowing greater focus on low-carbon marine, aerospace, and protective coatings in high-growth EMEA and APAC regions.

PPG Expands AI-Driven Waterborne Coatings and Infrastructure Solutions

PPG Industries, Inc. is strengthening its competitive position in the waterborne coatings market through pricing strategies, acquisitions, and innovation. In 2026, the company achieved an 80 basis point margin expansion supported by a 15–20% global price increase. Its acquisition of Ozark Materials significantly enhances its portfolio in waterborne pavement markings and infrastructure coatings, a segment experiencing strong demand from smart city projects. PPG’s AI-powered DELTRON® NXT system improves application efficiency by reducing coating time by 15%. With 43% of revenue derived from sustainably advantaged products, PPG is leading in zero-VOC latex paints and waterborne automotive coatings.

Sherwin-Williams Dominates Contractor Market with Integrated Waterborne Systems

The Sherwin-Williams Company maintains a dominant position in the waterborne coatings market, holding a 63% share of the U.S. professional contractor channel. The company reported a 6.8% increase in net sales to USD 5.67 billion in early 2026, driven by its Performance Coatings Group. Its strategy focuses on “Warm Minimalism” color trends to capture commercial MRO demand. Sherwin-Williams leverages its network of over 4,800 stores to provide real-time supply of high-build waterborne primers with 20% better coverage. The integration of BASF’s Decorative Paints business strengthens its expansion into the European DIY market with premium water-based emulsions.

Nippon Paint Expands APAC Dominance with Strategic Acquisitions and Bio-Based Innovation

Nippon Paint Holdings is a leading player in the waterborne coatings market, particularly in the Asia-Pacific region, which accounts for 39.77% of global demand. The company expanded its workforce in India to 2,399 employees by March 2026, reflecting aggressive regional growth. Its acquisition of Vibgyor Paints strengthens its presence in South Asian industrial coatings for infrastructure and railways. Nippon Paint is also driving sustainability through its HERizons initiative and collaboration with Humble Bee to develop bio-based resin technologies. The launch of n-SHIELD, a water-based adhesive coating for architectural glass and protection films, highlights its innovation in functional coatings applications.

BASF Leads Functional Coatings and AI-Optimized Waterborne Resin Technologies

BASF SE plays a critical role in the waterborne coatings market through its leadership in functional packaging coatings and advanced resin technologies. Its waterborne barrier coatings are becoming the standard for oxygen and moisture protection in food packaging. BASF has developed 2K waterborne polyurethane systems offering corrosion resistance comparable to solvent-based epoxies, enabling compliance with stringent regulations. The company is leveraging AI to optimize resin molecular structures, achieving a 30% reduction in drying energy. Its Specialty Additives segment reported a 12% volume increase, driven by demand for high-performance architectural coating additives.

China’s “Blue Sky” Industrial Transition Accelerating Waterborne Coatings Adoption

China continues to dominate the global waterborne coatings market, driven by stringent environmental mandates under the Fourteenth Five-Year Plan and aggressive green manufacturing policies. The introduction of updated national standards such as GB 45671-2025 and GB 45320-2025 has significantly tightened safety, fire resistance, and technical specifications for coatings, reinforcing the shift toward eco-friendly, water-based technologies. These regulatory frameworks are accelerating the transition away from solvent-based coatings across industrial and infrastructure applications.

Infrastructure expansion remains a major growth catalyst, with extensive use of water-based coatings in next-generation projects including 5G base stations, ultra-high voltage grids, and high-speed rail networks. Industrial capacity is also expanding, particularly in water-borne polyurethane dispersions (PUDs), to meet rising demand from consumer electronics and advanced manufacturing sectors. China’s leadership in electric vehicles is further driving innovation, with increased adoption of water-borne intumescent coatings for battery protection. Additionally, smart building projects in the Greater Bay Area are integrating advanced water-based coatings with thermal insulation and self-cleaning capabilities, highlighting the country’s push toward sustainable urbanization.

United States: Regulatory Push and Clean-Label Innovation Driving Market Growth

The United States waterborne coatings market is undergoing a transformation driven by federal VOC reduction targets and increasing demand for high-performance, sustainable coating solutions. New regulatory goals aiming for a 25% reduction in VOC emissions by 2027 are accelerating the adoption of water-borne systems across key sectors such as automotive, aerospace, and infrastructure maintenance.

The Infrastructure Investment and Jobs Act (IIJA) is a key growth driver, promoting the use of water-borne acrylic epoxy hybrids for public works projects due to their fast-drying properties and durability. In parallel, the shift toward PFAS-free formulations is reshaping the competitive landscape, with manufacturers reformulating products to comply with evolving environmental regulations. The adoption of bio-based raw materials, including soy-derived resins, is further supporting low-carbon construction initiatives. Technological advancements such as water-borne UV-cured coatings are enhancing productivity by reducing drying times, while capacity expansions by leading companies are strengthening the domestic supply of advanced water-based coatings.

Germany: Bio-Based Innovation and Circular Economy Leadership

Germany stands as a global leader in sustainable waterborne coatings, driven by strong regulatory frameworks and advanced R&D capabilities. The country’s focus on bio-based materials and circular economy principles is accelerating the development of eco-friendly coatings with high renewable content. Industry events such as Biobased Coatings Europe 2026 highlight the growing commercialization of water-borne coatings with significant bio-based composition, particularly in wood and industrial applications.

Stringent environmental regulations, including the Industrial Emissions Directive, are pushing manufacturers toward high-performance water-borne systems capable of delivering solvent-like durability. Germany’s renewable energy transition is also creating demand for specialized coatings used in wind turbine infrastructure, while emerging sectors such as hydrogen energy are driving the development of advanced epoxy coatings with zero-porosity properties. Innovation in preservative-free formulations is catering to health-conscious consumers, while advancements in self-crosslinking resins are enhancing performance in high-traffic environments such as hospitals and industrial facilities.

India: Infrastructure Expansion and Rapid Shift to Water-Based Technologies

India is one of the fastest-growing markets for waterborne coatings, supported by large-scale infrastructure development and increasing environmental awareness. Major domestic players are investing heavily in water-borne production capabilities, with significant capital expenditure directed toward establishing dedicated manufacturing hubs. This expansion is enabling the transition from traditional coatings to high-performance water-based emulsions across multiple end-use sectors.

Government initiatives such as the Smart Cities Mission and Pradhan Mantri Awas Yojana are key demand drivers, creating substantial consumption of water-based architectural coatings for residential and infrastructure projects. The automotive refinish sector is also witnessing a shift toward water-borne basecoats, driven by stricter urban air quality standards and improved workplace safety considerations. Regulatory developments such as the introduction of BIS “Green Pro” certification are reinforcing the adoption of eco-friendly coatings. Additionally, the agricultural and construction equipment sector is increasingly utilizing water-borne protective primers to meet export compliance standards, further expanding market opportunities.

Japan: High-Performance Coatings for Longevity and Resilience

Japan’s waterborne coatings market is characterized by a strong emphasis on durability, safety, and advanced functionality. The country’s stringent formaldehyde emission standards have made water-based coatings the default choice for indoor applications, ensuring high indoor air quality across residential and public infrastructure.

Innovation is focused on extending the lifespan of infrastructure and enhancing resilience to environmental challenges. Water-borne fluoropolymer coatings are being widely adopted for bridge maintenance to achieve long service life with minimal maintenance. Seismic resilience is a critical area of development, with highly flexible elastomeric coatings designed to withstand structural movement during earthquakes. Urban sustainability initiatives such as the “Cool City Tokyo” program are driving demand for solar-reflective coatings, while advancements in robotic finishing technologies are improving efficiency in modular housing construction. Additionally, the growth of EV infrastructure is creating demand for specialized water-borne coatings used in cleanroom and battery manufacturing environments.

Brazil: Regulatory Transformation and Export-Led Growth in Waterborne Coatings

Brazil plays a pivotal role in the Latin American waterborne coatings market, supported by regulatory reforms and strong industrial demand. New maritime environmental regulations aligned with International Maritime Organization (IMO) standards are accelerating the adoption of water-borne antifouling coatings in key port regions. Additionally, legislation aimed at reducing lead content in paints is reinforcing the dominance of water-based technologies across architectural applications.

The country benefits from a strong raw material base, particularly the availability of Titanium Dioxide (TiO₂), enabling cost-effective production of high-opacity coatings. Industry initiatives such as the Abrafati Quality Program have improved product standards, ensuring widespread adoption of high-performance waterborne coatings. Brazil’s role as a global agricultural machinery exporter is further driving demand for eco-compliant protective coatings. Moreover, the country is expanding its presence as a regional export hub, increasing shipments of water-borne coating technologies to neighboring Mercosur markets and strengthening its leadership in the region.

Waterborne Coatings Market Report Scope

Waterborne Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$155.9 Billion

|

|

Market Size (2032)

|

$228.3 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Resin Type (Acrylic, Polyurethane, Alkyd, Epoxy, Polyester, Fluoropolymers, Vinyl, Others), By Technology (Water-soluble, Waterborne Dispersions, Colloidal Dispersions, Electrodeposition Coatings), By End-User (Building and Construction, Automotive Manufacturers, General Manufacturing and Engineering, Furniture and Woodworking Industry, Marine and Offshore Energy, Consumer Goods and Appliances), By Curing Mechanism (Air Drying, Baking, UV, Dual Cure Systems), By Sales Channel (Direct Sales, Industrial and Specialty Chemical Distributors, Retail and DIY Centers, Online B2B), By Performance Grade (Premium, Standard Industrial Grade, Economy)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., BASF SE, Axalta Coating Systems, Kansai Paint Co., Ltd., Asian Paints Limited, Jotun A/S, RPM International Inc., Hempel A/S, Berger Paints India Limited, Masco Corporation, Tikkurila Oyj, Sika AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Waterborne Coatings Market Segmentation

By Resin Type

- Acrylic

- Polyurethane

- Alkyd

- Epoxy

- Polyester

- Fluoropolymers

- Vinyl

- Others

By Technology

- Water-soluble

- Waterborne Dispersions

- Colloidal Dispersions

- Electrodeposition Coatings

By End-User

- Building and Construction

- Automotive Manufacturers

- General Manufacturing and Engineering

- Furniture and Woodworking Industry

- Marine and Offshore Energy

- Consumer Goods and Appliances

By Curing Mechanism

- Air Drying

- Baking

- UV

- Dual Cure Systems

By Sales Channel

- Direct Sales

- Industrial and Specialty Chemical Distributors

- Retail and DIY Centers

- Online B2B

By Performance Grade

- Premium

- Standard Industrial Grade

- Economy

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Waterborne Coatings Industry

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- BASF SE

- Axalta Coating Systems

- Kansai Paint Co., Ltd.

- Asian Paints Limited

- Jotun A/S

- RPM International Inc.

- Hempel A/S

- Berger Paints India Limited

- Masco Corporation

- Tikkurila Oyj

- Sika AG

*- List not Exhaustive