White Oil Market Overview 2025–2034: $1.9 Billion to $2.8 Billion at 4.4% CAGR Supported by Pharma-Grade Expansion, Clean Beauty Shifts, and Group II Feedstock Dynamics

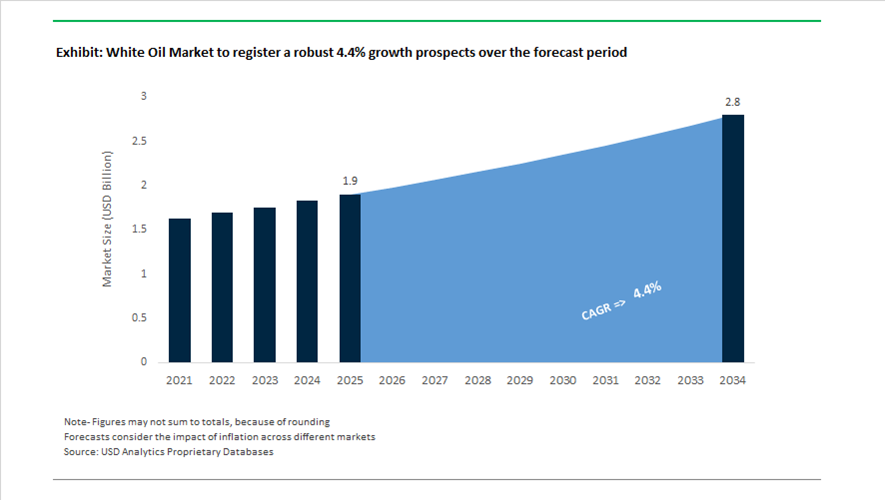

The White Oil market is valued at $1.9 billion in 2025 and is projected to reach $2.8 billion by 2034, registering a CAGR of 4.4%. White oils, also known as liquid paraffin or highly refined mineral oils, are used across pharmaceutical formulations, cosmetic emollients, personal care bases, food-grade lubricants, transformer oils, polystyrene processing aids, and flexible packaging plasticizers. Growth is being driven by rising demand for USP-grade white oils, cosmetic-grade mineral oils, and food-contact compliant process oils, particularly in Asia-Pacific and North America. Market dynamics are closely tied to Group II and Group III base oil availability, refinery throughput, and tightening global standards for purity, aromatics content, and migration limits in food and healthcare applications.

Upstream capacity and feedstock movements shaped supply conditions between 2024 and 2026. In February 2024, Chevron Lummus Global commissioned a new white oil processing unit in China utilizing advanced hydroprocessing technology to produce medicinal and cosmetic-grade oils for Asia-Pacific demand. In mid-2024, Savita Oil Technologies completed a 20% capacity expansion at its Maharashtra site to support India’s rapidly expanding D2C personal care market. In December 2024, Gandhar Oil Refinery India Ltd. finalized a ₹250 crore expansion, increasing specialty oil production including white oils by 15% to meet pharmaceutical and healthcare demand. In December 2025, Chevron announced price reductions for Group II base oils amid surplus inventories, influencing white oil production economics. In January 2026, ExxonMobil reported record refinery throughput in North America, reinforcing stable supply of high-purity base oils required for premium white oil grades.

Strategic acquisitions redefined competitive positioning in 2025. In March 2025, Sudarshan Chemical Industries acquired the Heubach Group, integrating wax and white oil-based pigment preparations into a broader additives portfolio targeting personal care and coatings. In July 2025, Shell finalized the acquisition of Raj Petro Specialities, significantly expanding its specialty white oil and petroleum jelly footprint across emerging markets through Shell’s global distribution network. In January 2026, customs data confirmed Savita Oil Technologies retained its position as India’s largest base oil importer for the sixth consecutive year, increasing its share to 16%, driven by strong demand in transformer oils and pharmaceutical-grade white oils.

Sustainability and formulation trends accelerated diversification. Throughout 2024–2025, Savita introduced biodegradable specialty fluids under its Bio Boost and bioTransol brands, reflecting movement toward lower-carbon alternatives while maintaining high-purity performance. In 2025, Sonneborn launched SonneNatural™ Fluidity and SonneNatural™ Synergy, bio-based alternatives positioned as replacements for low-viscosity white oils and cyclic siloxanes in clean beauty formulations. Major refiners including Gandhar Oil released new USP-grade white oils certified for “smart” flexible food packaging in 2025, engineered as non-migratory plasticizers meeting strict global food-contact standards.

Trends and Opportunities in the White Oil Market

Trend 1: Strategic Supply Chain Consolidation for Dermocosmetic Convergence

A defining trend in the white oil market is the rapid convergence of personal care and pharmaceutical value chains. Skincare products are increasingly positioned as dermocosmetics, blurring the line between cosmetic formulation and therapeutic delivery. This has created strong demand for white oils that meet both cosmetic-grade sensory expectations and pharmaceutical excipient requirements.

By 2025, pharmaceutical-grade white oil accounted for approximately 65% of total market volume, driven by aging demographics and the expansion of topical drug delivery systems. In dermocosmetic creams, ointments, and barrier-repair formulations, white oil is no longer a passive emollient but a critical inert carrier for APIs, retinoids, and corticosteroids, where even trace aromatic hydrocarbons can compromise product safety or stability.

To support global manufacturing footprints, major refiners such as ExxonMobil and Sonneborn are actively marketing harmonized pharmacopeia-compliant white oils that simultaneously meet USP, Ph. Eur., and JP standards. This “single-SKU global excipient” strategy allows multinational brands to eliminate region-specific reformulation, reduce analytical testing costs, and streamline regulatory submissions with the FDA and EMA. As a result, white oil suppliers with multi-pharmacopeia certification are gaining disproportionate share in premium personal care and pharmaceutical supply chains.

Trend 2: Mandatory Reformulation in Food-Contact Polymers Due to MOSH and MOAH Limits

Food safety regulation has become a decisive force in reshaping white oil demand, particularly in packaging, polymer compounding, and food-processing equipment. Regulatory focus has shifted from general mineral oil hydrocarbons to specific enforcement of MOAH limits, reflecting growing concern over genotoxicity risks.

In early 2025, the European Commission advanced the integration of MOAH maximum levels into the European Contaminants Regulation (EU) 2023/915, setting limits of 0.5 mg/kg for low-fat dry foods and 2.0 mg/kg for fats and oils. This regulatory move has forced packaging producers and adhesive formulators to abandon technical-grade mineral oils in favor of fully saturated, ultra-refined white oils with negligible aromatic content.

Following the EFSA Scientific Opinion, food business operators are now required to implement Limit of Quantification (LOQ) testing across the value chain. As a result, Direct Food Contact (3H) certified white oils are increasingly specified in food-processing machinery, conveyor lubrication, and polymer masterbatches to ensure that incidental migration remains below the new regulatory thresholds. This has structurally increased demand for high-severity hydrotreated and hydrocracked white oils, particularly in Europe and export-oriented Asian manufacturing hubs.

Opportunity 1: High-Performance Dielectric Coolants for EV Battery Packs

One of the fastest-emerging opportunities for white oils lies in electric vehicle battery immersion cooling, where safety, thermal stability, and electrical insulation are paramount. As EV platforms migrate toward cell-to-pack and cell-to-chassis architectures, the coolant is increasingly in direct contact with live electrical components, eliminating tolerance for conductive or reactive fluids.

Research published in December 2025 comparing mineral-based oils with natural esters demonstrated that high-purity white oils offer superior dielectric strength, low electrical conductivity, and excellent copper corrosion resistance. These properties are critical for preventing short circuits and material degradation in high-voltage battery environments.

Low-viscosity white oils in the ISO VG 7–15 range are seeing accelerated adoption due to their ability to maintain battery pack temperatures below 35.3°C under high-load charging and discharging cycles. This thermal performance reduces the risk of thermal runaway and extends battery service life, while offering a cost-effective alternative to synthetic fluorinated dielectric fluids. As fast-charging infrastructure expands, specialty white oils are increasingly positioned as enabling fluids rather than commodity lubricants.

Opportunity 2: Industrial-Scale Lubricants for Controlled Environment Agriculture (CEA)

The industrialization of agriculture through vertical farming and hydroponic systems is creating a durable, compliance-driven demand for food-safe white oil-based lubricants and anti-foams. Controlled Environment Agriculture operations rely on fully enclosed, automated systems where any chemical exposure risk directly threatens crop viability and regulatory compliance.

In regions such as the Middle East, where vertical farming is projected to reach $862 million by 2030, NSF H1-registered white oils are being specified for conveyor lubrication, pump systems, and climate-control actuators operating in close proximity to edible crops. These oils must be chemically inert, odorless, and non-toxic to support closed-loop hydroponic production.

Advanced vertical farms, including building-based systems that account for approximately 70% of installations, also utilize white oils as anti-foaming agents in nutrient reservoirs and as protective coatings for humidity and nutrient sensors. These applications support water reuse efficiencies of 90–95%, aligning with national food security and water conservation mandates in the UAE and Saudi Arabia. As CEA scales, white oil demand in agri-industrial applications is shifting from intermittent use to continuous, mission-critical consumption.

White Oil Market Share and Segmentation Insights

Product Type Market Share: Light Paraffinic White Oil Leads with Purity and Regulatory Compliance

Light paraffinic white oil holds a 48.60% share in the white oil market in 2025, driven by its low viscosity, high purity, and broad acceptance across pharmaceutical, food-grade, and cosmetic applications. Its odorless, tasteless nature and chemical stability make it ideal for sensitive end uses. Heavy paraffinic and naphthenic white oils serve industrial and specialized applications with different viscosity and solvency profiles. A key market trend is the advancement of hydroprocessing technology, enabling ultra-high purity white oils with reduced aromatic and sulfur content, supporting compliance with stringent global regulatory standards while maintaining cost efficiency.

Application Market Share: Personal Care and Cosmetics Leads with Emollient Performance and Safety Profile

Personal care and cosmetics account for 28.40% of the white oil market in 2025, supported by its widespread use in skincare, hair care, baby oils, and cosmetic formulations. Its emollient properties, hypoallergenic nature, and formulation stability drive strong demand across global beauty and personal care markets. Industrial applications, polymers, pharmaceuticals, food, textiles, and agriculture contribute additional demand segments. A key industry trend is the ongoing positioning of highly refined mineral oils as safe and effective ingredients, where manufacturers emphasize purity, regulatory compliance, and performance to address evolving consumer perceptions and maintain relevance in premium personal care formulations.

White Oil Market Competitive Landscape

The White Oil market in 2026 is shaped by regulatory-driven specialization, advanced hydrotreating technologies, and ISCC PLUS-certified supply chains, as manufacturers compete on ultra-high purity, low-volatility formulations for pharmaceutical-grade white oils, medical polymers, and premium dermo-cosmetic applications.

ExxonMobil Strengthens Pharmaceutical-Grade Leadership with Globally Consistent Primol™ and Marcol™ Portfolio

ExxonMobil continues to set the global benchmark in pharmaceutical-grade white oil through its Primol™ and Marcol™ product lines, widely used in medical polymers and food-grade applications. Primol™ 352 is a preferred choice for high-clarity thermoplastics such as polystyrene and TPE in medical tubing and electronics. The company expanded Marcol™ 82 applications as a vaccine adjuvant, comprising up to 50% of formulations in animal health. With $36 billion in 2025 earnings, ExxonMobil leverages refining integration to capture high-margin specialty segments. Its ability to deliver USP/EP-compliant white oils across global sites minimizes reformulation risk for multinational pharma and cosmetic brands. This consistency ensures regulatory compliance and supply reliability in highly sensitive applications.

Savita Oil Technologies Accelerates Regional Dominance with Integrated Specialty Oils Expansion

Savita Oil Technologies has emerged as a high-growth leader in the South Asian white oil market, driven by strong financial performance and supply chain control. The company reported a 170% surge in Q3 FY26 profits with total income reaching ₹1,093.2 crore, supported by its Specialty Oils division. Commissioning of Phase 2 at its Mahad facility enhances production of synthetic esters alongside white oils, enabling diversification into biodegradable alternatives. As India’s largest base oil importer with a 16% market share, Savita ensures consistent feedstock availability. Strategic collaboration with Mahindra strengthens its downstream integration in agricultural and industrial lubricants. This vertically integrated model enhances competitiveness in regional pharmaceutical and cosmetic-grade white oil demand.

Sonneborn Expands Medical-Grade White Oil Portfolio with Global Regulatory Backing and Vertical Integration

Sonneborn, under HF Sinclair, remains a key global supplier of high-purity white oils and petrolatums with extensive regulatory approvals across 80+ countries. Integration within HF Sinclair provides access to 34,000 barrels per day of specialty lubricant capacity, improving cost efficiency and feedstock optimization. The company is expanding into advanced wound care and ophthalmic lubricant markets where USP-grade white oils act as inert carriers for APIs. Sustainability initiatives focus on reducing refining carbon intensity across U.S. and European operations. Its long-standing regulatory approvals accelerate product adoption in highly regulated pharmaceutical and personal care sectors. This legacy-driven compliance advantage strengthens its position in global healthcare supply chains.

Petro-Canada Lubricants Advances Ultra-Purity White Oils with HT Processing and Food-Grade Certifications

Petro-Canada Lubricants leads in ultra-high purity white oil production using its proprietary HT Purity Process, achieving 99.9% base oil purity. Its PURITY™ FG white oils are widely adopted in food processing, offering NSF H1 and 3H certifications for safe incidental and direct contact. Integration with Suniso brand management expands its presence in refrigeration and HVAC applications. The company is leveraging automotive lubricant expertise to develop low-volatility white oils for EV components and advanced plasticizers. Backed by Suncor’s refinery throughput exceeding 99% utilization, supply stability remains a core strength. This ensures consistent availability of high-performance white oils across North American industrial and food-grade markets.

Sasol Differentiates with Fischer-Tropsch Synthetic White Oils for Zero-Aromatic High-Purity Applications

Sasol is positioning itself as a leader in synthetic white oils using Fischer-Tropsch technology, delivering zero-aromatic, highly paraffinic products for sensitive applications. The company reported R122.4 billion in H1 FY26 revenue with a 10% production increase supporting specialty chemical supply. Its synthetic white oils are critical for silicon-free cosmetic formulations and high-purity intermediates where contamination risks are unacceptable. The International Chemicals Reset Strategy is improving EBITDA while focusing on high-margin specialty segments. Sasol is integrating over 1,200 MW of renewable energy to reduce embedded carbon in its refining processes. This combination of synthetic purity and decarbonization aligns with evolving ESG and regulatory requirements in 2026.

India White Oil Market Anchored by Regulatory Formalization and High-Purity Manufacturing

India’s white oil market entered a structurally new phase in 2025 following the implementation of the Vegetable Oil Products Production and Availability Regulation Amendment Order. From August 1, 2025, all white oil manufacturers supplying the food and edible oil value chain are required to register through the National Single Window System, enabling real-time production and inventory monitoring. This reform has elevated white oil from a largely compliance-light petroleum derivative to a strategically monitored product, particularly for pharmaceutical, food contact, and personal care applications. As a result, refiners are prioritizing traceability, batch consistency, and pharmacopoeia alignment to remain eligible suppliers under the tightened oversight framework.

Operational excellence and digitization are becoming competitive differentiators. Numaligarh Refinery Limited integrated India’s first 5G captive network into its wax and white oil units in 2025, enabling tighter control over hydro-finishing and hydrogenation parameters. This has improved viscosity consistency for pharmaceutical and cosmetic grades, where deviation risk directly affects downstream formulation stability. On the commercial front, Gandhar Oil Refinery (India) Ltd expanded its international distribution reach in late 2025, targeting medicinal-grade white oil demand across the Middle East and Africa. Parallel to export growth, domestic demand is shifting toward high viscosity index white oils used in solar panel encapsulants, while multiple Indian refiners have initiated green refining trials that utilize renewable energy to power energy-intensive decolorization steps, reducing the carbon intensity of ultra-pure white oil production.

United States White Oil Market Driven by Clean Label, Semiconductors, and Energy Applications

The United States white oil market in 2025 is characterized by premiumization and application diversification rather than volume expansion. In the energy sector, ExxonMobil advanced lightweight proppant technologies that rely on specialized white oil carriers to enhance deep-well shale recovery rates. These formulations demand ultra-low aromatic content and high thermal stability, reinforcing the role of technically refined white oils in unconventional resource extraction. At the same time, regulatory and consumer pressure has accelerated the transition toward PFAS-free formulations in personal care and baby products, prompting refiners to redesign white oil purification pathways.

This regulatory shift has been particularly visible at Sonneborn, which accelerated PFAS-free white oil production following updated federal scrutiny of industrial surfactants in 2025. Downstream, supply chain discipline is tightening. Chevron Phillips Chemical received industry recognition for implementing ultra-pure white oil handling protocols under its Operation Clean Sweep initiative, aimed at preventing micro-plastic contamination in polymer processing. Demand from life sciences and electronics is also rising. Brenntag expanded its GMP-compliant white oil distribution partnership with ExxonMobil in late 2025 to support vaccine adjuvant formulations, while CHIPS Act-driven semiconductor investments are creating localized demand for electronic-grade white oils used as stable coolants in fabrication tools.

China White Oil Market Reshaped by Standards Harmonization and EV Thermal Fluids

China’s white oil market is undergoing a dual transformation focused on quality harmonization and advanced industrial use cases. BASF’s Zhanjiang Verbund site, nearing full mechanical completion in late 2025, integrates high-performance white oil dispersions into the production of aqueous packaging coatings. This reflects China’s push to internalize value chains for food-contact and packaging applications that previously relied on imports. Regulatory alignment is reinforcing this trend. Revised purity standards issued by the State Administration for Market Regulation will take effect in June 2026, bringing domestic white oil specifications in line with European Pharmacopoeia benchmarks for food and pharmaceutical contact.

Industrial policy is also reshaping product portfolios. In late 2025, Sinopec announced collaborations with electric vehicle manufacturers to develop white oil-based thermal management fluids. These fluids offer superior oxidation stability compared with conventional mineral oils and are increasingly used in battery and power electronics cooling systems. At the regional level, Zhejiang province has mandated a 30% reduction in aromatic content for industrial oils by 2026, accelerating investment in catalytic hydro-cracking and deep hydrogenation technologies. Collectively, these measures are pushing the Chinese white oil market toward higher purity, lower aromatic content, and closer integration with advanced manufacturing sectors.

Germany White Oil Market Focused on Specialty Additives and Circularity

Germany’s white oil market is less about scale and more about strategic repositioning within high-value specialty chemicals. Following the divestment of its Urethane Systems business in April 2025, LANXESS refocused its Specialty Additives segment on white oil-based carriers used in flame retardants and phthalate-free plasticizers. These applications require extremely stable, low-odor carriers that meet stringent EU chemical safety and sustainability expectations.

Innovation and circularity are emerging as defining themes. At the K 2025 plastics trade fair in Düsseldorf, German manufacturers showcased bio-based white oil alternatives derived from sustainable feedstocks, targeting measurable reductions in lifecycle carbon footprint for polymer processing. Complementing this, the German Federal Environment Agency initiated a 2026 pilot program to enable high-grade re-refining of technical white oils used in pharmaceutical manufacturing. This program positions white oil not as a single-use consumable but as part of a closed-loop specialty chemical system, aligning Germany’s white oil market with broader circular economy objectives.

White Oil Market Country Snapshot

White Oil Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key Application Focus

|

Market Direction

|

|

India

|

Regulatory formalization and digitized refining

|

Pharma, food contact, solar encapsulants

|

Export-oriented, purity-driven

|

|

United States

|

Clean label compliance and advanced manufacturing

|

Baby care, vaccines, semiconductors, shale

|

Premium grades and compliance-led

|

|

China

|

Standards harmonization and EV integration

|

Packaging, thermal management fluids

|

High-purity and low-aromatic shift

|

|

Germany

|

Specialty additives and circular economy

|

Flame retardants, plasticizers, polymers

|

Innovation- and sustainability-led

|

White Oil Market Report Scope

White Oil Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.9 Billion

|

|

Market Size (2034)

|

$2.8 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Product Type (Light Paraffinic White Oil, Heavy Paraffinic White Oil, Naphthenic White Oil), By Grade (Pharmaceutical and Medicinal Grade, Food Grade, Cosmetic Grade, Industrial and Technical Grade), By Application (Personal Care and Cosmetics, Pharmaceuticals, Food Industry, Polymers and Plastics, Textiles, Agriculture, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Exxon Mobil Corporation, Sinopec Corporation, HF Sinclair Corporation, Chevron Corporation, Gandhar Oil Refinery Limited, Petro-Canada Lubricants, LANXESS AG, Savita Oil Technologies Limited, Nynas AB, Shell plc, Suncor Energy Inc., Sasol Limited, Renkert Oil Inc., Petroyağ Lubricants, Panama Petrochem Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

White Oil Market Segmentation

By Product Type

- Light Paraffinic White Oil

- Heavy Paraffinic White Oil

- Naphthenic White Oil

By Grade

- Pharmaceutical and Medicinal Grade

- Food Grade

- Cosmetic Grade

- Industrial and Technical Grade

By Application

- Personal Care and Cosmetics

- Pharmaceuticals

- Food Industry

- Polymers and Plastics

- Textiles

- Agriculture

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the White Oil Market

- Exxon Mobil Corporation

- Sinopec Corporation

- HF Sinclair Corporation

- Chevron Corporation

- Gandhar Oil Refinery Limited

- Petro-Canada Lubricants

- LANXESS AG

- Savita Oil Technologies Limited

- Nynas AB

- Shell plc

- Suncor Energy Inc.

- Sasol Limited

- Renkert Oil Inc.

- Petroyağ Lubricants

- Panama Petrochem Limited

*- List not Exhaustive