Window Film Market Growth Accelerated by Energy Efficiency Mandates and Smart Glazing Technologies

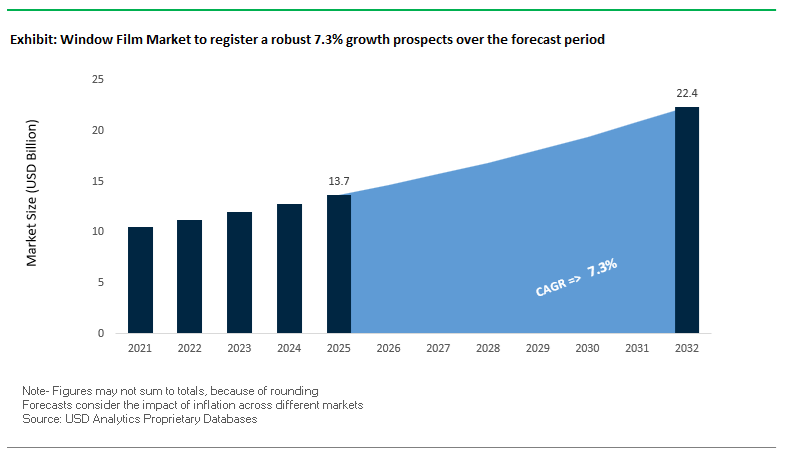

The global Window Film Market was valued at $13.7 billion in 2025 and is projected to expand at a CAGR of 7.3% from 2025 to 2032, reaching $22.4 billion by 2032. This strong growth trajectory is driven by rising demand for energy-efficient building solutions, automotive solar control films, and advanced safety glazing technologies across residential, commercial, and transportation sectors. Window films are increasingly recognized as a cost-effective retrofit solution to enhance thermal insulation, UV protection, glare reduction, and occupant comfort, aligning with global sustainability and decarbonization goals.

A key structural driver is the growing emphasis on green building certifications such as LEED and BREEAM, where window films contribute to reducing energy consumption and improving building performance. The adoption of solar control, low-emissivity (low-E), and spectrally selective films is accelerating, particularly in urban environments facing rising cooling loads due to climate change. Additionally, the automotive sector is witnessing increased integration of ceramic and nano-ceramic films, which offer superior heat rejection, durability, and signal-friendly performance for connected vehicles.

Technological advancements are transforming the market landscape, with innovations in smart films, electrochromic glazing, and high-performance polyester substrates enabling dynamic light control and enhanced aesthetic appeal. The integration of recycled materials, bio-based components, and circular production models is further strengthening the sustainability profile of window films. Moreover, the growing demand for safety and security films, particularly in commercial infrastructure and public spaces, is expanding the application scope of advanced multilayer film technologies.

Market Analysis: Smart Film Innovation, and Sustainability Certification Driving Competitive Dynamics

The Window Film Market is undergoing a significant transformation driven by strategic acquisitions, smart glazing innovation, and sustainability-focused product development, reshaping competitive dynamics across global markets. A major development is Madico’s acquisition of Johnson Window Films (January 2026), which consolidates two prominent U.S. manufacturers and integrates Johnson’s customer base into Madico’s extensive North American distribution network. This move strengthens Madico’s market position across automotive and architectural film segments, while enhancing operational scale and dealer reach.

Sustainability certification and transparency are emerging as critical differentiators. In March 2026, Avery Dennison published its first Environmental Product Declaration (EPD) for solar control window films, providing third-party verified lifecycle impact data. This initiative aligns with the growing demand from developers and contractors for quantifiable sustainability metrics, particularly in LEED- and BREEAM-certified projects. Complementing this, Avery Dennison’s Energy Savings Calculator enables end users to evaluate the ROI and carbon reduction potential of window film installations, reinforcing the shift toward data-driven decision-making.

Product innovation is increasingly focused on advanced materials and smart functionality. Saint-Gobain’s SageGlass RealTone™ (February 2025) represents the cutting edge of electrochromic glazing technology, offering dynamic tinting capabilities that optimize natural light while maintaining color fidelity. Meanwhile, Lintec’s launch of 100% recycled PET window film (July 2025) highlights the industry’s move toward circular material solutions, achieving significant CO₂ emission reductions without compromising performance.

Capacity expansion and global growth strategies are also shaping the market. Eastman Chemical’s expansion of its performance film production facilities focuses on high-end ceramic and nano-ceramic technologies, addressing rising demand in the automotive aftermarket and premium architectural segments. Additionally, Garware Hi-Tech Films’ leadership expansion (April 2026) reflects its strategic push to scale operations across India and Southeast Asia, capitalizing on strong regional demand growth.

Organizational restructuring is supporting long-term innovation and market penetration. Madico’s leadership transition and restructuring initiatives (2025–2026) are aimed at accelerating product development and strengthening global dealer partnerships, particularly for its Sunscape®, SafetyShield®, and ClearPlex® product lines. Furthermore, Avery Dennison’s sustainability awards program underscores the growing importance of circular economy practices, encouraging recycling and waste reduction across the value chain.

Market Trend: US DOE Efficiency Standards Accelerating High-Performance Solar Control Film Adoption

The evolving roadmap from the U.S. Department of Energy Building Technologies Office is significantly reshaping the window film market, particularly by promoting retrofit solutions that enhance building energy performance without full window replacement. In 2026, next-generation efficiency standards are prioritizing advanced solar control window films capable of delivering measurable improvements in building envelope performance.

Key performance benchmarks now emphasize reducing the Solar Heat Gain Coefficient to below 0.25 while maintaining visible light transmittance above 40%. This balance between solar heat rejection and natural daylighting is critical for commercial and residential retrofit applications seeking to optimize energy efficiency without compromising occupant comfort.

Energy audits conducted by the DOE indicate that high-performance window films can reduce cooling loads by 30% to 50%, making them a cost-effective solution for achieving Zero Energy Ready Home standards and equivalent commercial building certifications. This is driving increased adoption of energy-efficient window films and solar control coatings across retrofit and renovation projects in North America.

Market Trend: EU EPBD 2025–2026 Mandate Driving Solar Control Films in Zero-Emission Buildings

The implementation of the revised Energy Performance of Buildings Directive is accelerating the adoption of solar control window films across Europe. As part of the 2026 regulatory framework, passive cooling strategies are becoming mandatory for achieving Zero-Emission Building standards, positioning window films as a critical component of sustainable building design.

Under EPBD-aligned building codes, retrofitted glazing systems are required to achieve total solar energy rejection levels ranging from 50% to 70%. This is significantly increasing demand for high-performance window films capable of meeting stringent thermal performance criteria.

With approximately 75% of the European building stock classified as energy inefficient, the directive emphasizes building envelope improvements and solar heat mitigation as key strategies to achieve a 36% reduction in energy-related greenhouse gas emissions by 2030. This regulatory push is strengthening the role of solar control films in green building materials and energy-efficient construction solutions.

Market Opportunity: Smart Electrochromic Window Films Driving Growth in Dynamic Solar Control Solutions

The integration of smart technologies into building materials is creating significant opportunities for electrochromic and dynamic window films in the global window film market. These advanced films enable real-time control of light transmission and heat gain, supporting the development of intelligent and responsive building environments.

Modern electrochromic and polymer-dispersed liquid crystal films can transition from transparent to opaque states in under 60 seconds, enhancing occupant comfort by reducing glare and controlling solar heat ingress. This functionality is particularly valuable in commercial real estate, where occupant experience and energy efficiency are key performance metrics.

The adoption of smart window films is also contributing to sustainability certifications, with buildings potentially qualifying for up to nine LEED v4.1 credits across energy efficiency and indoor environmental quality categories. In Europe, compliance with the Smart Readiness Indicator framework further enhances the value proposition of these technologies, as buildings equipped with dynamic solar control systems achieve higher ratings and improved ESG performance.

This convergence of energy efficiency, automation, and occupant comfort is positioning smart window films as a high-growth segment within the advanced building materials market.

Market Opportunity: Antiviral and Antimicrobial Window Films Expanding in Public Infrastructure Applications

The increasing focus on hygiene and public health is creating strong demand for antiviral and antimicrobial window films across a wide range of applications, including healthcare facilities, educational institutions, and transportation infrastructure. These functional films provide continuous surface protection, addressing the need for long-term pathogen control in high-contact environments.

Advanced antimicrobial window films utilizing nano-silver and copper-ion technologies are achieving pathogen reduction rates of 99.99% within 24 hours, as validated by ISO 22196 and ISO 21702 testing standards. This high level of efficacy is critical for preventing the spread of bacteria and viruses in densely occupied public spaces.

Unlike temporary disinfectant solutions, these films offer durable protection with a service life exceeding five years, maintaining performance even under intensive cleaning protocols. Their mechanical durability and abrasion resistance make them suitable for demanding environments such as hospitals and transit hubs.

The integration of antimicrobial functionality with traditional window film benefits such as UV protection and solar control is expanding their application scope, positioning them as a key innovation in the functional films market and a critical component of modern health-focused building design.

Window Film Market Share and Segmentation Insights

Sun Control Films Lead with 47.2% Share Driven by Energy Savings and Thermal Performance

The sun control (solar/heat rejection) segment dominates the window film market with a 47.2% market share in 2025, fueled by rising demand for energy-efficient building solutions and indoor comfort enhancement. In the architectural window films and energy-saving coatings market, these films significantly reduce solar heat gain by 40–75%, lowering air conditioning costs and overall energy consumption in both commercial and residential buildings. This makes them a critical component in green building initiatives and sustainable construction practices. Additionally, sun control films provide up to 99% UV protection, preventing fading of interior furnishings, flooring, and artwork, while also offering health benefits by reducing harmful UV exposure. Their dual functionality of thermal insulation and UV shielding positions them as a leading solution in the global window film market, particularly as demand increases for energy-efficient retrofits and climate-responsive building materials.

Specialty Window Film Dealers Lead with 35.6% Share Through Professional Installation and Service Expertise

The specialty window film dealers segment leads the window film market with a 35.6% market share in 2025, driven by the need for professional installation and technical expertise. Within the window film distribution and installation services market, high-performance products such as safety and security films, spectrally selective films, and advanced sun control solutions require trained installers to ensure proper adhesion, performance, and warranty compliance. Specialty dealers provide end-to-end services, including consultation, product selection, and certified installation, making them the preferred choice for both commercial building owners and residential customers. This channel is particularly strong in energy efficiency retrofits, privacy enhancements, and decorative film applications, where precision and quality are critical. As demand grows for high-performance window films and customized installation solutions, specialty dealers continue to dominate the global window film market, supported by their expertise, service reliability, and customer-centric approach.

Window Film Market Competitive Landscape Driven by Sustainable Films, rPET Integration, and Energy-Efficient Building Solutions

The window film market is becoming increasingly competitive as manufacturers prioritize high-durability architectural films, recycled PET substrates, and energy-saving technologies. Growth is driven by green building regulations, automotive tinting demand, and smart film integration across commercial, residential, and mobility sectors.

3M Strengthens Architectural Film Leadership Through Dealer Network Expansion and Safety Solutions

3M Company continues to dominate the global window film market through its extensive distribution network and high-performance architectural film portfolio. In February 2026, the company reinforced its market presence via its National Dealer Meeting, supporting over 400 authorized dealers to expand commercial and institutional reach. Its multi-layer optical films, including the Prestige Series for solar control and Scotchshield™ for safety and security, address critical needs such as energy efficiency and impact resistance. Recognition of its partner Window Film Depot as 2026 National Dealer of the Year highlights its leadership in retrofit building solutions. 3M is also integrating film solutions with professional security consulting, particularly for schools and government infrastructure. This combination of product innovation and distribution strength secures its leadership in premium window film solutions.

Eastman Drives Circular Economy Leadership with Recycled PET Window Films and Global Expansion

Eastman Chemical Company is a major player in sustainable window film solutions, leveraging advanced molecular recycling technologies. Its Kingsport facility significantly increased recycled PET (rPET) output in 2025 and is set for a 130% capacity expansion to meet rising demand for low-carbon materials. Following the acquisition of Matrix Films, Eastman strengthened its global distribution footprint across North America, Europe, and the Middle East. The company generated nearly $1 billion in operating cash flow in 2025, reinvesting heavily into circular economy initiatives. Its vertical integration enables production of high-performance window films aligned with automotive OEM sustainability targets and green building certifications. This strong focus on recycled content and scalability positions Eastman at the forefront of sustainable film manufacturing.

Avery Dennison Advances Smart and Sustainable Window Films with Digital Energy Optimization Tools

Avery Dennison Corporation is innovating at the intersection of sustainability and smart film technology in the window film market. In 2026, the company introduced Environmental Product Declarations (EPDs) for solar control films, enhancing transparency around lifecycle environmental impact. Its investment in Wiliot signals future integration of ambient IoT and “physical AI” into functional films for smart buildings and supply chains. Avery Dennison and Hanita Coatings also launched an Energy Savings Calculator, enabling users to quantify ROI and energy efficiency benefits based on climate conditions. Its decorative and solar control films are widely used across commercial offices, schools, and hospitality sectors. This blend of digital tools and sustainable materials strengthens its competitive differentiation.

Saint-Gobain Expands Solar Gard Portfolio to Accelerate Building Decarbonization Initiatives

Saint-Gobain S.A. is leveraging its Solar Gard brand to deliver energy-efficient window film solutions aligned with global decarbonization goals. The company’s 2026 “Lead & Grow” strategy emphasizes expansion in non-residential construction and infrastructure, where retrofit solutions are critical. With 73% of its 2025 sales derived from sustainable products, Saint-Gobain is strongly positioned in green building materials. Its window films play a key role in reducing building energy consumption and supporting its target of up to 80% emission reduction in residential applications. The company has already achieved a 35% reduction in Scope 1 and 2 emissions since 2017. Its deep materials science expertise enables high-performance films validated under extreme climate conditions.

Garware Strengthens Global Presence with High-Performance BOPET Window Films and Middle East Expansion

Garware Hi-Tech Films Limited is a key player in the BOPET-based window film market, focusing on cost-efficient, high-performance solutions. In January 2026, the company announced expansion into the Middle East through a new Dubai subsidiary, targeting architectural and automotive film demand. Its Q3 FY26 revenue of ₹458.7 crore reflects steady growth driven by value-added film products. Garware’s sun control and paint protection films are widely used across automotive and building applications. Its in-house BOPET manufacturing ensures consistent quality, cost control, and scalability in mid-tier premium segments. This strategic expansion and manufacturing integration strengthen its global competitiveness.

Lintec Leads Circular Innovation with 100% Recycled PET Window Films and Advanced Adhesive Technologies

Lintec Corporation is advancing sustainability in the window film market through recycled material innovation and specialty adhesive systems. In 2025, the company introduced solar control films made from 100% recycled PET resin, setting a new benchmark for circular economy practices. Its China-based manufacturing operations have achieved Global Recycled Standard (GRS) certification, validating its sustainable supply chain. Lintec is also developing low-impact adhesives, including hot-melt and removable systems that reduce environmental impact during installation and removal. Beyond architectural films, the company provides high-performance optical films for electronics and semiconductor applications. This strong focus on sustainability and advanced materials positions Lintec as a leader in next-generation window film technologies.

China’s Nano-Ceramic Innovation and Smart Infrastructure Driving Window Film Demand

China continues to dominate the global window film market, supported by aggressive green building initiatives and rapid 5G infrastructure expansion. The integration of advanced nano-ceramic window films capable of delivering high infrared rejection while maintaining signal transparency is transforming adoption across smart-city skyscrapers. Regulatory frameworks such as GB 4806.10-2025 are tightening safety standards for coatings and laminates used in public infrastructure, reinforcing the shift toward high-performance, low-VOC architectural films.

Government-backed sustainability initiatives are accelerating deployment, with subsidies under the “Blue Sky” program encouraging retrofitting of commercial buildings with solar control films. China’s infrastructure scale is evident in applications such as high-speed rail, where waterborne adhesive-backed films are widely used for heat reduction and UV protection. Industrial expansion across Anhui and Guangdong provinces is further strengthening domestic production capacity, ensuring China remains the epicenter of global window film manufacturing and innovation.

United States: Policy-Driven Retrofits and Smart Window Film Technologies

The United States window film market is being reshaped by energy efficiency mandates and infrastructure modernization. The Inflation Reduction Act is a key growth catalyst, offering tax incentives for residential window film installations that meet Energy Star standards. This has significantly increased adoption in the retrofit segment, particularly in aging building stock where window replacement is cost-prohibitive.

Technological innovation is driving the next phase of market expansion. IoT-enabled window films are enabling real-time integration with building management systems, optimizing HVAC performance and reducing energy consumption. Regulatory standardization of visible light transmission (VLT) across multiple states is streamlining automotive film deployment nationwide. Additionally, the development of PFAS-free films is aligning with tightening chemical regulations. Infrastructure investments are also driving demand for safety and security films in public buildings, while capacity expansions by major manufacturers are supporting increased demand for hurricane-resistant laminated glass solutions.

Germany: Low-Emissivity Film Innovation and Sustainable Retrofitting Leadership

Germany stands at the forefront of the European window film market, driven by its leadership in energy-efficient building technologies and sustainability standards. The adoption of low-emissivity (Low-E) window films is accelerating as part of compliance with the EU Energy Performance of Buildings Directive, which mandates zero-emission buildings in the coming decade. These films play a critical role in improving thermal insulation, particularly in retrofit projects where structural modifications are limited.

Innovation in materials and adhesives is strengthening Germany’s market position. The development of amine-free waterborne polyurethane dispersion adhesives is reducing off-gassing and improving indoor air quality. Advanced hybrid films combining polysiloxane and acrylic technologies are delivering enhanced weather resistance for industrial applications. Investments in electrochromic glazing technologies are further expanding the scope of smart window films. Additionally, the use of bio-based materials in film liners is aligning with circular economy goals, reinforcing Germany’s leadership in sustainable architectural solutions.

India: Rapid Urbanization and Energy-Efficient Film Adoption

India is emerging as a high-growth market in the window film industry, driven by rising urban temperatures, increasing energy costs, and strong government support for sustainable construction. Initiatives such as the Smart Cities Mission and GRIHA certification programs have recognized solar window films as essential energy-saving solutions, accelerating their adoption across residential and commercial sectors.

Domestic manufacturing capacity is expanding rapidly, with significant investments aimed at meeting growing demand for sun-control films. Innovation in high-clarity, high-performance films is supporting premium residential applications, while specialized products such as anti-graffiti films are gaining traction in metro rail infrastructure. The hospitality and healthcare sectors are also driving demand, leveraging window films to reduce cooling loads while maintaining natural lighting. Enhanced distribution networks are improving market penetration, ensuring faster installation and service delivery across urban and semi-urban regions.

Japan: Precision Engineering and Safety-Focused Window Film Technologies

Japan’s window film market is characterized by advanced material engineering and a strong focus on safety and durability. The development of ultra-thin polyester substrates is enabling high-performance films that provide shatter resistance without compromising optical clarity, making them ideal for both residential and industrial applications.

Technological innovation extends to self-cleaning and photocatalytic films that reduce maintenance requirements in densely populated urban environments. Regulatory standards such as JIS A 5759 ensure high performance in solar control and disaster mitigation, reinforcing the use of window films in safety-critical applications. Investments in cool-roof and heat mitigation technologies are supporting urban sustainability initiatives, while specialized films for semiconductor cleanrooms highlight Japan’s focus on high-precision applications. The integration of AI-driven color matching further enhances customization in architectural retrofits, ensuring seamless aesthetic integration.

South Korea: Functional Film Innovation for Automotive and Marine Applications

South Korea is leveraging its technological expertise to drive innovation in functional window films, particularly for automotive and marine sectors. Advanced coating techniques such as dual-layer slot-die coating are enabling the integration of multiple functionalities—such as infrared blocking and anti-fog properties—within a single film layer, enhancing performance and efficiency.

Regulatory tightening under environmental laws is accelerating the shift toward low-VOC production processes, further boosting demand for advanced film technologies. South Korea is also a leader in maritime applications, developing specialized films that provide corrosion resistance for ships and offshore structures. Innovation in pressure-sensitive adhesive films with bubble-free application features is supporting growth in DIY and residential segments. Investments in R&D clusters are fostering collaboration between film manufacturers and electronics companies, driving advancements in next-generation display and smart film technologies.

Brazil: Bio-Based Innovation and Expanding Solar Control Applications

Brazil is emerging as a key player in the Latin American window film market, supported by its focus on bio-based materials and expanding automotive and construction sectors. The development of waterborne adhesives derived from renewable sources such as sucrose is positioning Brazil as a leader in sustainable film production.

Regulatory initiatives aimed at reducing solvent emissions are accelerating the adoption of eco-friendly window film solutions, particularly in automotive applications. The expansion of security films in high-density urban centers is addressing safety concerns while creating new growth opportunities. Additionally, the agricultural sector is driving demand for reflective films used in greenhouse and livestock applications to regulate temperature. Technological advancements in humidity-resistant films are ensuring durability in tropical climates, further strengthening Brazil’s market position in the global window film industry.

Window Film Market Report Scope

Window Film Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.7 Billion

|

|

Market Size (2032)

|

$22.4 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Product (Sun Control, Safety and Security Films, Decorative Films, Privacy Films, Insulating, Spectrally Selective Films), By Material (Polyester, Vinyl, Ceramic, Metallic, Carbon, Plastic), By Technology (Dyed Films, Metalized, Ceramic, Hybrid Films, Smart), By End-User Industry (Building and Construction, Automotive, Marine, Aerospace, Others), By Sales Channel (Direct Sales, Indirect Sales, Specialty Window Film Dealers, Automotive Aftermarket Shops, Home Improvement Centers, Online)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Eastman Chemical Company, Saint-Gobain Performance Plastics, Avery Dennison Corporation, Madico, Inc., Johnson Window Films, Inc., Toray Industries, Inc., Garware Hi-Tech Films Limited, XPEL, Inc., Lintec Corporation, KDX Composite Material, Haverkamp GmbH, Armolan Window Films, Reflectiv, American Standard Window Film

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Window Film Market Segmentation

By Product

- Sun Control

- Heat Rejection Films

- UV Blocking Films

- Glare Reduction Films

- Safety and Security Films

- Anti-Shatter

- Blast Mitigation Films

- Anti-Graffiti Films

- Decorative Films

- Frosted and Etched Films

- Patterned and Textured Films

- Stained Glass Films

- Privacy Films

- One-Way Mirror Films

- Blackout and Whiteout Films

- Insulating

- Spectrally Selective Films

By Material

- Polyester

- Vinyl

- Ceramic

- Metallic

- Carbon

- Plastic

By Technology

- Dyed Films

- Metalized

- Ceramic

- Hybrid Films

- Smart

By End-User Industry

- Building and Construction

- Residential

- Commercial

- Institutional

- Automotive

- Passenger Vehicles

- Commercial and Fleet Vehicles

- Marine

- Aerospace

- Others

By Sales Channel

- Direct Sales

- Indirect Sales

- Specialty Window Film Dealers

- Automotive Aftermarket Shops

- Home Improvement Centers

- Online

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Window Film Industry

- 3M Company

- Eastman Chemical Company

- Saint-Gobain Performance Plastics

- Avery Dennison Corporation

- Madico, Inc.

- Johnson Window Films, Inc.

- Toray Industries, Inc.

- Garware Hi-Tech Films Limited

- XPEL, Inc.

- Lintec Corporation

- KDX Composite Material

- Haverkamp GmbH

- Armolan Window Films

- Reflectiv

- American Standard Window Film

*- List not Exhaustive