Wireless Power Supply Systems Market Overview: Growth Outlook and Strategic Insights

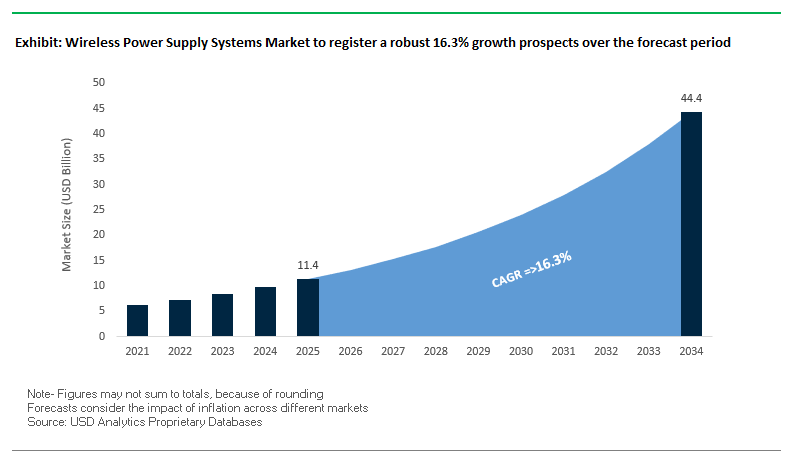

The wireless power supply systems market worldwide is anticipated to expand from USD 11.4 billion in 2025 to USD 44.4 billion by the year 2034, recording a CAGR of 16.3%. The highly growing segment is transforming the distribution of power in consumer electronics, electric mobility, industrial machines, and medical devices. It is driven by the requirement for cable-free convenience, enhanced safety, and embedding in connected ecosystems. While inductive coupling continues to be the preferred technology owing to its efficiency and established utilization in wearables and smartphones, magnetic resonance and RF-based long-range solutions are pushing the scope to mid-range and far-field use cases. The growth of EV wireless charging with in-motion systems coupled with smart home and industrial automation applications, is making wireless power a key facilitator of next-generation mobility and IoT infrastructure.

Key Insights for Industry Professionals

- Dominance of Inductive Coupling – Industry standard in mobile electronics due to high efficiency and Qi standard compliance.

- Next-Gen Standards – Qi2’s faster 25W charging capability is setting a new benchmark for performance and interoperability.

- EV Integration – Stationary and dynamic wireless charging solutions are gaining traction for electric and autonomous vehicles.

- Industrial & Medical Expansion – Adoption in AMR (automated mobile robot) charging and implanted medical devices where connector-free power enhances safety.

- Ubiquity Push – Wireless charging is being embedded in public spaces, furniture, and commercial environments to normalize adoption.

Wireless Power Supply Systems Market Analysis: Strategic Developments and Industry Momentum

The industry is witnessing fast product innovation, standards development, and multi-industry adoption. In July 2025, the Wireless Power Consortium introduced the Qi2 25W standard, which allows smartphones to be charged up to 50% in about 30 minutes, a huge advance in terms of efficiency and speed. Automotive integration is progressing fast, with WiTricity's FastTrack Integration Program allowing OEMs to test EV wireless charging within 90 days. Industrial customers such as EnerSys are aiming warehouse automation with the NexSys AIR Wireless Charger (April 2023), which is designed for use in forklifts and other motive power applications.

Consumer electronics are still a top impetus, with companies such as Belkin (April 2025) launching Qi2-qualified portable chargers and ESR launching CryoBoost thermal management technology to tackle heat concerns during rapid wireless charging. Meanwhile, Wi-Charge is spearheading long-range infrared beam technology, supported by leadership hires (August 2025) to propel international growth. Cross-sector synergies are developing like Samsung Galaxy Watch8 combining sophisticated health sensors in which wireless charging enables small form factor restrictions as well as continuous use.

The growth curve of the market is also driven by sustainability-oriented partnerships, like Powermat and Powercast's collective long- and short-range RF charging platforms honored with a "Sustainability Initiative of the Year" award. Such advancements collectively depict a market transitioning to multi-application leadership, mobility, wearables, and industrial applications being its fastest-growing verticals.

Trends and Opportunities Driving Innovation in the Wireless Power Supply Systems Market

Room-Scale RF Charging Redefining Device Power

The wireless power supply systems market is experiencing a paradigm shift with the introduction of room-scale RF charging technology for multi-meter far-field energy transfer. This technology extends the limitations of traditional inductive pads by creating a "power zone" in which multiple low-power IoT devices, sensors, and wearables can be charged simultaneously without touching the charging surface. Energous, among others, is using patented, safety-certified RF transmitters as a power delivery and data communication medium, offering seamless, over-the-air charging solutions for smart home devices, retail shelf labels, and industrial sensors. The AirFuel Alliance has developed standardized RF wireless charging specifications, with emphasis on placement flexibility and unbroken power delivery, which are particularly suitable for large-scale, low-power installations in smart buildings and industrial automation.

EV Dynamic Charging Revolutionizing Mobility

Dynamic wireless EV charging where on-road power systems power moving vehicles is gaining steam as a revolutionary wave in electric mobility infrastructure. By offering lossless energy transfer during travel, the technology eliminates range anxiety, reduces the need for oversized EV batteries, and optimizes overall grid efficiency. Government-sponsored pilot tests in the United States and Europe already test this technology on public roads to gather evidence for the validity of its safety, cost-effectiveness, and scalability. Research has established that dynamic charging can avoid over 20% of the CO₂ emissions in comparison to traditional charging, optimizing energy consumption based on real-time grid conditions. Integrating dynamic charging with future EV infrastructure has the potential to transform fleet management, long-distance logistics, and public transit systems.

Wireless Medical Implant Charging Solutions

Wireless charging for medical implant is a rapidly growing segment for the healthcare market. Inductive coupling technology, with an efficiency of up to 95%, allows non-invasive powering of neuro-stimulators, pacemakers, and glucose monitors. Medical device miniaturization and long-term implantable needs are growth drivers. Companies are speeding up clinical trials of non-invasive subcutaneous power systems, making continuous, infection-free, and maintenance-free implant operation a reality in the near future. This reduces the frequency of replacement surgeries, resulting in much improved patient outcomes and lower healthcare costs.

Wireless-powered Industrial IoT Sensor Networks

The IIoT industry can significantly benefit from wireless power transfer systems that avoid the logistics and cost of mass replacement of batteries. Factory floors, warehouses, and logistics facilities are employing wireless power networks to supply ultra-low-power sensors for vibration, temperature, and pressure sensing. RF, vibration, and heat energy harvesting extends sensor lifespan and allows predictive maintenance, reducing unplanned downtime. Organizations like Energous are offering scalable wireless charging ecosystems that enhance automation, operational efficiency, and sustainability in industrial environments.

Wireless Power Supply Systems Market Share and Segmentation Insights

Market Share by Technology: Inductive Charging Dominates, RF Gains Ground

Inductive charging holds the largest market share at 62%, driven by widespread integration into consumer electronics such as smartphones, wearables, and wireless earbuds. Its proven efficiency, safety certifications, and established manufacturing ecosystem make it the default choice for high-volume applications. Resonant charging (28%) is gaining popularity in medium-power use cases due to its extended spatial freedom and multi-device charging capability, making it ideal for commercial and industrial settings. Radio frequency (RF) charging, though still a smaller segment, is rapidly expanding in low-power, long-distance IoT applications, with hybrid systems that combine inductive, resonant, and RF technologies emerging in premium solutions for specialized markets.

Market Share by Application: Consumer Electronics Lead, Automotive on the Rise

Consumer electronics command 45% of the market, fueled by the near-ubiquitous adoption of wireless charging in flagship smartphones and wearables from leading brands like Apple and Samsung. Automotive applications account for 25%, with strong growth driven by both in-cabin wireless device charging and the rollout of EV wireless charging infrastructure, including dynamic charging pilots. The industrial segment (15%) is leveraging wireless power for mission-critical IoT sensors and robotics, while healthcare (10%) adoption is increasing in medical implants and portable equipment requiring sterile, cable-free power delivery. Aerospace and defense (5%) remain niche but promising, with use cases in in-flight systems, unmanned aerial vehicles, and soldier-worn electronics.

.png)

Competitive Landscape – Leading Innovators in the Wireless Power Supply Systems Market

Wireless power innovations advance magnetic resonance, far-field RF, and inductive charging, enhancing consumer, industrial, and automotive applications globally. Key players included are WiTricity, Powercast, Qualcomm, Energous Corporation, Powermat Technologies, Infineon Technologies, Texas Instruments, Renesas Electronics, Wi-Charge, Semtech, Ossia, TDK Corporation, NXP Semiconductors, Integrated Device Technology (IDT), Zens, Others.

Qualcomm Technologies, Inc. – Multi-Sector Wireless Power Leadership

Qualcomm delivers wireless charging platforms for consumer electronics and high-power EV applications, notably through its Halo magnetic resonance technology. Its solutions are optimized for easy integration into diverse devices, from smartphones to industrial tools, while actively supporting standardized infrastructure development.

Energous Corporation – Far-Field RF Charging Specialist

Energous’ WattUp technology offers over-the-air charging for multiple devices simultaneously, targeting IoT, industrial asset tracking, and medical applications. Its collaboration with Atmosic Technologies exemplifies its strategy to build an ecosystem around continuous, connector-free power delivery.

WiTricity Corporation – Magnetic Resonance Pioneer for EVs

Focused on EV wireless charging, WiTricity’s systems offer greater misalignment tolerance and extended range over inductive methods. Its patented charging platforms serve both passenger and commercial vehicles, with active contributions to global standard-setting for automotive wireless power.

Powermat Technologies Ltd. – Public & Enterprise Charging Infrastructure

Powermat specializes in inductive charging for consumer and enterprise environments, with installations in airports, cafes, and office furniture. Its sustainability initiatives especially through its partnership with Powercast position it as a key player in developing green wireless power ecosystems.

Samsung Electronics Co., Ltd. – Integrated Consumer Ecosystem Player

Samsung embeds wireless charging across its ecosystem of smartphones, smartwatches, and earbuds, ensuring Qi compatibility and reverse charging capabilities. Its Galaxy Watch8 series demonstrates the convergence of wireless charging with advanced health metrics and lifestyle integration.

United States: High-Power Innovation, Space-Based Energy, and Regulatory Readiness

The United States leads the high-power wireless charging landscape, with the Oak Ridge National Laboratory (ORNL) demonstrating a 270-kilowatt transfer to a light-duty EV paving the way for ultra-fast wireless charging that could fully replenish a car in minutes. Large-scale pilots like the Indiana DOT’s dynamic wireless power transfer (DWPT) project with Purdue University are testing in-motion charging for heavy-duty trucks, potentially transforming logistics and freight electrification.

Beyond terrestrial applications, the California Institute of Technology’s Space Solar Power Project marks a milestone in space-based power transmission, successfully beaming collected solar energy from orbit to Earth. Long-range RF power solutions from companies like Powercast are enabling battery-free operation of IoT devices over significant distances, and the FCC’s progressive regulatory approvals are providing a clear path for commercialization. On the consumer front, tech giants continue integrating Qi-standard and inductive charging into smartphones, wearables, and accessories, reinforcing wireless power as a default feature in modern electronics.

China: Standardization Push and IoT-Centric Growth

China is cementing its leadership role in wireless power through regulatory standardization, as shown by the September 1, 2024 "Provisional Regulations on Radio Management of Wireless Charging", which sets detailed technical and operational requirements, including frequency band allocation for both high- and low-power EV wireless charging. This regulatory clarity is expected to accelerate adoption across transportation and consumer electronics.

As the world’s largest manufacturing base for wireless power components, China’s competitive ecosystem supports both mass-market and high-end product lines. The country is also driving R&D in RF-to-electricity conversion for IoT devices, enabling long-distance, maintenance-free charging of connected sensors. E-commerce remains a dominant distribution channel, with livestream sales and platform-driven discovery helping domestic and international brands capture consumer attention.

European Union: Advanced R&D, Unified Standards, and Medical Applications

The European Union is channeling significant research funding into machine learning-enhanced wireless power designs to improve efficiency and stability under variable load conditions. Collaborative efforts like the COST Project are working toward a harmonized regulatory and technical framework that could streamline commercial deployment across member states.

One standout application area is healthcare, where European innovators are advancing resonant inductive coupling for powering implantable devices, reducing the need for invasive battery replacements. The EU’s circular economy mandate is also influencing product development, encouraging the creation of battery-free devices and sustainable power solutions that align with waste-reduction goals.

Japan: Industrial, Drone, and Sustainability-Driven WPT Applications

Japan’s wireless power sector is highly diversified, with industrial applications benefiting from partnerships between domestic firms and WiTricity to develop robust WPT solutions for heavy machinery and robotics. A breakthrough in drone endurance has come from Japanese researchers using air-core beam transmission to deliver power mid-flight, potentially enabling uninterrupted aerial missions for logistics, surveillance, and inspection.

Aligned with Japan’s 2050 net-zero target, there is a growing push for wirelessly powered, battery-free sensors in buildings to enable real-time energy optimization. This integration of WPT into smart infrastructure underscores Japan’s strategy of pairing advanced energy technology with its environmental commitments.

South Korea: High-Power, Medical, and Versatile Wireless Power Solutions

South Korea’s wireless power market features a strong high-power transfer segment, with companies developing systems capable of up to 4kW output and actively targeting European expansion. Innovation in healthcare is equally notable DGIST researchers have created an ultrasound-based wireless charging system for implantable medical sensors, achieving twice the efficiency of previous models and full charges in under two hours.

Korean manufacturers are deploying WPT across LED lighting, EVs, drones, and AGVs, emphasizing the versatility and cross-industry applicability of their technology. This multi-sector approach positions South Korea as both a technology innovator and a global market contender in advanced wireless power systems.

Wireless Power Supply Systems Market Report Scope

Wireless Power Supply Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.4 Billion

|

|

Market Size (2034)

|

$44.4 Billion

|

|

Market Growth Rate

|

16.3%

|

|

Segments

|

By Technology (Inductive, Resonant, Radio Frequency), By Application (Consumer Electronics, Automotive (Electric Vehicles), Industrial (Robotics), Healthcare (Medical Devices), Aerospace & Defense), By Component (Transmitters, Receivers, Power Amplifiers, Converters), By Power Range (Low-Power (1W-100W), Mid-Power (100W-1kW), High-Power (>1kW)), By Distance (Near-Field, Far-Field)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

WiTricity, Powercast, Qualcomm, Energous Corporation, Powermat Technologies, Infineon Technologies, Texas Instruments, Renesas Electronics, Wi-Charge, Semtech, Ossia, TDK Corporation, NXP Semiconductors, Integrated Device Technology (IDT), Zens, Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Wireless Power Supply Systems Market Segmentation

By Technology

- Inductive

- Resonant

- Radio Frequency

By Application

- Consumer Electronics

- Automotive

- Industrial

- Healthcare

- Medical Devices

- Aerospace & Defense

By Component

- Transmitters

- Receivers

- Power Amplifiers

- Converters

By Power Range

- Low-Power (1W-100W)

- Mid-Power (100W-1kW)

- High-Power (>1kW)

By Distance

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Wireless Power Supply Systems Market

- WiTricity

- Powercast

- Qualcomm

- Energous Corporation

- Powermat Technologies

- Infineon Technologies

- Texas Instruments

- Renesas Electronics

- Wi-Charge

- Semtech

- Ossia

- TDK Corporation

- NXP Semiconductors

- Integrated Device Technology (IDT)

- Zens

* List Not Exhaustive

Research Coverage

This report investigates the Wireless Power Supply Systems Market across consumer, automotive, industrial, medical, and aerospace use cases—delivering strategic breakthroughs, analysis reviews, and highlights on how inductive, resonant, and RF/far-field technologies are scaling from pads to room-scale power zones and EV infrastructure. Produced by USDAnalytics, the study maps standardization shifts (e.g., Qi2), OEM integration patterns, and commercialization levers from transmitters/receivers to power electronics. It also benchmarks high-growth adjacencies—dynamic EV charging, IIoT sensors, and implantable devices—so leaders can quantify runway by power range, distance, and component stack. This report is an essential resource for product strategists, investors, and policy makers seeking data-driven guidance on interoperability, safety, and business models that turn wireless power into ubiquitous infrastructure. Scope includes-

- Segmentation covered:

- By Technology: Inductive; Resonant; Radio Frequency

- By Application: Consumer Electronics; Automotive; Industrial; Healthcare; Medical Devices; Aerospace & Defense

- By Component: Transmitters; Receivers; Power Amplifiers; Converters

- By Power Range: Low-Power (1W–100W); Mid-Power (100W–1kW); High-Power (>1kW)

- By Distance: Near-Field; Far-Field

- Geographic scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Historical 2021–2024 and forecasts 2025–2034.

- Companies: Strategy assessments and profiles of 15+ innovators.

Methodology

USDAnalytics applies a triangulated approach blending primary interviews (standards bodies, EV/OEM engineering teams, chipset vendors, hospital technology leads, and industrial automation buyers) with secondary intelligence (standards specifications, patents, certification logs, import/export data, company filings, and retail/SKU trackers). Bottom-up sizing aggregates country-level shipments and installed base by technology, power range, and application, then reconciles top-down to macro device and EV production baselines. Forecasts use diffusion models for Qi2/automotive WPT adoption, price–performance learning curves in power semis, and scenario testing for regulatory emissions/EMC constraints. Competitive scoring evaluates efficiency at misalignment, thermal behavior, EMI compliance, bill-of-materials trends, and ecosystem lock-in (modules, software, certified accessories). All findings undergo multi-source triangulation and sensitivity analysis.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.