Wood Coatings Market Growth Supported by Sustainable Formulations and High-Performance Industrial Applications

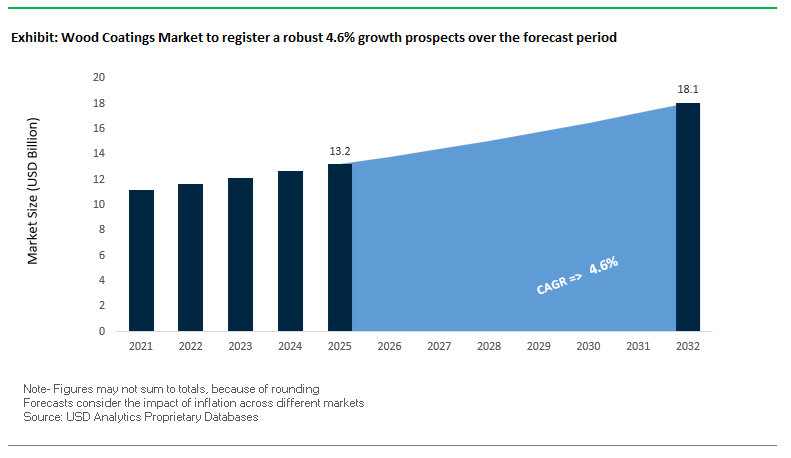

The global Wood Coatings Market was valued at $13.2 billion in 2025 and is projected to grow at a CAGR of 4.6% from 2025 to 2032, reaching $18.1 billion by 2032. This steady expansion is driven by increasing demand for durable, low-VOC, and aesthetically advanced coatings across furniture, cabinetry, flooring, and architectural wood applications. Wood coatings are evolving from basic protective layers into high-performance, multifunctional solutions that enhance durability, visual appeal, and environmental compliance.

A key growth driver is the rising adoption of sustainable and waterborne coating technologies, particularly in regions with strict environmental regulations. Manufacturers are transitioning toward bio-based resins, low-emission formulations, and energy-efficient curing systems, aligning with global decarbonization goals and indoor air quality standards. At the same time, advancements in UV-curable coatings, acrylic-polyurethane hybrids, and LED/EB curing technologies are enabling faster processing, reduced energy consumption, and improved surface performance, particularly in high-volume industrial manufacturing.

The market is also benefiting from the expansion of residential renovation, modular furniture, and ready-to-assemble (RTA) segments, which require coatings that support high-speed production, consistent finish quality, and resistance to wear, chemicals, and UV exposure. Additionally, the growing integration of functional coatings—such as anti-scratch, anti-yellowing, heat-reflective, and antimicrobial finishes—is expanding application scope, particularly in premium furniture and outdoor wood structures.

Market Analysis: Strategic Realignment, Bio-Based Innovation, and Capacity Expansion Driving Competitive Landscape

The Wood Coatings Market is undergoing a transformation shaped by strategic restructuring, product innovation, and regional capacity expansion, as key players focus on enhancing performance and sustainability. A major development is Hempel’s 2026 global strategy launch and CEO succession plan, signaling a renewed focus on commercial execution and customer-centric innovation in industrial wood and decorative coatings. This follows the successful integration of the Farrow & Ball brand, which strengthens Hempel’s position in the premium coatings segment.

Product innovation remains a core competitive lever. PPG’s launch of AQUACRON® waterborne shop primers (March 2026) introduces a new polymer platform that is being extended to wood substrates, enabling rapid curing, ultra-low VOC emissions, and compatibility with high-speed production lines. Similarly, Axalta’s “Solar Boost” reflective technology (January 2026) enhances UV stability and gloss retention, addressing the growing demand for durable outdoor wood coatings in architectural and furniture applications.

Sustainability-driven advancements are accelerating across the market. AkzoNobel’s RUBBOL WF 3350 bio-based coating (February 2025), featuring 20% renewable content, represents a significant milestone in delivering industrial-grade durability with reduced carbon footprint. Complementing this, Teknos’ TEKNOLUX AQUA 1728, unveiled at LIGNA 2025, integrates compatibility with UV, LED, and electron beam curing, enabling up to 30% energy savings and faster production cycles for interior wood applications.

Capacity expansion and regional manufacturing strategies are reinforcing market growth. Hempel’s Zhangjiagang facility in China, reaching its full 200,000-tonne capacity, serves as a critical hub for supplying advanced waterborne wood coatings across Asia-Pacific. Meanwhile, Sherwin-Williams’ expansion in Central Canada (October 2025) enhances localized service capabilities and automated tinting solutions for manufacturers operating in harsh climatic conditions.

Innovation is also targeting production efficiency and workflow optimization. Teknos’ launch of UVILUX PUTTY 1465 enables instant UV curing, eliminating bottlenecks in automated flooring lines and improving throughput. Additionally, Gemini Coatings’ acquisition of Hood Finishing Products strengthens its presence in the custom cabinetry and millwork segment, expanding its distribution network and specialty product portfolio.

Further reinforcing market evolution, Hempel’s Farrow & Ball Flat Eggshell launch combines premium aesthetics with industrial-grade durability, reflecting the convergence of decorative and industrial coating requirements. Collectively, these developments highlight a market transitioning toward bio-based, high-performance, and production-efficient wood coating solutions, supported by strategic realignment, innovation in curing technologies, and expanding global manufacturing capabilities.

Market Trend: CARB 2025–2026 VOC Regulations Driving Waterborne Wood Coatings Transition

The implementation of the California Air Resources Board 2025–2026 Suggested Control Measure is significantly transforming the global wood coatings market, establishing a stringent VOC ceiling of 50 g/L across multiple California air districts. This regulatory shift is positioning California as the most demanding market for low-VOC wood coatings, accelerating the transition from traditional solvent-based systems to advanced waterborne wood coatings.

Conventional nitrocellulose and acid-catalyzed wood finishes, which typically emit between 500 and 700 g/L of VOCs, are being rapidly phased out under the 2026 compliance framework. In their place, manufacturers are adopting one-component and two-component waterborne wood coating systems capable of maintaining VOC levels below 50 g/L while preserving critical attributes such as film clarity, gloss retention, and surface smoothness.

In parallel, the regulatory focus on hazardous air pollutant reduction is driving further innovation in eco-friendly wood coatings. The use of bio-based coalescents with high boiling points and zero VOC contribution under EPA Method 24 is becoming standard practice. This is strengthening the market position of sustainable wood coatings and enabling manufacturers to meet both VOC and HAP compliance requirements without compromising performance.

Market Trend: China GB/T 41662-2025 Standard Elevating Hygrothermal Stability and Aesthetic Durability

China’s GB/T 41662-2025 standard, fully enforced by early 2026, is redefining quality benchmarks in the wood coatings market by shifting focus from chemical compliance to mechanical and environmental performance. The emphasis on hygrothermal stability is particularly relevant for high-humidity regions, where coating failure has historically impacted durability and maintenance cycles.

The regulation mandates a minimum wet bond strength of 0.4 MPa after 168 hours of continuous water immersion, effectively eliminating lower-quality waterborne coatings from the commercial joinery and furniture segments. This is driving increased adoption of polymer-modified coatings and high-performance waterborne systems capable of delivering superior adhesion and moisture resistance.

In addition to durability, the standard enforces strict aesthetic performance criteria. For first-grade wood coatings, the Delta b value must remain below 1.5 after 500 hours of UV exposure, ensuring minimal yellowing and long-term color stability. This requirement is accelerating the shift toward acrylic-urethane hybrid coatings, which offer enhanced UV resistance and visual consistency compared to legacy waterborne alkyd systems. These advancements are strengthening the demand for premium wood coatings in residential, commercial, and export-oriented furniture manufacturing markets.

Market Opportunity: High-Hardness Waterborne Wood Coatings Expanding into Commercial Interior Applications

The increasing demand for durable and low-maintenance finishes in commercial interiors is creating significant opportunities for high-hardness waterborne wood coatings. These advanced systems are gaining traction in segments such as commercial flooring, retail environments, hospitality spaces, and office furniture, where mechanical durability is critical.

Next-generation two-component waterborne coatings based on polyurethane dispersions are achieving pencil hardness levels of 2H or higher within 48 hours of application. This provides enhanced scratch resistance and surface durability required for high-traffic environments, enabling waterborne coatings to compete directly with solvent-based polyurethane systems.

Abrasion resistance performance is also improving, with these coatings demonstrating mass loss below 20 milligrams per 1,000 cycles in ASTM D4060 Taber Abrasion testing. This ensures long-term resistance to wear and tear, making them suitable for demanding applications such as commercial flooring and hospitality interiors.

Chemical resistance further enhances their applicability, with modern waterborne coatings showing no degradation after 24-hour exposure to aggressive substances including cleaning agents, alcohol, and alkaline solutions. This makes them ideal for use in office furniture, countertops, and cafeteria surfaces where hygiene and durability are essential.

Market Opportunity: UV-Curable Wood Coatings Driving High-Speed Manufacturing and Efficiency Gains

The growing emphasis on production efficiency and throughput optimization is creating strong opportunities for UV-curable wood coatings and waterborne UV technologies in the furniture manufacturing sector. These advanced systems combine the environmental benefits of waterborne coatings with the rapid curing capabilities of UV technology, enabling significant improvements in manufacturing productivity.

Modern UV-curable wood coatings support production line speeds exceeding 20 meters per minute in high-speed digital and roller-coating processes, far surpassing the 5 to 10 meters per minute typical of conventional air-dry waterborne coatings. This enables manufacturers to increase output while maintaining consistent coating quality.

Energy efficiency is a key advantage, with UV-LED curing systems reducing oven energy consumption by 50% to 60% compared to traditional thermal drying methods. This contributes to lower operational costs and aligns with sustainability targets in industrial manufacturing.

The rapid curing capability of these coatings, achieving full cure in less than 10 seconds, allows for immediate stacking and packaging of finished products. This significantly reduces production cycle times and enables a reduction of approximately 30% in factory floor space requirements by minimizing drying tunnel length and eliminating cooling zones. These benefits are positioning UV-curable wood coatings as a critical innovation in high-performance and sustainable furniture finishing technologies.

Wood Coatings Market Share and Segmentation Insights

Paints and Enamels Lead with 33.6% Share Due to Full Coverage and High-Volume Applications

The paints and enamels segment dominates the wood coatings market with a 33.6% market share in 2025, driven by its ability to deliver both aesthetic enhancement and superior surface protection. In the wood coatings and decorative finishes market, paints and enamels provide complete color coverage, effectively hiding wood grain imperfections and surface defects, making them ideal for furniture, trim, siding, fencing, and decking applications. These coatings offer excellent resistance to UV radiation, moisture, and abrasion, ensuring long-term durability in both interior and exterior environments. Their widespread use across residential construction, renovation, and commercial projects positions them as the highest volume segment within the wood coatings industry. Additionally, the growing demand for custom color finishes, weather-resistant coatings, and long-lasting protection further supports their dominance. As consumers prioritize durability, aesthetics, and ease of maintenance, paints and enamels continue to lead the global wood coatings market.

Premium Wood Coatings Lead with 35.7% Share Driven by Durability and Brand Differentiation

The premium segment leads the wood coatings market by performance grade with a 35.7% market share in 2025, reflecting increasing demand for high-performance, long-lasting coating solutions. In the premium wood coatings and advanced protective finishes market, these products offer extended service life of 5–10 years for exterior applications, along with enhanced UV resistance, color retention, and fade protection, making them ideal for high-value residential and commercial wood surfaces. Consumers and professionals are increasingly willing to invest in premium coatings due to their lower maintenance requirements and long-term cost savings. Additionally, major industry players such as PPG, Sherwin-Williams, AkzoNobel, and Benjamin Moore are driving innovation through proprietary resin technologies and advanced additive systems, enabling superior performance and brand differentiation. As demand rises for high-quality, durable, and aesthetically superior wood finishes, the premium segment continues to dominate the global wood coatings market.

Competitive Landscape Analysis of the Wood Coatings Market

AkzoNobel Expands Waterborne Wood Coatings Leadership Through Axalta Merger Strategy

AkzoNobel N.V. is reinforcing its leadership in the wood coatings market through its ongoing merger with Axalta Coating Systems, expected to finalize in late 2026. The company reported a Q1 2026 adjusted EBITDA margin of 14.5%, driven by its Industrial Excellence program and manufacturing optimization initiatives, including six site closures in 2025. Its “Rhythm of Blues” 2026 collection incorporates water-based pigments and bio-attributed materials developed in partnership with Arkema and BASF. Additionally, AkzoNobel upgraded its 4,000m² Pilawa facility in Poland to enhance raw material storage and expand waterborne paint production capacity for the EMEA wood coatings market.

Sherwin-Williams Strengthens Premium Wood Coatings with AI-Driven Innovation

The Sherwin-Williams Company is a dominant force in the wood coatings market. Its Performance Coatings Group generated $1.71 billion in sales, driven by strong demand in industrial wood coatings. The company introduced SHER-WOOD® Environmentally Adaptive (EA) Hydroplus™ technology, a waterborne coating designed to maintain productivity across varying environmental conditions. Sherwin-Williams is integrating AI into product development to accelerate customized coating solutions and improve customer engagement. Its acquisition of Sayerlack has further strengthened its global leadership in high-end furniture finishes, particularly in premium Italian-style coatings.

PPG Advances UV-Cured Wood Coatings for High-Speed Manufacturing

PPG Industries, Inc. is strengthening its position in the wood coatings market by focusing on sustainably advantaged products, which account for 43% of its total revenue in 2026. The company is targeting growth in residential renovation and modular furniture segments, supported by its acquisition of Ozark Materials. PPG’s industrial wood coatings portfolio emphasizes radiation-cured (UV) technology, enabling instant-cure finishes with zero VOC emissions, ideal for high-speed furniture production lines. The company also reported strong Q1 2026 performance, exceeding earnings expectations due to effective pricing strategies and improved supply chain stability.

Nippon Paint Expands Global Wood Coatings Footprint with APAC Growth Strategy

Nippon Paint Holdings Co., Ltd. continues to expand its presence in the wood coatings market, reporting consolidated revenue of ¥1,774.2 billion (USD 11.5 billion) in FY2025. The company holds the #1 position in Asia and ranks fourth globally, with strong growth driven by its NIPSEA operations. Its decorative wood coatings segment in China and India benefits from rapid urbanization and rising demand for furniture finishes. Nippon Paint is targeting an 8–9% revenue CAGR through 2027 under its decentralized management model. The integration of Cromology Group assets has also strengthened its position in the European wood coatings market.

Axalta Strengthens Industrial Wood Coatings with High-Performance Product Innovation

Axalta Coating Systems is a key player in the wood coatings market, achieving a record adjusted EBITDA of $1,128 million in FY2025 and targeting a 22% margin. Its Performance Coatings segment remains strong, generating $828 million in quarterly sales. The company launched the Zenamel™ range, designed specifically for cabinet manufacturing, offering superior chemical resistance and finish clarity. Axalta’s strategic focus includes maintaining its leadership in industrial wood and refinish coatings while preparing for integration with AkzoNobel. Its $100 million share repurchase program signals strong confidence in its operational strategy and future growth trajectory.

China’s Regulatory Reform and Food-Safe Innovation Accelerating Waterborne Wood Coatings Adoption

China continues to dominate the global wood coatings market, driven by aggressive environmental regulations and a large-scale transition toward waterborne technologies. The implementation of GB 4806.10-2025 is significantly tightening safety requirements for coatings used in indirect food-contact applications such as kitchen cabinetry and wooden dining products. This regulatory shift is compelling manufacturers to adopt low-VOC waterborne polyurethane coatings to meet both domestic and export compliance standards.

Government initiatives are reinforcing this transformation through the expansion of VOC-related regulatory systems, including higher taxes on high-VOC coatings, effectively incentivizing water-based alternatives. Industrial infrastructure is also evolving, with the development of “Green Furniture” clusters in the Pearl River Delta that feature centralized treatment facilities tailored for waterborne coating processes. Technological advancements such as intermittent coating systems are improving production efficiency in wood laminate manufacturing. China’s leadership in ready-to-assemble (RTA) furniture further strengthens demand for waterborne coatings that offer low odor, rapid drying, and superior export readiness.

United States: AI Integration and LED-UV Innovation Driving Wood Coatings Market Growth

The United States wood coatings market is undergoing a transformation characterized by digitalization and advanced curing technologies. The integration of artificial intelligence into formulation processes is significantly reducing development timelines for custom waterborne coatings, enhancing product innovation and responsiveness to market demands. Technologies such as environmentally adaptive waterborne coatings are addressing performance challenges across varying humidity conditions, improving production efficiency.

Regulatory pressure is also a key driver, with stricter VOC limits under federal and state regulations accelerating the shift toward waterborne and UV-curable coatings. Investments in modern manufacturing facilities are supporting the adoption of LED-UV curing systems, enabling faster production cycles and energy efficiency. Product innovations targeting the cabinet refacing market are expanding application opportunities, particularly in residential renovation projects. High demand in custom cabinetry and commercial furniture segments is further driving the adoption of fast-curing, high-performance waterborne coatings in the U.S. market.

Germany: Bio-Based Resin Leadership and Circular Economy Integration

Germany remains at the forefront of the European wood coatings market, driven by its focus on sustainability and advanced material science. The commercialization of bio-based polyurethane dispersions is significantly enhancing the performance of waterborne coatings while reducing environmental impact. These innovations are particularly important for preserving the aesthetic quality of light-colored wood species by minimizing yellowing.

Investments in circular economy infrastructure are enabling the production of bio-attributed resin precursors, reducing emissions across the value chain. Advanced product innovations, such as self-healing coatings, are improving durability in high-traffic applications like hardwood flooring. Regulatory frameworks, including REACH and the DGNB certification system, are promoting the use of environmentally friendly coatings in public infrastructure projects. Technological advancements in application equipment, such as automated electrostatic sprayers, are improving efficiency and reducing waste, reinforcing Germany’s leadership in high-performance, sustainable wood coatings.

Vietnam: Export-Oriented Growth and Compliance with Global Standards

Vietnam is rapidly emerging as a key production hub in the wood coatings market, driven by its strong export orientation and compliance with international environmental standards. Infrastructure investments such as the Binh Duong Furniture Hub are enabling large-scale adoption of advanced coating technologies, including UV-LED systems that support low-emission manufacturing processes.

Government initiatives are promoting the use of waterborne coatings in residential and commercial applications, particularly in social housing projects. Regulatory requirements for VOC monitoring are pushing manufacturers to upgrade to compliant coating systems, enhancing export competitiveness. The presence of global coating companies in Vietnam is accelerating knowledge transfer and adoption of advanced technologies. High-volume production of outdoor furniture is a key application area, with waterborne acrylic coatings replacing traditional oil-based finishes to meet sustainability standards and improve UV resistance.

Italy: Premium Design Innovation and High-Performance Waterborne Coatings

Italy continues to lead in high-end wood coatings, focusing on aesthetic innovation and premium performance. The development of “natural-touch” waterborne finishes is enabling manufacturers to replicate the look and feel of untreated wood while maintaining high chemical resistance. These coatings are particularly востребованы in luxury furniture and interior design applications.

Technological advancements include antimicrobial coatings incorporating silver-ion technology, catering to healthcare and hospitality sectors. Investments in automated manufacturing systems are enhancing production efficiency, particularly in complex furniture designs. Regulatory frameworks such as Green Public Procurement are promoting the use of sustainable coatings in public-sector furniture. Key application areas include bespoke cabinetry and luxury yacht interiors, where waterborne coatings provide safety, durability, and superior aesthetic quality. Innovations such as self-leveling coatings are also reducing labor costs and improving production efficiency in high-end woodworking applications.

India: Market Transformation and Domestic Manufacturing Expansion

India is undergoing a structural transformation in the wood coatings market, driven by domestic manufacturing expansion and evolving consumer preferences. Strategic acquisitions and investments by major players are reshaping the competitive landscape, increasing the availability of advanced waterborne coating solutions. Government initiatives, including tax reductions on eco-friendly coatings, are encouraging the adoption of water-based products in residential and DIY applications.

Infrastructure development, particularly in electronic manufacturing clusters, is creating new demand for coatings used in wood-plastic composite components. Product innovation is focused on hybrid coatings that combine the visual appeal of solvent-based finishes with the environmental benefits of water-based systems. The growing demand for smart furniture is also influencing coating requirements, with the need for compatibility with integrated electronic components. Technological advancements in drying systems are improving efficiency in humid conditions, supporting the widespread adoption of waterborne coatings across India.

Brazil: Bio-Polymer Innovation and Sustainable Wood Coatings Growth

Brazil is emerging as a key player in the global wood coatings market, leveraging its agricultural resources to develop bio-based coating solutions. Regulatory measures aimed at reducing lead content in coatings are accelerating the transition toward safer, waterborne technologies. The use of renewable raw materials such as sucrose-derived polyols and soybean-based resins is positioning Brazil as a leader in sustainable coating innovation.

Investments in local resin production are strengthening the domestic supply chain, reducing reliance on imports and improving cost competitiveness. Innovative applications such as “cool-wood” coatings are gaining traction, particularly in tropical regions where heat management is critical. The agricultural sector is also driving demand for water-repellent coatings used in structural timber and storage facilities. Government initiatives promoting sustainable timber exports are further boosting the adoption of eco-friendly coatings, reinforcing Brazil’s role in the global wood coatings market.

Wood Coatings Market Report Scope

Wood Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.2 Billion

|

|

Market Size (2032)

|

$18.1 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Resin Type (Polyurethane, Acrylics, Nitrocellulose, Unsaturated Polyester, Melamine Formaldehyde, Hybrid Systems), By Product (Stains and Varnishes, Shellac Coatings, Wood Preservatives, Water Repellents, Paints and Enamels, Sealers and Fillers), By Technology (Solvent-borne, Waterborne, Radiation Cured, Powder Coating), By End-User Industry (Residential, Commercial, Industrial, Institutional), By Performance (Premium, Standard Industrial Grade, Eco-friendly, Bio-based)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., Axalta Coating Systems Ltd., BASF SE, Kansai Paint Co., Ltd., RPM International Inc., Jotun A/S, Asian Paints Limited, Hempel A/S, Teknos Group, Berger Paints India Limited, Masco Corporation, Sika AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Wood Coatings Market Segmentation

By Resin Type

- Polyurethane

- Acrylics

- Nitrocellulose

- Unsaturated Polyester

- Melamine Formaldehyde

- Hybrid Systems

By Product

- Stains and Varnishes

- Shellac Coatings

- Wood Preservatives

- Water Repellents

- Paints and Enamels

- Sealers and Fillers

By Technology

- Solvent-borne

- Waterborne

- Radiation Cured

- Powder Coating

By End-User Industry

- Residential

- Commercial

- Industrial

- Institutional

By Performance

- Premium

- Standard Industrial Grade

- Eco-friendly

- Bio-based

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Wood Coatings Industry

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Axalta Coating Systems Ltd.

- BASF SE

- Kansai Paint Co., Ltd.

- RPM International Inc.

- Jotun A/S

- Asian Paints Limited

- Hempel A/S

- Teknos Group

- Berger Paints India Limited

- Masco Corporation

- Sika AG

*- List not Exhaustive