Wood Protection Coatings and Preservatives Market Expansion Driven by Infrastructure Demand and Advanced Biocidal Technologies

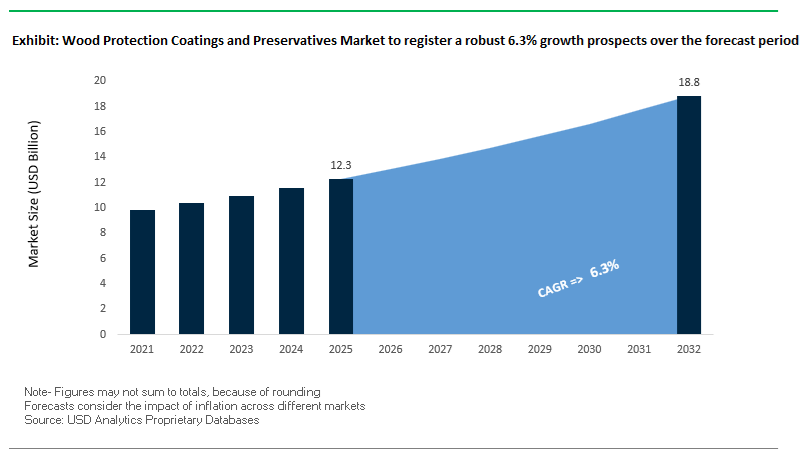

The global Wood Protection Coatings and Preservatives Market was valued at $12.3 billion in 2025 and is projected to grow at a CAGR of 6.3% from 2025 to 2032, reaching $18.9 billion by 2032. This above-average growth is being driven by rising demand for durable, long-life wood protection solutions across infrastructure, residential construction, utilities, and industrial applications. The market is increasingly shaped by the need to enhance wood longevity, resistance to biological degradation, fire protection, and environmental durability, particularly in outdoor and high-load structural applications.

A key structural growth driver is the surge in infrastructure modernization and energy grid expansion, especially linked to the rapid buildout of data centers, renewable energy systems, and AI-driven industrial facilities. Treated wood products—such as utility poles, railway ties, and structural timber—require advanced preservative systems capable of delivering long-term resistance against fungi, insects, moisture, and extreme weather conditions. Additionally, the increasing adoption of engineered wood and mass timber construction is further amplifying demand for high-performance protective coatings.

Sustainability is becoming a central pillar of market evolution. Manufacturers are transitioning toward low-VOC, waterborne preservative systems, bio-based chemicals, and halogen-free flame retardants, aligning with global environmental regulations and green building standards. Innovations in nanotechnology-based preservatives, antimicrobial coatings, and multifunctional protection systems are enabling deeper penetration, improved efficacy, and reduced environmental impact. Furthermore, the integration of digital tools such as carbon footprint calculators and lifecycle assessment platforms is enhancing transparency and enabling customers to make data-driven product selections.

Market Analysis: Infrastructure-Led Demand, Sustainability Initiatives, and Strategic Restructuring Reshaping Market Dynamics

The Wood Protection Coatings and Preservatives Market is undergoing a transformation driven by infrastructure-led demand growth, sustainability-focused innovation, and strategic corporate restructuring, redefining competitive dynamics across global markets. A major development is Koppers’ 2026 strategy targeting utility poles for AI and data center infrastructure, with the company projecting an 11% demand increase for industrial-grade preservatives. This reflects the growing importance of treated wood in electrical grid expansion and digital infrastructure development, particularly in North America.

Supply chain integration and portfolio optimization are also shaping market positioning. Koppers’ acquisition of Douglas Fir supply assets (January 2026) strengthens its access to high-quality raw materials for treated wood applications, while its divestment of the Railroad Structures division (August 2025) enables a sharper focus on high-margin performance chemicals and advanced wood preservation technologies. Additionally, the company’s “Catalyst” transformation program has improved operational efficiency and profitability through plant optimization and localized production strategies.

Sustainability-driven innovation continues to accelerate across the market. AkzoNobel’s “It All Adds Up” campaign (December 2025) promotes the adoption of zero-VOC UV coating systems and waterborne preservatives, supported by digital carbon footprint tools. Similarly, Bona’s achievement of a 46% reduction in greenhouse gas emissions (June 2025) highlights the industry’s shift toward renewable energy-powered manufacturing and low-impact chemical formulations.

Product innovation is increasingly focused on multifunctionality and environmental safety. Greentai’s launch of LignoShield NanoFlameX (April 2025) introduces a nanotechnology-based preservative that combines biocidal protection with halogen-free flame retardancy, addressing both durability and fire safety requirements in construction and renewable energy applications. Meanwhile, Sherwin-Williams’ 2026 wood protection trend forecast introduces waterborne preservative-stain hybrids that deliver enhanced grain clarity alongside regulatory-compliant biocidal performance.

Operational restructuring is further enhancing global competitiveness. Arxada’s implementation of the “One Lonza” strategy (April 2025) streamlines production of specialty biocides, accelerating global deployment of advanced preservative solutions such as Tanasote S40. Additionally, AkzoNobel’s “Rhythm of Blues” collection (September 2025) integrates antimicrobial and anti-fungal protection directly into decorative coatings, reducing application steps and improving manufacturing efficiency.

Market Trend: EPA CCA Phase-Out Driving Shift Toward Arsenic-Free Wood Preservatives

The enforcement of the EPA’s 2024–2026 registration review final rule is significantly transforming the wood protection coatings and preservatives market by accelerating the phase-out of Chromated Copper Arsenate in industrial applications. As of early 2026, stricter handling, disposal, and reporting requirements are making arsenic-based preservatives economically unviable, pushing manufacturers toward safer alternatives such as Alkaline Copper Quaternary and Copper Azole systems.

Advanced micronized copper azole formulations are demonstrating a 90% reduction in copper leaching compared to earlier ACQ systems, making them highly suitable for environmentally sensitive applications near marine and freshwater ecosystems. This performance improvement is strengthening the adoption of eco-friendly wood preservatives and sustainable wood treatment chemicals.

Additionally, modern copper-based preservatives are incorporating corrosion inhibitors, significantly enhancing compatibility with metal fasteners. These systems are achieving up to three times longer lifespan for galvanized steel components in pressure-treated wood compared to earlier formulations. The updated EPA toxic release reporting thresholds introduced in March 2026 are further reinforcing the transition, positioning arsenic-free wood preservatives as the only viable pathway for new wood treatment facilities.

Market Trend: EU BPR Creosote Ban Accelerating Adoption of Safer Wood Protection Alternatives

The European Union Biocidal Products Regulation is driving a major transformation in the wood preservatives market through the effective phase-out of creosote. By 2026, several EU member states have officially prohibited the placement of creosote-treated utility poles on the market, marking a decisive shift toward non-toxic wood protection solutions.

Copper-oil systems and bio-based preservative oils are now replacing creosote in approximately 65% of new utility pole installations, delivering comparable service life of up to 40 years without the associated carcinogenic risks. This transition is significantly increasing demand for environmentally friendly wood coatings and long-life wood protection systems across infrastructure applications.

The regulatory framework also includes strict transition timelines, with a 180-day window concluding in August 2026 for clearing existing inventories. This is forcing suppliers to rapidly adopt polymer-encapsulated preservatives and alternative treatment technologies, particularly in railway and utility sectors.

Furthermore, the classification of creosote-treated wood as hazardous waste across the EU is increasing disposal costs to €250–€400 per tonne. This economic pressure is driving a 40% increase in the specification of recyclable and non-toxic wood preservatives, reinforcing sustainability as a key market driver.

Market Opportunity: Transparent Wood Preservatives Enabling Protection Without Compromising Natural Aesthetics

The rapid growth of mass timber construction is creating strong opportunities for clear and transparent wood preservatives that protect structural wood while preserving its natural appearance. These coatings are increasingly used in premium timber applications such as glulam beams, cedar siding, and architectural wood elements.

Next-generation transparent wood coatings incorporate nano-scale UV absorbers capable of reducing ultraviolet transmittance to 5% or lower while remaining visually undetectable. This prevents surface degradation and discoloration, extending the aesthetic life of exposed wood by up to five years in high-UV environments.

In addition to UV protection, these coatings offer high vapor permeability, achieving perm ratings above 10. This allows timber structures to regulate internal moisture effectively, reducing the risk of internal rot by approximately 25%. This feature is particularly critical for large structural components in log homes and mass timber buildings.

Environmental compliance is also a key advantage, with premium transparent wood preservatives achieving VOC levels below 50 g/L. This aligns with LEED v4.1 low-emitting material requirements, making them suitable for sustainable construction projects and green building certifications.

Market Opportunity: Dual-Action Fire and Decay Resistant Coatings Driving Growth in High-Risk Environments

The increasing focus on wildfire resilience and building safety is creating significant opportunities for dual-action wood protection coatings that combine fire retardancy with fungal resistance. These advanced coatings are gaining traction in wildfire-prone regions such as North America and Australia, where building codes are becoming increasingly stringent.

Modern intumescent wood coatings are engineered to expand up to 50 times their original thickness when exposed to high temperatures, forming an insulating barrier that protects structural wood for 60 to 120 minutes during fire events. This level of protection is critical for meeting Class A fire rating requirements in high-risk zones.

At the same time, these coatings incorporate polymer-bound biocides that provide long-lasting resistance to fungal decay without the leaching issues associated with traditional treatments. They maintain performance even after prolonged exposure to weathering, passing accelerated aging tests without degradation in fire resistance properties.

The combined benefits of fire protection and biological resistance are also translating into economic advantages, as properties treated with certified dual-action coatings are receiving insurance premium reductions of 10% to 15% in wildfire-prone regions. This is positioning fire-retardant wood coatings and decay-resistant treatments as a high-growth segment within the advanced wood protection market.

Wood Protection Coatings and Preservatives Market Share and Segmentation Insights

Water-Based Preservatives Lead with 43.2% Share Due to Low-VOC Compliance and Ease of Use

The water-based preservatives segment dominates the wood protection coatings and preservatives market with a 43.2% market share in 2025, driven by increasing demand for environmentally friendly, low-toxicity wood treatment solutions. In the wood preservatives and protective coatings market, advanced formulations such as copper azole and alkaline copper quaternary (ACQ) have largely replaced traditional chromated copper arsenate (CCA) in residential and light commercial applications due to stringent environmental and safety regulations. These water-based systems offer low-VOC emissions, reduced odor, and safer handling, making them ideal for decking, fencing, outdoor furniture, and structural wood components. Additionally, they provide ease of application and soap-and-water cleanup, along with faster drying times compared to solvent- and oil-based alternatives. As sustainability and regulatory compliance continue to shape the industry, water-based preservatives remain the leading segment in the global wood protection coatings market.

Pressure Treatment Dominates with 56.5% Share Due to Deep Penetration and Structural Protection

The pressure treatment segment leads the wood protection coatings and preservatives market with a 56.5% market share in 2025, driven by its ability to deliver deep, long-lasting protection for structural wood applications. In the industrial wood treatment and construction materials market, pressure treatment processes force preservatives deep into the cellular structure of wood, providing superior resistance against rot, fungal decay, insects, and termite damage. This makes it the industry standard for utility poles, railway sleepers, decking, fencing, and outdoor structural components. A key growth driver is its compliance with building codes and standards such as AWPA and EN 335, which mandate pressure-treated wood for ground contact and high-exposure environments. As demand increases for durable, weather-resistant, and low-maintenance wood products, pressure treatment continues to dominate the global wood preservatives and protection coatings market, ensuring extended service life and structural reliability.

Competitive Landscape Analysis of the Wood Protection Coatings and Preservatives Market

Koppers Leads Wood Preservation Market with Micronized Copper and Lifecycle Solutions

Koppers Holdings Inc. dominates the wood protection coatings market, holding 22% share of the North American treated wood segment. In 2026, its Performance Chemicals division reported record sales, driven by a 12% surge in micronized copper preservatives. The company has evolved into a full-service provider through its Life-Cycle Asset Management program, targeting the USD 15 billion utility pole and railroad tie markets. Its MicroPro® Gen 3 preservative, featuring 90% recycled copper and GREENGUARD Gold certification, addresses sustainability trends in residential decking. With over 25 global facilities, Koppers is expanding into APAC infrastructure projects, particularly high-speed rail applications.

Lonza (Arxada) Expands Metal-Free Wood Preservatives Under REACH Compliance

Lonza (Arxada Wood Protection Division) is a global leader in the wood preservatives market, leveraging regulatory expertise and innovation. Following EU REACH phase-outs, the company transitioned to copper-azole and metal-free preservative systems, achieving a 20% rise in compliance-driven revenue in 2026. Its Wolmanized® Outdoor® Wood line remains a benchmark, with next-generation formulations incorporating carbon-capturing resins that improve dimensional stability by 18%. Lonza’s division recorded a 5.3% CAGR between 2024 and 2026, supported by demand from South Asian housing initiatives. With over 1,200 biocide registrations globally, Lonza maintains a strong competitive moat in regulatory compliance.

BASF Advances Nano-Copper Wood Preservatives for Sustainable Timber Construction

BASF SE is strengthening its position in the wood protection coatings market through innovation in sustainable preservatives and partnerships. In 2026, the company commissioned a net-zero carbon production line for copper-based preservatives, reducing energy costs by 15%. Its partnership with IKEA focuses on supplying low-VOC, bio-attributed wood impregnations for outdoor furniture. BASF’s Invisiguard™ Nano-Copper technology enables transparent protection while preserving natural wood grain, meeting the aesthetic demand for “Warm Minimalism.” The company holds a strong presence in the European timber construction sector, particularly in cross-laminated timber (CLT) applications for high-rise buildings.

Lanxess Expands High-Durability Wood Protection for Marine and Infrastructure Applications

Lanxess AG is a key player in the wood preservatives market, particularly in high-performance applications such as marine piling and infrastructure. The integration of Troy Corporation assets has increased its market share in wood fungicides and insecticides by 30% in Latin America. Its Preventol® range delivers up to 30-year service life in extreme saltwater environments, making it ideal for coastal infrastructure. Lanxess reported a 9% EBITDA increase in Q1 2026, driven by value-based pricing strategies. Its hybrid preservative-plus-coating systems reduce maintenance cycles by 40%, offering long-term cost savings for commercial boardwalk and infrastructure projects.

Sherwin-Williams Expands Consumer Wood Protection Solutions with Design-Focused Preservatives

Sherwin-Williams is strengthening its presence in the wood protection coatings market through its Wood Care division and brands like Thompson’s WaterSeal and Minwax. In 2026, the company capitalized on the “refresh rather than replace” trend, driving a 22% increase in demand for deck restorers and wood preservatives. Its design-focused Foundational Neutrals palette combines aesthetic appeal with durability, offering up to 5-year fade resistance. Sherwin-Williams also leverages AI-driven color matching across its 4,800+ stores to provide customized preservative solutions that meet regional and historical design requirements, enhancing its competitiveness in both DIY and professional segments.

Viance Drives Fire-Retardant and Non-Metallic Wood Preservatives Innovation

Viance, a joint venture of Dow and Venator, is advancing in the wood preservatives market with specialized solutions for safety and sustainability. Its D-Blaze® fire-retardant treated wood saw a 25% volume increase in 2026, driven by stricter wildfire building codes in key regions. The company’s Ecolife® non-metallic preservative is gaining traction in residential markets, achieving a 12.5% share in the kid-and-pet-safe lumber segment. Viance also benefits from strategic partnerships securing copper oxide supply, mitigating raw material volatility. Its advanced pressure-treatment technology ensures full penetration in difficult wood species, addressing critical performance challenges in construction applications.

China’s Transition to High-Performance Green Standards in Wood Protection Coatings

China continues to lead the global wood protection coatings and preservatives market, driven by stringent environmental regulations and rapid industrial modernization. The implementation of GB 30981.1-2025 is significantly tightening limits on hazardous substances such as phthalates and solvents, accelerating the adoption of eco-friendly, low-VOC wood protection coatings. These regulatory frameworks are reshaping the industry toward sustainable and high-performance waterborne solutions.

Technological innovation is playing a critical role in this transition. The development of water-borne vacuum pressure impregnation (VPI) technologies is replacing traditional preservative systems such as CCA, improving safety and environmental compliance. Government initiatives under the “Blue Sky” program are further incentivizing manufacturers to adopt UV-curable and water-based coatings. Demand is also rising in infrastructure and landscaping projects, particularly for bamboo-wood composites requiring advanced antifungal protection. Additionally, investments in automated roll-to-roll coating systems and innovations such as graphene-enhanced coatings are improving durability, fire resistance, and UV protection in modern wood applications.

United States: Infrastructure Modernization and Mass Timber Driving Market Expansion

The United States wood protection coatings market is experiencing strong growth, supported by infrastructure investments and the rising adoption of mass timber construction. Funding from federal initiatives such as the Inflation Reduction Act is driving the rehabilitation of wooden infrastructure, including utility poles and bridges, where advanced preservatives with reduced environmental impact are increasingly specified.

Regulatory pressures are accelerating the transition toward safer coating technologies. Tightened EPA standards are pushing manufacturers toward high-solids and water-reducible formulations, reducing emissions while maintaining performance. Innovation is also evident in the development of PFAS-free water-repellent preservatives tailored for residential decking applications. The growing use of cross-laminated timber (CLT) in urban construction is creating demand for specialized fire-retardant coatings. Additionally, the integration of AI-driven technologies in coating application processes is improving efficiency and material utilization, supporting the market’s technological advancement.

Germany: Circular Economy Leadership and Bio-Based Wood Protection Technologies

Germany remains at the forefront of sustainable wood protection coatings, driven by its focus on circular economy principles and stringent regulatory standards. Alignment with the EU Biocidal Products Regulation is accelerating the shift toward environmentally friendly preservative systems, including copper-azole and borate-based formulations. These developments are reducing reliance on traditional chemical treatments and enhancing environmental safety.

Innovation in Germany is centered on advanced material science and digitalization. The development of amine-free polyurethane dispersions is improving indoor air quality while maintaining high-performance standards. The integration of digital twin technologies in wood treatment facilities is enabling real-time monitoring and optimization of preservative application processes. Government initiatives such as DGNB certification requirements are promoting the use of non-toxic coatings in public infrastructure projects. Additionally, investments in recyclable construction materials are driving the development of wood protection solutions that support future reuse and sustainability goals.

Vietnam: Export Compliance and Advanced Manufacturing Integration

Vietnam is rapidly emerging as a high-growth market in the wood protection coatings segment, driven by its strong export orientation and compliance with international environmental standards. Regulatory frameworks requiring VOC monitoring are pushing manufacturers to adopt waterborne and low-emission coating systems, enhancing their competitiveness in global markets.

The Vietnam-EU Free Trade Agreement is further accelerating the adoption of compliant wood preservatives, particularly those aligned with European deforestation and sustainability regulations. Infrastructure investments in smart manufacturing clusters are enabling the integration of advanced coating technologies such as UV-LED curing, improving energy efficiency and production scalability. The growing demand for outdoor furniture is driving the use of durable waterborne acrylic coatings that meet international quality standards. Additionally, the presence of global coating companies is facilitating technology transfer and accelerating the adoption of advanced wood protection solutions.

India: Domestic Manufacturing Expansion and Smart Infrastructure Demand

India is witnessing significant growth in the wood protection coatings market, supported by increasing domestic manufacturing and infrastructure development. Strategic investments by major conglomerates are expanding the availability of advanced waterborne coating solutions, particularly in the wood-care segment. Government initiatives such as the Gati Shakti National Master Plan are driving demand for fire-retardant coatings in infrastructure projects including airports and metro systems.

Technological advancements are enabling the development of hybrid coatings that combine performance with environmental compliance. The growing adoption of Industry 4.0 technologies in woodworking is improving production efficiency and coating application precision. Demand is also rising in emerging applications such as wood-plastic composites and smart furniture, where coatings must meet both functional and aesthetic requirements. Regulatory frameworks set by green building organizations are further encouraging the use of low-VOC coatings, reinforcing the transition toward sustainable wood protection solutions in India.

Brazil: Bio-Polymer Innovation and Climate-Resilient Wood Protection

Brazil is leveraging its natural resource base to emerge as a leader in bio-based wood protection coatings. The use of renewable raw materials such as soybean and castor oil is driving the development of sustainable preservatives that offer natural UV resistance and durability in tropical climates. Regulatory initiatives promoting cleaner production processes are further supporting the adoption of eco-friendly coating technologies.

Innovation in Brazil is focused on addressing the challenges of high humidity and extreme weather conditions. Advanced formulations are being developed to maintain coating integrity and performance in demanding environments. Investments in sustainable packaging and bio-based materials are aligning the industry with environmental goals. Key applications include the protection of agricultural timber used in silos and fencing, where non-leaching, livestock-safe preservatives are essential. Additionally, the development of “cool-wood” coatings is helping reduce heat absorption in residential construction, supporting energy efficiency and climate resilience.

Canada: Mass Timber Innovation and Lifecycle-Focused Wood Protection

Canada is emerging as a global leader in the wood protection coatings market, driven by its strong focus on mass timber construction and lifecycle sustainability. Significant investments in high-rise timber projects are increasing demand for advanced protective coatings that maintain wood aesthetics while ensuring fire safety and durability.

Technological innovation is centered on improving the longevity and recyclability of wood structures. Research into reversible coatings and adhesives is enabling the disassembly and reuse of timber components, supporting circular construction practices. The development of nanotechnology-based preservatives is enhancing penetration and performance in dense wood species. Government initiatives, including mass timber action plans, are promoting the use of low-carbon, bio-based coatings. Additionally, investments in refining facilities are enabling the production of sustainable wood-protection materials from forestry waste, reinforcing Canada’s leadership in environmentally responsible wood coating solutions.

Wood Protection Coatings and Preservatives Market Report Scope

Wood Protection Coatings and Preservatives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.3 Billion

|

|

Market Size (2032)

|

$18.9 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Formulation Technology (Water-based Preservatives, Solvent-based Preservatives, Oil-based, Natural Oil Finishes and Bio-based Preservatives), By Active Ingredient Chemistry (Inorganic Ingredients, Organic Ingredients, Organic Solvent-borne), By Treatment Method (Pressure Treatment, Non-Pressure Treatment, Thermal Treatment), By Application (Decking and Fencing, Siding, Cladding and Roofing, Flooring and Woodwork, Cabinets and Furniture, Industrial Heavy Timber), By End-User Industry (Residential Construction, Commercial and Institutional Buildings, Infrastructure and Public Works, Industrial and Agriculture), By Performance Tier (Ground Contact, Above Ground, High-Hazard, Fire Retardant Preservatives)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Koppers Performance Chemicals, LANXESS AG, Arxada AG, BASF SE, The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Viance, LLC, RPM International Inc., Osmose Utilities Services, Inc., Nisus Corporation, Remmers Gruppe AG, Hempel A/S, Kurt Obermeier GmbH and Co. KG, Jotun A/S

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Wood Protection Coatings and Preservatives Market Segmentation

By Formulation Technology

- Water-based Preservatives

- Solvent-based Preservatives

- Oil-based

- Natural Oil Finishes and Bio-based Preservatives

By Active Ingredient Chemistry

- Inorganic Ingredients

- Organic Ingredients

- Organic Solvent-borne

By Treatment Method

- Pressure Treatment

- Non-Pressure Treatment

- Thermal Treatment

By Application

- Decking and Fencing

- Siding, Cladding and Roofing

- Flooring and Woodwork

- Cabinets and Furniture

- Industrial Heavy Timber

By End-User Industry

- Residential Construction

- Commercial and Institutional Buildings

- Infrastructure and Public Works

- Industrial and Agriculture

By Performance Tier

- Ground Contact

- Above Ground

- High-Hazard

- Fire Retardant Preservatives

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Wood Protection Coatings and Preservatives Industry

- Koppers Performance Chemicals

- LANXESS AG

- Arxada AG

- BASF SE

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Viance, LLC

- RPM International Inc.

- Osmose Utilities Services, Inc.

- Nisus Corporation

- Remmers Gruppe AG

- Hempel A/S

- Kurt Obermeier GmbH & Co. KG

- Jotun A/S

*- List not Exhaustive