Zero Friction Coatings Market Growth Driven by Advanced Surface Engineering and Energy-Efficient Industrial Applications

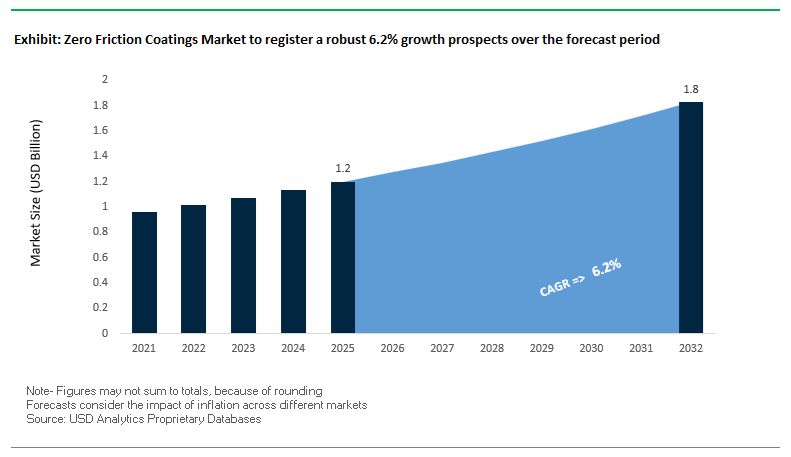

The global Zero Friction Coatings Market was valued at $1.2 billion in 2025 and is projected to grow at a CAGR of 6.2% from 2025 to 2032, reaching $1.8 billion by 2032. This growth is being driven by increasing demand for ultra-low friction, wear-resistant, and energy-efficient surface coatings across automotive, aerospace, electronics, packaging, and industrial machinery applications. Zero friction coatings are engineered to minimize surface drag, mechanical wear, and energy loss, significantly improving operational efficiency and extending component lifespan.

A primary growth driver is the rising adoption of precision-engineered components in sectors such as electric vehicles (EVs), hydrogen fuel systems, and high-speed automation, where even minor friction reductions can deliver measurable gains in energy efficiency, thermal management, and system reliability. These coatings are increasingly utilized in bearings, seals, threaded components, and moving mechanical assemblies, enabling smoother operation under extreme conditions, including high pressure, temperature, and chemical exposure.

Technological advancements are significantly enhancing the performance of zero friction coatings. Innovations in polymer-based lubricative coatings, nano-engineered surfaces, and hybrid inorganic-organic formulations are enabling superior non-stick properties, abrasion resistance, and chemical stability. Additionally, the integration of bio-based lubricative materials and waterborne coating systems is aligning product development with sustainability goals, reducing reliance on traditional solvent-based lubricants.

The market is also benefiting from the expansion of automated manufacturing and high-speed production lines, particularly in packaging and electronics, where low-friction coatings improve throughput and reduce maintenance requirements. Furthermore, the growing focus on clean-room manufacturing environments and contamination-sensitive applications is increasing demand for coatings that provide dry lubrication without particulate generation.

Market Analysis: Laser-Curing Innovation, Hydrogen-Compatible Coatings, and Sustainable Formulations Reshaping Market Dynamics

The Zero Friction Coatings Market is evolving rapidly, driven by cutting-edge curing technologies, hydrogen economy integration, and sustainability-focused innovation, redefining competitive dynamics across industries. A major breakthrough is AkzoNobel’s launch of Interpon laser-curing technology (February 2026), developed in partnership with IPG Photonics. This system enables selective, ultra-fast curing of low-friction powder coatings, significantly reducing energy consumption and allowing application on temperature-sensitive substrates, marking a step-change in industrial coating efficiency.

Sustainability and regulatory compliance are also shaping product innovation. Henkel’s expansion of water-based low-friction barrier coatings (April 2026) addresses the EU’s Packaging and Packaging Waste Regulation (PPWR) by replacing plastic-based lubricants with high-slip, non-stick coating formulations for automated packaging lines. Similarly, the AkzoNobel–BASF collaboration (May 2025) introduces low-carbon industrial coatings using bio-attributed resins, including low-friction variants designed for large-scale machinery.

The hydrogen economy is emerging as a key application area. DuPont’s MOLYKOTE® HP-300 (January 2025) achieved certification under ISO 14687:2019 hydrogen purity standards, making it suitable for fuel cell stacks and high-pressure refueling systems without contaminating hydrogen. This development highlights the growing importance of clean, non-reactive, zero-friction coatings in next-generation energy systems.

Operational efficiency and localization strategies are also influencing market growth. Nippon Paint’s Direct-to-Factory (D2F) logistics expansion (February 2026) streamlines the supply of anti-friction coatings to automotive and electronics OEMs, particularly in clean-room manufacturing environments. Meanwhile, PPG’s expansion of small-batch, high-performance coating production in Italy (September 2025) enables customized solutions for precision industries such as medical devices and aerospace.

Advanced material innovation continues to expand application boundaries. Mankiewicz’s “Resilience” coatings series (November 2025) introduces ultra-low-friction topcoats designed for consumer electronics and aerospace interiors, combining tactile smoothness with resistance to fingerprints and abrasion. Additionally, AkzoNobel’s bio-based interior coatings derived from rapeseed and pine oil demonstrate the shift toward plant-based, low-friction surface solutions in automotive interiors.

Sustainability in production is also gaining traction. AkzoNobel’s solar-powered manufacturing facility in Poland supports the production of low-emission coatings, ensuring that even energy-intensive processes for advanced materials are aligned with renewable energy adoption.

Market Trend: EPA TSCA PFAS Reporting Driving Transition Away from PTFE-Based Zero Friction Coatings

The enforcement of EPA TSCA Section 8(a)(7) is significantly reshaping the zero friction coatings market, particularly by intensifying regulatory scrutiny on PFAS-based materials such as PTFE coatings. As of April 13, 2026, the mandatory reporting window requires manufacturers and importers to disclose detailed information on PFAS usage over a 12-year period, including chemical composition, production volumes, and byproduct data.

This comprehensive reporting requirement is accelerating the phase-out of PTFE-based low-friction coatings, as even trace levels of intentionally added PFAS must now be documented. The regulatory environment is becoming increasingly stringent, with limited scope for de minimis exemptions, forcing manufacturers to adopt transparent chemical management practices.

In parallel, updates to the Design for the Environment certification have effectively excluded PFAS-based coatings from green procurement programs, further reducing their market viability. This is driving a strong shift toward PFAS-free coatings, including silicon-based lubricious coatings and advanced polymer friction modifiers. These alternatives are gaining traction across industrial, automotive, and aerospace applications, positioning PFAS-free zero friction coatings as a critical growth segment in the sustainable coatings market.

Market Trend: EU REACH Nanomaterial Regulations Driving Substitution of MoS₂-Based Lubricant Coatings

The updated EU REACH framework is introducing stricter controls on nanomaterials, significantly impacting the use of molybdenum disulfide in zero friction coatings. Under the 2025–2026 nanomaterial definition, coatings containing particles with more than 50% of their distribution below 100 nanometers are subject to enhanced toxicological evaluation and compliance requirements.

Manufacturers are now required to meet Annex VIII obligations, including detailed safety profiling and risk assessment for nano-scale friction-reducing agents. This has increased compliance costs and complexity, particularly for small-batch and specialty coating producers operating in the European market.

As a result, industrial sectors such as aerospace and defense are actively transitioning away from MoS₂-based dry-film lubricants toward alternative materials such as tungsten disulfide and graphene-based nanocomposites. These substitutes offer comparable or superior friction reduction performance while avoiding regulatory constraints, reinforcing the trend toward safer and compliant nanotechnology coatings.

Market Opportunity: Diamond-Like Carbon Coatings Enabling High-Efficiency EV Powertrain Performance

The rapid expansion of the electric vehicle market is creating substantial opportunities for diamond-like carbon coatings in the zero friction coatings industry. These coatings are increasingly used in EV powertrain components to enhance efficiency, reduce wear, and extend operational lifespan.

Advanced hydrogen-free DLC coatings are demonstrating friction reduction levels of 50% to 70% compared to uncoated steel surfaces. This reduction in friction translates directly into improved energy efficiency, contributing to a 1.5% to 3% increase in battery range for electric vehicles.

In high-load applications such as planetary gear systems, DLC coatings provide exceptional wear resistance, extending component lifespan by up to ten times by preventing surface scuffing during repetitive start-stop cycles. This is particularly critical for electric motors, which operate under high torque conditions.

Thermal stability is another key advantage, with modern DLC coatings maintaining performance at temperatures up to 450°C. This enables the use of minimal lubrication or dry operating conditions, reducing maintenance requirements and fluid drag in EV gearboxes. These benefits are positioning DLC coatings as a cornerstone technology in next-generation automotive engineering and advanced tribological coatings.

Market Opportunity: Graphene-Based Coatings Driving Performance Gains in Wind Energy Applications

The offshore wind energy sector is emerging as a key growth area for graphene-based zero friction coatings, particularly in large-scale turbine applications where durability and reliability are critical. With turbine capacities exceeding 15 megawatts in 2026, the demand for advanced coating solutions that reduce wear and corrosion is increasing significantly.

Graphene-polyurethane hybrid coatings are demonstrating a 30% reduction in wear rates for critical components such as main shaft bearings. This performance improvement is translating into substantial cost savings, with lifecycle maintenance reductions estimated at $150,000 per turbine.

In terms of friction performance, graphene-infused coatings maintain a stable coefficient of friction below 0.05 even under high-humidity maritime conditions. This outperforms traditional lubrication systems and ensures consistent performance in offshore environments.

These coatings also provide enhanced corrosion protection, achieving more than 2,000 hours of salt spray resistance. This dual functionality of friction reduction and corrosion resistance prevents micro-pitting and structural degradation, which are common causes of failure in wind turbine components.

The integration of graphene-based coatings into renewable energy infrastructure is therefore driving innovation in high-performance, sustainable coating technologies, positioning them as a key solution in the evolving zero friction coatings market.

Zero Friction Coatings Market Share and Segmentation Insights

PTFE Coatings Lead with 39.4% Share Due to Lowest Friction and High Chemical Stability

The polytetrafluoroethylene (PTFE) segment dominates the zero friction coatings market with a 39.4% market share in 2025, driven by its exceptionally low coefficient of friction (0.05–0.10) and unmatched performance across industrial applications. In the low-friction coatings and surface engineering market, PTFE is widely used in bearings, bushings, fasteners, seals, and food processing equipment, where reduced wear and smooth motion are critical. A key advantage is its broad operating temperature range from -200°C to +260°C, combined with excellent chemical inertness, making it highly suitable for demanding environments in automotive, aerospace, chemical processing, and semiconductor manufacturing industries. Additionally, PTFE coatings offer non-stick properties, corrosion resistance, and long service life, reinforcing their dominance in the advanced tribological coatings market. As industries increasingly focus on efficiency, durability, and reduced maintenance, PTFE continues to lead the global zero friction coatings market.

Direct Sales Channel Leads with 46.5% Share Through Custom Formulations and Bulk Contracts

The direct sales segment dominates the zero friction coatings market by sales channel with a 46.5% market share in 2025, supported by strong demand from large-scale industrial manufacturers and OEMs. Within the industrial coatings and tribology solutions market, sectors such as automotive, aerospace, and medical device manufacturing require customized zero-friction coating formulations, with validated wear life, coefficient of friction, and performance under extreme conditions. Direct supplier relationships enable precise formulation development, testing, and quality assurance, ensuring optimal results for critical components. Additionally, high-volume manufacturers of fasteners, bearings, and sealing systems secure bulk supply agreements directly with coating material providers, benefiting from consistent batch quality, cost efficiency, and supply reliability. This combination of technical collaboration, customization, and volume procurement reinforces the dominance of direct sales in the global zero friction coatings market supply chain.

Competitive Landscape Analysis of the Zero Friction Coatings Market

Oerlikon Balzers Leads DLC Zero Friction Coatings for Aerospace and Machining

Oerlikon Balzers is strengthening its leadership in the zero friction coatings market through its INSPIRA carbon platform, which uses S3p plasma technology to deposit dense, ultra-low-friction DLC coatings. In April 2026, the company expanded operations in Querétaro, Mexico, adding capacity for aerospace honeycomb structures and turbine coatings amid a 20% surge in North American aerospace demand. Its BALINIT® series, especially BALINIT OPTURA, remains a benchmark for high-load machining, reducing friction-related tool heat by 25%. Backed by resilient Surface Solutions results and a CHF 350 million bond placement, Oerlikon is investing in IIoT-enabled coating platforms.

Henkel Advances PFAS-Free Anti-Friction Coatings for Automotive Electronics and EVs

Henkel AG & Co. KGaA is expanding in the zero friction coatings market through PFAS-free innovation and automotive-focused surface technologies. In April 2026, the company launched Loctite AF 8810 and 8812, anti-fingerprint and zero-friction coatings for automotive touchscreens and plastic lenses. Its expanded Bonderite® dry film lubricant portfolio includes water-based grades for EV e-axles and gearbox components, targeting the automotive sector’s 35% share of zero-friction coating demand. Henkel reported FY2025 sales of €20.5 billion, with Adhesive Technologies achieving 16.7% adjusted return on sales. AI-driven formulation supports fluorine-free coatings that meet OEM Net-Zero 2030 targets while maintaining 9H hardness.

Chemours Maintains Fluoropolymer Coating Leadership in Chemical Processing Applications

The Chemours Company remains a major player in zero friction coatings, supported by its refreshed Teflon® Industrial Coatings portfolio and shift toward PFAS-reduced formulations. Its 2026 flagship fluoropolymer lines deliver an ultra-low coefficient of friction below μ<0.05, serving industrial fasteners, food processing equipment, and high-performance mechanical components. Chemours’ vertical integration in fluorochemistry helps stabilize PTFE and FEP coating supply despite broader specialty chemical price increases. The company dominates the chemical processing industry, where zero-friction coatings protect valves and pumps handling corrosive media at temperatures above 260°C, reinforcing its strength in extreme-service industrial applications.

Trelleborg Drives Low-Friction Sealing Technologies for Robotics and Medical Devices

Trelleborg AB is advancing the zero friction coatings market through specialized seal coatings and smart surface treatments. In 2026, it commercialized Turcon® Roto L, a rotary seal coating that eliminates startup torque in hydraulic systems and improves machine energy efficiency by 5–8%. Its Seal-Glide® nanoscale treatment reduces friction in elastomeric seals by up to 80%, targeting medical device and pharmaceutical packaging applications. Trelleborg also introduced reduced-carbon-footprint EPDMs that combine bio-sourced elastomers with low-friction surfaces, cutting Scope 3 emissions by 20%. Its Cognitive Sealing initiative integrates sensors with coated parts for predictive maintenance in robotic assembly lines.

Bodycote Expands Zero Friction Surface Hardening Through Kolsterising Technology

Bodycote PLC is strengthening its position in the zero friction coatings market through acquisitions and specialist surface technologies. In January 2026, the company acquired Spectrum Thermal Processing, expanding North American capacity for S3P specialty stainless steel processes. Bodycote reported trailing 12-month revenue of USD 958 million as of December 2025, while its Specialist Technologies segment grew 18%, outperforming traditional heat treatment. Its Kolsterising® technology hardens stainless steel surfaces without compromising corrosion resistance, making it valuable for medical implants and marine hardware. In 2026, Bodycote patented a low-temperature annealing method that adds low-friction properties to cold-deformed components without dimensional distortion.

China’s EV-Led Expansion and Regulatory Push Accelerating Zero Friction Coatings Adoption

China remains the dominant force in the zero friction coatings market, driven by stringent environmental regulations and its leadership in electric vehicle (EV) manufacturing. The implementation of GB 4806.10-2025 is redefining safety requirements for food-contact coatings, significantly impacting traditional PTFE-based systems and accelerating the adoption of advanced, eco-friendly alternatives. Government initiatives promoting low-VOC and water-based lubrication systems are further strengthening the shift toward sustainable zero friction coatings.

Industrial growth is strongly tied to infrastructure and advanced manufacturing. The country’s “New Infrastructure” program is increasing demand for friction-reducing coatings in mechanical components used in 5G base stations. Technological innovation is also advancing, with high-precision coating techniques achieving sub-micron thickness accuracy for battery electrode production. China’s EV ecosystem is a major demand driver, where zero friction coatings play a critical role in reducing noise, vibration, and wear in motor components. Additionally, expansion of industrial clusters dedicated to dry lubricant technologies is enhancing production capabilities and reinforcing China’s global leadership in high-performance coating solutions.

United States: Semiconductor Growth and Clean-Label Coating Innovation

The United States zero friction coatings market is evolving rapidly, supported by strong investments in semiconductor manufacturing and energy transition technologies. Government initiatives such as the Inflation Reduction Act are encouraging the modernization of coating processes, promoting the adoption of low-emission, high-performance friction-reducing systems. Additionally, funding from the CHIPS and Science Act is driving the deployment of advanced coating equipment for semiconductor packaging applications.

Regulatory developments are reshaping product innovation, particularly with the phase-out of PFAS-based materials, prompting the development of safer alternatives for aerospace and medical applications. Technological advancements in AI-driven defect detection are enhancing coating precision and quality control in roll-to-roll manufacturing processes. The hydrogen economy is also emerging as a key application area, with specialized coatings being used in fuel cell components to improve efficiency and durability. Strategic investments by major manufacturers are further supporting the growth of advanced coating technologies across automotive, electronics, and energy sectors.

Germany: Circular Economy and Advanced Friction-Reducing Technologies

Germany continues to lead in sustainable zero friction coating technologies, driven by its focus on circular economy principles and advanced material innovation. The development of bio-based polyurethane dispersions is improving coating performance while reducing environmental impact, aligning with strict EU regulatory frameworks. These innovations are particularly relevant in industrial applications where durability and sustainability are critical.

Technological advancements in Germany include the development of self-healing coatings that can repair surface damage, extending the lifespan of industrial components. The adoption of robotic application systems is improving precision and efficiency in coating processes. Germany is also a leader in renewable energy applications, where friction-reducing coatings are used in wind turbine components to enhance performance and reduce maintenance requirements. Regulatory alignment with REACH is driving the elimination of hazardous substances, further accelerating the transition toward environmentally friendly coating solutions.

Japan: Nanotechnology Integration and High-Precision Coating Applications

Japan’s zero friction coatings market is characterized by its focus on nanotechnology and high-precision engineering. The development of nano-ceramic coatings with extremely low coefficients of friction is enabling advanced applications in electronics and next-generation communication technologies. These coatings are essential for maintaining performance in high-speed, high-precision manufacturing environments.

Innovation extends to the development of ultra-thin coating technologies capable of achieving consistent sub-micron thickness, supporting applications in flexible displays and organic photovoltaics. Government support for advanced manufacturing technologies is accelerating the adoption of next-generation coating systems. Japan is also investing in smart coatings with integrated sensing capabilities, enabling real-time monitoring of coating performance. These advancements position Japan as a leader in high-value, precision-driven coating applications.

India: Manufacturing Localization and Emerging High-Growth Applications

India is rapidly emerging as a key market for zero friction coatings, driven by government initiatives aimed at strengthening domestic manufacturing capabilities. Programs such as the Production Linked Incentive (PLI) scheme are boosting demand for advanced coating technologies in battery manufacturing and electronics production. Significant investments in semiconductor manufacturing are further accelerating the adoption of specialized friction-reducing coatings.

Infrastructure development is supporting the growth of local supply chains, with the establishment of chemical parks dedicated to the production of high-purity raw materials. The medical device sector is also contributing to demand, with increasing adoption of low-friction coatings in high-precision applications such as catheters and stents. Strategic collaborations between global companies and local manufacturers are enhancing technology transfer and accelerating market growth. These developments highlight India’s transition toward becoming a regional hub for advanced coating technologies.

South Korea: High-Performance Coatings for Battery and Electronics Applications

South Korea is leveraging its strengths in electronics and shipbuilding to drive innovation in the zero friction coatings market. The development of advanced coating technologies, including dual-layer coating processes, is enabling improved performance in EV battery applications. These innovations are critical for enhancing energy density and operational efficiency in next-generation battery systems.

Government initiatives supporting the battery and semiconductor industries are accelerating the adoption of eco-friendly coating technologies. Investments in research and development are driving the creation of high-performance coatings capable of withstanding extreme environmental conditions. South Korea’s leadership in display technologies is also contributing to demand for specialized coatings used in polarizing films. Additionally, regulatory measures aimed at reducing emissions are encouraging the transition toward sustainable coating solutions, reinforcing the country’s position in high-tech manufacturing.

Italy: Precision Engineering and Specialty Coating Innovation

Italy is a key player in the zero friction coatings market, particularly in high-value applications requiring precision and aesthetic quality. The country’s expertise in specialty coatings is evident in the development of advanced powder coatings designed for small-batch, high-performance applications. These coatings are widely used in industries such as automotive, medical devices, and luxury manufacturing.

Technological advancements are focused on creating coatings that combine functionality with aesthetic appeal, such as ultra-matte finishes that offer both durability and a premium tactile experience. Regulatory frameworks promoting environmentally friendly coatings are driving the adoption of waterborne technologies across industrial sectors. Investments in automated manufacturing systems are enhancing production efficiency and enabling precise application of advanced coatings. Italy’s focus on high-end applications, including luxury automotive interiors and specialized industrial components, underscores its leadership in precision coating technologies.

Zero Friction Coatings Market Report Scope

Zero Friction Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.2 Billion

|

|

Market Size (2032)

|

$1.8 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Type (Molybdenum Disulfide, Polytetrafluoroethylene, Tungsten Disulfide, Graphite based, Ceramic Composites, Polymer based, Nano-coatings), By Formulation (Solvent-based Coatings, Water-based Coatings, Powder-based Coatings, Dispersion), By Application (Bearings, Automotive Parts, Power Transmission Items, Valves and Actuators, Fasteners and Connectors, Medical Devices, Aerospace Assemblies), By End-User Industry (Automotive and Transportation, Aerospace and Defense, General Industrial Engineering, Energy, Food and Healthcare, Electronics and Electrical), By Substrate Type (Metals and Alloys, Polymers and Plastics, Ceramics, Composites), By Sales Channel (Direct Sales, Specialized Industrial Distributors, Contract Coating Service Providers, Online B2B Marketplaces),

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Chemours Company, DuPont de Nemours, Inc., PPG Industries, Inc., Klüber Lubrication, Daikin Industries, Ltd., Henkel AG and Co. KGaA, Akzo Nobel N.V., Whitford Worldwide, Bechem, Oerlikon Balzers, ASV Multichemie Pvt. Ltd., Endura Coatings, Poeton Industries Ltd., IKV Tribology Ltd., Hauzer Techno Coating B.V., ,

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Zero Friction Coatings Market Segmentation

By Type

- Molybdenum Disulfide

- Polytetrafluoroethylene

- Tungsten Disulfide

- Graphite based

- Ceramic Composites

- Polymer based

- Nano-coatings

By Formulation

- Solvent-based Coatings

- Water-based Coatings

- Powder-based Coatings

- Dispersion

By Application

- Bearings

- Automotive Parts

- Power Transmission Items

- Valves and Actuators

- Fasteners and Connectors

- Medical Devices

- Aerospace Assemblies

By End-User Industry

- Automotive and Transportation

- Aerospace and Defense

- General Industrial Engineering

- Energy

- Food and Healthcare

- Electronics and Electrical

By Substrate Type

- Metals and Alloys

- Polymers and Plastics

- Ceramics

- Composites

By Sales Channel

- Direct Sales

- Specialized Industrial Distributors

- Contract Coating Service Providers

- Online B2B Marketplaces

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Zero Friction Coatings Industry

- The Chemours Company

- DuPont de Nemours, Inc.

- PPG Industries, Inc.

- Klüber Lubrication

- Daikin Industries, Ltd.

- Henkel AG & Co. KGaA

- Akzo Nobel N.V.

- Whitford Worldwide

- Bechem

- Oerlikon Balzers

- ASV Multichemie Pvt. Ltd.

- Endura Coatings

- Poeton Industries Ltd.

- IKV Tribology Ltd.

- Hauzer Techno Coating B.V.

*- List not Exhaustive