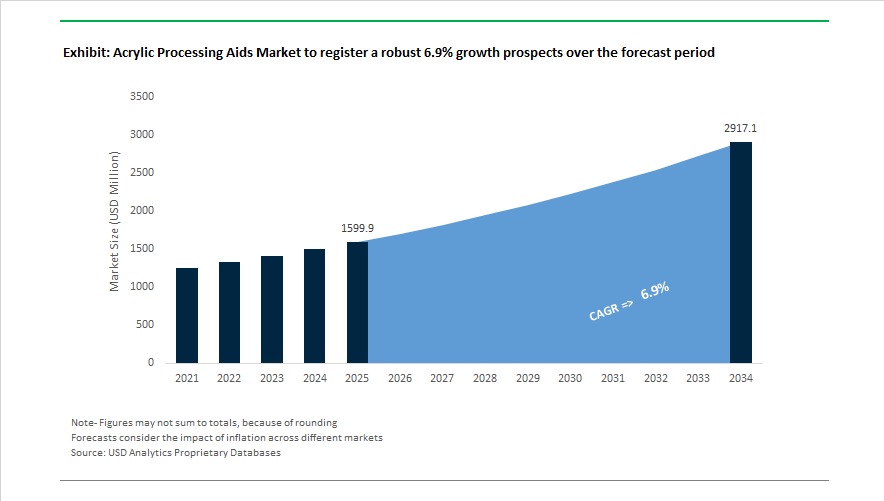

Market Overview: Acrylic Processing Aids Market Growth to $2.9 Billion by 2034 Fueled by PFAS-Free Transition and Structural Portfolio Shifts

The global acrylic processing aids market is on a sustained expansion path, projected to grow from $1,599.9 Million in 2025 to $2,916.7 Million by 2034, registering a 6.9% CAGR. Growth is being driven by accelerating substitution of fluoropolymer-based additives, rising PVC consumption in construction and infrastructure, and increasing adoption of high-performance acrylic modifiers in packaging, automotive, and medical plastics. Processing aids—critical for melt flow improvement, surface finish enhancement, impact strength, and extrusion stability—are becoming strategically important as polymer processors face tighter environmental regulations, higher energy costs, and demand for precision-grade materials. The competitive environment is shifting from volume-driven commodity additives toward technology-intensive, regulatory-compliant, and sustainability-aligned acrylic copolymer solutions, positioning specialty processing aids as a high-value segment within the broader polymer additives industry.

A major inflection point occurred in January 2025, when Kaneka Corporation restructured its vinyl resin and additive production system to optimize supply for its Kane Ace PA acrylic processing aid line, strengthening its position in Asian infrastructure polymers. Consolidation momentum intensified in March 2025 as Nippon Paint Holdings completed its $4.4 billion acquisition of AOC Resins, expanding upstream access to acrylic-based additive technologies for composite materials. Portfolio realignment continued into December 2025, when Arkema announced the divestment of its global acrylic processing aids and impact modifiers business (AIMPA scope and MBS copolymers) to Praana, retaining only U.S. operations to focus on higher-value specialties. Completion of this transaction—covering the Vlissingen facility—is expected in March 2026, establishing Praana (owner of Galata Chemicals) as a major force in PVC additives. Earlier downstream integration by Arkema through the May 2024 acquisition of Dow’s flexible packaging adhesives business reinforced its position in packaging-linked acrylic additive demand.

Regulatory disruption is simultaneously catalyzing product innovation. In September 2025, Dow introduced DOWSIL 5-1050, a PFAS-free silicone processing aid targeting film extrusion, directly responding to tightening global restrictions on fluorinated additives. That same month, Ampacet launched PROFLOW 1611, a non-fluorinated processing aid for high-heat extrusion compatible with acrylic systems. Reformulation urgency escalated as the EU Packaging and Packaging Waste Regulation moved toward a PFAS ban effective August 2026, triggering rapid migration to acrylic and silicone-based alternatives. Sustainability-led product engineering also advanced in mid-2025 when Akdeniz Kimya rolled out high-efficiency acrylic aids enabling lower processing temperatures and reduced energy intensity in PVC extrusion. Meanwhile, supply-side optimization in China accelerated in late 2025 as Shandong Ruifeng Chemical prioritized RFA and RFB high-end acrylic aid series to reduce reliance on imported medical and electronic-grade additives. Strategic repositioning continued in January 2026, when Mitsubishi Chemical Corporation shifted toward “technology premium” METABLEN P-series processing aids, targeting semiconductor and medical-grade plastics—underscoring the industry’s migration from scale to specialization.

Strategic Market Trends and High-Potential Growth Opportunities in the Acrylic Processing Aids Market

Market Trend: Capacity Expansion Targeting Bio-based and Specialty Acrylic Processing Aids

A defining development in the acrylic processing aids market is the industry-wide pivot toward bio-attributed and low-carbon APA grades driven by downstream pressure from PVC pipe, profile extrusion, and construction material manufacturers aiming to reduce product carbon footprints. Regulatory forces—including carbon taxes, green building mandates, and Scope 3 disclosure requirements—have accelerated a shift where buyers are actively prioritizing additive suppliers with ISCC+ certifications and low-emission value chains.

Arkema's early 2025 certification of global acrylic monomer and additive facilities in Carling (France) and Zwickau (Germany) signals the commercial maturity of mass balance–integrated APA production. The launch of the ENCOR bio-based acrylic dispersion line, featuring 30% bio-content and 40% reduced CO₂ impact, further reinforces the structural move toward specialty additives replacing commodity grades. Reinforcing this strategic shift, Arkema is divesting standard APA and impact modifier divisions, worth €44 million in 2024, to free capital for high-performance and circular-economy–linked acrylic solutions. This trend indicates an irreversible industry movement toward performance chemistry backed by environmental certification rather than volume-led competition.

Market Trend: Supply Chain Regionalization and Local Production of Acrylic Processing Aids

Post-pandemic lessons, volatile freight costs, and geopolitical fragmentation are pushing chemical producers to regionalize APA production, particularly close to PVC and construction markets. BASF’s commissioning of a new dispersions line in Dilovası, Türkiye, creates a blueprint for future investments: on-continent production, 100% green electricity integration, and short-lead logistics to Türkiye, the Middle East, and North Africa.

Localized APA facilities are increasingly decentralized to ensure just-in-time industrial delivery, especially for segments that are expanding—such as construction profiles, medical PVC, and flooring. Producers like Mitsubishi Chemical are expanding footprints across Southeast Asia to insulate supply chains from the 2022–2023 logistics crisis. Regional APA manufacturing is becoming a competitive differentiator, improving pricing stability, allowing custom formulation for climate-driven applications (heat-resistant, low-VOC grades), and helping end-users qualify for regional green-building and low-carbon construction certifications.

Market Opportunity: Acrylic Processing Aids as Enablers for Recycler-Grade PVC and Circular Polymer Value Chains

One of the most transformative growth avenues lies in APAs enabling high-recyclate PVC formulations, shifting their role from “optional performance enhancers” to mandatory enablers of circular PVC ecosystems. Countries including India are mandating minimum recycled content in PVC-based construction and packaging materials beginning April 2025 under updated Plastic Waste Management Rules, creating exponential demand for processing aids that stabilize poor-quality recyclate.

Technical evaluations of grades such as PARALOID K-175 show recyclate melt-fusion enhancement of 25% to 30 percent, enabling processors to increase post-consumer waste content without sacrificing tensile strength, gloss, or surface finish. Emerging use cases include upcycling reclaimed polyvinyl butyral (PVB) from automotive glass into vinyl flooring, where specialty acrylic aids prevent surface indentation and reduce polymer stickiness. The long-term implication: APAs will be contractually embedded in recycling-driven manufacturing rather than used only in premium applications, unlocking recurring revenue channels tied to recycling quotas and ESG-linked procurement.

Market Opportunity: Acrylic Processing Aids as Critical Functional Additives for Lithium-Ion Battery Manufacturing

The most technically advanced and high-margin opportunity area is the use of APAs within lithium-ion battery manufacturing, where they support binder performance, separator coating quality, and solvent-free electrode production. Modified acrylic binders (PAANa) for graphite anodes have demonstrated laboratory durability of 360 charge-discharge cycles at 1C, compared with 192 cycles for traditional commercial binders, representing a clear lifetime-extension advantage for EV batteries.

Arkema’s Incellion Sp acrylic-based binder platform is gaining adoption as a thermal-stabilizing safety component for separator coatings to prevent deformation in high-temperature or high-energy-density environments. Meanwhile, the transition toward aqueous, solvent-free electrode manufacturing, replacing N-methyl-2-pyrrolidone and PVDF systems, is amplifying demand for acrylic latex binders that provide rheology control and adhesion. As EV cell makers scale gigafactory capacity, APAs could evolve from a supporting additive to a strategic material class that enables reduced cost-per-kWh, improved energy density, and safer charging cycles, positioning APA producers to gain long-term supply agreements within the battery supply chain.

Acrylic Processing Aids Market Share and Segmentation Insights

Market Share by Type: Multi-Functional Acrylic Processing Aids Consolidate Leadership

Multi-functional acrylic processing aids dominate the global acrylic processing aids market with an estimated 45% share in 2025, reflecting PVC processors’ growing preference for single-additive systems that deliver both internal fusion promotion and external metal release. This dual functionality reduces inventory complexity, minimizes dosing errors, and improves production efficiency across rigid and flexible PVC applications. Internal processing aids retain a strong secondary position due to their critical role in achieving uniform melt flow in rigid PVC pipes, fittings, and profiles, where consistent fusion directly impacts mechanical performance. External processing aids hold the smallest market share but remain indispensable for high-gloss finishes, preventing melt fracture in thin films and complex extrusion profiles. However, reliance on standalone external aids is gradually declining as next-generation multi-functional acrylic chemistries continue to improve surface quality while maintaining extrusion stability, reshaping additive selection strategies across packaging and construction-grade PVC formulations.

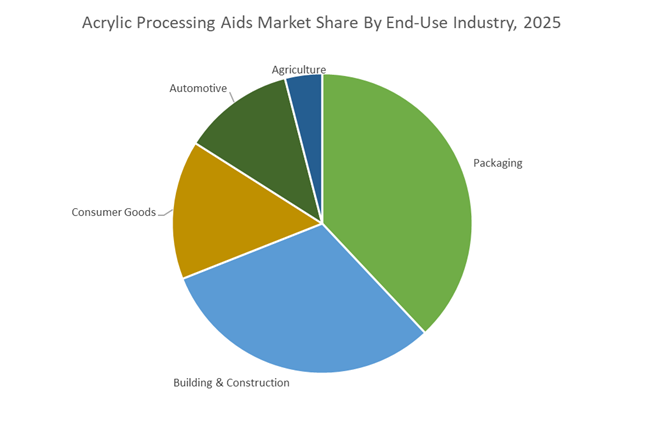

Market Share by End-Use Industry: Packaging Leads While Construction Anchors Volume Stability

Packaging represents approximately 38% of acrylic processing aids consumption in 2025, making it the largest end-use segment. Growth is driven by the transition from rigid PVC to foamed PVC sheets in food packaging applications such as fruit punnets and meat trays, where high-performance processing aids are essential to control cell structure while preserving mechanical strength during lightweighting. Building & construction ranks second, supported by steady infrastructure investment in water pipes and window profiles, even as higher interest rates moderated residential housing starts in 2024–2025. Automotive shows moderate expansion through PVC underbody coatings and interior trim, although the shift toward electric vehicles slightly tempers growth due to reduced PVC wiring insulation. Agriculture holds the smallest share, limited to irrigation tubing and greenhouse films, with high price sensitivity encouraging lower dosages or non-acrylic alternatives.

Acrylic Processing Aids Market Competitive Landscape: Innovation, Core-Shell Technology, and Circular PVC Processing

The Acrylic Processing Aids Market is defined by high molecular weight ACR modifiers, core-shell polymer technology, and process optimization solutions for rigid PVC, foamed PVC, WPC, and engineering resins. Competition centers on fusion efficiency, melt strength enhancement, plate-out reduction, and improved recyclability. Leading manufacturers are leveraging vertical integration in MMA and acrylic resin production, expanding capacity in Asia and Europe, and developing bio-polymer compatible processing aids aligned with circular economy mandates. Strategic portfolio rationalization and sustainability-driven innovation are reshaping supplier positioning across construction, automotive lightweighting, and advanced extrusion markets.

Dow Inc. drives ultra-high molecular weight PVC processing performance with PARALOID™ leadership

Dow remains a dominant force in acrylic processing aids through its legacy PARALOID™ and SURECEL™ series, engineered for ultra-high molecular weight performance in rigid and foamed PVC applications. These additives enable high-output extrusion of PVC window profiles, siding, and lightweight foam-core pipes by enhancing fusion consistency and melt strength. In 2024–2025, Dow streamlined its portfolio by divesting its flexible packaging adhesives business to Arkema S.A., sharpening its focus on high-value plastic additives and downstream materials science. Backed by global manufacturing operations across 31 countries and integration with in-house resin production, Dow ensures consistent additive quality and technical reliability worldwide.

Arkema S.A. advances high-speed extrusion solutions with Plastistrength® technology

Arkema positions its acrylic additives as high-performance solutions for complex polymer blends, led by the Plastistrength® range designed to eliminate surface defects and prevent plate-out during high-speed PVC extrusion. The company has developed next-generation grades optimized for bio-polymers such as PLA and recycled PVC, aligning with green chemistry and circular plastics initiatives. The acquisition of Dow’s laminating adhesives business in 2024 significantly strengthened Arkema’s additives footprint across packaging and construction value chains. Strategically transitioning toward a pure specialty materials model, Arkema prioritizes additives that enhance recyclability, improve processing stability, and support sustainable polymer systems.

Kaneka Corporation pioneers core-shell PVC modifiers under the KANE ACE™ platform

Kaneka Corporation is a recognized leader in core-shell polymer technology, with its KANE ACE™ PA series engineered to drastically reduce fusion time and enhance PVC melt elasticity. These high-functionality processing aids are widely used in premium applications such as acrylic capping for weather-resistant outdoor building materials. Through its Green Planet™ initiative, Kaneka integrates biodegradable polymer solutions to address microplastic concerns while leveraging biotechnology and advanced polymer synthesis expertise. The company’s hybrid additives function both as lubricants and processing aids, providing formulation efficiency in Asian and North American construction markets where high-aesthetic PVC applications dominate demand.

Mitsubishi Chemical Group expands METABLEN™ processing aids into engineering resin applications

Mitsubishi Chemical Group focuses on high-efficiency additives under the METABLEN™ brand, extending beyond PVC into engineering resins for automotive and electronics. With full-stack integration from methyl methacrylate monomers to finished P-type processing aids, the company ensures raw material security and formulation control. Recent expansion of METABLEN™ P-1901 reactive agents enables chain extension in recycled plastics, restoring mechanical performance in circular polymer systems. Key applications include automotive interiors, electronic housings, and high-clarity sheet extrusion where optical transparency is critical. Strategically, Mitsubishi Chemical is pivoting toward value-added specialty chemicals targeting EV mobility and 5G-enabled electronics.

LG Chem Ltd. scales next-generation ACR production for global construction growth

LG Chem has rapidly expanded as a leading supplier of acrylic processing aids to India and Southeast Asia’s booming construction markets. The PA-900 series is recognized for strong cost-to-performance advantages in pipe and profile extrusion. The company is investing heavily in next-generation SAP and ACR production facilities in South Korea to meet rising 2026 demand for high-performance additives in global building materials. LG Chem is also expanding its LETZero platform to include mass-balanced bio-feedstock processing aids, reinforcing its sustainability roadmap. Strong vertical integration with large-scale petrochemical complexes enables rapid commercialization and competitive supply stability.

Shandong Ruifeng Chemical leverages scale leadership in ACR processing aids for PVC foam and WPC

Shandong Ruifeng Chemical stands as one of the largest independent ACR processing aid producers globally, representing China’s scale-driven manufacturing advantage. Its LP-series, including LP-20, LP-55, and LP-90, features ultra-high molecular weight additives tailored for PVC foam boards and rigid profiles. The company is aggressively expanding exports to Europe and North America with competitively priced technical-grade powders. Ruifeng plays a critical role in the WPC industry and rigid foam board production for construction applications. Its core strengths lie in high-volume capacity, formulation flexibility, and responsiveness to the large domestic Chinese infrastructure market.

China Acrylic Processing Aids Market: Infrastructure-Led Volume Growth and Recycled PVC Compliance

China remains the largest volume-driven market for acrylic processing aids, supported by sustained infrastructure spending and rapid industrial standardization. In 2025, the government retained an annual ceiling of approximately CNY 3.85 trillion (USD 570+ billion) for new infrastructure bonds, directly stimulating demand for APA-enhanced PVC pipes, window profiles, siding systems, and foam boards. This has reinforced the use of high-molecular-weight acrylic processing aids to improve melt elasticity, surface finish, and dimensional stability in rigid PVC applications. Parallelly, China’s aggressive 5G rollout—surpassing 792,000 base stations by 2025—has accelerated the need for specialized wire and cable jacketing compounds, where APAs are critical for preventing melt fracture during high-speed extrusion.

On the supply side, domestic manufacturers such as Shandong Ruifeng Chemical and Shandong Rike Chemical have expanded production capacity to meet rising regional demand, particularly for PVC foam boards used in signage and interior construction. Export strategies are also evolving, with Chinese producers targeting Southeast Asia and the Pacific through customized APA masterbatch solutions optimized for local extrusion conditions. Regulatory standardization under the Ministry of Industry and Information Technology (MIIT) is playing a decisive role; new quality benchmarks for recycled PVC are pushing processors to increase APA usage to maintain melt strength and surface quality in high-recycled-content formulations. Technologically, the market is shifting away from conventional internal lubricants toward multifunctional acrylic copolymers that simultaneously enhance gloss, impact resistance, and processing stability—especially in automotive interior components.

India Acrylic Processing Aids Market: Recycling Mandates, Localization, and Infrastructure-Driven Processing Demand

India’s acrylic processing aids market is entering a high-growth phase, underpinned by regulatory enforcement, financial incentives, and rapid expansion of packaging and infrastructure sectors. The June 2025 amendments issued by the Ministry of Environment, Forest and Climate Change mandate traceability and recycled content targets across plastic products, significantly increasing the need for advanced APAs capable of processing heterogeneous and difficult-to-extrude recycled polymer streams. These requirements are particularly relevant for rigid PVC and flexible packaging, where maintaining melt strength and surface consistency is increasingly challenging.

Government-backed financial support is accelerating technology upgrades. Under the Plastic Industry Subsidy 2025 scheme, the Government of India has committed ₹3,000 crore, offering 25–30% capital subsidies to MSMEs for adopting energy-efficient extrusion machinery that relies on precision-formulated acrylic processing aids. Demand is further amplified by India’s packaging sector, projected to reach USD 204.81 billion by 2025, driving large-scale consumption of APAs in blown and cast film extrusion. Localization initiatives under the Aatmanirbhar Bharat program have enabled players such as Indofil Industries to expand domestic APA portfolios, including K-series grades like K-120 ND, reducing reliance on imported additives. Infrastructure development under the National Infrastructure Pipeline continues to boost CPVC and UPVC pipe production, where APAs are essential to prevent surface defects such as “shark skin.” Skill development programs launched with Central Institute of Petrochemicals Engineering and Technology (CIPET) are further enhancing compounding efficiency through digitalization and process control training.

United States Acrylic Processing Aids Market: Regulatory Substitution and High-Efficiency Extrusion

The United States acrylic processing aids market is being reshaped by trade policy, chemical regulation, and advanced manufacturing practices. Elevated tariffs on chemical imports in 2025 have strengthened demand for North America–sourced acrylic resins and additives, favoring domestic suppliers such as Dow and 3M. Simultaneously, the accelerated phase-out of PFAS-based processing aids at state and federal levels has triggered a rapid transition toward PFAS-free acrylic and silicone-based alternatives, particularly in film packaging applications.

Compliance with food contact regulations is another defining factor. New APA formulations are undergoing extensive validation against FDA 21 CFR 174.5 standards to support high-barrier food packaging films, increasing development costs but raising entry barriers for lower-quality imports. From a processing standpoint, US compounders are adopting Industry 4.0-enabled smart dosing systems, enabling up to 15% reductions in APA loading while maintaining throughput and surface quality in large-diameter pipe extrusion. Sustainability-oriented R&D is gaining momentum, with investments in bio-derived acrylic acid pathways supporting the emergence of “green” acrylic processing aids aligned with circular economy goals. Additionally, the automotive transition toward electrification is expanding APA usage in lightweight thermoplastic elastomer seals for EV battery housings, where dimensional precision and thermal stability are critical.

Germany Acrylic Processing Aids Market: PFAS-Free Innovation and Energy-Efficient PVC Processing

Germany represents the technological and regulatory epicenter of acrylic processing aid innovation in Europe. Alignment with the EU Green Deal and the Packaging and Packaging Waste Regulation (PPWR) has driven the adoption of next-generation APA grades that preserve recyclability without leaving harmful residues. The K 2025 trade fair in Düsseldorf highlighted this transition, serving as the launch platform for multiple PFAS-free acrylic-based processing aids designed for high-speed polyolefin and PVC extrusion.

Energy efficiency is a central theme in the German market. Chemical producers are investing in APAs that enable lower processing temperatures for rigid PVC, directly reducing energy consumption and carbon emissions for window profile and construction material manufacturers. High-purity requirements are also shaping demand, particularly for medical and healthcare packaging, where low-extractable acrylic processing aids are becoming mandatory. Germany remains the primary European R&D hub for molecular architecture optimization in APAs, allowing ultra-high-speed extrusion without melt fracture—a key differentiator for export-oriented machinery and profile manufacturers operating under tight tolerance regimes.

South Korea Acrylic Processing Aids Market: Electronics, Batteries, and Precision Polymer Engineering

South Korea’s acrylic processing aids market is increasingly specialized, with strong alignment to batteries, electronics, and advanced materials. LG Chem has intensified R&D efforts in acrylic-based binders and processing aids tailored for battery separator films, a critical component in improving the thermal stability and lifecycle performance of lithium-ion batteries. This positions APAs as enablers of South Korea’s broader EV and energy storage strategy.

In parallel, demand for high-clarity acrylic sheets used in display manufacturing and semiconductor clean-room infrastructure is driving the use of ultra-pure acrylic processing aids. South Korean producers are leveraging Free Trade Agreements to export high-performance additive series to North American automotive markets, particularly for precision-molded interior and exterior components. Technological advancement is further reinforced by the deployment of AI-driven polymerization control systems, enabling tighter molecular weight distributions in APAs for niche injection molding and specialty extrusion applications, strengthening Korea’s reputation for high-consistency, application-specific processing aids.

Comparative Snapshot: Country-Level Dynamics in Acrylic Processing Aids

Acrylic Processing Aids Market County Level Snapshot

|

Country

|

Primary Demand Drivers

|

Strategic Impact on APA Market

|

|

China

|

Infrastructure bonds, 5G rollout, recycled PVC standards

|

High-volume growth, export-oriented masterbatch innovation

|

|

India

|

Recycling mandates, MSME subsidies, packaging expansion

|

Localization, rapid adoption of advanced APAs

|

|

United States

|

PFAS phase-out, food contact compliance, Industry 4.0

|

High-performance, sustainable APA development

|

|

Germany

|

EU Green Deal, energy efficiency, PFAS-free regulations

|

Technology leadership and premium-grade APAs

|

|

South Korea

|

Battery separators, electronics, AI-driven processing

|

Precision additives for high-tech applications

|

Acrylic Processing Aids Market Report Scope

Acrylic Processing Aids Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1599.9 Million

|

|

Market Size (2034)

|

$2916.7 Million

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Type (Internal Processing Aids, External Processing Aids, Multi-functional Acrylic Processing Aids), By Polymer Matrix (Polyvinyl Chloride (PVC), Polyethylene (PE), Polypropylene (PP), Engineering Plastics), By Fabrication Process (Extrusion, Injection Molding, Calendering, Thermoforming, Blow Molding), By End-Use Industry (Building & Construction, Packaging, Automotive, Consumer Goods, Agriculture), By Form (Powder, Granules/Beads, Liquid/Emulsion, Masterbatch)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Dow Chemical Company, Arkema S.A., Kaneka Corporation, Mitsubishi Chemical Group, LG Chem Ltd., 3M Company, BASF SE, Clariant AG, Shandong Ruifeng Chemical Co., Ltd., Shandong Rike Chemical Co., Ltd., Indofil Industries Limited, Akdeniz Chemson, Novista Group, WSD Chemical Limited, Pau Tai Industrial Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Acrylic Processing Aids Market Segmentation

By Type

- Internal Processing Aids

- External Processing Aids

- Multi-functional Acrylic Processing Aids)

- By Polymer Matrix (Polyvinyl Chloride (PVC)

- Polyethylene (PE)

- Polypropylene (PP)

- Engineering Plastics

By Fabrication Process

- Extrusion

- Injection Molding

- Calendering

- Thermoforming

- Blow Molding

By End-Use Industry

- Building & Construction

- Packaging

- Automotive

- Consumer Goods

- Agriculture

By Form

- Powder

- Granules/Beads

- Liquid/Emulsion

- Masterbatch

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Acrylic Processing Aids Market

- The Dow Chemical Company

- Arkema S.A.

- Kaneka Corporation

- Mitsubishi Chemical Group

- LG Chem Ltd.

- 3M Company

- BASF SE

- Clariant AG

- Shandong Ruifeng Chemical Co. Ltd.

- Shandong Rike Chemical Co. Ltd.

- Indofil Industries Limited

- Akdeniz Chemson

- Novista Group

- WSD Chemical Limited

- Pau Tai Industrial Corporation

*- List not Exhaustive